Many of you reading the articles on this website will be just about to start, or will have just started, studying economics at university. For some of you this will involve building on the knowledge you obtained prior to university, whereas for others it will be the first time you have ever studied the subject before. Will studying economics change the way you behave? Should it come with a health warning?

Many of you reading the articles on this website will be just about to start, or will have just started, studying economics at university. For some of you this will involve building on the knowledge you obtained prior to university, whereas for others it will be the first time you have ever studied the subject before. Will studying economics change the way you behave? Should it come with a health warning?

Can studying economics change the way you think and behave? The subject is often sold to prospective students on the grounds that it can. For example it is stated on the Economics Network’s Why Study Economics? website that

The economic way of thinking can help us make better choices

However, is it possible that studying economics could change people’s behaviour in a way that would be to the detriment of society? Some observers have argued that it can. They have suggested that students might be influenced by some of the assumptions that are made in traditional economic theory.

As social scientists, economists are always trying to analyse human behaviour. However, people vary in many different ways and have very diverse preferences. If we want to build a theory that predicts how people will behave and respond in different situations, then some type of simplifying assumptions are inevitable.

Traditionally one of the key simplifying assumptions that economists have used in their theories of human behaviour is that people make decisions in their own self-interest. There is some debate about exactly what self-interest means. For example it could be argued that giving £10 to charity is acting in your own self-interest if it gives you more pleasure than spending that £10 on yourself. However, in many of the economic theories that you first study in economics a narrow meaning of self-interest tends to be used. This is clearly illustrated by the following quote from Milgrom and Roberts. Referring to economic theory they state that:

It is often assumed that people behave as if they were entirely motivated by narrow, selfish concerns

It is important to make it clear that economists are not assuming that people behave in a selfish manner all of the time. Instead, they are assuming that the people in their theories are acting in a selfish manner. The value of making this assumption is whether the predictions about human behaviour that follow from using it are supported by evidence from the real world.

Some researchers have argued that when people study economic theory built on this assumption it makes them more likely to behave in a selfish way. The evidence for this comes from a range of research papers. Here are some findings:

Economics students were more likely than those studying other subjects to recommend the most expensive plumber to a student society if that plumber offered the student a side payment.

Students took part in an experiment in a computer room where they could either keep the money they had been given or donate it to a public good. On average the economics students kept more of the money.

Economics professors gave less money to charity than professors of other subjects such as psychology and sociology.

Some studies also found that selfish people were more likely to choose economics as a subject to study and became more selfish after they had studied it for some time.

If you are about to begin your study of economics then perhaps you should take care that your behaviour outside the classroom is not being unduly influenced by some of the assumptions you are learning about inside the classroom. On a more practical note perhaps you should avoid sharing a restaurant bill or buying rounds of drinks when in the company of other economists!!!

However on a brighter note, the evidence in these papers can be interpreted in a number of different ways. There are even some studies that found economics students were less selfish than those on other courses.

Re-Post: Does Studying Economics Make You Selfish? The Splintered Mind (21/11/12)

Does studying economics make you more selfish? BBC (22/10/13)

Does Studying Economics Breed Greed? Huffington Post (22/10/13)

The Dismal Education The New York Times (16/12/11)

Does Economics Make You a Bad Person? Conversable Economist (31/3/14)

Economists aren’t all bad FT Magazine (11/4/14)

Questions

- What is an economic model? Why is it necessary to make simplifying assumptions?

- How are economic models judged? How important is it for the assumptions to accurately describe the real world?

- Try to find some jokes that have been made about the use of assumptions in economic theory.

- Can you think of any alternative explanations for the results found in the research papers referred to in the case?

- Try to find a research paper that finds evidence that economics students are less selfish than other students.

- What is a public good? Explain why someone with selfish preferences would not contribute to the public good.

