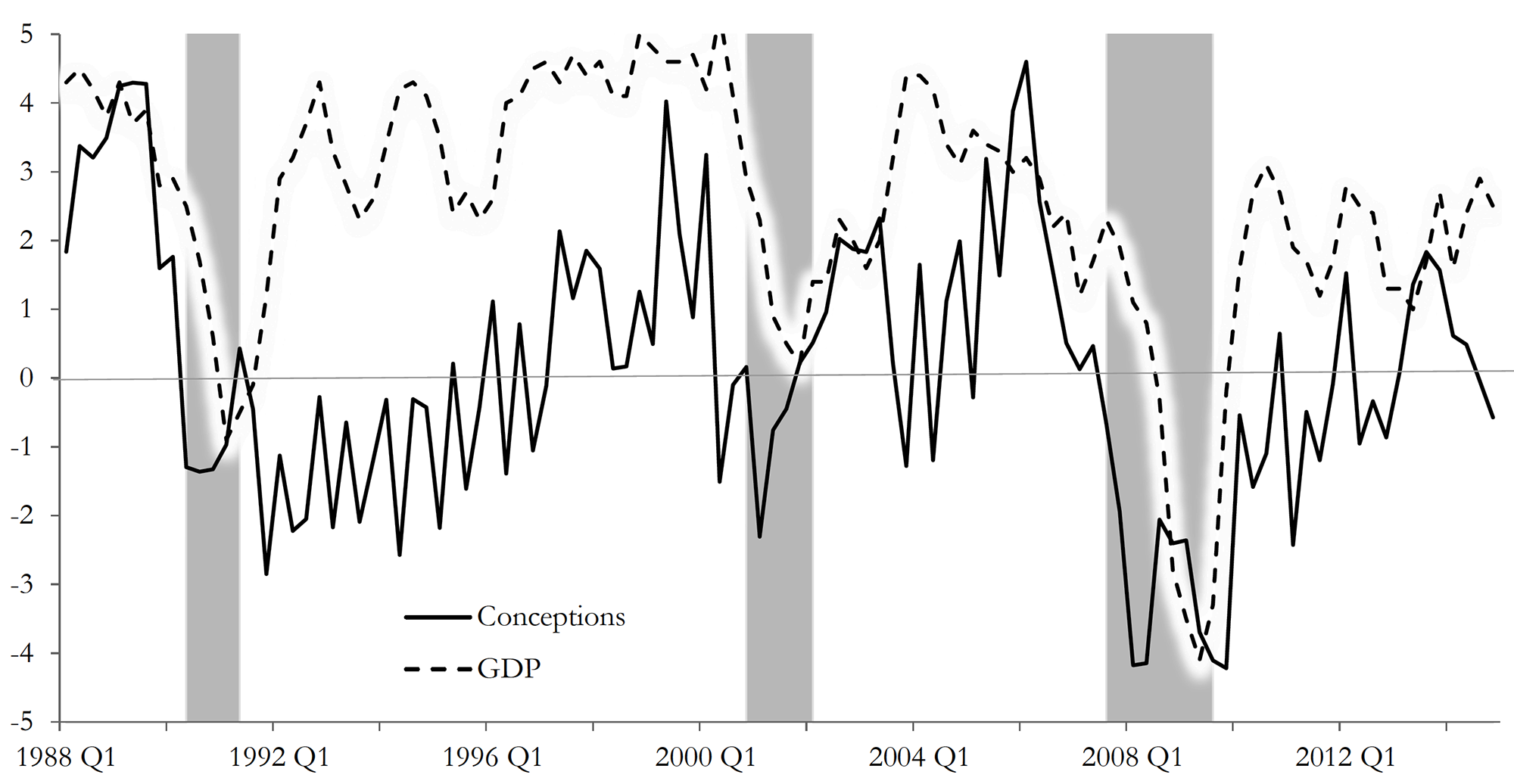

Would you start a family if you were pessimistic about the future of the economy? Buckles et al (2017) (see link below) believe that fewer of us would do so and, therefore, fertility rates could be used by investors and central banks as an early signal to pick up subtle changes in consumer confidence and overall economic climate.

