So here we are, summer is over (or almost over if you’re an optimist) and we are sitting in front of our screens reminiscing about hot sunny days (at least I do)! There is no doubt, however: a lot happened in the world of politics and economics in the past three months. The escalation of the US-China trade war, the run on the Turkish lira, the (successful?) conclusion of the Greek bailout – these are all examples of major economic developments that took place during the summer months, and which we will be sure to discuss in some detail in future blogs. Today, however, I will introduce a topic that I am very interested in as a researcher: the liberalisation of energy markets in developing countries and, in particular, Mexico.

So here we are, summer is over (or almost over if you’re an optimist) and we are sitting in front of our screens reminiscing about hot sunny days (at least I do)! There is no doubt, however: a lot happened in the world of politics and economics in the past three months. The escalation of the US-China trade war, the run on the Turkish lira, the (successful?) conclusion of the Greek bailout – these are all examples of major economic developments that took place during the summer months, and which we will be sure to discuss in some detail in future blogs. Today, however, I will introduce a topic that I am very interested in as a researcher: the liberalisation of energy markets in developing countries and, in particular, Mexico.

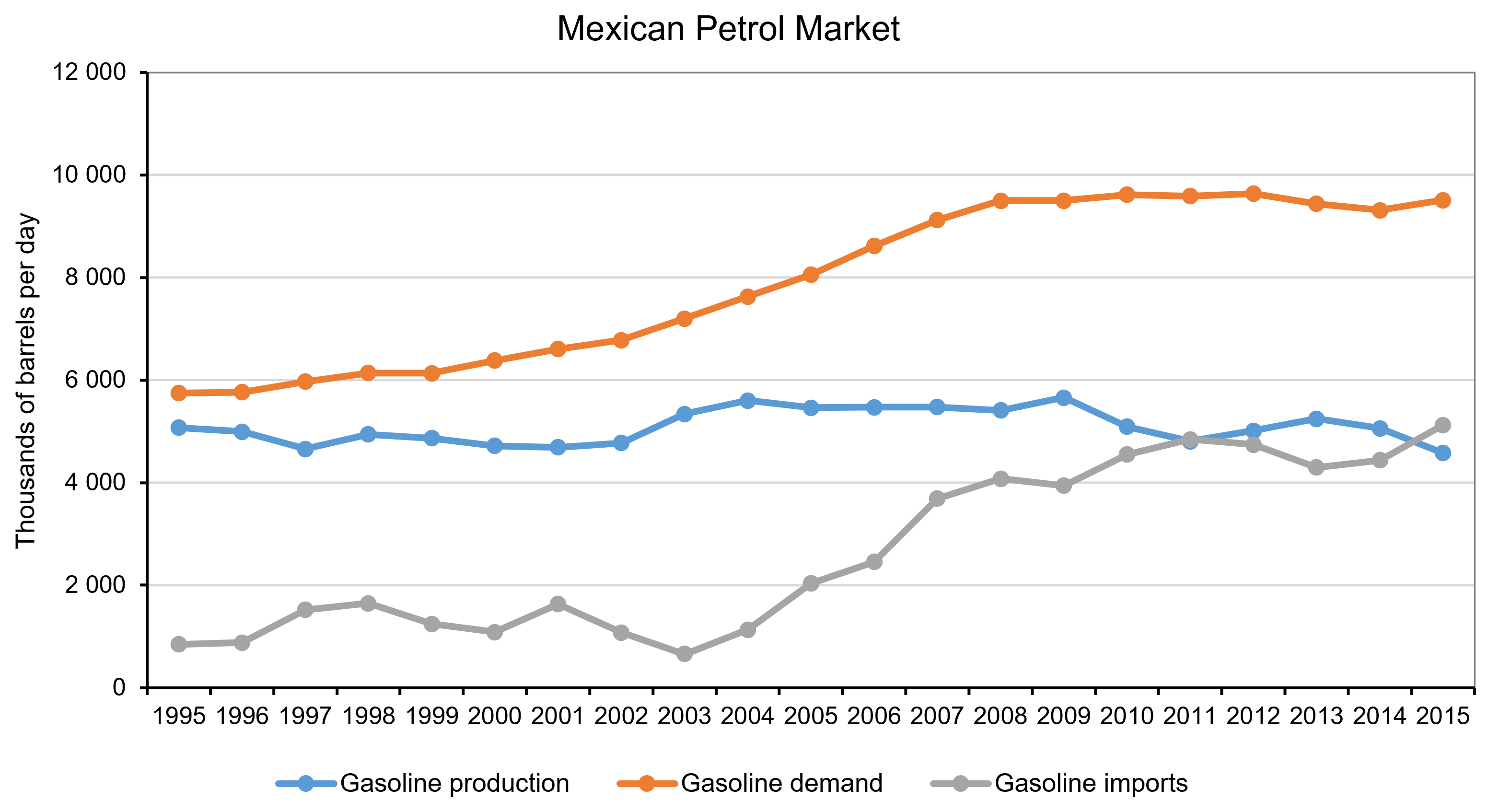

Why Mexico? Well, because it is a great example of a large developing economy that has been attempting to liberalise its energy market and reverse price setting and monopolistic practices that go back several decades. Until very recently, the price of petrol in Mexico was set and controlled by Pemex, a state monopolist. This put Pemex under pressure since, as a sole operator, it was responsible for balancing growing demand and costs, even to the detriment of its own finances.

The petrol (or ‘gasoline’) price liberalisation started in May 2017 and took place in stages – starting in the North part of Mexico and ending in November of the same year in the central and southern regions of the country. The main objective was to address the notable decrease in domestic oil production that put at risk the ability of the country to meet demand; as well as Mexico’s increasing dependency on foreign markets affected by the surge of the international oil price. The government has spent the past five years trying to create a stronger regulatory framework, while easing the financial burden on the state and halting the decline in oil reserves and production. Unsurprisingly, opening up a monopolistic market turns out to be a complex and bumpy process.