The British love to talk about house prices. Stories about the latest patterns in prices regularly adorn the front pages of newspapers. We take this opportunity to update an earlier blog looking not only at house prices in the UK, but in other countries too (see the (not so) cool British housing market). This follows the latest data release from the ONS which shows the UK’s annual house price inflation rate ticking up from 10.2 per cent in June to 11.7 per cent in July and which contrasts markedly with the annual rate in July 2013 of 3.3 per cent.

The British love to talk about house prices. Stories about the latest patterns in prices regularly adorn the front pages of newspapers. We take this opportunity to update an earlier blog looking not only at house prices in the UK, but in other countries too (see the (not so) cool British housing market). This follows the latest data release from the ONS which shows the UK’s annual house price inflation rate ticking up from 10.2 per cent in June to 11.7 per cent in July and which contrasts markedly with the annual rate in July 2013 of 3.3 per cent.

The July annual house price inflation figure of 11.7 per cent for the UK is heavily influenced by the rates in London and the South East. In London house price inflation is running at 19.1 per cent while in the South East it is 12.2 per cent. Across the rest of the UK the average rate is 7.9 per cent, though this has to be seen in the context of the July 2013 rate of 0.8 per cent.

Chart 1 shows house price inflation rates across the home nations since the financial crisis of the late 2000s. It shows a rebound in house price inflation over the second half of 2013 and across 2014. In July 2014 house price inflation was running at 12.0 per cent in England, 7.6 per cent in Scotland, 7.4 per cent in Wales and 4.5 per cent in Northern Ireland. If we use the East Midlands as a more accurate barometer of England, annual house price inflation in July was 7.6 per cent – the same as across Scotland. (Click here for a PowerPoint of the chart.)

Chart 1 shows house price inflation rates across the home nations since the financial crisis of the late 2000s. It shows a rebound in house price inflation over the second half of 2013 and across 2014. In July 2014 house price inflation was running at 12.0 per cent in England, 7.6 per cent in Scotland, 7.4 per cent in Wales and 4.5 per cent in Northern Ireland. If we use the East Midlands as a more accurate barometer of England, annual house price inflation in July was 7.6 per cent – the same as across Scotland. (Click here for a PowerPoint of the chart.)

Consider a more historical perspective. The average annual rate of growth since 1970 is 9.7 per cent in the UK, 9.7 per cent in England (9.6 per cent in the East Midlands), 9.6 per cent in Wales, 8.8 per cent in Scotland and 8.7 per cent in Northern Ireland. Therefore, house prices in the home nations have typically grown by 9 to 10 per cent per annum. But, as recent experience shows, this has been accompanied by considerable volatility. An interest question is the extent to which these two characteristics of British house prices are unique to Britain. To address this question, let’s go international.

Chart 2 shows annual house price inflation rates for the UK and six other countries since 1996. Interestingly, it shows that house price volatility is a common feature of housing markets. It is not a uniquely British thing. It too shows shows something of a recovery in global house prices. However, the rebound in the UK and the USA does appear particularly strong compared with core eurozone economies, like the Netherlands and France, where the recovery is considerably more subdued. (Click here for a PowerPoint of the chart.)

Chart 2 shows annual house price inflation rates for the UK and six other countries since 1996. Interestingly, it shows that house price volatility is a common feature of housing markets. It is not a uniquely British thing. It too shows shows something of a recovery in global house prices. However, the rebound in the UK and the USA does appear particularly strong compared with core eurozone economies, like the Netherlands and France, where the recovery is considerably more subdued. (Click here for a PowerPoint of the chart.)

The chart captures very nicely the effect of the financial crisis and subsequent economic downturn on global house prices. Ireland saw annual rates of house price deflation exceed 24 per cent in 2009 compared with rates of deflation of 12 per cent in the UK. Denmark too suffered significant house price deflation with prices falling at an annual rate of 15 per cent in 2009.

