Policymakers around the world have used Gross Domestic Product as the main gauge of economic performance – and have often adopted policies that aim to maximise its rate of growth. Generation after generation of economists have committed significant time and effort to thinking about the factors that influence GDP growth, on the premise that an expanding and healthy economy is one that sees its GDP increasing every year at a sufficient rate.

Policymakers around the world have used Gross Domestic Product as the main gauge of economic performance – and have often adopted policies that aim to maximise its rate of growth. Generation after generation of economists have committed significant time and effort to thinking about the factors that influence GDP growth, on the premise that an expanding and healthy economy is one that sees its GDP increasing every year at a sufficient rate.

But is economic output a good enough indicator of national economic wellbeing? Costanza et al (2014) (see link below) argue that, despite its merits, GDP can be a ‘misleading measure of national success’:

GDP measures mainly market transactions. It ignores social costs, environmental impacts and income inequality. If a business used GDP-style accounting, it would aim to maximize gross revenue — even at the expense of profitability, efficiency, sustainability or flexibility. That is hardly smart or sustainable (think Enron). Yet since the end of the Second World War, promoting GDP growth has remained the primary national policy goal in almost every country. Meanwhile, researchers have become much better at measuring what actually does make life worthwhile. The environmental and social effects of GDP growth is a misleading measure of national success. Countries should act now to embrace new metrics.

The limitations of GDP growth as a measure of economic wellbeing and national strength are becoming increasingly clear in today’s world. Some of the world’s wealthiest countries are plagued by discontent, with a growth in populism and social discontent – attitudes which are often fuelled by high rates of poverty and economic hardship. In a recent report titled ‘The Living Standards Audit 2018’ published by the Resolution Foundation, a UK economic thinktank (see link below), the authors found that child poverty rose in 2016–17 as a result of declining incomes of the poorest third of UK households:

The limitations of GDP growth as a measure of economic wellbeing and national strength are becoming increasingly clear in today’s world. Some of the world’s wealthiest countries are plagued by discontent, with a growth in populism and social discontent – attitudes which are often fuelled by high rates of poverty and economic hardship. In a recent report titled ‘The Living Standards Audit 2018’ published by the Resolution Foundation, a UK economic thinktank (see link below), the authors found that child poverty rose in 2016–17 as a result of declining incomes of the poorest third of UK households:

While the economic profile of UK households has changed, living standards – with the exception of pensioner households – have mostly stagnated since the mid-2000s. Typical household incomes are not much higher than they were in 2003–04. This stagnation in living standards for many has brought with it a rise in poverty rates for low to middle income families. Over a third of low to middle income families with children are in poverty, up from a quarter in the mid-2000s, and nearly two-fifths say that they can’t afford a holiday away for their children once a year. On the other hand, the share of non-working families in poverty has fallen, though not by enough to prevent an overall rise in poverty since 2010.

Their projections also show that this rise in poverty was likely to have continued in 2017–18:

Although the increase in broad measures of inequality were relatively muted last year, our nowcast suggests that there was a pronounced rise in poverty (measured after housing costs[…]. The increase in overall poverty (from 22.1 to 23.2 per cent) was the largest since 1988. But this was dwarfed by the increase in child poverty, which rose from 30.3 per cent to 33.4 per cent. […]The fortunes of middle-income households diverged from those towards the bottom of the distribution and so a greater share of households, and children, found themselves below the poverty threshold.

A simple literature search on Scope (or even Google Scholar) shows that there has been a significant increase in the number of journal articles and reports in the last 10 years on this topic. We do talk more about the limitations of GDP, but we are still using it as the main measure of national economic performance.

Is it then time to stop focusing our attention on GDP growth exclusively and start considering broader metrics of social development? And what would such metrics look like? Both interesting questions that we will try to address in coming blogs.

Articles

Report

Data

Hearing

Questions

- What are the main strengths and weakness of using GDP as measure of economic performance?

- Is high GDP growth alone enough to foster economic and social wellbeing? Explain your answer using examples.

- Write a list of alternative measures that could be used alongside GDP-based metrics to measure economic and social progress. Explain your answer.