Source: Author’s calculations using data from the Energy Information Bank, Ministry of Energy, Mexico

Source: Author’s calculations using data from the Energy Information Bank, Ministry of Energy, Mexico

Despite all the reforms, retail petrol prices have kept rising. Although part of this price rise is demand-driven, an increasing number of researchers highlight the significance of the distribution of oil-related infrastructure in determining price outcomes at the federal and regional (state) level. Saturation and scarcity of both distribution and storage infrastructure are probably the two most significant impediments to opening the sector up to competition (Mexico Institute, 2018). You see, the original design of these networks and the deployment of the infrastructure was not aimed at maximising efficiency of distribution – the price was set by the monopolist and, in a way that was compliant with government policy (Mexico Institute, 2018). Economic efficiency was not always part of this equation. As a result, consumers located in better-deployed areas were subsidising the inherent logistics costs of less ‘well endowed’ regions by facing an artificially higher price than they would have in a competitive market.

But what about now? Do such differences in the allocation of infrastructure between regions lead to location-related differences in the price of petrol? If so, by how much? And, what policies should the government pursue to address such imbalances? These are all questions that I explore in one of my recent working papers titled ‘Widening the Gap: Lessons from the aftermath of the energy market reform in Mexico’ (with Hugo Vallarta) and I will be sharing some of the answers with you in a future blog.

Articles

Data

Questions

- Are state-owned monopolies effective in delivering successful market outcomes? Why yes, why no?

- In the case of Mexico, are you surprised about the complexities that were involved with opening up markets to competition? Explain why.

- Use Google to identify countries in which energy markets are controlled by state-owned monopolies.

The UK government has finally given the go-ahead to build the new Hinkley C nuclear power station in Somerset. It will consist of two European pressurised reactors, a relatively new technology. No EPR plant has yet been completed, with the one in the most advanced stages of construction at Flamanville in France, having experienced many safety and construction problems. This is currently expected to be more than three times over budget and at least six years behind its original completion date of 2012.

