The global economic impact of the coronavirus outbreak is uncertain but potentially very large. There has already been a massive effect on China, with large parts of the Chinese economy shut down. As the disease spreads to other countries, they too will experience supply shocks as schools and workplaces close down and travel restrictions are imposed. This has already happened in South Korea, Japan and Italy. The size of these effects is still unknown and will depend on the effectiveness of the containment measures that countries are putting in place and on the behaviour of people in self isolating if they have any symptoms or even possible exposure.

The OECD in its March 2020 interim Economic Assessment: Coronavirus: The world economy at risk estimates that global economic growth will be around half a percentage point lower than previously forecast – down from 2.9% to 2.4%. But this is based on the assumption that ‘the epidemic peaks in China in the first quarter of 2020 and outbreaks in other countries prove mild and contained.’ If the disease develops into a pandemic, as many health officials are predicting, the global economic effect could be much larger. In such cases, the OECD predicts a halving of global economic growth to 1.5%. But even this may be overoptimistic, with growing talk of a global recession.

Governments and central banks around the world are already planning measures to boost aggregate demand. The Federal Reserve, as an emergency measure on 3 March, reduced the Federal Funds rate by half a percentage point from the range of 1.5–1.75% to 1.0–1.25%. This was the first emergency rate cut since 2008.

Economic uncertainty

With considerable uncertainty about the spread of the disease and how effective containment measures will be, stock markets have fallen dramatically. The FTSE 100 fell by nearly 14% in the second half of February, before recovering slightly at the beginning of March. It then fell by a further 7.7% on 9 March – the biggest one-day fall since the 2008 financial crisis. This was specifically in response to a plunge in oil prices as Russia and Saudi Arabia engaged in a price war. But it also reflected growing pessimism about the economic impact of the coronavirus as the global spread of the epidemic accelerated and countries were contemplating more draconian lock-down measures.

Firms have been drawing up contingency plans to respond to panic buying of essential items and falling demand for other goods. Supply-chain managers are working out how to respond to these changes and to disruptions to supplies from China and other affected countries.

Firms are also having to plan for disruptions to labour supply. Large numbers of employees may fall sick or be advised/required to stay at home. Or they may have to stay at home to look after children whose schools are closed. For some firms, having their staff working from home will be easy; for others it will be impossible.

Some industries will be particularly badly hit, such as airlines, cruise lines and travel companies. Budget airlines have cancelled several flights and travel companies are beginning to offer substantial discounts. Manufacturing firms which are dependent on supplies from affected countries have also been badly hit. This is reflected in their share prices, which have seen large falls.

Longer-term effects

Uncertainty could have longer-term impacts on aggregate supply if firms decide to put investment on hold. This would also impact on the capital goods industries which supply machinery and equipment to investing firms. For the UK, already having suffered from Brexit uncertainty, this further uncertainty could prove very damaging for economic growth.

While aggregate supply is likely to fall, or at least to grow less quickly, what will happen to the balance of aggregate demand and supply is less clear. A temporary rise in demand, as people stock up, could see a surge in prices, unless supermarkets and other firms are keen to demonstrate that they are not profiting from the disease. In the longer term, if aggregate demand continues to grow at past rates, it will probably outstrip the growth in aggregate supply and result in rising inflation. If, however, demand is subdued, as uncertainty about their own economic situation leads people to cut back on spending, inflation and even the price level may fall.

How quickly the global economy will ‘bounce back’ depends on how long the outbreak lasts and whether it becomes a serious pandemic and on how much investment has been affected. At the current time, it is impossible to predict with any accuracy the timing and scale of any such bounce back.

VOX CEPR Policy Portal, Richard Baldwin, Beatrice Weder di Mauro eds (6/3/20)

Questions

Using a supply and demand diagram, illustrate the fall in stock market prices caused by concerns over the effects of the coronavirus.

Using either (i) an aggregate demand and supply diagram or (ii) a DAD/DAS diagram, illustrate how a fall in aggregate supply as a result of the economic effects of the coronavirus would lead to (a) a fall in real income and (i) a fall in the price level or (ii) a fall in inflation; (b) a fall in real income and (i) a rise in the price level or (ii) a rise in inflation.

What would be the likely effects of central banks (a) cutting interest rates; (b) engaging in further quantitative easing?

What would be the likely effects of governments running a larger budget deficit as a means of boosting the economy?

Distinguish between stabilising and destabilising speculation. How would you characterise the speculation that has taken place on stock markets in response to the coronavirus?

