I recently found myself talking about my favourite TV shows from my childhood. Smurfs aside, the most popular one for me (and I suppose for many other people from my generation) had to be Knight Rider. It was a story about a crime fighter (David Hasselhoff) and his a heavily modified, artificially intelligent Pontiac Firebird. ‘Kitt’ was a car that could drive itself, engage in thoughtful and articulate conversations, carry out missions and (of course) come up with solutions to complex problems! A car that was very far from what was technologically possible in the 80s – and this was part of its charm.

Today this technology is becoming reality. Google, Tesla and most major automakers are testing self-driving cars with many advanced features like Kitt’s – if not better. They may not fire rockets, but they can drive themselves; they can search the internet; they can answer questions in a language of your choice; and they can be potentially integrated with a number of other technologies (such as car sharing apps) to revolutionise the way we own and use our cars. It will take years until we are able to purchase and use a self-driving car – but it appears very likely that this technology is going to become roadworthy within our lifetime.

Artificial intelligence (AI) is already becoming part of our life. You can buy a robotic vacuum cleaner online for less than a £1000. You can get gadgets like Amazon’s Alexa, that can help you automate your supermarket shopping, for instance. If you are Saudi, you can boast that you are compatriots with a humanoid: Saudi Arabia was the first country to grant citizenship to Sophia, an impressive humanoid and apparently a notorious conversationalist who does not miss an opportunity to address a large audience – and it has done so numerous times already in technology fairs, national congresses – even the UN Assembly! Sophia is the first robot to be honoured with a UN title!

What will be the impact of such technologies on labour markets? If cars can drive themselves, what is going to happen to the taxi drivers? Or the domestic housekeepers – who may find themselves increasingly displaced by cleaning robots. Or warehouse workers who may find themselves displaced by delivery bots (did you know that Alibaba, the Chinese equivalent of eBay, owns a warehouse where most of the work is carried out by robots?). There is no doubt that labour markets are bound to change. But should we (the human labour force) be worried about it? Acemoglu et al (2017) think that we should:

Using a model in which robots compete against human labor in the production of different tasks, we show that robots may reduce employment and wages […] According to our estimates, one more robot per thousand workers reduces the employment to population ratio by about 0.18–0.34 percentage points and wages by 0.25–0.5 per cent.[1]

Automation is likely to affect unskilled workers more than skilled ones, as unskilled jobs are the easiest ones to automate. This could have widespread social implications, as it might widen the divide between the poor (who are more likely to have unskilled jobs) and the affluent (who are more likely to own AI technologies). As mentioned in a recent Boston Consulting Group report (see below):

The future of work is likely to involve large structural changes to the labour market and potentially a net loss of jobs, mostly in routine occupations. An estimated 15 million UK jobs could be at risk of automation, with 63 per cent of all jobs impacted to a medium or large extent.

On the other hand, the adoption of automation is likely to result in higher efficiency, huge productivity gains and less waste. Automation will enable us to use the resources that we have in the most efficient way – and this is bound to result in wealth creation. It will also push human workers away from manual, routine jobs – and it will force them to acquire skills and engage in creative thinking. One thing is for certain: labour markets are changing and they are changing fast!

The Boston Consulting Group, Sutton Trust (July 2017)

Questions

What do you think is going to be the effect of automation on labour market participation in the future? Why?

Using the Solow growth model, explain how automation is likely to affect economic growth and capital returns.

In the context of the answer you gave to question 2, explain how human capital accumulation may affect the ability of workers to benefit from automation.

[1] Daron Acemoglu and Pascual Restrepo, Robots and Jobs: Evidence from US Labor Markets, NBER Working Paper No. 23285 (March 2017)

The last two weeks have been quite busy for macroeconomists, HM Treasury staff and statisticians in the UK. The Chancellor of the Exchequer, Mr Phillip Hammond, delivered his (fairly upbeat) Spring Budget Statement on 13 March, highlighting among other things the ‘stellar performance’ of UK labour markets. According to a Treasury Press Release:

Employment has increased by 3 million since 2010, which is the equivalent of 1,000 people finding work every day. The unemployment rate is close to a 40-year low. There is also a joint record number of women in work – 15.1 million. The OBR predict there will be over 500,000 more people in work by 2022.