House price volatility appears to be an inherent characteristic of housing markets worldwide. Consider now the extent to which house prices rise over the longer term. In doing so, we analyse real house price growth after having stripped out the effect of consumer price inflation. Real house price growth measures the growth of house prices relative to consumer prices.

Chart 3 shows real house prices since 1995 Q1. (Click here for a PowerPoint of the chart.) It shows that up to 2014 Q2, real house prices in the UK have risen by a factor of 2.4 This is a little less than in Sweden where prices are 2.6 times higher. Nonetheless, the increase in real house prices in the UK and Sweden is significantly higher than in the other countries in the sample. In particular, in the USA real house prices in 2014 Q2 were only 1.2 times higher than in 1995 Q1. Therefore, in America actual house prices, when viewed over the past 19 years or so, have grown only a little more quickly than consumer prices.

Chart 3 shows real house prices since 1995 Q1. (Click here for a PowerPoint of the chart.) It shows that up to 2014 Q2, real house prices in the UK have risen by a factor of 2.4 This is a little less than in Sweden where prices are 2.6 times higher. Nonetheless, the increase in real house prices in the UK and Sweden is significantly higher than in the other countries in the sample. In particular, in the USA real house prices in 2014 Q2 were only 1.2 times higher than in 1995 Q1. Therefore, in America actual house prices, when viewed over the past 19 years or so, have grown only a little more quickly than consumer prices.

The latest data on house prices suggest that house price volatility is not unique to the UK. The house price roller coaster is an international phenomenon. However, the rate of growth in UK house prices over the longer term, relative to consumer prices, is markedly quicker than in many other countries. It is this which helps to explain the amount of attention paid to the UK housing market. The ride continues.

Data

House Price Indices: Data Tables Office for National Statistics

Articles

Property prices in all regions of the UK grow at the fastest annual pace seen in seven years Independent, Gideon Spanier (16/9/14)

UK House Prices Have Not Soared This Fast In Seven Years The Huffington Post UK, Asa Bennett (16/9/14)

UK house prices hit new record as London average breaks £500,000 Guardian, Phillip Inman (6/12/14)

Six regions hit new house price peak, says ONS BBC News, (16/9/14)

Welsh house prices nearing pre-crisis peak BBC News, (16/9/14)

Questions

- What is meant by the annual rate of house price inflation? What about the annual rate of house price deflation?

- What factors are likely to affect housing demand?

- What factors are likely to affect housing supply?

- Explain the difference between nominal and real house prices. What does a real increase in house prices mean?

- How might we explain the recent differences between house price inflation rates in London and the South East relative to the rest of the UK?

- What might explain the very different long-term growth rates in real house prices in the USA and the UK?

- Why were house prices so affected by the financial crisis?

- What factors help explain the volatility in house prices?

- How might we go about measuring the affordability of housing?

- In what ways might house price patterns impact on the macroeconomy?

Merlin Entertainments PLC is one of the largest operator of visitor attractions in the world and owns over a third of the most popular theme parks in Europe. It runs the four most visited parks in England – Alton Towers, Legoland Windsor, Thorpe Park and Chessington World of Adventures as well as the most popular theme park in Italy – Gardaland. Alton Towers alone had 2.5 million visitors in 2013. Anybody thinking of going to one of these attractions is faced with a wide range of different entry fees .

Merlin Entertainments PLC is one of the largest operator of visitor attractions in the world and owns over a third of the most popular theme parks in Europe. It runs the four most visited parks in England – Alton Towers, Legoland Windsor, Thorpe Park and Chessington World of Adventures as well as the most popular theme park in Italy – Gardaland. Alton Towers alone had 2.5 million visitors in 2013. Anybody thinking of going to one of these attractions is faced with a wide range of different entry fees .

Theme parks and tourist attractions have market power so their owners have to make some interesting pricing decisions. They have to tackle the same dilemma that confronts any seller that faces a downward sloping demand curve for its goods/services.