The UK government has finally given the go-ahead to build the new Hinkley C nuclear power station in Somerset. It will consist of two European pressurised reactors, a relatively new technology. No EPR plant has yet been completed, with the one in the most advanced stages of construction at Flamanville in France, having experienced many safety and construction problems. This is currently expected to be more than three times over budget and at least six years behind its original completion date of 2012.

The Hinkley C power station, first proposed in 2007, is currently estimated to cost £18 billion. This cost will be borne entirely by its builder, EDF, the French 85% state-owned company, and its Chinese partner, CGN. When up and running – currently estimated at 2025 – it is expected to produce around 7% of the UK’s electricity output.

On becoming Prime Minister in July 2016, Theresa May announced that the approval for the plant would be put on hold while further investigation of its costs, benefits,  security concerns, technological issues and safeguards was conducted. This has now been completed and approval has been granted subject to new conditions. The main one is that the government “will be able to prevent the sale of EDF’s controlling stake prior to the completion of construction”. This will allow the government to prevent change of ownership during the construction phase. Thus, for example, EDF, would not be allowed to sell its share of Hinkley C to CGN, which currently has a one-third share in the project. EDF and CGN have accepted the new terms.

security concerns, technological issues and safeguards was conducted. This has now been completed and approval has been granted subject to new conditions. The main one is that the government “will be able to prevent the sale of EDF’s controlling stake prior to the completion of construction”. This will allow the government to prevent change of ownership during the construction phase. Thus, for example, EDF, would not be allowed to sell its share of Hinkley C to CGN, which currently has a one-third share in the project. EDF and CGN have accepted the new terms.

After Hinkley the government will have a ‘golden share’ in all future nuclear projects. “This will ensure that significant stakes cannot be sold without the Government’s knowledge or consent.”

In return for their full financing of the project, the government has guaranteed EDF and CGN a price of £92.50 per megawatt hour of electricity (in 2012 prices). This price will be borne by consumers. It will rise with inflation from now and over the first 35 years of the power station’s operation. It is expected that the Hinkley C will have a life of 60 years.

Critics point out that this guaranteed ‘strike price’ is more than double the current wholesale price of electricity and, with the price of renewables falling as technology improves, it will be an expensive way to meet the UK’s electricity needs and cut carbon emissions.

Those in favour argue that it is impossible to predict electricity prices into the distant future and that the certainty this plant will give is worth the high price by current standards.

To assess the desirability of the plant requires an assessment of its costs and benefits. In principle, this is a relatively simple process of identifying and measuring the costs and benefits, including external costs and benefits; discounting future costs and benefits to give them a present value; weighting them by their probability of occurrence; then calculating whether the net present value is positive or negative. A sensitivity analysis could also be conducted to show just how sensitive the net present value would be to changes in the value of specific costs or benefits.

In practice the process is far from simple – largely because of the huge uncertainty over specific costs and benefits. These include future wholesale electricity prices, unforeseen problems in construction and operation, and a range of political issues, such as pressure from various interest groups, and attitudes and actions of EDF and CGN and their respective governments, which will affect not only Hinkley C but other future power stations.

The articles look at the costs and benefits of this, the most expensive construction project ever in the UK, and possibly on Earth..

Articles

Hinkley Point: UK approves nuclear plant deal BBC News (15/9/16)

Hinkley Point: What is it and why is it important? BBC News, John Moylan (15/9/16)

‘The case hasn’t changed’ for Hinkley Point C BBC Today Programme, Malcolm Grimston (29/7/16)

‘The case hasn’t changed’ for Hinkley Point C BBC Today Programme, Malcolm Grimston (29/7/16)

U.K. Approves EDF’s £18 Billion Hinkley Point Nuclear Project Bloomberg, Francois De Beaupuy (14/9/16)

Hinkley Point C nuclear power station gets government green light The Guardian, Rowena Mason and Simon Goodley (15/9/16)

Hinkley Point C: now for a deep rethink on the nuclear adventure? The Guardian, Nils Pratley (15/9/16)

Hinkley Point C finally gets green light as Government approves nuclear deal with EDF and China The Telegraph, Emily Gosden (15/9/16)

UK gives go-ahead for ‘revised’ £18bn Hinkley Point plant Financial Times, Andrew Ward, Jim Pickard and Michael Stothard (15/9/16)

Hinkley Point: Is the UK getting a good deal? Financial Times, Andrew Ward (15/9/16)

Hinkley Point is risk for overstretched EDF, warn critics Financial Times, Michael Stothard (15/9/16)

Hinkley C must be the first of many new nuclear plants The Conversation, Simon Hogg (16/9/16)

Report

Nuclear power in the UK National Audit Office, Sir Amyas Morse, Comptroller and Auditor General (12/7/16)

Questions

- Summarise the arguments for going ahead with Hinkley C.

