Three recent reports (see links below) have suggested that US consumers and businesses pay most of the tariffs imposed by the second Trump administration. The percentage varies from around 86% to 96%. US customs revenue surged by approximately $200 billion in 2025, but this was a tax paid almost entirely by US consumers and businesses. Foreign suppliers largely maintained their (pre-tariff) prices. They took a hit in terms of reduced volumes rather than reduced pre-tariff prices.

The incidence of a tariff between consumers, domestic importers and overseas producers will depend on price elasticities of demand and supply. The following diagram shows a product where the importing country is large enough to have a degree of market power, which will normally be the case with the USA. The greater its buying power, the flatter will be its demand curve, showing that the foreign supplier will have little influence on the price. With no tariff, the equilibrium price paid by importers will be at point a, where demand equals supply. Q1 would be imported at a price of P1.

Imposition of a tariff will shift the supply curve upwards by the amount of the tariff. The new equilibrium price paid by importers will be at point b, where the new supply curve crosses the demand curve. Importers thus now pay a post-tariff price of P2: an effective rise in price of P2 minus P1. Foreign exporters receive P3, which is what they are paid by importers after the tariff has been paid.

The consumer price will be above P2 as that includes a mark-up by US businesses on top of the price they pay to import the product. Importers may bear some of the increase in price and not pass the full amount onto consumers, depending on competition and their ability to absorb cost increases.

President Trump argued that there would be very little rise in price from the tariffs and that overseas suppliers would bear the brunt of the tariffs. Indeed, recently he has argued that this must be the case as US inflation has been falling. In response, critics maintain that the rate of inflation would have fallen more without the tariffs and that current prices would be lower than they are. Also, if US importing firms or retailers bear some of the increased cost, even though this helps to dampen the price rise, their lower profits could damage investment and employment.

The Reports

The first report is from the New York Fed (one of the regional branches of the Federal Reserve Bank). It examines the effect of tariffs imposed in 2025, over three periods: (i) January to August, (ii) September to October, and (iii) November. In the first period, 94% of the tariffs were paid by US importers and 6% by foreign exports; in the second period, the figures were 92% and 8% and in the third period, 86% and 14%.

The second report is The Budget and Economic Outlook: 2026 to 2036 from the Congressional Budget Office. Box 2-1 notes that, as of November 2025, ‘the effective tariff rate was about 13 percentage points higher than the roughly 2 percent rate on imports in 2024’. Its analysis suggests that 95% of the tariffs will be borne by importers. Of these higher import prices, 30% will be borne by US businesses, largely through reduced profit margins, and 70% by consumers through higher prices. This will also allow many businesses which produce goods that compete with foreign imports to ‘increase their prices because of the decline in competition from abroad and the increased demand for tariff-free domestic goods’.

The third report is from the Kiel Insitut. In its Policy Brief, Americaʼs Own Goal: Who Pays the Tariffs?, it finds that US importers and consumers bear 96% of the cost of the 2025 tariffs, with foreign exporters absorbing only about 4%. It bases it findings on shipment-level data covering over 25 million transactions valued at nearly $4 trillion. This also shows that exports to the USA declined as foreign exporters preferred to reduce volumes rather than absorbing the tariffs.

The tariffs raised some $200 billion in 2025, around 3.8% of Federal tax receipts. But, as we have seen, this was paid largely by US consumers and business. It goes some way to offsetting the annual cut in tax revenues of around $450 to $520 billion per year from the tax cuts, largely to the better off, in Trump’s ‘One Big Beautiful Bill’.

Over the decades, economies have become increasingly interdependent. This process of globalisation has involved a growth in international trade, the spread of technology, integrated financial markets and international migration.