To put these figures in perspective, according to recent ONS estimates, in January 2018 the rate of UK unemployment was 4.3 per cent – down from 4.4 per cent in December 2017. This is the lowest it has been since 1975. This is of course good news: a thriving labour market is a prerequisite for a healthy economy and a good sign that the UK is on track to full recovery from its 2008 woes.

The Bank of England welcomed the news with a mixture of optimism and relief, and signalled that the time for the next interest rate hike is nigh: most likely at the next MPC meeting in May.

But what is the practical implication of all this for UK consumers and workers?

For workers it means it’s a ‘sellers’ market’: as more people get into employment, it becomes increasingly difficult for certain sectors to fill new vacancies. This is pushing nominal wages up. Indeed, UK wages increased on average by 2.6 per cent year-to-year.

In real terms, however, wage growth has not been high enough to outpace inflation: real wages have fallen by 0.2 per cent compared to last year. Britain has received a pay rise, but not high enough to compensate for rising prices. To quote Matt Hughes, a senior ONS statistician:

Employment and unemployment levels were both up on the quarter, with the employment rate returning to its joint highest ever. ‘Economically inactive’ people — those who are neither working nor looking for a job — fell by their largest amount in almost five and a half years, however. Total earnings growth continues to nudge upwards in cash terms. However, earnings are still failing to outpace inflation.

An increase in interest rates is likely to put further pressure on indebted households. Even more so as it coincides with the end of the five-year grace period since the launch of the 2013 Help-to-Buy scheme, which means that many new homeowners who come to the end of their five year fixed rate deals, will soon find themselves paying more for their mortgage, while also starting to pay interest on their Help-to-buy government loan.

Will wages grow fast enough in 2018 to outpace inflation (and despite Brexit, which is now only 12 months away)? We shall see.

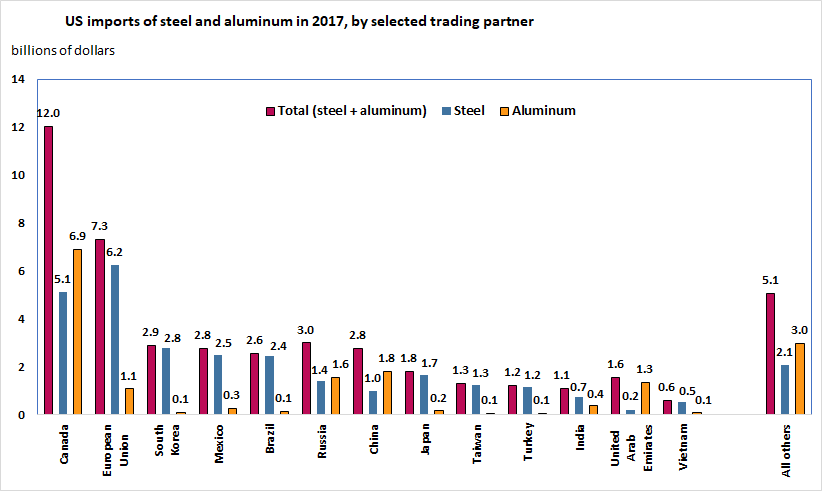

The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

Source: Bown (2018), Figure 1

A number of economists and policymakers are worried that such policies restrict trade and are likely to provoke retaliation by the affected trade partners. In recent statements, the EU has pledged to take counter-measures if the bloc is affected by these policies. In a recent press conference, the Commissioner for Trade, Cecilia Malmstrom, stated that:

We have made it clear that a move that hurts the EU and puts thousands of European jobs in jeopardy will be met with a firm and proportionate response.

She added that, ‘I truly hope that this will not happen. A trade war has no winners.’

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.