- Summarise the objections to Hinkley C.

- What categories of uncertain costs and uncertain benefits are there for the project?

- Is the project in EDF’s interests?

- How will the government’s golden share system operate?

- How should the discount rate be chosen for discounting future costs and benefits from a project such as Hinkley C?

- What factors will determine the wholesale price of electricity over the coming years? In real terms, do you think it is likely to rise or fall? Explain.

- If nuclear power has high fixed costs and low marginal costs, how does this affect how much nuclear power stations should be used in a situation of daily and seasonal fluctuations in demand?

- How could ‘smart grid’ technology smooth out peaks and troughs in electricity supply and demand? How does this affect the relative arguments about nuclear power versus renewables?

Over 90% of UK households buy their gas and electricity from one of the ‘big six’ energy suppliers – British Gas (Centrica), EDF, E.ON, npower (RWE), Scottish Power (Iberdrola) and SSE. The big six are currently being investigated by the Competition and Markets Authority (CMA) for possible breach of a dominant market position.

Over 90% of UK households buy their gas and electricity from one of the ‘big six’ energy suppliers – British Gas (Centrica), EDF, E.ON, npower (RWE), Scottish Power (Iberdrola) and SSE. The big six are currently being investigated by the Competition and Markets Authority (CMA) for possible breach of a dominant market position.

An updated ‘issues statement‘ summarises the investigation group’s initial thinking based on the evidence it has received. In paragraph 16 it states:

Comparing all available domestic tariffs – including those offered by the independent suppliers – we calculate that, over the period Quarter 1 2012 to Quarter 2 2014, over 95% of the dual fuel customers of the Six Large Energy Firms could have saved by switching tariff and/or supplier and that the average saving available to these customers was between £158 and £234 a year (depending on the supplier).

Between 40% and 50% of customers have been with a supplier for more than 10 years. The companies are thus accused of exploiting these ‘loyalty’ customers, many of whom are too busy or ill-informed to switch to an alternative supplier. According to the uSwitch article below:

Between 40% and 50% of customers have been with a supplier for more than 10 years. The companies are thus accused of exploiting these ‘loyalty’ customers, many of whom are too busy or ill-informed to switch to an alternative supplier. According to the uSwitch article below:

This is a particular issue for the most vulnerable of customers, including the elderly, who view switching as ‘impossible’.

But the elderly were not the only consumers losing out; the CMA found that those customers most likely to be on expensive standard tariffs were less educated, or on lower incomes, or single parents, and did not necessarily have access to the Internet.

And the problem of penalising ‘loyalty’ customers who do not shop around applies in other industries, most notably banking. People who regularly switch savings accounts can get higher interest rates, often for a temporary ‘introductory’ period. Similarly, people who regularly transfer credit card debt from one card to another can take advantage of low interest rate, or even zero interest rate, deals for an introductory period.

Returning to the energy industry. Is the problem one of oligopoly? Do the big six have too much market power and, if so, what can be done about it? Should they be split up? Should regulation be tightened? Should new entrants be encouraged and, if so, what specific measures can be taken? The following articles explore the issues and possible policies.