When the global economy is growing, globalisation spreads the benefits around the world. However, when there are economic problems in one part of the world, this can spread like a contagion to other parts. This was clearly illustrated by the credit crunch of 2007–8. A crisis that started in the sub-prime market in the USA soon snowballed into a worldwide recession. More recently, the impact of Covid-19 on international supply chains has highlighted the dangers of relying on a highly globalised system of production and distribution. And more recently still, the war in Ukraine has shown the dangers of food and fuel dependency, with rapid rises in prices of basic essentials having a disproportionate effect on low-income countries and people on low incomes in richer countries.

Moves towards autarky

So is the answer for countries to become more self-sufficient – to adopt a policy of greater autarky? Several countries have moved in this direction. The USA under President Trump pursued a much more protectionist agenda than his predecessors. The UK, although seeking new post-Brexit trade relationships, has seen a reduction in trade as new barriers with the EU have reduced UK exports and imports as a percentage of GDP. According to the Office for Budget Responsibility’s November 2022 Economic and Fiscal Outlook, Brexit will result in the UK’s trade intensity being 15 per cent lower in the long run than if it had remained in the EU.

Many European countries are seeking to achieve greater energy self-sufficiency, both as a means of reducing reliance on Russian oil and gas, but also in pursuit of a green agenda, where a greater proportion of energy is generated from renewables. More generally, countries and companies are considering how to reduce the risks of relying on complex international supply chains.

Limits to the gains from trade

The gains from international trade stem partly from the law of comparative advantage, which states that greater levels of production can be achieved by countries specialising in and exporting those goods that can be produced at a lower opportunity cost and importing those in which they have a comparative disadvantage. Trade can also lead to the transfer of technology and a downward pressure on costs and prices through greater competition.

But trade can increase dependence on unreliable supply sources. For example, at present, some companies are seeking to reduce their reliance on Taiwanese parts, given worries about possible Chinese actions against Taiwan.

Also, governments have been increasingly willing to support domestic industries with various non-tariff barriers to imports, especially since the 2007–8 financial crisis. Such measures include subsidies, favouring domestic firms in awarding government contracts and using regulations to restrict imports. These protectionist measures are often justified in terms of achieving security of supply. The arguments apply particularly starkly in the case of food. In the light of large price increases in the wake of the Ukraine war, many countries are considering how to increase food self-sufficiency, despite it being more costly.

Also, trade in goods involves negative environmental externalities, as freight transport, whether by sea, air or land, involves emissions and can add to global warming. In 2021, shipping emitted over 830m tonnes of CO2, which represents some 3% of world total CO2 emissions. In 2019 (pre-pandemic), the figure was 800m tonnes. The closer geographically the trading partner, the lower these environmental costs are likely to be.

The problems with a globally interdependent world have led to world trade growing more slowly than world GDP in recent years after decades of trade growth considerably outstripping GDP growth. Trade (imports plus exports) as a percentage of GDP peaked at just over 60% in 2008. In 2019 and 2021 it was just over 56%. This is illustrated in the chart (click here for a PowerPoint). Although trade as a percentage of GDP rose slightly from 2020 to 2021 as economies recovered from the pandemic, it is expected to have fallen back again in 2022 and possibly further in 2023.

But despite this reduction in trade as a percentage of GDP, with de-globalisation likely to continue for some time, the world remains much more interdependent than in the more distant past (as the chart shows). Greater autarky may be seen as desirable by many countries as a response to the greater economic and political risks of the current world, but greater autarky is a long way from complete self-sufficiency. The world is likely to remain highly interdependent for the foreseeable future. Reports of the ‘death of globalisation’ are premature!

Explain the law of comparative advantage and demonstrate how trade between two countries can lead to both countries gaining.

What are the main economic problems arising from globalisation?

Is the answer to the problems of globalisation to move towards greater autarky?

Would the expansion/further integration of trading blocs be a means of exploiting the benefits of globalisation while reducing the risks?

Is the role of the US dollar likely to decline over time and, if so, why?

Summarise Karl Polanyi’s arguments in The Great Transformation (see the Daniel W. Drezner article linked below). How well do they apply to the current world situation?