A number of studies have attempted to estimate the effect of trade restrictions and tariff wars on welfare: see for instance Anderson and Wincoop (2001), Syropoulos (2002), Fellbermayr et al. (2013). The results vary widely, depending on the case. However, there seems to be consensus that the more similar (in terms of size and industry composition) the adversaries are, the more mutually damaging a trade war is likely to be (and, therefore, less likely to happen).

As Miyagiwa et al (2016, p43) explain:

A country initiates contingent protection policy against a trading partner only if the latter has a considerably smaller domestic market than its own, while avoiding confrontation with a country having a substantially larger domestic market than its own.

As both Canada and the EU are very large advanced market economies, it remains to be seen how much risk (and potential damage to the local and global economy) US trade policymakers are willing to take.

Last week was a rough week for Britain. The “Beast from the East” and storm Emma swept through the country, bringing with them unusually heavy snowfall, which resulted in severe disruption across nearly all parts of the country. Some recent estimates put the cost of these extreme weather conditions at up to £1 billion per day. The construction industry suffering the biggest hit as work came to a halt for the best part of the week. Losses for the industry were estimated to be up to £2 billion.

Closed restaurants, empty shops and severely disrupted transport networks were all part of the effect that this extreme weather had on the overall economy. According to Howard Archer, chief economic adviser of the EY ITEM Club (a UK forecasting group):

It is possible that the severe weather [of the last few days] could lead to GDP growth being reduced by 0.1 percentage point in Q1 2018 and possibly 0.2 percentage points if the severe weather persist.

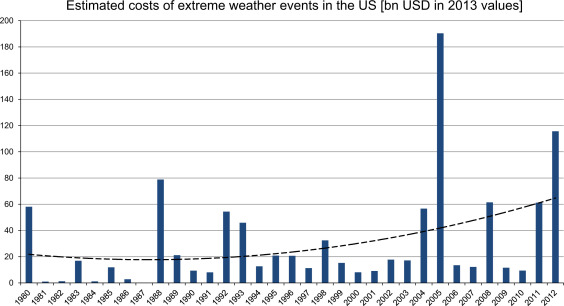

Source: Jahn (2015), Figure 2

As the occurrence of freak weather increases across the globe due to climate change, so does the economic cost of these events. The figure above shows the estimated costs of extreme weather events in the USA between 1980 and 2012 and it is reproduced from Jahn (see link below), who also fits a quadratic trend to show that these costs have been increasing over time. He goes on to characterise the impact of different types of extreme weather (including cold waves, heat waves, storms and others) on different sectors of the local economy – ranging from tourism and agriculture, to housing and the insurance sector.

Linnenluecke et al (linked below) argue that extreme weather caused by climate change could influence the decision of firms on where to locate and could lead to a reshuffle of economic activity across the world and have important policy implications. As the authors explain:

Climate change-related relocation has been given consideration in policy-oriented discussions, but not in management decisions. The effects of climate change and extreme weather events have been considered as peripheral or as a risk factor, but not as a determining factor in firm relocation processes…. This paper therefore [provides] insights for understanding how firms can enhance strategic decision-making in light of understanding and assessing their vulnerability as well as likely impacts that climate change may have on relocation decisions.

The likelihood and associated costs of extreme weather events could therefore become an increasingly important matter for discussion amongst economists and policy makers. Such weather events are likely to have profound economic implications for the world.