What are the implications of people being paid on zero-hour contracts of the government requiring workplaces to close?

What long-term changes to working practices and government policy could result from short-term adjustments to the epidemic?

Is the long-term macroeconomic impact of the coronavirus likely to be zero, as economies bounce back? Explain.

The linked article below, by Evan Davis, assesses the state of economics. He argues that economics has had some major successes over the years in providing a framework for understanding how economies function and how to increase incomes and well-being more generally.

Over the last few decades, economists have …had an influence over every aspect of our lives. …And during this era in which economists have reigned, the world has notched up some marked successes. The reduction in the proportion of human beings living in abject poverty over the last thirty years has been extraordinary.

With the development of concepts such as opportunity cost, the prisoners’ dilemma, comparative advantage and the paradox of thrift, economics has helped to shape the way policymakers perceive economic issues and policies.

These concepts are ‘threshold concepts’. Understanding and being able to relate and apply these core economic concepts helps you to ‘think like an economist’ and to relate the different parts of the subject to each other. Both Economics (10th edition) and Essentials of Economics (8th edition) examine 15 of these threshold concepts. Each time a threshold concept is used in the text, a ‘TC’ icon appears in the margin with the appropriate number. By locating them in this way, you can see their use in a variety of contexts.

But despite the insights provided by traditional economics into the various problems that society faces, the discipline of economics has faced criticism, especially since the financial crisis, which most economists did not foresee.

Even Davis identifies two major shortcomings of the discipline – both beginning with ‘C’. ‘One is complexity, the other is community.’

In terms of complexity, the criticism is that economic models are often based on simplistic assumptions, such as ‘rational maximising behaviour’. This might make it easier to express the models mathematically, but mathematical elegance does not necessarily translate into predictive accuracy. Such models do not capture the ‘messiness’ of the real world.

These models have a certain theoretical elegance but there is now an increasing sense that economies do not evolve along a well-defined mathematical path, but in a far more messy way. The individual players within the economy face radical uncertainty; they adapt and learn as they go; they watch what everybody else does. The economy stumbles along in a process of slow discovery, full of feedback loops.

As far as ‘community’ is concerned, people do not just act as self-interested individuals. Their actions are often governed by how other people behave and also by how their own actions will affect other people, such as family, friends, colleagues or society more generally.

And the same applies to firms. They will be influenced by various other firms, such as competitors, trend setters and suppliers and also by a range of stakeholders – not just shareholders, but also workers, customers, local communities, etc. A firm’s aim is thus unlikely to be simple short-term profit maximisation.

And this broader set of interests translates into policy. The neoliberal free-market, laissez-faire approach to policy is challenged by the desire to take account of broader questions of equity, community and social justice. However privately efficient a free market is, it does not take account of the full social and environmental costs and benefits of firms’ and consumers’ actions or a fair distribution of income and wealth.

It would be wrong, however, to say that economics has not responded to these complexities and concerns. The analysis of externalities, income distribution, incentives, herd behaviour, uncertainty, speculation, cumulative causation and institutional values and biases are increasingly embedded in the economics curriculum and in economic research. What is more, behavioural economics is becoming increasingly mainstream in examining the behaviour of consumers, workers, firms and government. We have tried to reflect these developments in successive editions of our four textbooks.