When did you last think about buying a new car? If not recently, then you may be in for a surprise next time you shop around for car deals. First, you will realise that the range of hybrid cars (i.e. cars that combine conventional combustion and electric engines) has widened significantly. The days when you only had a choice of Toyota Prius and another two or three hybrids are long gone! A quick search on the web returned 10 different models (although five of them belong to the Toyota Prius family), including Chevrolet Malibu, VW Jetta and Ford Fusion. And these are only the cars that are currently available in the UK market.

When did you last think about buying a new car? If not recently, then you may be in for a surprise next time you shop around for car deals. First, you will realise that the range of hybrid cars (i.e. cars that combine conventional combustion and electric engines) has widened significantly. The days when you only had a choice of Toyota Prius and another two or three hybrids are long gone! A quick search on the web returned 10 different models (although five of them belong to the Toyota Prius family), including Chevrolet Malibu, VW Jetta and Ford Fusion. And these are only the cars that are currently available in the UK market.

But the biggest surprise of all may be the number of purely (plug-) electric cars that are available to UK buyers these days. The table below provides a summary of total registrations of light-duty plug-electric cars by model in the UK, between 2010 and June 2016.

Source: Wikipedia, “Plug-in electric vehicles in the United Kingdom”

In 2010 there were nly 138 electric vehicles in total registered in the UK. They were indeed an unusual sight at that time – and good luck to you if you had one and you happened to run out of power in the middle of a journey. In 2011 this (small) number increased sevenfold – an increase that was driven mostly by the successful introduction of Nissan Leaf (635 electric Nissans were registered in the UK that year). And since then the number of electric vehicles registered in the country has increased with spectacular speed, at an average rate of 252% per year.

There is clearly strong interest in electric vehicles – an interest likely to increase as their price becomes more competitive. However, they are still very expensive items to buy, especially when compared with their conventional fuel-engine counterparts. What makes electric cars expensive? One thing is the cost of purchasing and maintaining a battery that can deliver a reasonable range. But the cost of batteries is falling, as more and more companies realise the potential of this new market and join the R&D race. As mentioned in a special report that was published recently in the FT:

The cost of lithium-ion batteries has fallen by 75 per cent over the past eight years, measured per kilowatt hour of output. Every time battery production doubles, costs fall by another 5 per cent to 8 per cent, according to analysts at Wood Mackenzie.

There is no doubt that more research will result in more efficient batteries, and will increase the interest in electric cars not only by consumers but also by producers, who already see the opportunity of this new global market.  Does this mean that prices will necessarily fall further? You might think so, but then you have to take into consideration the availability and cost of mining further raw materials to make these batteries (such as cobalt, which is one of the materials used in the making of lithium-ion batteries and nearly half of which is currently sourced from the Democratic Republic of Congo). This may lead to bottlenecks in the production of new battery units. In which case, the price of batteries (and, by extension, the price of electric cars) may not fall much further until some new innovation happens that changes either the material or its efficiency.

Does this mean that prices will necessarily fall further? You might think so, but then you have to take into consideration the availability and cost of mining further raw materials to make these batteries (such as cobalt, which is one of the materials used in the making of lithium-ion batteries and nearly half of which is currently sourced from the Democratic Republic of Congo). This may lead to bottlenecks in the production of new battery units. In which case, the price of batteries (and, by extension, the price of electric cars) may not fall much further until some new innovation happens that changes either the material or its efficiency.

The good news is that a lot of researchers are currently looking into these questions, and innovation will do what it always does: give solutions to problems that previously appeared insurmountable. They had better be fast because, according to estimates by Wood Mackenzie, the number of electric vehicles globally is expected to rise by over 50 times – from 2 million (in 2017) to over 125 million by 2035.

How many economists does it take to charge an electric car? I guess we are going to find out!

Articles

Information

Questions

- Using a demand and supply diagram, explain the relationship between the price of a battery and the market (equilibrium) price of a plug-in electric vehicle.

- List all non-price factors that influence demand for plug-in electric vehicles. Briefly explain each.

- Should the government subsidise the development and production of electric car batteries? Explain the advantages and disadvantages of such intervention and take a position.