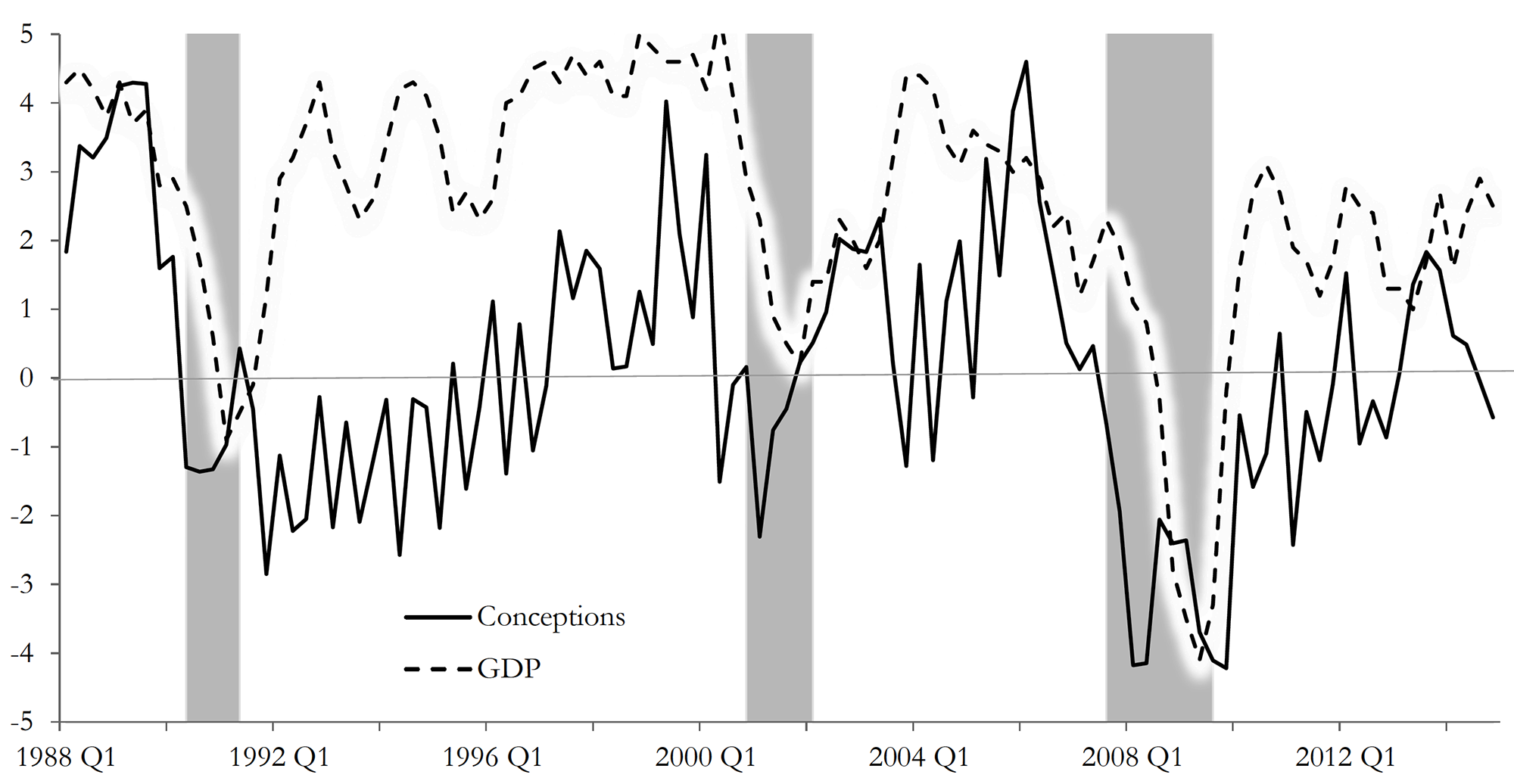

Would you start a family if you were pessimistic about the future of the economy? Buckles et al (2017) (see link below) believe that fewer of us would do so and, therefore, fertility rates could be used by investors and central banks as an early signal to pick up subtle changes in consumer confidence and overall economic climate.

Their study titled ‘Fertility is a leading economic indicator’ uses ‘live births’ data, sourced from US birth certificates, to explore if there is any association between fertility changes (measured as the rate of change in number of births) and GDP growth. Their results suggest that, in the case of the USA, there is: dips in fertility rates tend to precede by several quarters slowdown in economic activity. As the authors state:

The growth rate of conceptions declines prior to economic downturns and the decline occurs several quarters before recessions begin. Our measure of conceptions is constructed using live births; we present evidence suggesting that our results are indeed driven by changes in conceptions and not by changes in abortion or miscarriage. Conceptions compare well with or even outperform other economic indicators in anticipating recessions.