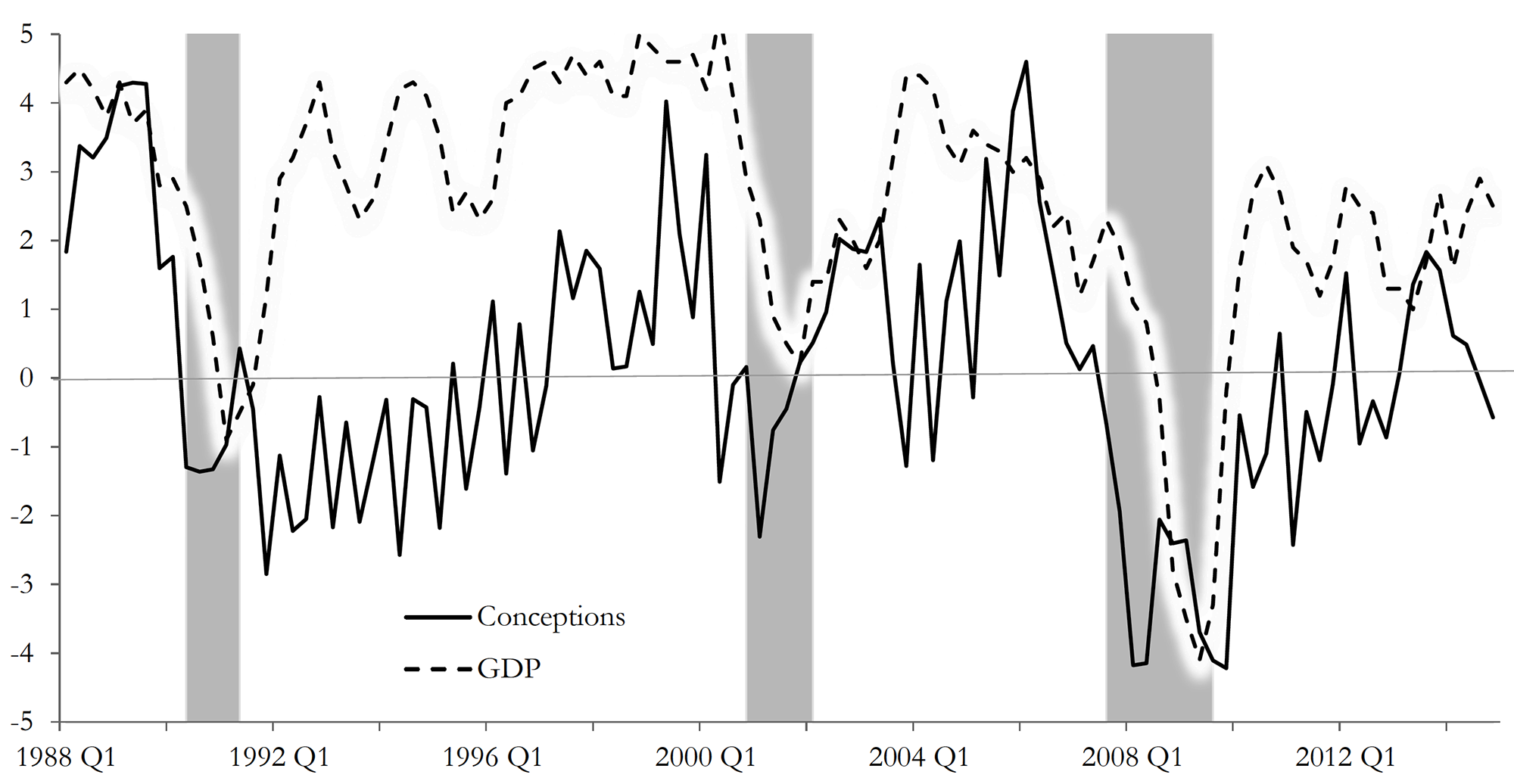

Would you start a family if you were pessimistic about the future of the economy? Buckles et al (2017) (see link below) believe that fewer of us would do so and, therefore, fertility rates could be used by investors and central banks as an early signal to pick up subtle changes in consumer confidence and overall economic climate.

Their study titled ‘Fertility is a leading economic indicator’ uses ‘live births’ data, sourced from US birth certificates, to explore if there is any association between fertility changes (measured as the rate of change in number of births) and GDP growth. Their results suggest that, in the case of the USA, there is: dips in fertility rates tend to precede by several quarters slowdown in economic activity. As the authors state:

The growth rate of conceptions declines prior to economic downturns and the decline occurs several quarters before recessions begin. Our measure of conceptions is constructed using live births; we present evidence suggesting that our results are indeed driven by changes in conceptions and not by changes in abortion or miscarriage. Conceptions compare well with or even outperform other economic indicators in anticipating recessions.

Conception and GDP Growth Rates (source Buckles et al p33: see below)

Although this is not the first piece of academic writing to claim that fertility has pro-cyclical qualities (see for instance, Adsera (2004, 2011), Adsera and Menendez (2011), Currie and Schwandt (2014) and Chatterjee and Vogle (2016) linked below), it is, to the best of our knowledge, the most recent paper (in terms of data used) to depict this relationship and to explore the suitability of fertility as a macroeconomic indicator to predict recessions.

Economies, after all, are groups of people who participate actively in day-to-day production and consumption activities – as consumers, workers and business leaders. Changes in their environment should affect their expectations about the future.

Are people, however, forward-looking enough to guide their current behaviours by their expectations of future economic outcomes? They may be, according to the findings of this study.

Did you know, for instance, that sales of ties tend to increase in economic downturns, as men buy more ties to show that they are working harder, in fear of losing their job[1]? But this is probably a topic for another blog.