Ten years ago, the financial crisis deepened and stock markets around the world plummeted. The trigger was the collapse of Lehman Brothers, the fourth-largest US investment bank. It filed for bankruptcy on September 15, 2008. This was not the first bank failure around that time. In 2007, Northern Rock in the UK (Aug/Sept 2007) had collapsed and so too had Bear Stearns in the USA (Mar 2008).

Ten years ago, the financial crisis deepened and stock markets around the world plummeted. The trigger was the collapse of Lehman Brothers, the fourth-largest US investment bank. It filed for bankruptcy on September 15, 2008. This was not the first bank failure around that time. In 2007, Northern Rock in the UK (Aug/Sept 2007) had collapsed and so too had Bear Stearns in the USA (Mar 2008).

Initially there was some hope that the US government would bail out Lehmans. But when Congress rejected the Bank Bailout Bill on September 29, the US stock market fell sharply, with the Dow Jones falling by 7% the same day. This was mirrored in other countries: the FTSE 100 fell by 15%.

At the core of the problem was excessive lending by banks with too little capital. What is more, much of the capital was of poor quality. Many of the banks held securitised assets containing ‘sub-prime mortgage debt’. The assets, known as collateralised debt obligations (CDOs), were bundles of other assets, including mortgages. US homeowners had been lent money based on the assumption that their houses would increase in value. When house prices fell, homeowners were left in a position of negative equity – owing more than the value of their house. With many people forced to sell their houses, prices fell further. Mortgage debt held by banks could not be redeemed: it was ‘sub-prime’ or ‘toxic debt’.

Response to the crisis

The outcome of the financial crash was a series of bailouts of banks around the world. Banks cut back on lending and the world headed for a major recession.

Initially, the response of governments and central banks was to stimulate their economies through fiscal and monetary policies. Government spending was increased; taxes were cut; interest rates were cut to near zero. By 2010, the global economy seemed to be pulling out of recession.

However, the expansionary fiscal policy, plus the bailing out of banks, had led to large public-sector deficits and growing public-sector debt. Although a return of economic growth would help to increase revenues, many governments felt that the size of the public-sector deficits was too large to rely on economic growth.

As a result, many governments embarked on a period of austerity – tight fiscal policy, involving cutting government expenditure and raising taxes. Although this might slowly bring the deficit down, it slowed down growth and caused major hardships for people who relied on benefits and who saw their benefits cut. It also led to a cut in public services.

Expanding the economy was left to central banks, which kept monetary policy very loose. Rock-bottom interest rates were then accompanied by quantitative easing. This was the expansion of the money supply by central-bank purchases of assets, largely government bonds. A massive amount of extra liquidity was pumped into economies. But with confidence still low, much of this ended up in other asset purchases, such as stocks and shares, rather than being spent on goods and services. The effect was a limited stimulation of the economy, but a surge in stock market prices.

Expanding the economy was left to central banks, which kept monetary policy very loose. Rock-bottom interest rates were then accompanied by quantitative easing. This was the expansion of the money supply by central-bank purchases of assets, largely government bonds. A massive amount of extra liquidity was pumped into economies. But with confidence still low, much of this ended up in other asset purchases, such as stocks and shares, rather than being spent on goods and services. The effect was a limited stimulation of the economy, but a surge in stock market prices.

With wages rising slowly, or even falling in real terms, and with credit easy to obtain at record low interest rates, so consumer debt increased.

Lessons

So have the lessons of the financial crash been learned? Would we ever have a repeat of 2007–9?

On the positive side, financial regulators are more aware of the dangers of under capitalisation. Banks’ capital requirements have increased, overseen by the Bank for International Settlements. Under its Basel II and then Basel III regulations (see link below), banks are required to hold much more capital (‘capital buffers’). Some countries’ regulators (normally the central bank), depending on their specific conditions, exceed these the Basel requirements.

But substantial risks remain and many of the lessons have not been learnt from the financial crisis and its aftermath.

There has been a large expansion of household debt, fuelled by low interest rates. This constrains central banks’ ability to raise interest rates without causing financial distress to people with large debts. It also makes it more likely that there will be a Minsky moment, when a trigger, such as a trade war (e.g. between the USA and China), causes banks to curb lending and consumers to rein in debt. This can then lead to a fall in aggregate demand and a recession.