Conception and GDP Growth Rates (source Buckles et al p33: see below)

Although this is not the first piece of academic writing to claim that fertility has pro-cyclical qualities (see for instance, Adsera (2004, 2011), Adsera and Menendez (2011), Currie and Schwandt (2014) and Chatterjee and Vogle (2016) linked below), it is, to the best of our knowledge, the most recent paper (in terms of data used) to depict this relationship and to explore the suitability of fertility as a macroeconomic indicator to predict recessions.

Economies, after all, are groups of people who participate actively in day-to-day production and consumption activities – as consumers, workers and business leaders. Changes in their environment should affect their expectations about the future.

Are people, however, forward-looking enough to guide their current behaviours by their expectations of future economic outcomes? They may be, according to the findings of this study.

Did you know, for instance, that sales of ties tend to increase in economic downturns, as men buy more ties to show that they are working harder, in fear of losing their job[1]? But this is probably a topic for another blog.

Give two reasons why fertility rates may be a good indicator of economic activity.

Give two reasons why fertility rates may NOT be a good indicator of economic activity.

Do a literature search to identify and explain an ‘unorthodox’ macroeconomic indicator of your choice, and how it has been used to track economic activity.

I recently found myself talking about my favourite TV shows from my childhood. Smurfs aside, the most popular one for me (and I suppose for many other people from my generation) had to be Knight Rider. It was a story about a crime fighter (David Hasselhoff) and his a heavily modified, artificially intelligent Pontiac Firebird. ‘Kitt’ was a car that could drive itself, engage in thoughtful and articulate conversations, carry out missions and (of course) come up with solutions to complex problems! A car that was very far from what was technologically possible in the 80s – and this was part of its charm.

I recently found myself talking about my favourite TV shows from my childhood. Smurfs aside, the most popular one for me (and I suppose for many other people from my generation) had to be Knight Rider. It was a story about a crime fighter (David Hasselhoff) and his a heavily modified, artificially intelligent Pontiac Firebird. ‘Kitt’ was a car that could drive itself, engage in thoughtful and articulate conversations, carry out missions and (of course) come up with solutions to complex problems! A car that was very far from what was technologically possible in the 80s – and this was part of its charm. Artificial intelligence (AI) is already becoming part of our life. You can buy a robotic vacuum cleaner online for less than a £1000. You can get gadgets like Amazon’s Alexa, that can help you automate your supermarket shopping, for instance. If you are Saudi, you can boast that you are compatriots with a humanoid: Saudi Arabia was the first country to grant citizenship to Sophia, an impressive humanoid and apparently a notorious conversationalist who does not miss an opportunity to address a large audience – and it has done so numerous times already in technology fairs, national congresses – even the UN Assembly! Sophia is the first robot to be honoured with a UN title!

Artificial intelligence (AI) is already becoming part of our life. You can buy a robotic vacuum cleaner online for less than a £1000. You can get gadgets like Amazon’s Alexa, that can help you automate your supermarket shopping, for instance. If you are Saudi, you can boast that you are compatriots with a humanoid: Saudi Arabia was the first country to grant citizenship to Sophia, an impressive humanoid and apparently a notorious conversationalist who does not miss an opportunity to address a large audience – and it has done so numerous times already in technology fairs, national congresses – even the UN Assembly! Sophia is the first robot to be honoured with a UN title! Robot jobs ‘fourth industrial revolution’

Robot jobs ‘fourth industrial revolution’ The last two weeks have been quite busy for macroeconomists, HM Treasury staff and statisticians in the UK. The Chancellor of the Exchequer, Mr Phillip Hammond, delivered his (fairly upbeat) Spring Budget Statement on 13 March, highlighting among other things the ‘stellar performance’ of UK labour markets. According to a

The last two weeks have been quite busy for macroeconomists, HM Treasury staff and statisticians in the UK. The Chancellor of the Exchequer, Mr Phillip Hammond, delivered his (fairly upbeat) Spring Budget Statement on 13 March, highlighting among other things the ‘stellar performance’ of UK labour markets. According to a

The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.