Give two reasons why fertility rates may be a good indicator of economic activity.

Give two reasons why fertility rates may NOT be a good indicator of economic activity.

Do a literature search to identify and explain an ‘unorthodox’ macroeconomic indicator of your choice, and how it has been used to track economic activity.

The IMF has just published its six-monthly World Economic Outlook. It expects world aggregate demand and growth to remain subdued. A combination of worries about the effects of Brexit and slower-than-expected growth in the USA has led the IMF to revise its forecasts for growth for both 2016 and 2017 downward by 0.1 percentage points compared with its April 2016 forecast. To quote the summary of the report:

Global growth is projected to slow to 3.1 percent in 2016 before recovering to 3.4 percent in 2017. The forecast, revised down by 0.1 percentage point for 2016 and 2017 relative to April, reflects a more subdued outlook for advanced economies following the June UK vote in favour of leaving the European Union (Brexit) and weaker-than-expected growth in the United States. These developments have put further downward pressure on global interest rates, as monetary policy is now expected to remain accommodative for longer.

Although the market reaction to the Brexit shock was reassuringly orderly, the ultimate impact remains very unclear, as the fate of institutional and trade arrangements between the United Kingdom and the European Union is uncertain.

The IMF is pessimistic about the outlook for advanced countries. It identifies political uncertainty and concerns about immigration and integration resulting in a rise in demands for populist, inward-looking policies as the major risk factors.

It is more optimistic about growth prospect for some emerging market economies, especially in Asia, but sees a sharp slowdown in other developing countries, especially in sub-Saharan Africa and in countries generally which rely on commodity exports during a period of lower commodity prices.

With little scope for further easing of monetary policy, the IMF recommends the increased use of fiscal policies:

Accommodative monetary policy alone cannot lift demand sufficiently, and fiscal support — calibrated to the amount of space available and oriented toward policies that protect the vulnerable and lift medium-term growth prospects — therefore remains essential for generating momentum and avoiding a lasting downshift in medium-term inflation expectations.

These fiscal policies should be accompanied by supply-side policies focused on structural reforms that can offset waning potential economic growth. These should include efforts to “boost labour force participation, improve the matching process in labour markets, and promote investment in research and development and innovation.”

The UK government has finally given the go-ahead to build the new Hinkley C nuclear power station in Somerset. It will consist of two European pressurised reactors, a relatively new technology. No EPR plant has yet been completed, with the one in the most advanced stages of construction at Flamanville in France, having experienced many safety and construction problems. This is currently expected to be more than three times over budget and at least six years behind its original completion date of 2012.

The Hinkley C power station, first proposed in 2007, is currently estimated to cost £18 billion. This cost will be borne entirely by its builder, EDF, the French 85% state-owned company, and its Chinese partner, CGN. When up and running – currently estimated at 2025 – it is expected to produce around 7% of the UK’s electricity output.

On becoming Prime Minister in July 2016, Theresa May announced that the approval for the plant would be put on hold while further investigation of its costs, benefits, security concerns, technological issues and safeguards was conducted. This has now been completed and approval has been granted subject to new conditions. The main one is that the government “will be able to prevent the sale of EDF’s controlling stake prior to the completion of construction”. This will allow the government to prevent change of ownership during the construction phase. Thus, for example, EDF, would not be allowed to sell its share of Hinkley C to CGN, which currently has a one-third share in the project. EDF and CGN have accepted the new terms.

After Hinkley the government will have a ‘golden share’ in all future nuclear projects. “This will ensure that significant stakes cannot be sold without the Government’s knowledge or consent.”

In return for their full financing of the project, the government has guaranteed EDF and CGN a price of £92.50 per megawatt hour of electricity (in 2012 prices). This price will be borne by consumers. It will rise with inflation from now and over the first 35 years of the power station’s operation. It is expected that the Hinkley C will have a life of 60 years.

Critics point out that this guaranteed ‘strike price’ is more than double the current wholesale price of electricity and, with the price of renewables falling as technology improves, it will be an expensive way to meet the UK’s electricity needs and cut carbon emissions.

Those in favour argue that it is impossible to predict electricity prices into the distant future and that the certainty this plant will give is worth the high price by current standards.

To assess the desirability of the plant requires an assessment of its costs and benefits. In principle, this is a relatively simple process of identifying and measuring the costs and benefits, including external costs and benefits; discounting future costs and benefits to give them a present value; weighting them by their probability of occurrence; then calculating whether the net present value is positive or negative. A sensitivity analysis could also be conducted to show just how sensitive the net present value would be to changes in the value of specific costs or benefits.