Their study titled ‘Fertility is a leading economic indicator’ uses ‘live births’ data, sourced from US birth certificates, to explore if there is any association between fertility changes (measured as the rate of change in number of births) and GDP growth. Their results suggest that, in the case of the USA, there is: dips in fertility rates tend to precede by several quarters slowdown in economic activity. As the authors state:

The growth rate of conceptions declines prior to economic downturns and the decline occurs several quarters before recessions begin. Our measure of conceptions is constructed using live births; we present evidence suggesting that our results are indeed driven by changes in conceptions and not by changes in abortion or miscarriage. Conceptions compare well with or even outperform other economic indicators in anticipating recessions.

Conception and GDP Growth Rates (source Buckles et al p33: see below)

Although this is not the first piece of academic writing to claim that fertility has pro-cyclical qualities (see for instance, Adsera (2004, 2011), Adsera and Menendez (2011), Currie and Schwandt (2014) and Chatterjee and Vogle (2016) linked below), it is, to the best of our knowledge, the most recent paper (in terms of data used) to depict this relationship and to explore the suitability of fertility as a macroeconomic indicator to predict recessions.

Economies, after all, are groups of people who participate actively in day-to-day production and consumption activities – as consumers, workers and business leaders. Changes in their environment should affect their expectations about the future.

Are people, however, forward-looking enough to guide their current behaviours by their expectations of future economic outcomes? They may be, according to the findings of this study.

Did you know, for instance, that sales of ties tend to increase in economic downturns, as men buy more ties to show that they are working harder, in fear of losing their job[1]? But this is probably a topic for another blog.

Give two reasons why fertility rates may be a good indicator of economic activity.

Give two reasons why fertility rates may NOT be a good indicator of economic activity.

Do a literature search to identify and explain an ‘unorthodox’ macroeconomic indicator of your choice, and how it has been used to track economic activity.

The Winter Olympics are full on as athletes from all over the world compete against each other, hoping to set new world records, win medals and be known as Olympians. Pyeongchang, the South Korean county that hosts the 2018 Winter games, enjoys a large influx of tourists – estimated at 80,000 people a day. This is certainly an unusually large number of tourists for a region that has a regular winter-time population of no more than 45,000 people.

Having such a high number of visitors to the Winter Olympics, and even more to the larger Summer Olympics, is not an unusual occurrence, however, and it is often mentioned as one of the benefits of being a host to the Olympic Games.

Baade and Matheson (see link below) distinguish between three key benefits of hosting the Olympic Games: “the short-run benefits of tourist spending during the Games; the long-run benefits or the ‘Olympic legacy’, which might include improvements in infrastructure and increased trade, foreign investment, or tourism after the Games; and intangible benefits such as the ‘feel-good effect’ or civic pride”.

On these grounds, a number of studies have been authored, attempting to analyse some or all of these benefits, distinguishing between short-term and long-term effects. Müller (see link below), uses data from the 2014 Oympic Games in Sochi, Russia, to assess the net economic outcome for the host region. He concludes that any short-term economic benefits caused by the investment influx (before and during the games) could not offset the long-term costs, leading to an estimated net loss of $1.2 billion per year.

Zimbalist (2015) and Szymanski (2011) report similar results when analysing data from the London Games (2012) and past major sporting events (Games and FIFA World Cup). Kasimati (2003) points out the significant economic benefits that host regions tend to enjoy for years after hosting the games, but argues that the overall effect depends on a number of factors (including pre-existing infrastructure and location).

The jury is, therefore, still out on what is the overall economic effect of being host to this ancient institution. But I must now dash as women’s hockey is soon to start. “Let everyone shine”.

Using supply and demand diagrams, explain whether you would expect hotel room prices to change during the hosting of a major sports event, such as the Winter Olympics.

List three economic (or economics-related) arguments in favour of and against the hosting of the Olympic games. Relate your answer to the empirical evidence presented in the literature.

Why is it so difficult to estimate with accuracy the net economic effect of the Olympic Games?

These are challenging times for business. Economic growth has weakened markedly over the past 18 months with output currently growing at an annual rate of around 1.5 per cent, a percentage point below the long-term average. Spending power continues to be squeezed, with the annual rate of inflation in October reported to be running at 3.1 per cent compared to annual earnings growth of 2.5 per cent (see the squeeze continues). Moreover, consumer confidence remains fragile with households continuing to express particular concerns about the general economy and unemployment.