Total debt of the private and public sectors now amounts to $164 trillion, or 225% of world GDP – 12 percentage points higher than in 2009.

China poses a considerable risk, as well as being a driver of global growth. China has very high levels of consumer debt and many of its banks are undercapitalised. It has already experienced one stock market crash. From mid-June 2015, there was a three-week fall in share prices, knocking about 30% off their value. Previously the Chinese stock market had soared, with many people borrowing to buy shares. But this was a classic bubble, with share prices reflecting exuberance, not economic fundamentals.

It has already experienced one stock market crash. From mid-June 2015, there was a three-week fall in share prices, knocking about 30% off their value. Previously the Chinese stock market had soared, with many people borrowing to buy shares. But this was a classic bubble, with share prices reflecting exuberance, not economic fundamentals.

Although Chinese government purchases of shares and tighter regulation helped to stabilise the market, it is possible that there may be another crash, especially if the trade war with the USA escalates even further. The Chinese stock market has already lost 20% of its value this year.

Then there is the problem with shadow banking. This is the provision of loans by non-bank financial institutions, such as insurance companies or hedge funds. As the International Business Times article linked below states:

A mind-boggling study from the US last year, for example, found that the market share of shadow banking in residential mortgages had rocketed from 15% in 2007 to 38% in 2015. This also represents a staggering 75% of all loans to low-income borrowers and risky borrowers. China’s shadow banking is another major concern, amounting to US$15 trillion, or about 130% of GDP. Meanwhile, fears are mounting that many shadow banks around the world are relaxing their underwriting standards.

Another issue is whether emerging markets can sustain their continued growth, or whether troubles in the more vulnerable emerging-market economies could trigger contagion across the more exposed parts of the developing world and possibly across the whole global economy. The recent crises in Turkey and Argentina may be a portent of this.

Then there is a risk of a cyber-attack by a rogue government or criminals on key financial insitutions, such as central banks or major international banks. Despite investing large amounts of money in cyber-security, financial institutions worry about their vulnerability to an attack.

Then there is a risk of a cyber-attack by a rogue government or criminals on key financial insitutions, such as central banks or major international banks. Despite investing large amounts of money in cyber-security, financial institutions worry about their vulnerability to an attack.

Any of these triggers could cause a crisis of confidence, which, in turn, could lead to a fall in stock markets, a fall in aggregate demand and a recession.

Finally there is the question of the deep and prolonged crisis in capitalism itself – a crisis that manifests itself, not in a sudden recession, but in a long-term stagnation of the living standards of the poor and ‘just about managing’. Average real weekly earnings in many countries today are still below those in 2008, before the crash. In Great Britain, real weekly earnings in July 2018 were still some 6% lower than in early 2008.

Articles

- The Lehman Brothers Crash And The Chaos That Followed – Everything You Need To Know

HuffPost, Isabel Togoh (15/9/18)

- Ten years after the crash: have the lessons of Lehman been learned?

The Guardian, Yanis Varoufakis, Ann Pettifor, Mark Littlewood, David Blanchflower, Olli Rehn, Nicky Morgan and Micah White (14/9/18)

- Financial crisis 10 years on: Who are the winners and losers?

Independent, Kate Hughes (14/9/18)

- Investment winners and losers 10 years after the crash

Financial Times, Kate Beioley (14/9/18)

- Nine Lessons From the Global Financial Crisis

Bloomberg, Mohamed A. El-Erian (13/9/18)

- Lehman — why we need a change of mindset

Deutsche Welle, Thomas Straubhaar (14/9/18)

- ‘The world is sleepwalking into a financial crisis’ – Gordon Brown

The Guardian, Larry Elliott (12/9/18)

Economists warn of new financial crisis on anniversary of 2008 crash

Economists warn of new financial crisis on anniversary of 2008 crashChannel 4 news, Helia Ebrahimi (15/9/18)

- Financial crisis 2008: Five biggest risks of a new crash

International Business Times, Nafis Alam (14/9/18)

- Carney warns against complacency on 10th anniversary of financial crisis

BBC News, Kamal Ahmed (12/9/18)

- A cyberattack could trigger the next financial crisis, new report says

CNBC, Bob Pisani (13/9/18)

Information and data

Questions

- Explain the major causes of the financial market crash in 2008.