In practice the process is far from simple – largely because of the huge uncertainty over specific costs and benefits. These include future wholesale electricity prices, unforeseen problems in construction and operation, and a range of political issues, such as pressure from various interest groups, and attitudes and actions of EDF and CGN and their respective governments, which will affect not only Hinkley C but other future power stations.

Nuclear power in the UKNational Audit Office, Sir Amyas Morse, Comptroller and Auditor General (12/7/16)

Questions

Summarise the arguments for going ahead with Hinkley C.

Summarise the objections to Hinkley C.

What categories of uncertain costs and uncertain benefits are there for the project?

Is the project in EDF’s interests?

How will the government’s golden share system operate?

How should the discount rate be chosen for discounting future costs and benefits from a project such as Hinkley C?

What factors will determine the wholesale price of electricity over the coming years? In real terms, do you think it is likely to rise or fall? Explain.

If nuclear power has high fixed costs and low marginal costs, how does this affect how much nuclear power stations should be used in a situation of daily and seasonal fluctuations in demand?

How could ‘smart grid’ technology smooth out peaks and troughs in electricity supply and demand? How does this affect the relative arguments about nuclear power versus renewables?

The global economic impact of the coronavirus outbreak is uncertain but potentially very large. There has already been a massive effect on China, with large parts of the Chinese economy shut down. As the disease spreads to other countries, they too will experience supply shocks as schools and workplaces close down and travel restrictions are imposed. This has already happened in South Korea, Japan and Italy. The size of these effects is still unknown and will depend on the effectiveness of the containment measures that countries are putting in place and on the behaviour of people in self isolating if they have any symptoms or even possible exposure.

The global economic impact of the coronavirus outbreak is uncertain but potentially very large. There has already been a massive effect on China, with large parts of the Chinese economy shut down. As the disease spreads to other countries, they too will experience supply shocks as schools and workplaces close down and travel restrictions are imposed. This has already happened in South Korea, Japan and Italy. The size of these effects is still unknown and will depend on the effectiveness of the containment measures that countries are putting in place and on the behaviour of people in self isolating if they have any symptoms or even possible exposure. For some firms, having their staff working from home will be easy; for others it will be impossible.

For some firms, having their staff working from home will be easy; for others it will be impossible. While aggregate supply is likely to fall, or at least to grow less quickly, what will happen to the balance of aggregate demand and supply is less clear. A temporary rise in demand, as people stock up, could see a surge in prices, unless supermarkets and other firms are keen to demonstrate that they are not profiting from the disease. In the longer term, if aggregate demand continues to grow at past rates, it will probably outstrip the growth in aggregate supply and result in rising inflation. If, however, demand is subdued, as uncertainty about their own economic situation leads people to cut back on spending, inflation and even the price level may fall.

While aggregate supply is likely to fall, or at least to grow less quickly, what will happen to the balance of aggregate demand and supply is less clear. A temporary rise in demand, as people stock up, could see a surge in prices, unless supermarkets and other firms are keen to demonstrate that they are not profiting from the disease. In the longer term, if aggregate demand continues to grow at past rates, it will probably outstrip the growth in aggregate supply and result in rising inflation. If, however, demand is subdued, as uncertainty about their own economic situation leads people to cut back on spending, inflation and even the price level may fall. The linked article below, by Evan Davis, assesses the state of economics. He argues that economics has had some major successes over the years in providing a framework for understanding how economies function and how to increase incomes and well-being more generally.

The linked article below, by Evan Davis, assesses the state of economics. He argues that economics has had some major successes over the years in providing a framework for understanding how economies function and how to increase incomes and well-being more generally.  Even Davis identifies two major shortcomings of the discipline – both beginning with ‘C’. ‘One is complexity, the other is community.’

Even Davis identifies two major shortcomings of the discipline – both beginning with ‘C’. ‘One is complexity, the other is community.’ And the same applies to firms. They will be influenced by various other firms, such as competitors, trend setters and suppliers and also by a range of stakeholders – not just shareholders, but also workers, customers, local communities, etc. A firm’s aim is thus unlikely to be simple short-term profit maximisation.

And the same applies to firms. They will be influenced by various other firms, such as competitors, trend setters and suppliers and also by a range of stakeholders – not just shareholders, but also workers, customers, local communities, etc. A firm’s aim is thus unlikely to be simple short-term profit maximisation.