Interest rates are the main tool of monetary policy and crucially affect investment. There has been much discussion since the end of the financial crisis concerning when UK interest rates would eventually rise. Uncertainty over just when, and by how much, interest rates will rise affects business confidence and hence investment. Businesses therefore listen carefully to what the Bank of England says about future movements in Bank Rate. But Mark Carney has now spoken about another cause of uncertainty and its impct on investment. This is the uncertainty over the outcome of the referendum on whether the UK should leave the EU.

Interest rates are the main tool of monetary policy and crucially affect investment. There has been much discussion since the end of the financial crisis concerning when UK interest rates would eventually rise. Uncertainty over just when, and by how much, interest rates will rise affects business confidence and hence investment. Businesses therefore listen carefully to what the Bank of England says about future movements in Bank Rate. But Mark Carney has now spoken about another cause of uncertainty and its impct on investment. This is the uncertainty over the outcome of the referendum on whether the UK should leave the EU.

By 2017, the Prime Minister has promised a referendum on staying in the EU, but Mark Carney has urged for this to be held ‘as soon as possible’. Whether or not the UK remains in the EU will have a big effect on businesses and with the uncertainty surrounding the UK’s future, this may soon turn to a lack of investment.  As yet, businesses have not responded to this uncertainty, but the longer the delay for the referendum, the more inclined firms will be to postpone investment. As Mark Carney said:

As yet, businesses have not responded to this uncertainty, but the longer the delay for the referendum, the more inclined firms will be to postpone investment. As Mark Carney said:

“We talk to a lot of bosses and there has been an awareness of some of this political uncertainty – whether because of the election or because of the referendum … What they’ve been telling us, and we see it in the statistics, is they have not yet acted on that uncertainty – or to put it another way, they are continuing to invest, they are continuing to hire.”

Leaving the EU will have big effects on consumers and businesses, given that the EU is the UK’s largest market, trading partner and investor. With a referendum sooner rather than later, uncertainty will be more limited and any reaction by businesses will take place over a shorter time period. There are many other factors that affect business investment, some of which are related to the UK’s relationship with the EU and the following articles consider these issues.

EU referendum should be held ‘as soon as necessary’, says Mark Carney BBC News (14/5/15)

Business want an early EU referendum, Mark Carney indicates The Telegraph, Ben Riley-Smith (14/5/15)

EU poll should take place ‘as soon as necessary’, says Bank of England Chief The Guardian, Angela Monaghan (14/5/15)

Threat of business leaving the EU is fuelling business ‘uncertainty’, says Bank of England governor Mark Carney Mail Online, Matt Chorley (14/5/15)

Bank of England’s Mark Carney urges speedy EU referendum Financial Times, George Parker (14/5/15)

Questions

- Why is the EU important to the UK’s economic performance?

- If the UK were to leave the EU, what impact would this have on UK consumers?

- What would be the impact on UK firms if the UK were to leave the EU?

- Consider an AD/AS diagram and use this to explain the potential impact on the macroeconomic variables if the UK were to leave the EU.

- Why is uncertainty over the UK’s referendum likely to have an adverse effect on investment?

With an election approaching in the UK, uncertainty is a term we will hear frequently over the next few weeks. Until we know which party or parties will be in power and hence which policies will be implemented, planning anything is difficult. This is just one of the factors that has caused the British pound sterling to fall last week by 2% to an almost five year low against the dollar.

With an election approaching in the UK, uncertainty is a term we will hear frequently over the next few weeks. Until we know which party or parties will be in power and hence which policies will be implemented, planning anything is difficult. This is just one of the factors that has caused the British pound sterling to fall last week by 2% to an almost five year low against the dollar.

In the last election, uncertainty also prevailed and continued even after the election before the Coalition was formed. Given how close this election appears to be at present, another Coalition may have to be formed and this is adding to the current election uncertainty. A currency strategist at Standard Bank said:

“A $1.40 level for sterling/dollar is certainly not out of reach if the election aftermath turns ugly”

With such uncertainty, investors are refraining from putting their money into the UK and this has contributed towards the deprecation of the British pound against the dollar.

Another factor adding to this downward pressure on the pound is the latest data on industrial output. Although economic growth figures for the UK in 2014 were very positive, there are some suggestions that 2015 will not be as good as expected, though still a strong performance. The first quarter data will not be available until just before the election, but data from the ONS on industrial output shows very minimal growth at just 0.1% from January to February. Chris Williams at Markit said:

“Clearly this all bodes ill for economic growth in the opening quarter of the year. It’s now looking like the economy slowed, and possibly quite markedly, compared to the 0.6% expansion seen in the closing quarter of 2014 … The trend should improve in March, however, according to survey data.”