- Would it have been a good idea to have continued with expansionary fiscal policy beyond 2009?

- Summarise the Basel III banking regulations.

- How could quantitative easing have been differently designed so as to have injected more money into the real sector of the economy?

- What are the main threats to the global economy at the current time? Are any of these a ‘hangover’ from the 2007–8 financial crisis?

- What is meant by ‘shadow banking’ and how might this be a threat to the future stability of the global economy?

- Find data on household debt in two developed countries from 2000 to the present day. Chart the figures. Explain the pattern that emerges and discuss whether there are any dangers for the two economies from the levels of debt.

I admit it, the title of my blog today is a little bit misleading – but at the same time very appropriate for today’s topic. Nancy Sinatra certainly wasn’t thinking about emigration when she was singing this song – it had nothing to do with it, after all. It is, however, very relevant to economists: Indeed, there are many economics papers discussing the effects of skilled immigration on host and source economies and regions.

I admit it, the title of my blog today is a little bit misleading – but at the same time very appropriate for today’s topic. Nancy Sinatra certainly wasn’t thinking about emigration when she was singing this song – it had nothing to do with it, after all. It is, however, very relevant to economists: Indeed, there are many economics papers discussing the effects of skilled immigration on host and source economies and regions.

Economists often use the term ‘brain drain’ to describe the migration of highly skilled workers from poor/developing to rich/developed economies. Such flows are anything but unusual. As The Economist points out in a recent article, ‘[I]n the decade to 2010–11 the number of university-educated migrants in the G20, a group of large economies that hosts two-thirds of the world’s migrants, grew by 60% to 32m according to the OECD, a club of mostly rich countries.’.

The effects of international migration are found to be overwhelmingly positive for both skilled migrant workers and their hosts. This is particularly true for highly skilled workers (such as academics, physicians and other professionals), who, through emigration, get the opportunity to earn a significantly higher return on their skills that what they might have had in their home country. Very often their home country is saturated and oversupplied with skilled workers competing for a very limited number of jobs. Also, they get the opportunity to practise their profession – which they might not have had otherwise.

But what about their home countries? Are they worse off for such emigration?

But what about their home countries? Are they worse off for such emigration?

There are different views when it comes to answering this question. One argument is that the prospect of international migration incentivises people in developing countries to accumulate skills (brain gain) – which they might not choose to do otherwise, if the expected return to skills was not high enough to warrant the effort and opportunity cost that comes with it. Beine et al (2011) find that:

Our empirical analysis predicts conditional convergence of human capital indicators. Our findings also reveal that skilled migration prospects foster human capital accumulation in low-income countries. In these countries, a net brain gain can be obtained if the skilled emigration rate is not too large (i.e. it does not exceed 20–30% depending on other country characteristics). In contrast, we find no evidence of a significant incentive mechanism in middle-income, and not surprisingly, high-income countries.

Other researchers find that emigration can have a significant negative effect on source economies (countries or regions) – especially if it affects a large share of the local workforce within a short time period. Ha et al (2016), analyse the effect of emigration on human capital formation and economic growth of Chinese provinces:

First, we find that permanent emigration is conducive to the improvement of both middle and high school enrollment. In contrast, while temporary emigration has a significantly positive effect on middle school enrollment it does not affect high school enrollment. Moreover, the different educational attainments of temporary emigrants have different effects on school enrollment. Specifically, the proportion of temporary emigrants with high school education positively affects middle school enrollment, while the proportion of temporary emigrants with middle school education negatively affects high school enrollment. Finally, we find that both permanent and temporary emigration has a detrimental effect on the economic growth of source regions.

So yes or no? Good or bad? As everything else in economics, the answer quite often is ‘it depends’.