Here, we update our blog of July 2016 which, following the UK vote to leave the European Union, noted the fears for UK growth as confidence fell sharply. Consumer confidence is frequently identified by macro-economists as an important source of economic volatility. Indeed many macro models use a change in consumer confidence as a means of illustrating how economic shocks affect a range of macro variables, including growth, employment and inflation. Many economists agree that, in the short term at least, falling levels of confidence adversely affect activity because aggregate demand falls as households spend less.

The European Commission’s confidence measure is collated from questions in a monthly survey. In the UK around 2000 individuals are surveyed. Across the EU as a whole over 41 000 people are surveyed. In the survey individuals are asked a series of 12 questions which are designed to provide information on spending and saving intentions. These questions include perceptions of financial well-being, the general economic situation, consumer prices, unemployment, saving and the undertaking of major purchases.

The responses elicit either negative or positive responses. For example, respondents may feel that over the next 12 months the financial situation of their household will improve a little or a lot, stay the same or deteriorate a little or a lot. A weighted balance of positive over negative replies can be calculated. The balance can vary from -100, when all respondents choose the most negative option, to +100, when all respondents choose the most positive option.

The European Commission’s principal consumer confidence indicator is the average of the balances of four of the twelve questions posed: the financial situation of households, the general economic situation, unemployment expectations (with inverted sign) and savings, all over the next 12 months. These forward-looking balances are seasonally adjusted. The aggregate confidence indicator is thought to track developments in households’ spending intentions and, in turn, likely movements in the rate of growth of household consumption.

Chart 1 shows the consumer confidence indicator for the UK. The long-term average of –8.6 shows that negative responses across the four questions typically outweigh positive responses. In November 2017 the confidence balance stood at -5.2 roughly on par with its value in the previous two months, though marginally up on values of close to -7 over the summer. However, as recently as the beginning of 2016 the aggregate confidence score was running at around +4. In this context, current levels do constitute a significant change in consumer sentiment, changes which do ordinarily mark similar turning points in economic activity.(Click here to download a PowerPoint of the chart.)

Chart 2 allows to look behind the European Commission’s headline confidence indicator for the UK by looking at its four component balances. From it, we can see a deterioration in all four components. However, by far the most significant change in the individual confidence balances has been the sharp deterioration in expectations for the general economy. In November the forward-looking general economic situation stood at -25.5, compared to its long-run average of -11.6. (Click here to download a PowerPoint of the chart.)

The fall in UK consumer confidence is even more stark when compared to developments in consumer confidence across the whole of the European Union and in the 19 countries that make up the Euro area. Chart 3 shows how UK consumer confidence recovered relatively more strongly following the financial crisis of the late 2000s. The headline confidence indicator rose strongly from the middle of 2013 and was consistently in positive territory during 2014, 2015 and into 2016. The fall in consumer confidence in the UK has seen the headline confidence measure fall below that for the EU and the euro area. (Click here to download a PowerPoint of the chart.)

Consumer (and business) confidence is closely linked to uncertainty. The circumstances following the UK vote to leave the EU have undoubtedly created the conditions for acute uncertainty. Uncertainty breeds caution. Economists sometimes talk about spending being affected by two conflicting motives: prudence and impatience. While impatience creates a desire for spending now, prudence pushes us towards saving and insuring ourselves against uncertainty and unforeseen events. The worry is that the twin forces of fragile confidence and squeezed real earning are weighting heavily in favour of prudence and patience (a reduction in impatience). Going forward, this could create the conditions for a sustained period of subdued growth which, if it were to impact heavily on firms’ investment plans, could adversely impact on the economy’s productive potential. The hope is that the Brexit negotiations can move apace to reduce uncertainty and limit uncertainty’s adverse impact on economic activity.

Draw up a series of factors that you think might affect consumer confidence.

Explain what you understand by a positive and a negative demand-side shock. How might changes in consumer confidence generate demand shocks?

Analyse the ways in which consumer confidence might affect economic activity.

Which of the following statements is likely to be more accurate: (a) Consumer confidence drives economic activity or (b) Economic activity drives consumer confidence?