One option for the firm would be to increase the entry fee. This would produce higher profits per visitor as some of the surplus from the transaction previously enjoyed by the consumer will be extracted by the seller and converted into producer surplus. Unfortunately for the business the higher price, all other things equal, will also result in fewer visitors. Some people will be deterred from visiting because of the higher price and the seller will lose out on potential revenue.

An alternative strategy would be for the theme park to reduce its entry fee. All other things equal, this will increase the number of visitors. However, it would also mean that the profit per customer would fall. The frustrating issue for the seller is that some of its customers, who would still have visited the attraction at the higher price, are now able to get a better deal.

This dilemma exists if the seller has to charge all of its different customers the same entry fee. If it could charge a higher entry fee to those customers who would be willing to pay more and a lower entry fee to those who would be willing to pay less then it could make more money. Extra revenue could be obtained from those additional sales that take place at the lower price while more consumer surplus could be extracted from those still paying the higher price.

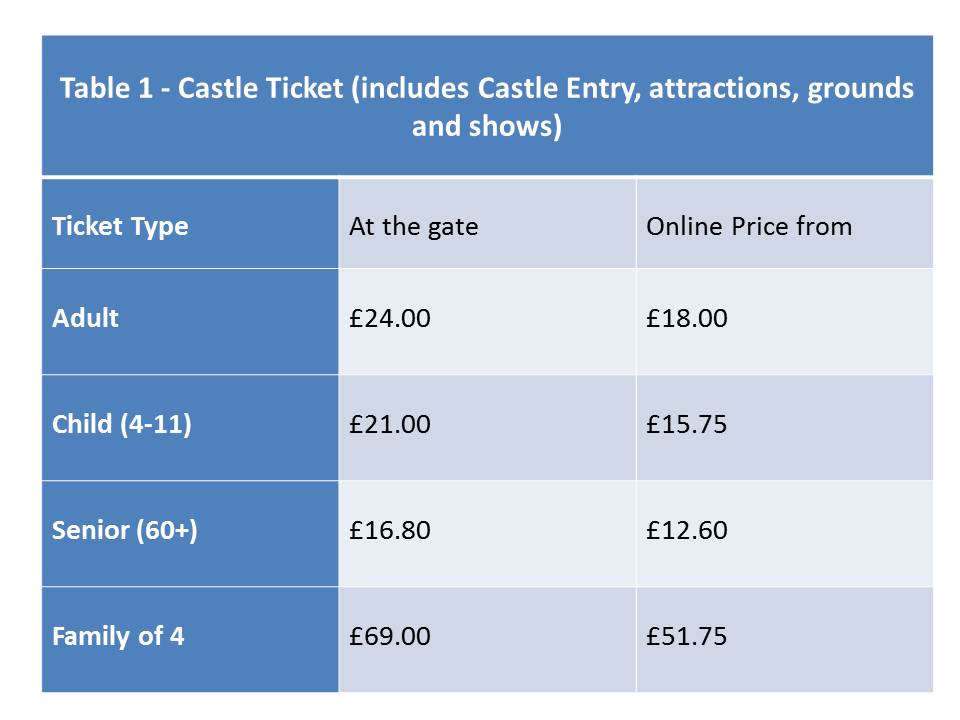

Is it possible for a firm to charge different prices to different customers for the same or a similar good or service? Table 1 below shows the entry fees for Warwick Castle, another tourist attraction owned by Merlin Entertainments PLC.

It can immediately be seen from this table that some groups of customers pay a different entry fee from others. For example adults have to pay £24 to enter on the day while people aged 60 and over pay a lower price £16.80. The entry fee for children aged between 4 and 11 is £21.00 while those aged 3 and under go for free. Students aged 16-18 can gain entry for a price of £13.50 if they can provide valid ID and purchase the tickets from the visitbritainshop website.

In this example, the company has allocated people into different categories by age (i.e. senior, adult, student, older children and younger children) and has set the entry fee that customers in each group have to pay.