Articles

British energy customers missed out on savings Reuters, Nina Chestney (18/2/15)

U.K. Energy Customers Could Save by Shopping Around: CMA BloombergBusiness, Aoife White (18/2/15)

Big six energy firms overcharging customers by up to £234 a year The Guardian, Sean Farrell (18/1/15)

Big six energy firms may lose quarter of customers by 2020, analysts warn The Guardian, Terry Macalister (1/10/14)

UK watchdog says big energy groups do not enjoy unfair advantage Financial Times, Michael Kavanagh (18/2/15)

CMA energy market investigation update: millions are punished for being loyal uSwitch, Lauren Vasquez (19/2/15)

Gas and electricity bills – the key questions Channel 4 News (18/2/15)

Energy customers miss big savings, says CMA inquiry BBC News, John Moylan (18/2/15)

Big Six energy companies overcharging loyal customers by up to £234 a year says watchdog Independent, Simon Read (18/2/15)

Consumer groups demand change after ‘Big Six’ accused of penalising customers out of hundreds of pounds Independent, Simon Read (19/2/15)

Energy companies’ loyalty problem lights the way forward The Conversation, Bridget Woodman (19/2/15)

CMA press releases and reports

Energy market investigation – updated issues statement Competition and Markets Authority (18/2/15)

Energy market investigation Competition and Markets Authority (23/2/15)

Energy Market Investigation: Updated Issues Statement Competition and Markets Authority (18/2/15)

Questions

- What barriers to entry exist in the electricity and gas supply markets?

- Explain how the big six are practising price discrimination. What form does it take and how are the markets separated?

- Find out what tariffs are offered by each of the big six. When you have done so, reflect on how easy it was to find out the information and why so few customers switch.

- How could more people be encouraged to ‘shop around’ and switch energy suppliers?

- Explain the five theories of harm identified by the CMA. Would a rise in market share of the smaller energy suppliers adequately combat each of the five types of harm?

- In what ways may UK energy regulation be ‘a barrier to pro-competitive innovation and change’?

- What are the arguments for and against breaking up the big six?

- What are the arguments for and against electricity and gas price control?

As Elizabeth noted in Fuelling the Political Playing Field, there has been much debate recently about energy prices in the UK. Four of the ‘Big Six’ energy companies have now announced price rises. They average 9.1% – way above the rate of consumer price inflation and even further above the average rate of wage increases. What is more, they are considerably above the rate of increase in wholesale energy prices, which, according to Ofgem, have risen by just 1.7% in the past year.

The bosses of the energy companies have appeared before the House of Commons Energy and Climate Change Select Committee to answer for their large price increases. The energy companies claim that the increases are necessary to cover not only rising wholesale prices, but also green levies by the government and ‘network charges’ for investments in infrastructure.  However, it is hard to see how, even taking into account all three of these possible sources of cost increases, the scale of price increases can be justified.

However, it is hard to see how, even taking into account all three of these possible sources of cost increases, the scale of price increases can be justified.

Another possible explanation for the price hikes is that they are partly the result of a system of transfer pricing (see). The energy industry is vertically integrated. Energy companies are not only retailers to customers, but also generators of electricity and wholesale shippers of gas. It is possible that, by the producing/shipping arms of these companies charging higher prices to their retailing arms, the retailers’ costs do indeed go up more than the wholesale market cost. The result, however, is higher profits for the producing arms of these businesses. In other words, a higher transfer price allows profits to be diverted from each company’s retailing arm to its producing arm.

This is an argument for making the wholesale market more competitive and for stopping the by-passing of this market by producing arms of companies selling directly to their retailing arms. What the companies are being accused of is an abuse of market power and possibly of colluding with each other, at least tacitly, to support the continuation of such a practice.

This is an argument for making the wholesale market more competitive and for stopping the by-passing of this market by producing arms of companies selling directly to their retailing arms. What the companies are being accused of is an abuse of market power and possibly of colluding with each other, at least tacitly, to support the continuation of such a practice.

So is the answer a price freeze, as proposed by the Labour Party? Is it an investigation of the energy market by the Competition Commission? Or is it, at least as a first step, much more openness by the energy companies and transparency about their pricing practices? Or is it to encourage consumers to switch between energy companies, including the smaller ones, which at present account for less than 5% of energy supply? The videos, podcasts and articles consider these issues.