These two factors have combined to push the pound down, with investors preferring to hold their money in dollars, despite the weak US unemployment data. However, it is not only against the dollar that we must consider sterling’s performance. Against the euro, it has performed better, rising by 1.5%. Whether this is positive for the UK or very negative for the Eurozone is another question. The following articles consider the performance of the British pound.

Sterling falls to five-year low Financial Times, Neil Dennis (10/4/15)

Sterling plummets to five year low as economic slowdown looms The Telegraph, Mehreen Khan (10/4/15)

Pound at five-year low against dollar on weak output BBC News (10/4/15)

Sterling falls after Bank of England’s Haldane says even chances of rate cut or rise Reuters (10/4/15)

Pound falls to five-year low as volatility jumps before election Bloomberg, Anooja Debnath and David Goodman (11/4/15)

Pound falls to a five-year low against the dollar as polls suggest election will create economic uncertainty Mail Online, Matt Chorley (10/4/15)

Questions

- Draw a diagram illustrating the way in which the $/£ exchange rate is determined.

- Explain why the election is causing economic uncertainty in the UK.

- How would uncertainty affect the demand and supply of sterling and hence the exchange rate?

- US job data is worse than expected. Shouldn’t this have caused the dollar to depreciate against the pound and not appreciate?

- Industrial output data for the UK economy is lower than expected. What has caused this?

- Why does slower growth in industrial output cause the exchange rate to depreciate?

- In order to keep the UK’s inflation rate on target, Haldane has said that we could expect a cut or rise in interest rates and policy should be prepared for both. How has this affected the exchange rate?

- Are there any advantages of having a lower pound?

Many UK coal mines closed in the 1970s and 80s. Coal extraction was too expensive in the UK to compete with cheap imported coal and many consumers were switching away from coal to cleaner fuels. Today many shale oil producers in the USA are finding that extraction has become unprofitable with oil prices having fallen by some 50% since mid-2014 (see A crude indicator of the economy (Part 2) and The price of oil in 2015 and beyond). So is it a bad idea to invest in fossil fuel production? Could such assets become unusable – what is known as ‘stranded assets‘?

Many UK coal mines closed in the 1970s and 80s. Coal extraction was too expensive in the UK to compete with cheap imported coal and many consumers were switching away from coal to cleaner fuels. Today many shale oil producers in the USA are finding that extraction has become unprofitable with oil prices having fallen by some 50% since mid-2014 (see A crude indicator of the economy (Part 2) and The price of oil in 2015 and beyond). So is it a bad idea to invest in fossil fuel production? Could such assets become unusable – what is known as ‘stranded assets‘?

In a speech on 3 March 2015, Confronting the challenges of tomorrow’s world, delivered at an insurance conference, Paul Fisher, Deputy Governor of the Bank of England, warned that a switch to both renewable sources of energy and actions to save energy could hit investors in fossil fuel companies.

‘One live risk right now is of insurers investing in assets that could be left ‘stranded’ by policy changes which limit the use of fossil fuels. As the world increasingly limits carbon emissions, and moves to alternative energy sources, investments in fossil fuels and related technologies – a growing financial market in recent decades – may take a huge hit. There are already a few specific examples of this having happened.

… As the world increasingly limits carbon emissions, and moves to alternative energy sources, investments in fossil fuels and related technologies – a growing financial market in recent decades – may take a huge hit. There are already a few specific examples of this having happened.’

Much of the known reserves of fossil fuels could not be used if climate change targets are to be met. And investment in the search for new reserves would be of little value unless they were very cheap to extract. But will climate change targets be met?  That is hard to predict and depends on international political agreements and implementation, combined with technological developments in fields such as clean-burn technologies, carbon capture and renewable energy. The scale of these developments is uncertain. As Paul Fisher said in his speech:

That is hard to predict and depends on international political agreements and implementation, combined with technological developments in fields such as clean-burn technologies, carbon capture and renewable energy. The scale of these developments is uncertain. As Paul Fisher said in his speech:

‘Tomorrow’s world inevitably brings change. Some changes can be forecast, or guessed by extrapolating from what we know today. But there are, inevitably, the unknown unknowns which will help shape the future. … As an ex-forecaster I can tell you confidently that the only thing we can be certain of is that there will be changes that no one will predict.’

The following articles look at the speech and at the financial risks of fossil fuel investment. The Guardian article also provides links to some useful resources.