The table also shows that if customers purchase on- line then they can get the tickets more cheaply. The entry fee for each category is 25% lower if the ticket is booked seven days in advance i.e. the prices shown in the last column in the table. If the booking is made between 2-6 days in advance then the discount is only 10% i.e. an adult ticket would cost £21.60. The on-line discounts are open to everyone. People are given the choice to either book on-line in advance or pay on the day. This is different from a situation where you are placed into a category by the firm. For example the customer cannot choose whether they are over 60!

If people are prepared to spend more time searching on the internet then other cheaper prices can also be obtained. Once again these offers are open to anyone willing to spend the time and effort in order to find them.

All the ticket prices above give people access to exactly the same attractions on the day. They do not give the visitor access to two of the attractions at the castle – the Dragon Tower and Castle Dungeon. Entry to the Dragon Tower would cost an adult on the day an extra £1.80 while entry to the Castle Dungeon would cost an extra £5.40.

Warwick Castle Ticket Prices Warwick Castle (accessed on 04/09/14)

Alton Towers Alton Towers (accessed on 08/09/14)

Warwick Castle Tickets visitbritainshop (accessed on 02/09/14)

Global Attractions Attendance Report teaconnect (accessed on 05/09/14)

Merlin Entertainments Merlin Entertainments (accessed on 08/09/14)

Questions

- What pricing decisions do firms have to make if they operate in a perfectly competitive market?

- Explain why an individual tourist attraction will have a downward sloping demand curve

- Paying an entry fee and an extra payment per attraction is known as what type of pricing? What advantages does this type of price strategy have for the seller?

- How would you calculate the profit per customer? What factors other than the entrance fee would determine the profit made per customer in a theme park or tourist attractions?

- Paying a different price depending on which category you have been assigned to by the seller is known as what type of pricing strategy? Can this type of pricing strategy ever be in the interests of society?

- In the example used in the case, customers are assigned to different categories by age. Can you think of any other ways that firms could categorise their customers?

- Given the category customers have been assigned to they can pay different prices depending on whether they buy the tickets on line. What is the price strategy called when customers can choose from a variety of pricing options for the same or similar product? Can you think of any different methods that could be used by the seller to carry out this type of pricing strategy?

Commodity prices have been falling for the past three years and have reached a four-year low. Since early 2011, the IMF overall commodity price index (based on 2005 prices) has fallen by 16.5%: from 210.1 in April 2011 to 175.4 in August 2014. The last time it was this low was December 2010.

Commodity prices have been falling for the past three years and have reached a four-year low. Since early 2011, the IMF overall commodity price index (based on 2005 prices) has fallen by 16.5%: from 210.1 in April 2011 to 175.4 in August 2014. The last time it was this low was December 2010.

Some commodity prices have fallen by greater percentages, and in other cases the fall has been only slight. But in the past few months the falls have been more pronounced across most commodities. The chart below illustrates these falls in the case of three commodity groups: (a) food and beverages, (b) agricultural raw materials and (c) metals, ores and minerals. (Click here for a PowerPoint of the chart.)

Commodity prices are determined by demand and supply, and factors on both the demand and supply sides have contributed to the falls.

With growth slowing in China and with zero growth in the eurozone, demand for commodities has shown little growth and in some cases has fallen as stockpiles have been reduced.

On the supply side, investment in mining has boosted the supply of minerals and good harvests in various parts of the world have boosted the supply of many agricultural commodities.

But in historical terms, prices are still relatively high. There was a huge surge in commodity prices in the period up to the financial crisis of 2008 and then another surge as the world economy began to recover from 2009–11. Nevertheless, taking a longer-term perspective still, commodity prices have risen in real terms since the 1960s, but with considerable fluctuations around this trend, reflecting demand and supply at the time.