Articles

- Open future: What educated people from poor countries make of the “brain drain” argument

The Economist, R.S. (27/8/18)

- Brain drain, brain gain, and economic growth in China

China Economic Review, Wei Ha, Junjian Yi and Junsen Zhang (April 2016)

- A Panel Data Analysis of the Brain Gain

World Development, Michel Beine, Ric Docquier and Cecily Oden-Defoort (Vol 39, No 4, pp 523–532, 2011)

Questions

- ‘The brain drain makes a bad situation worse, by stripping developing economies of their most valuable assets: skilled workers’. Discuss.

- Using Google, find data on the inflows and outflows of skilled labour for a developing country of your choice. Explain your results.

- ‘Brain drain’ or ‘brain gain’? What is your personal view on this debate? Explain your opinion by using anecdotal evidence, personal experience and examples.

- Referring to the previous question, write a critique of your answer.

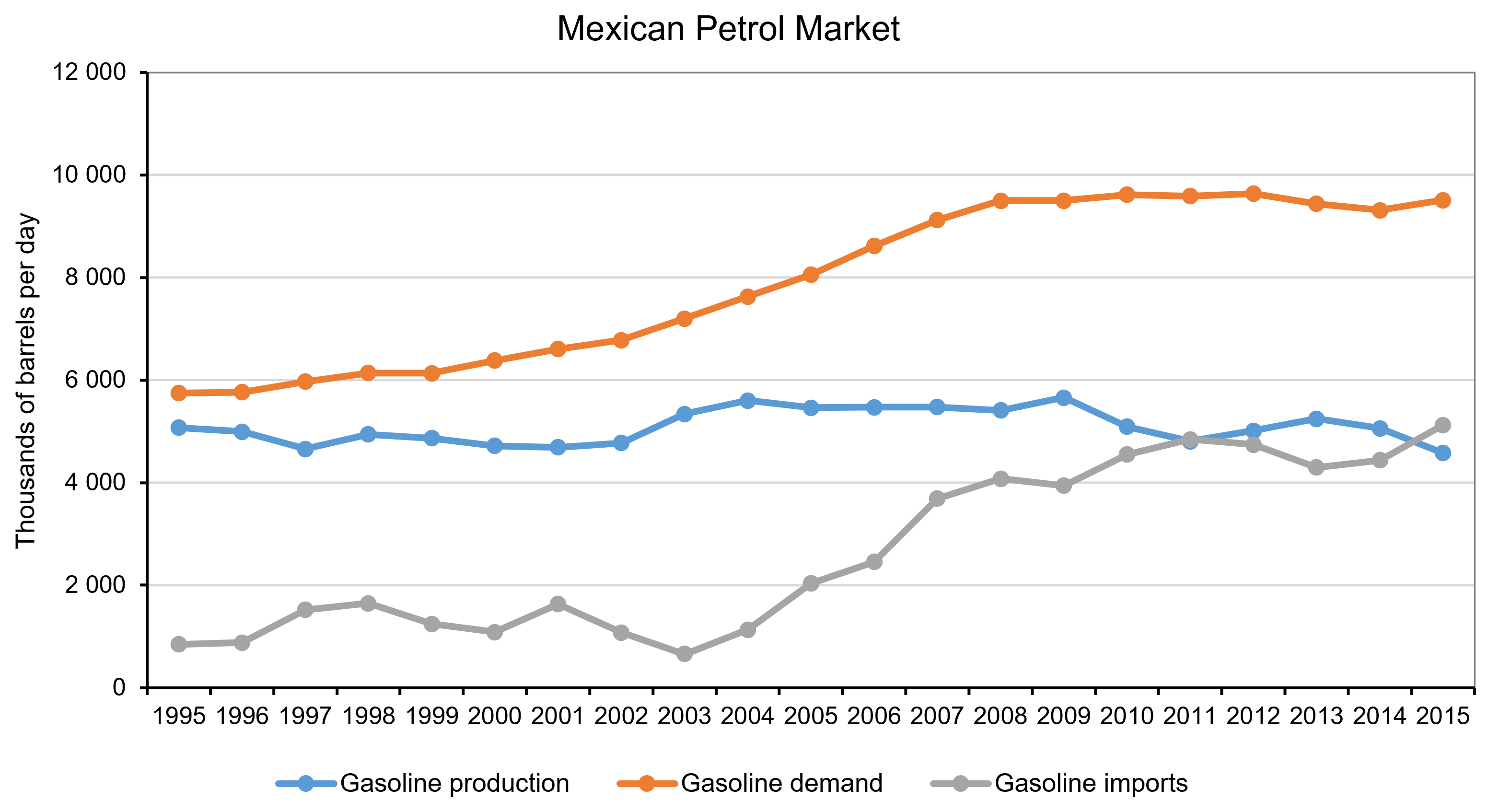

So here we are, summer is over (or almost over if you’re an optimist) and we are sitting in front of our screens reminiscing about hot sunny days (at least I do)! There is no doubt, however: a lot happened in the world of politics and economics in the past three months. The escalation of the US-China trade war, the run on the Turkish lira, the (successful?) conclusion of the Greek bailout – these are all examples of major economic developments that took place during the summer months, and which we will be sure to discuss in some detail in future blogs. Today, however, I will introduce a topic that I am very interested in as a researcher: the liberalisation of energy markets in developing countries and, in particular, Mexico.

So here we are, summer is over (or almost over if you’re an optimist) and we are sitting in front of our screens reminiscing about hot sunny days (at least I do)! There is no doubt, however: a lot happened in the world of politics and economics in the past three months. The escalation of the US-China trade war, the run on the Turkish lira, the (successful?) conclusion of the Greek bailout – these are all examples of major economic developments that took place during the summer months, and which we will be sure to discuss in some detail in future blogs. Today, however, I will introduce a topic that I am very interested in as a researcher: the liberalisation of energy markets in developing countries and, in particular, Mexico.

Why Mexico? Well, because it is a great example of a large developing economy that has been attempting to liberalise its energy market and reverse price setting and monopolistic practices that go back several decades. Until very recently, the price of petrol in Mexico was set and controlled by Pemex, a state monopolist. This put Pemex under pressure since, as a sole operator, it was responsible for balancing growing demand and costs, even to the detriment of its own finances.