Articles

Bank of England warns of huge financial risk from fossil fuel investments The Guardian, Damian Carrington (3/3/15)

PRA warns insurers on fossil fuel assets Insurance Asset Risk (3/3/15)

Energy trends changing investment dynamics UPI, Daniel J. Graeber (3/3/15)

Speech

Confronting the challenges of tomorrow’s world Bank of England, Paul Fisher (3/3/15)

Questions

- What factors are taken into account by investors in fossil fuel assets?

- Why might a power station become a ‘stranded asset’?

- How is game theory relevant in understanding the process of climate change negotiations and the outcomes of such negotiations?

- What social functions are filled by insurance?

- Why does climate change impact on insurers on both sides of their balance sheets?

- What is the Prudential Regulation Authority (PRA)? What is its purpose?

- Explain what is meant by ‘unknown unknowns’. How do they differ from ‘known unknowns’?

- How do the arguments in the article and the speech relate to the controversy about investing in fracking in the UK?

- Explain and comment on the statement by World Bank President, Jim Yong Kim, that sooner rather than later, financial regulators must address the systemic risk associated with carbon-intensive activities in their economies.

Economic journalists, commentators and politicians have been examining the possible economic effects of a Yes vote in the Scottish independence referendum on 18 September. For an economist, there are two main categories of difficulty in examining the consequences. The first is the positive question of what precisely will be the consequences. The second is

Economic journalists, commentators and politicians have been examining the possible economic effects of a Yes vote in the Scottish independence referendum on 18 September. For an economist, there are two main categories of difficulty in examining the consequences. The first is the positive question of what precisely will be the consequences. The second is  the normative question of whether the likely effects will be desirable or undesirable and how much so.

the normative question of whether the likely effects will be desirable or undesirable and how much so.

The first question is largely one of ‘known unknowns’. This rather strange term was used in 2002 by Donald Rumsfeld, US Secretary of Defense, in the context of intelligence about Iraq. The problem is a general one about forecasting the future. We may know the types of thing that are likely happen, but the magnitude of the outcome cannot be precisely known because there are so many unknowable things that can influence it.

Here are some known issues of Scottish independence, but with unknown consequences (at least in precisely quantifiable terms). The list is certainly not exhaustive and you could probably add more questions yourself to the list.

|

|

| • |

Will independence result in lower or higher economic growth in the short and long term? |

| • |

Will there be a currency union, with Scotland and the rest of the UK sharing the pound and a central bank? Or will Scotland merely use the pound outside a currency union? Would it prefer to have its own currency or join the euro over the longer term? |

| • |

What will happen to the sterling exchange rate with the dollar, the euro and various other countries? |

| • |

How will businesses react? Will independence encourage greater inward investment in Scotland or will there be a net capital outflow? And either way, what will be the magnitude of the effect? |

| • |

How will assets, such as oil, be shared between Scotland and the rest of the UK? And how will national debt be apportioned? |

| • |

How big will the transition costs be of moving to an independent Scotland? |

| • |

How will independence impact on Scottish trade (a) with countries outside the UK and (b) with the rest of the UK? |

| • |

What will happen about Scotland’s membership of the EU? Will other EU countries, such as Spain (because of its concerns about independence movements in Catalonia and the Basque country), attempt to block Scotland remaining in or rejoining the EU? |

| • |

What will happen to tax rates in Scotland, with the new Scottish government free to set its own tax rates? |

| • |

What will be the consequences for Scottish pensions and the Scottish pensions industry? |

| • |

What will happen to the distribution of income in Scotland? How might Scottish governments behave in terms of income redistribution and what will be its consequences on output and growth? |

Of course, just because the effects cannot be known with certainty, attempts are constantly being made to quantify the outcomes in the light of the best information available at the time. These are refined as circumstances change and newer data become available.

But forecasts also depend on the assumptions made about the post-referendum decisions of politicians in Scotland, the rest of the UK and in major trading partner countries. It also depends on assumptions about the reactions of businesses. Not surprisingly, both sides of the debate make assumptions favourable to their own case.

But forecasts also depend on the assumptions made about the post-referendum decisions of politicians in Scotland, the rest of the UK and in major trading partner countries. It also depends on assumptions about the reactions of businesses. Not surprisingly, both sides of the debate make assumptions favourable to their own case.

Then there is the second category of question. Even if you could quantify the effects, just how desirable would they be? The issue here is one of the weightings given to the various costs and benefits. How would you weight distributional consequences, given that some people will gain or lose more than others? What social discount rate would you apply to future costs and benefits?