Articles

Commodities Fall to 5-Year Low With Plenty of Supplies Bloomberg Businessweek, Chanyaporn Chanjaroen (11/9/14)

Commodity ETFs at Multi-Year Lows on Supply Glut ETF Trends, Tom Lydon (11/9/14)

What dropping commodity prices mean CNBC, Art Cashin (11/9/14)

What dropping commodity prices mean CNBC, Art Cashin (11/9/14)

Goldman sees demand hitting commodity price DMM FX (12/9/14)

Commodity price slump is a matter of perspective Sydney Morning Herald, Stephen Cauchi (11/9/14)

Commodities index tumbles to five-year low Financial Times, Neil Hume (12/9/14)

Commodities: More super, less cycle HSBC Global Research, Paul Bloxham (8/1/13)

Commodity prices in the (very) long run The Economist (12/3/13)

Data

IMF Primary Commodity Prices IMF

UNCTADstat UNCTAD (Select: Commodities > Commodity price long-term trends)

Commodity prices Index Mundi

Questions

- Identify specific demand-and supply-side factors that have affected prices of (a) grains; (b) meat; (c) metal prices; (d) oil.

- Why is the demand for commodities likely to be relatively inelastic with respect to price, at least in the short term? What are the implications of this for price responses to changes in supply?

- Why may there currently be a ‘buying opportunity’ for potential commodity purchasers?

- What is meant by the ‘futures market’ and future prices? Why may the 6-month future price quoted today not necessarily be the same as the spot price (i.e. the actual price for immediate trading) in 6 months’ time?

- How does speculation affect commodity prices?

- How does a strong US dollar affect commodity prices (which are expressed in dollars)?

- How may changes in stockpiles give an indication of likely changes in commodity prices over the coming months?

- Distinguish between real and nominal commodity prices. Which have risen more and why?

- How do real commodity prices today compare with those in previous decades?

Economic journalists, commentators and politicians have been examining the possible economic effects of a Yes vote in the Scottish independence referendum on 18 September. For an economist, there are two main categories of difficulty in examining the consequences. The first is the positive question of what precisely will be the consequences. The second is

Economic journalists, commentators and politicians have been examining the possible economic effects of a Yes vote in the Scottish independence referendum on 18 September. For an economist, there are two main categories of difficulty in examining the consequences. The first is the positive question of what precisely will be the consequences. The second is  the normative question of whether the likely effects will be desirable or undesirable and how much so.

the normative question of whether the likely effects will be desirable or undesirable and how much so.

The first question is largely one of ‘known unknowns’. This rather strange term was used in 2002 by Donald Rumsfeld, US Secretary of Defense, in the context of intelligence about Iraq. The problem is a general one about forecasting the future. We may know the types of thing that are likely happen, but the magnitude of the outcome cannot be precisely known because there are so many unknowable things that can influence it.

Here are some known issues of Scottish independence, but with unknown consequences (at least in precisely quantifiable terms). The list is certainly not exhaustive and you could probably add more questions yourself to the list.

|

|

| • |

Will independence result in lower or higher economic growth in the short and long term? |

| • |

Will there be a currency union, with Scotland and the rest of the UK sharing the pound and a central bank? Or will Scotland merely use the pound outside a currency union? Would it prefer to have its own currency or join the euro over the longer term? |

| • |

What will happen to the sterling exchange rate with the dollar, the euro and various other countries? |

| • |

How will businesses react? Will independence encourage greater inward investment in Scotland or will there be a net capital outflow? And either way, what will be the magnitude of the effect? |

| • |

How will assets, such as oil, be shared between Scotland and the rest of the UK? And how will national debt be apportioned? |

| • |

How big will the transition costs be of moving to an independent Scotland? |

| • |

How will independence impact on Scottish trade (a) with countries outside the UK and (b) with the rest of the UK? |

| • |

What will happen about Scotland’s membership of the EU? Will other EU countries, such as Spain (because of its concerns about independence movements in Catalonia and the Basque country), attempt to block Scotland remaining in or rejoining the EU? |

| • |

What will happen to tax rates in Scotland, with the new Scottish government free to set its own tax rates? |

| • |

What will be the consequences for Scottish pensions and the Scottish pensions industry? |

| • |

What will happen to the distribution of income in Scotland? How might Scottish governments behave in terms of income redistribution and what will be its consequences on output and growth? |

Of course, just because the effects cannot be known with certainty, attempts are constantly being made to quantify the outcomes in the light of the best information available at the time. These are refined as circumstances change and newer data become available.