Webcasts and Podcasts

Energy bosses blame high bills on wholesale prices Channel 4 News, Gary Gibbon (29/10/13)

Why are energy bosses being questioned? BBC News, Stephanie McGovern (29/10/13)

Key questions Big Six energy companies must answer The Telegraph, Ann Robinson (29/10/13)

Energy bosses offer excuses for prices rises The Telegraph (29/10/13)

Energy bosses face MPs over price rises BBC News, John Moylan (29/10/13)

Energy boss ‘can’t explain’ competitors’ price hikes The Telegraph (29/10/13)

Ovo boss: Competition Commission would take too long BBC News (30/10/13)

Dale Vince: Energy market is ‘dysfunctional’ BBC Today Programme (30/10/13)

Tony Cocker: Public mistrust energy industry BBC Today Programme (30/10/13)

Ed Davey: Energy deals not just for ‘internet savvy’ BBC Today Programme (31/10/13)

Articles

Energy giants ‘charge as much as they can get away with’ The Telegraph, Peter Dominiczak (29/10/13)

UK energy markets need perestroika Financial Times (27/10/13)

Britain’s energy utilities must embrace glasnost Reuters, John Kemp (29/10/13)

Small energy firms ‘escape levies’ BBC News (30/10/13)

Is the energy market structurally flawed? BBC news, Robert Peston (30/10/13)

The energy market needs a Competition Commission investigation Fingleton Associates, John Fingleton (12/10/13)

Energy firms raised prices despite drop in wholesale costs The Guardian, Rowena Mason (29/10/13)

Only full-scale reform of our energy market will prevent endless price rises The Observer, Phillip Lee (26/10/13)

Energy Giants Blame Rising Bills On Green ‘Stealth Taxes’ Huffington Post, Asa Bennett (29/10/13)

Big Six energy firms ‘like cartel’ Belfast Telegraph (30/10/13)

Energy boss says he hasn’t done sums on green levies The Telegraph, Georgia Graham (30/10/13)

Graphic: How your energy bills have soared in ten years The Telegraph, Matthew Holehouse (30/10/13)

British energy suppliers’ explanations for price hikes just don’t add up The Guardian, Larry Elliott (31/10/13)

The 18th energy market investigation since 2001: Will this one be different? The Carbon Brief, Ros Donald (31/10/13)

Energy: Is there enough competition in the market? BBC News, Hugh Pym (26/11/13)

Information and Reports

Wholesale [electricity] market Ofgem

Wholesale [gas] market Ofgem

Response on wholesale energy costs Ofgem Press Release (29/10/13)

Response to Government’s Annual Energy Statement Ofgem Press Release (31/10/13)

Real Energy Market Reform The Labour Party

Questions

- Why may the costs of energy paid by the energy retailers to energy producers/shippers have risen more than the wholesale price?

- Explain what is meant by transfer pricing. How could transfer pricing be used to divert profits between the different divisions of a business?

- How can transfer pricing be designed by multinational companies to help them minimise their tax bills?

- Why is policing transfer pricing arrangements notoriously difficult?

- What evidence is there to show that switching between retailers by customers can help to drive retail energy prices down?

- How did the old electricity pool system differ from the current wholesale system?

- Should electricity companies be forced to pool the electricity they generate and not sell it to themselves through bilateral deals?

- Comment on the following: “The current electricity trading arrangements ‘create the very special incentive for the oligopolists. …The best of all possible worlds is where nobody invests. As supply and demand close up, the price spikes upwards, and supernormal profits result.'”

The UK electricity supply market is an oligopoly. Over 95% of the market is supplied by the ‘big six’: British Gas (Centrica), EDF Energy, E.ON, npower (RWE), Scottish Power (Iberdrola) and SSE. The big six also generate much of the electricity they supply; they are vertically integrated companies. Between them they generate nearly 80% of the country’s electricity. There are a further two large generators, Drax Power Limited and GDF Suez Energy UK, making the generation industry an oligopoly of eight key players.

The UK electricity supply market is an oligopoly. Over 95% of the market is supplied by the ‘big six’: British Gas (Centrica), EDF Energy, E.ON, npower (RWE), Scottish Power (Iberdrola) and SSE. The big six also generate much of the electricity they supply; they are vertically integrated companies. Between them they generate nearly 80% of the country’s electricity. There are a further two large generators, Drax Power Limited and GDF Suez Energy UK, making the generation industry an oligopoly of eight key players.