Then there are the normative and largely unquantifiable costs and benefits. How would you assess the desirability of political consequences, such as greater independence in decision-making or the break-up of a union dating back over 300 years? But these questions about nationhood are crucial issues for many of the voters.

Articles

Scottish Independence would have Broad Impact on UK Economy NBC News, Catherine Boyle (9/9/14)

Scottish independence: the economic implications The Guardian, Angela Monaghan (7/9/14)

Scottish vote: Experts warn of potential economic impact BBC News, Matthew Wall (9/9/14)

The economics of Scottish independence: A messy divorce The Economist (21/2/14)

Dispute over economic impact of Scottish independence Financial Times, Mure Dickie, Jonathan Guthrie and John Aglionby (28/5/14)

10 economic benefits for a wealthier independent Scotland Michael Gray (6/3/14)

Scottish independence, UK dependency New Economics Foundation (NEF), James Meadway (4/9/14)

Scottish Jobs and the World Economy Scottish Economy Watch, Brian Ashcroft (25/8/14)

Scottish yes vote: what happens to the pound in your pocket? Channel 4 News (9/9/14)

What price Scottish independence? BBC News, Robert Peston (12/9/14)

What price Scottish independence? BBC News, Robert Peston (7/9/14)

Economists can’t tell Scots how to vote BBC News, Robert Peston (16/9/14)

Books and Reports

The Economic Consequences of Scottish Independence Scottish Economic Society and Helmut Schmidt Universität, David Bell, David Eiser and Klaus B Beckmann (eds) (August 2014)

The potential implications of independence for businesses in Scotland Oxford Economics, Weir (April 2014)

Questions

- What is a currency union? What implications would there be for Scotland being in a currency union with the rest of the UK?

- If you could measure the effects of independence over the next ten years, would you treat £1m of benefits or costs occurring in ten years’ time the same as £1m of benefits and costs occurring next year? Explain.

- Is it inevitable that events occurring in the future will at best be known unknowns?

- If you make a statement that something will occur in the future and you turn out to be wrong, was your statement a positive one or a normative one?

- What would be the likely effects of Scottish independence on the current account of the balance of payments (a) for Scotland; (b) for the rest if the UK?

- How does inequality in Scotland compare with that in the rest of the UK and in other countries? Why might Scottish independence lead to a reduction in inequality? (See the chapter on inequality in the book above edited by David Bell, David Eiser and Klaus B Beckmann.)

- One of the problems in assessing the arguments for a Yes vote is uncertainty over what would happen if there was a majority voting No. What might happen in terms of further devolution in the case of a No vote?

- Why is there uncertainty over the amount of national debt that would exist in Scotland if it became independent?

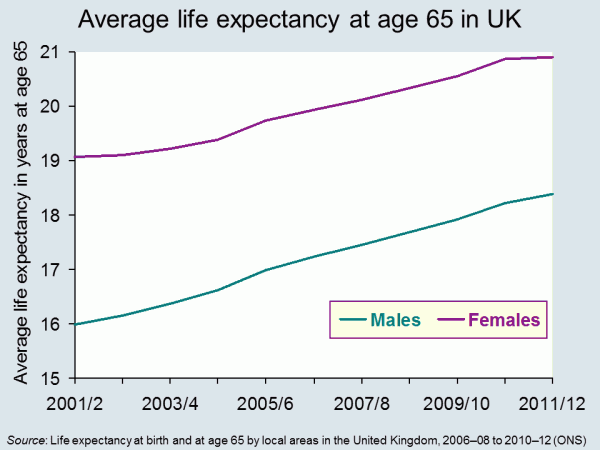

Life expectancy is increasing across the world and the latest set of figures from the Office for National Statistics show that in the UK it has passed 79 for boys born in 2010–12, and 82 for girls born then. In fact the prediction is that over a third of babies born in 2013 will live to more than 100. The data throws up some interesting questions. How well prepared are we for lives that last this long? And how evenly distributed is this increase in life expectancy? Pensions’ minister, Steve Webb, has called for better information on life expectancy to be shared. How would this impact on our decision making?

Life expectancy is increasing across the world and the latest set of figures from the Office for National Statistics show that in the UK it has passed 79 for boys born in 2010–12, and 82 for girls born then. In fact the prediction is that over a third of babies born in 2013 will live to more than 100. The data throws up some interesting questions. How well prepared are we for lives that last this long? And how evenly distributed is this increase in life expectancy? Pensions’ minister, Steve Webb, has called for better information on life expectancy to be shared. How would this impact on our decision making?