What macroeconomic indicators would those compiling the consumer confidence indicator expect the indicator to predict?

Analyse the possible short-term and longer-term economic implications of a fall in consumer confidence.

How might uncertainty affect consumer confidence?

What do the concepts of impatience and prudence mean in the context of consumer spending? When consumer confidence falls which of these might become more significant for consumer spending?

UK CPI inflation rose to 3.1% in November. This has forced Mark Carney to write a letter of explanation to the Chancellor – something he is required to do if inflation is more than 1 percentage point above (or below) the target of 2%.

The rise in inflation over the past few months has been caused largely by the depreciation of sterling following the Brexit vote. But there have been other factors at play too. The dollar price of oil has risen by 32% over the past 12 months and there have been large international rises in the price of metals and, more recently, in various foodstuffs. For example, butter prices have risen by over 20% in the past year (although they have declined somewhat recently). Other items that have seen large price rises include books, computer games, clothing and public transport.

The rate of CPI inflation is the percentage increase in the consumer prices index over the previous 12 months. When there is a one-off rise in prices, such as a rise in oil prices, its effect on inflation will only last 12 months. After that, assuming the price does not rise again, there will be no more effect on inflation. The CPI will be higher, but inflation will fall back. The effect may not be immediate, however, as input price changes take a time to work through supply chains.

Given that the main driver of inflation has been the depreciation in sterling, once the effect has worked through in terms of higher prices, inflation will fall back. Only if sterling continued depreciating would an inflation effect continue. So, many commentators are expecting that the rate on inflation will soon begin to fall.

But what will have been the effect on real incomes? In the past 12 months, nominal average earnings have risen by around 2.5% (the precise figures will not be available for a month). This means that real average earnings have fallen by around 0.6%. (Click here for a PowerPoint of the chart.)

For many low-income families the effect has been more severe. Many have seen little or no increase in their pay and they also consume a larger proportion of items whose prices have risen by more than the average. Those on working-age benefits will be particularly badly hit as benefits have not risen since 2015.

If inflation does fall and if real incomes no longer fall, people will still be worse off unless real incomes rise back to the levels they were before they started falling. That could be some time off.

Apart from CPI inflation, what other measures of inflation are there? Explain their meaning.

Why is inflation of 2%, rather than 0%, seen as the optimal rate by most central banks?

Apart from the depreciation of sterling, what other effects is Brexit likely to have on living standards in the UK?

What are the arguments for and against the government raising benefits by the rate of CPI inflation?

If Europe and the USA continue to grow faster than the UK, what effect is this likely to have on the euro/pound and dollar/pound exchange rates? What determines the magnitude of this effect?

Unemployment is at its lowest level since 1975. Why, then, are real wages falling?

Why, in the light of inflation being above target, has the Bank of England not raised Bank Rate again in December (having raised it from 0.25% to 0.5% in November)?

Bitcoin was created in 2009 by an unknown person, or people, using the alias Satoshi Nakamoto. It is a digital currency in the form of a line of computer code. Bitcoins are like ‘electronic cash’ which can be held or used for transactions, with holdings and transactions heavily encrypted for security – hence it is a form of ‘crytocurrency’. People can buy and sell bitcoins for normal currencies as well as using them for transactions. People’s holdings are held in electronic ‘wallets’ and can be accessed on their computers or phones via the Internet. Transfers of bitcoins from one person or organisation to another are recorded in a public electronic ledger in the form of a ‘blockchain‘.

The supply of bitcoins is not controlled by central banks; rather, it is determined by a process known as ‘mining’. This involves individuals or groups solving complex and time-consuming mathematical problems and being rewarded with a new block of bitcoins.

The supply of bitcoins is currently growing at around 150 per hour and the current supply is around ₿16.7 million. However, the number of new bitcoins in a block is halved for every 210,000 blocks. This means that the rate of increase in the supply of bitcoins is slowing – the number generated being halved roughly every four years. The supply will eventually reach a maximum of ₿21 million, probably sometime in the next century, but around 99% will have been mined by around 2032.