World politicians, business leaders, charities and pressure groups are meeting in Davos at the 2022 World Economic Forum. Normally this event takes place in January each year, but it was postponed to this May because of Covid-19 and is the first face-to-face meeting since January 2020.

The meeting takes place amid a series of crises facing the world economy. The IMF’s Managing Director, Kristalina Georgieva, described the current situation as a ‘confluence of calamities’. Problems include:

Continuing hangovers from Covid have caused economic difficulties in many countries.

The bounceback from Covid has led to demand outpacing supply. The world is suffering from a range of supply-chain problems and shortages of key materials and components, such as computer chips.

The war in Ukraine has not only caused suffering in Ukraine itself, but has led to huge energy and food price increases as a result of sanctions and the difficulties in exporting wheat, sunflower oil and other foodstuffs.

Supply shocks have led to rising global inflation. This will feed into higher inflationary expectations, which will compound the problem if they result in higher prices and wages in response to higher costs.

Central banks have responded by raising interest rates. These dampen an already weakened global economy and could push the world into recession.

Global inequality is rising rapidly, both within countries and between countries, as Covid disruptions and higher food and energy prices hit the poor disproportionately. Poor people and countries also have a higher proportion of debt and are thus hit especially hard by higher interest rates.

Global warming is having increasing effects, with a growing incidence of floods, droughts and hurricanes. These lead to crop failures and the displacement of people.

Countries are increasingly resorting to trade restrictions as they seek to protect their own economies. These slow economic growth.

World leaders at Davos will be debating what can be done. One approach is to use fiscal policy. Indeed, Kristalina Georgieva said that her ‘main message is to recognise that the world must spend the billions necessary to contain Covid in order to gain trillions in output as a result’. But unless the increased expenditure is aimed specifically at tackling supply shortages and bottlenecks, it could simply add to rising inflation. Increasing aggregate demand in the context of supply shortages is not the solution.

In the long run, supply bottlenecks can be overcome with appropriate investment. This may require both greater globalisation and greater localisation, with investment in supply chains that use both local and international sources.

International sources can be widened with greater investment in manufacturing in some of the poorer developing countries. This would also help to tackle global inequality. Greater localisation for some inputs, especially heavier or more bulky ones, would help to reduce transport costs and the consumption of fuel.

With severe supply shocks, there are no simple solutions. With less supply, the world produces less and becomes poorer – at least temporarily until supply can increase again.

Donald Trump has threatened to pull out of the World Trade Organization. ‘If they don’t shape up, I would withdraw from the WTO,’ he said. He argues that the USA is being treated very badly by the WTO and that the organisation needs to ‘change its ways’.

Historically, the USA has done relatively well compared with other countries in trade disputes brought to the WTO. However, President Trump does not like being bound by an international organisation which prohibits the unilateral imposition of tariffs that are not in direct retaliation against a trade violation by other countries. Such tariffs have been imposed by the Trump administration on steel and aluminium imports. This has led to retaliatory tariffs on US imports by the EU, China and Canada – something that is permitted under WTO rules.

Whether or not the USA does withdraw from the WTO, Trump’s threats bring into question the power of the WTO and other countries’ compliance with WTO rules. With the rise in protectionist sentiments around the world, the power of the WTO would seem to be on the wane.

Even if the USA does not withdraw from the WTO, it is succeeding in weakening the organisation. Appeals cases have to be heard by an ‘appellate body’, consisting of at least three judges drawn from a list of seven, each elected for four years. But the USA has the power to block new appointees – and has done so. As Larry Elliott states in the first article below:

The list of judges is already down to four and will be down to the minimum of three when the Mauritian member, Shree Baboo Chekitan Servansing, retires at the end of September. Two more members will go by the end of next year, at which point the appeals process will come to a halt.

This raises the question of the implication of a ‘no-deal’ Brexit – something that seems more likely as the UK struggles to reach a trade agreement with the EU. Leaving without a deal would mean ‘reverting to WTO rules’. But if these rules are being ignored by powerful countries such as the USA and possibly China, and if the appeals procedure has ground to a halt, this could leave the UK without the safety net of international trade rules. Outside the EU – the world’s most powerful trade bloc – the UK could find itself having to accept poor trade terms with the USA and other large countries.