It seems reasonable to think that increasing life expectancy must be good news. And of course, for individuals it can be. In 1951 the average man retiring at 65, in England and Wales, could expect to live and draw a pension for another 12.1 years. By 2014 this had risen to 22 years.

But while we can look forward to longer life, for the government, it presents some challenges The first is that we just don’t save enough for our old age. This seems to be partly because we find it hard to make decisions that will have an impact so far in the future. There are a number of measures that have been put in place to encourage us to save more, including auto-enrolment into company pension schemes. This is being rolled out across businesses over the next three years. In the 2014 Budget, the Chancellor announced that people reaching retirement age will be able to draw all their pension as a cash lump sum, rather than having to take it as a regular income.

But while we can look forward to longer life, for the government, it presents some challenges The first is that we just don’t save enough for our old age. This seems to be partly because we find it hard to make decisions that will have an impact so far in the future. There are a number of measures that have been put in place to encourage us to save more, including auto-enrolment into company pension schemes. This is being rolled out across businesses over the next three years. In the 2014 Budget, the Chancellor announced that people reaching retirement age will be able to draw all their pension as a cash lump sum, rather than having to take it as a regular income.

Another concern for government is the variations that we find in life expectancy across the UK. The 2014 ONS data identified that life expectancy for men born in Glasgow in 2012 is 72.6, in East Dorset it is 82.9. 25% of those in Glasgow are not expected to live to 65. The gap in years of good health is even greater. This presents governments with a long-term problem. How do they achieve greater equality in this instance? Do they focus resources on the areas that need it most? Do they legislate to address behaviour? Or do they rely on the provision of good advice – on diet, exercise and other factors?

Information has a role to play in both areas identified above. In April 2014, Steve Webb, suggested that in order to make good decisions at the point of retirement, people need to understand more about what lies ahead. He said:

People tend to underestimate how long they’re likely to live, so we’re talking about averages, something very broad-brush. Based on your gender, based on your age, perhaps asking one or two basic questions, like whether you’ve smoked or not, you can tell somebody that they might, on average, live for another 20 years or so.

This suggestion has led to some concerns being expressed at what appears to be an over-simplistic approach. Estimates can only be based on a mix of averages modified by individual information. Would the projections be shared with pension providers? What would you do if you exceeded your forecast life expectancy – by a long way – and had spent all your money? Could you sue someone?

Will your pension pot last as long as you will? The Telegraph, Dan Hyde and Richard Dyson (23/4/2014)

Scientists invent death test that will tell us how long we have to live Metro (11/8/13)

Games host Glasgow has worst life expectancy in the UK The Guardian, Caroline Davies (16/4/2014)

Pensioners could get life expectancy guidance BBC News Politics (17/4/14)

ONS reveals gaps in life expectancy across the UK FT Adviser Pensions, Kevin White (23/4/14)

Health care aid for developing countries boosts life expectancy Health Canal, Ruth Ann Richter (22/4/14)

A third of babies born this year will live to 100 This is Money.co.uk, Adam Uren (11/12/13)

Questions

- Thinking about the UK, what are the factors that might explain variations in life expectancy across different regions? How might the government address these differences? Why would they want to do so?

- Do the same factors explain variations between countries? Who can address these differences? Who would want to do so?

- If you could have a reasonable prediction of your life expectancy at 65, would you want it? How would your behaviour change if you were predicted a longer than average life expectancy? How would it change if you were predicted a shorter than average life expectancy?

- If you could have an accurate prediction of your life expectancy at 18, how would your answers differ? If this were possible, would it present any problems?

Interest rates are the main tool of monetary policy and crucially affect investment. There has been much discussion since the end of the financial crisis concerning when UK interest rates would eventually rise. Uncertainty over just when, and by how much, interest rates will rise affects business confidence and hence investment. Businesses therefore listen carefully to what the Bank of England says about future movements in Bank Rate. But Mark Carney has now spoken about another cause of uncertainty and its impct on investment. This is the uncertainty over the outcome of the referendum on whether the UK should leave the EU.

Interest rates are the main tool of monetary policy and crucially affect investment. There has been much discussion since the end of the financial crisis concerning when UK interest rates would eventually rise. Uncertainty over just when, and by how much, interest rates will rise affects business confidence and hence investment. Businesses therefore listen carefully to what the Bank of England says about future movements in Bank Rate. But Mark Carney has now spoken about another cause of uncertainty and its impct on investment. This is the uncertainty over the outcome of the referendum on whether the UK should leave the EU.