The petrol (or ‘gasoline’) price liberalisation started in May 2017 and took place in stages – starting in the North part of Mexico and ending in November of the same year in the central and southern regions of the country. The main objective was to address the notable decrease in domestic oil production that put at risk the ability of the country to meet demand; as well as Mexico’s increasing dependency on foreign markets affected by the surge of the international oil price. The government has spent the past five years trying to create a stronger regulatory framework, while easing the financial burden on the state and halting the decline in oil reserves and production. Unsurprisingly, opening up a monopolistic market turns out to be a complex and bumpy process.

Source: Author’s calculations using data from the Energy Information Bank, Ministry of Energy, Mexico

Source: Author’s calculations using data from the Energy Information Bank, Ministry of Energy, Mexico

Despite all the reforms, retail petrol prices have kept rising. Although part of this price rise is demand-driven, an increasing number of researchers highlight the significance of the distribution of oil-related infrastructure in determining price outcomes at the federal and regional (state) level. Saturation and scarcity of both distribution and storage infrastructure are probably the two most significant impediments to opening the sector up to competition (Mexico Institute, 2018). You see, the original design of these networks and the deployment of the infrastructure was not aimed at maximising efficiency of distribution – the price was set by the monopolist and, in a way that was compliant with government policy (Mexico Institute, 2018). Economic efficiency was not always part of this equation. As a result, consumers located in better-deployed areas were subsidising the inherent logistics costs of less ‘well endowed’ regions by facing an artificially higher price than they would have in a competitive market.

But what about now? Do such differences in the allocation of infrastructure between regions lead to location-related differences in the price of petrol? If so, by how much? And, what policies should the government pursue to address such imbalances? These are all questions that I explore in one of my recent working papers titled ‘Widening the Gap: Lessons from the aftermath of the energy market reform in Mexico’ (with Hugo Vallarta) and I will be sharing some of the answers with you in a future blog.

Articles

Data

Questions

- Are state-owned monopolies effective in delivering successful market outcomes? Why yes, why no?

- In the case of Mexico, are you surprised about the complexities that were involved with opening up markets to competition? Explain why.

- Use Google to identify countries in which energy markets are controlled by state-owned monopolies.