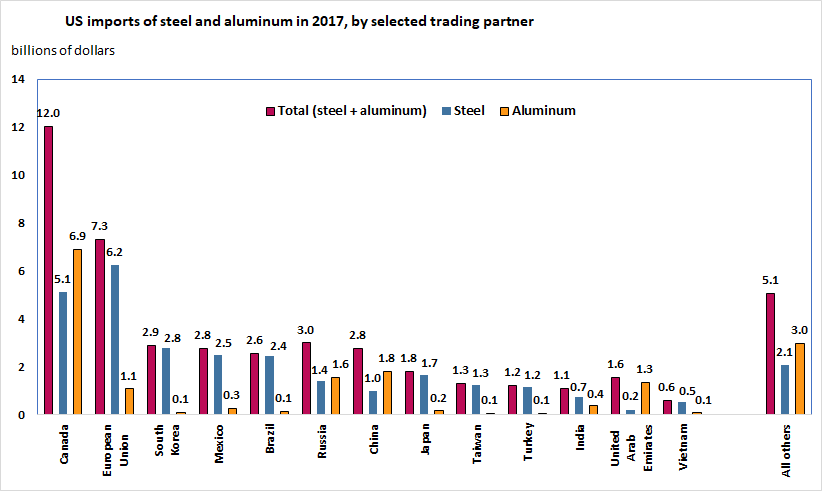

The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

Source: Bown (2018), Figure 1

A number of economists and policymakers are worried that such policies restrict trade and are likely to provoke retaliation by the affected trade partners. In recent statements, the EU has pledged to take counter-measures if the bloc is affected by these policies. In a recent press conference, the Commissioner for Trade, Cecilia Malmstrom, stated that:

We have made it clear that a move that hurts the EU and puts thousands of European jobs in jeopardy will be met with a firm and proportionate response.

She added that, ‘I truly hope that this will not happen. A trade war has no winners.’

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.

A number of studies have attempted to estimate the effect of trade restrictions and tariff wars on welfare: see for instance Anderson and Wincoop (2001), Syropoulos (2002), Fellbermayr et al. (2013). The results vary widely, depending on the case. However, there seems to be consensus that the more similar (in terms of size and industry composition) the adversaries are, the more mutually damaging a trade war is likely to be (and, therefore, less likely to happen).

As Miyagiwa et al (2016, p43) explain:

A country initiates contingent protection policy against a trading partner only if the latter has a considerably smaller domestic market than its own, while avoiding confrontation with a country having a substantially larger domestic market than its own.

As both Canada and the EU are very large advanced market economies, it remains to be seen how much risk (and potential damage to the local and global economy) US trade policymakers are willing to take.

Three recent reports (see links below) have suggested that US consumers and businesses pay most of the tariffs imposed by the second Trump administration. The percentage varies from around 86% to 96%. US customs revenue surged by approximately $200 billion in 2025, but this was a tax paid almost entirely by US consumers and businesses. Foreign suppliers largely maintained their (pre-tariff) prices. They took a hit in terms of reduced volumes rather than reduced pre-tariff prices.

Three recent reports (see links below) have suggested that US consumers and businesses pay most of the tariffs imposed by the second Trump administration. The percentage varies from around 86% to 96%. US customs revenue surged by approximately $200 billion in 2025, but this was a tax paid almost entirely by US consumers and businesses. Foreign suppliers largely maintained their (pre-tariff) prices. They took a hit in terms of reduced volumes rather than reduced pre-tariff prices. Imposition of a tariff will shift the supply curve upwards by the amount of the tariff. The new equilibrium price paid by importers will be at point b, where the new supply curve crosses the demand curve. Importers thus now pay a post-tariff price of P2: an effective rise in price of P2 minus P1. Foreign exporters receive P3, which is what they are paid by importers after the tariff has been paid.