Ofgem, the energy market regulator, has just published a report on the wholesale electricity market, arguing that it is insufficiently liquid. This, argues the report, acts as a barrier to entry to competitor suppliers. It thus proposes measures to increase liquidity and thereby increase effective competition. Liquidity, according to the report, is:

… the ability to quickly buy or sell a commodity without causing a significant change in its price and without incurring significant transaction costs. It is a key feature of a well-functioning market. A liquid market can also be thought of as a ‘deep’ market where there are a number of prices quoted at which firms are prepared to trade a product. This gives firms confidence that they can trade when needed and will not move the price substantially when they do so.

A liquid wholesale electricity market ensures that electricity products are available to trade, and that their prices are robust. These products and price signals are important for electricity generators and suppliers, who need to trade to manage their risks. Liquidity in the wholesale electricity mark et therefore supports competition in generation and supply, which has benefits for consumers in terms of downward pressure on bills, better service and greater choice.

A liquid wholesale electricity market ensures that electricity products are available to trade, and that their prices are robust. These products and price signals are important for electricity generators and suppliers, who need to trade to manage their risks. Liquidity in the wholesale electricity mark et therefore supports competition in generation and supply, which has benefits for consumers in terms of downward pressure on bills, better service and greater choice.

So how can liquidity be increased? Ofgem is proposing that the big six publish prices for two years ahead at which they are contracting to purchase electricity from generators in long-term contracts. These bilateral deals with generators are often with their own company’s generating arm. Publishing prices in this way will allow smaller suppliers to be able to seek out market opportunities. The generating companies will not be allowed to refuse to contract to supply smaller companies at the prices they are being forced to publish.

In addition, Ofgem is proposing that generators would have to sell 20% of output in the open market instead of through bilateral deals. As it is, however, some 30% of output is currently auctioned on the wholesale spot market (i.e. the market for immediate use).

But it is pricing transparency plus small suppliers being able to gain access to longer-term contracts that are the two key elements of the proposed reform.

Articles

UK utilities face having to disclose long-term deals Reuters, Karolin Schaps and Rosalba O’Brien (12/6/13)

Ofgem set to ‘break stranglehold’ in the energy market BBC News, John Moylan (12/6/13)

Ofgem plan ‘to end energy stranglehold’ BBC Today Programme, John Moylan and Ian Marlee (12/6/13)

Ofgem outlines proposals to ‘break stranglehold’ of big six energy suppliers on electricity market The Telegraph (12/6/13)

Ofgem widens investigation into alleged rigging of gas and power markets The Guardian, Terry Macalister (6/6/13)

Ofgem moves to break stranglehold of ‘big six’ energy suppliers Financial Times, Guy Chazan (12/6/13)

Ofgem to crackdown on Big Six energy suppliers in bid to cut electricity prices Independent, Simon Read (12/6/13)

Reports and data

Opening up Electricity Market to Effective Competition Ofgem Press Release (12/6/13)

Wholesale power market liquidity: final proposals for a ‘Secure and Promote’ licence condition – Draft Impact Assessment Ofgem (12/6/13)

Electricity statistics Department of Energy & Climate Change

The Dirty Half Dozen Friends of the Earth (Oct 2011)

Questions

- What barriers to entry exist in (a) the wholesale and (b) the retail market for electricity?

- Distinguish between spot and forward markets. Why is competition in forward markets particularly important for small suppliers of electricity?

- How will ‘liquidity’ be increased by the measures Ofgem is proposing?

- To what extent does vertical integration in the energy industry benefit consumers of electricity?

- What is a price reporting agency (PRA)? What anti-competitive activities have been taking place in the short-term energy market and why may PRAs not be ‘fit for purpose’?

- Do you think that the measures Ofgem is proposing will ensure that the big generators trade fairly with small suppliers? Explain.

- What are the dangers in the proposals for the large generators?