But forecasts also depend on the assumptions made about the post-referendum decisions of politicians in Scotland, the rest of the UK and in major trading partner countries. It also depends on assumptions about the reactions of businesses. Not surprisingly, both sides of the debate make assumptions favourable to their own case.

But forecasts also depend on the assumptions made about the post-referendum decisions of politicians in Scotland, the rest of the UK and in major trading partner countries. It also depends on assumptions about the reactions of businesses. Not surprisingly, both sides of the debate make assumptions favourable to their own case.

Then there is the second category of question. Even if you could quantify the effects, just how desirable would they be? The issue here is one of the weightings given to the various costs and benefits. How would you weight distributional consequences, given that some people will gain or lose more than others? What social discount rate would you apply to future costs and benefits?

Then there are the normative and largely unquantifiable costs and benefits. How would you assess the desirability of political consequences, such as greater independence in decision-making or the break-up of a union dating back over 300 years? But these questions about nationhood are crucial issues for many of the voters.

Articles

Scottish Independence would have Broad Impact on UK Economy NBC News, Catherine Boyle (9/9/14)

Scottish independence: the economic implications The Guardian, Angela Monaghan (7/9/14)

Scottish vote: Experts warn of potential economic impact BBC News, Matthew Wall (9/9/14)

The economics of Scottish independence: A messy divorce The Economist (21/2/14)

Dispute over economic impact of Scottish independence Financial Times, Mure Dickie, Jonathan Guthrie and John Aglionby (28/5/14)

10 economic benefits for a wealthier independent Scotland Michael Gray (6/3/14)

Scottish independence, UK dependency New Economics Foundation (NEF), James Meadway (4/9/14)

Scottish Jobs and the World Economy Scottish Economy Watch, Brian Ashcroft (25/8/14)

Scottish yes vote: what happens to the pound in your pocket? Channel 4 News (9/9/14)

What price Scottish independence? BBC News, Robert Peston (12/9/14)

What price Scottish independence? BBC News, Robert Peston (7/9/14)

Economists can’t tell Scots how to vote BBC News, Robert Peston (16/9/14)

Books and Reports

The Economic Consequences of Scottish Independence Scottish Economic Society and Helmut Schmidt Universität, David Bell, David Eiser and Klaus B Beckmann (eds) (August 2014)

The potential implications of independence for businesses in Scotland Oxford Economics, Weir (April 2014)

Questions

- What is a currency union? What implications would there be for Scotland being in a currency union with the rest of the UK?

- If you could measure the effects of independence over the next ten years, would you treat £1m of benefits or costs occurring in ten years’ time the same as £1m of benefits and costs occurring next year? Explain.

- Is it inevitable that events occurring in the future will at best be known unknowns?

- If you make a statement that something will occur in the future and you turn out to be wrong, was your statement a positive one or a normative one?

- What would be the likely effects of Scottish independence on the current account of the balance of payments (a) for Scotland; (b) for the rest if the UK?

- How does inequality in Scotland compare with that in the rest of the UK and in other countries? Why might Scottish independence lead to a reduction in inequality? (See the chapter on inequality in the book above edited by David Bell, David Eiser and Klaus B Beckmann.)

- One of the problems in assessing the arguments for a Yes vote is uncertainty over what would happen if there was a majority voting No. What might happen in terms of further devolution in the case of a No vote?

- Why is there uncertainty over the amount of national debt that would exist in Scotland if it became independent?