Imposition of a tariff will shift the supply curve upwards by the amount of the tariff. The new equilibrium price paid by importers will be at point b, where the new supply curve crosses the demand curve. Importers thus now pay a post-tariff price of P2: an effective rise in price of P2 minus P1. Foreign exporters receive P3, which is what they are paid by importers after the tariff has been paid.

Over the decades, economies have become increasingly interdependent. This process of globalisation has involved a growth in international trade, the spread of technology, integrated financial markets and international migration.

Over the decades, economies have become increasingly interdependent. This process of globalisation has involved a growth in international trade, the spread of technology, integrated financial markets and international migration. According to the Office for Budget Responsibility’s November 2022 Economic and Fiscal Outlook, Brexit will result in the UK’s trade intensity being 15 per cent lower in the long run than if it had remained in the EU.

According to the Office for Budget Responsibility’s November 2022 Economic and Fiscal Outlook, Brexit will result in the UK’s trade intensity being 15 per cent lower in the long run than if it had remained in the EU.  But trade can increase dependence on unreliable supply sources. For example, at present, some companies are seeking to reduce their reliance on Taiwanese parts, given worries about possible Chinese actions against Taiwan.

But trade can increase dependence on unreliable supply sources. For example, at present, some companies are seeking to reduce their reliance on Taiwanese parts, given worries about possible Chinese actions against Taiwan.  The problems with a globally interdependent world have led to world trade growing more slowly than world GDP in recent years after decades of trade growth considerably outstripping GDP growth. Trade (imports plus exports) as a percentage of GDP peaked at just over 60% in 2008. In 2019 and 2021 it was just over 56%. This is illustrated in the chart (click

The problems with a globally interdependent world have led to world trade growing more slowly than world GDP in recent years after decades of trade growth considerably outstripping GDP growth. Trade (imports plus exports) as a percentage of GDP peaked at just over 60% in 2008. In 2019 and 2021 it was just over 56%. This is illustrated in the chart (click

World politicians, business leaders, charities and pressure groups are meeting in Davos at the

World politicians, business leaders, charities and pressure groups are meeting in Davos at the  In the long run, supply bottlenecks can be overcome with appropriate investment. This may require both greater globalisation and greater localisation, with investment in supply chains that use both local and international sources.

In the long run, supply bottlenecks can be overcome with appropriate investment. This may require both greater globalisation and greater localisation, with investment in supply chains that use both local and international sources.  Donald Trump has threatened to pull out of the World Trade Organization. ‘If they don’t shape up, I would withdraw from the WTO,’ he said. He argues that the USA is being treated very badly by the WTO and that the organisation needs to ‘change its ways’.

Donald Trump has threatened to pull out of the World Trade Organization. ‘If they don’t shape up, I would withdraw from the WTO,’ he said. He argues that the USA is being treated very badly by the WTO and that the organisation needs to ‘change its ways’. This raises the question of the implication of a ‘no-deal’ Brexit – something that seems more likely as the UK struggles to reach a trade agreement with the EU. Leaving without a deal would mean ‘reverting to WTO rules’. But if these rules are being ignored by powerful countries such as the USA and possibly China, and if the appeals procedure has ground to a halt, this could leave the UK without the safety net of international trade rules. Outside the EU – the world’s most powerful trade bloc – the UK could find itself having to accept poor trade terms with the USA and other large countries.

This raises the question of the implication of a ‘no-deal’ Brexit – something that seems more likely as the UK struggles to reach a trade agreement with the EU. Leaving without a deal would mean ‘reverting to WTO rules’. But if these rules are being ignored by powerful countries such as the USA and possibly China, and if the appeals procedure has ground to a halt, this could leave the UK without the safety net of international trade rules. Outside the EU – the world’s most powerful trade bloc – the UK could find itself having to accept poor trade terms with the USA and other large countries. The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.