The bitcoin bubble

The price of bitcoins has soared in recent months and especially in the past two. On 4 October, the price of a bitcoin was $4226; by 7 December it was nearly four times higher, at $16,858 – a rise of 399% in just nine weeks. Many people have claimed that this is a bubble, which will soon burst. Already there have been severe fluctuations. By December 10, for example, the price had fallen at one point to $13,152 – a fall of nearly 22% in just two days – only to recover to over $15,500 within a few hours.

So what determines the price of bitcoin? The simple answer is very straightforward – it’s determined by demand and supply. But what has been happening to demand and supply and why? And what will happen in the near and more distant future?

As we have seen, the supply is limited by the process of mining, which allows a relatively stable, but declining, increase. The explanation of the recent price rise and what will happen in the future lies on the demand side. Increasing numbers of people have been buying bitcoin, not because they want to use it for transactions, whether legitimate or illegal over the dark web, but because they want to invest in bitcoin. In other words, they want to hold bitcoin as an asset which is increasing in value. These people are known as ‘hodlers’ – a deliberate misspelling of ‘holders’.

But this speculation is of the destabilising form. The more prices have risen, the more people have bought bitcoin, thus pushing the price up further. This is a classic bubble, whereby the price does not reflect an underlying value, but rather the exuberance of buyers.

The problem with bubbles is that they will burst, but just when is virtually impossible to predict with any accuracy. If the price of bitcoins falls, what will happen next depends on how the fall is interpreted. It could be interpreted as a temporary fall, caused by some people cashing in to take advantage of the higher prices. At the same time, other people, believing that it is only a temporary fall, will rush to buy, snapping up bitcoins at the temporary low price. This ‘stabilising speculation’ will move the price back up again.

However, the fall in price may be seen as the bubble bursting, with even bigger falls ahead. In this case, people will rush to sell before it falls further, thereby pushing the price even lower. This destabilising speculation will amplify the fall in prices.

But even if the bubble does burst, people may believe that another bubble will then occur and, once they think the bottom has been reached, will thus start buying again and there will be a second speculative rise in the price.

The crash could be very short-lived. This happened with the second biggest cryptocurrency, Ethereum. On 21 June this year, the price at the beginning of the day was $360. It then began to fall during the say. Once its price reached $315, it then collapsed by 96% to $13 with massive selling, much of it automatic with computers programmed to sell when the price falls by more than a certain amount. But then, on the same day, it rebounded. Within minutes it had bounced back and was trading at $337 at the end of the day. It is now trading at around $450 – up from around $300 four weeks ago.

Whether the bubble in bitcoin has more to inflate, when it will burst, and when it will rebound and by how much, depends on people’s expectations. But what we are looking at here is people’s expectations of what other people are likely to do – in other words, of other people’s expectations, which in turn depend on their expectations of other people’s expectations. This situation is known as a Keynesian Beauty Contest (see the blog, A stock market beauty contest of the machines). Perhaps we need a crystal ball.

To what extent does Bitcoin meet the functions of money?

Why is bitcoin unsuitable for normal transactions?

To what extent is bitcoin like gold as a means of holding wealth?

How would you advise someone thinking of buying bitcoin today? Explain why.

Does a rapid rise in the price of an asset always indicate a bubble? Explain

To what extent is the current rise in the price of bitcoin similar to that of the tulip, Poseidon and Beanie Baby bubbles?

If bitcoin is appreciating relative to the dollar and other currencies, does this mean that the price of goods and services valued in bitcoin are falling? Explain.

Explain and comment on the following sentence from the first Conversation article: “Like any asset, Bitcoin has some fundamental value, even if only a hope value, or a value arising from scarcity.”

How might the introduction of futures trading in bitcoin impact on its price and the volatility of price swings?

Explain and assess the argument that the price trend of bitcoin is more likely to be an S curve rather than a roller coaster

Would you start a family if you were pessimistic about the future of the economy? Buckles et al (2017) (see link below) believe that fewer of us would do so and, therefore, fertility rates could be used by investors and central banks as an early signal to pick up subtle changes in consumer confidence and overall economic climate.

Would you start a family if you were pessimistic about the future of the economy? Buckles et al (2017) (see link below) believe that fewer of us would do so and, therefore, fertility rates could be used by investors and central banks as an early signal to pick up subtle changes in consumer confidence and overall economic climate.