Donald Trump has suggested that the Fed should cut interest rates by 1 percentage point and engage in a further round of quantitative easing. He wants to see monetary policy used to give a substantial boost to US economic growth at a time when inflation is below target. In a pair of tweets just before the meeting of the Fed to decide on interest rates, he said:

China is adding great stimulus to its economy while at the same time keeping interest rates low. Our Federal Reserve has incessantly lifted interest rates, even though inflation is very low, and instituted a very big dose of quantitative tightening. We have the potential to go up like a rocket if we did some lowering of rates, like one point, and some quantitative easing. Yes, we are doing very well at 3.2% GDP, but with our wonderfully low inflation, we could be setting major records &, at the same time, make our National Debt start to look small!

But would this be an appropriate policy? The first issue concerns the independence of the Fed.

It is supposed to take decisions removed from the political arena. This means sticking to its inflation target of 2 per cent over the medium term – the target it has officially had since January 2012. To do this, it adjusts the federal funds interest rate and the magnitude of any bond buying programme (quantitative easing) or bond selling programme (quantitative tightening).

The Fed is supposed to assess the evidence concerning the pressures on inflation (e.g. changes in aggregate demand) and what inflation is likely to be over the medium term in the absence of any changes in monetary policy. If the Federal Open Market Committee (FOMC) expects inflation to exceed 2 per cent over the medium term, it will probably raise the federal funds rate; if it expects inflation to be below the target it will probably lower the federal funds rate.

In the case of the economy being in recession, and thus probably considerably undershooting the target, it may also engage in quantitative easing (QE). If the economy is growing strongly, it may sell some of its portfolio of bonds and thus engage in quantitative tightening (QT).

Since December 2015 the Fed has been raising interest rates by 0.25 percentage points at a time in a series of steps, so that the federal funds rate stands at between 2.25% and 2.5% (see chart). And since October 2017, it has also been engaged in quantitative tightening. In recent months it has been selling up to $50 billion of assets per month from its holdings of around $4000 billion and so far has reduced them by around £500 billion. It has, however, announced that the programme of QT will end in the second half of 2019.

This does raise the question of whether the FOMC is succumbing to political pressure to cease QT and put interest rate rises on hold. If so, it is going against its remit to base its policy purely on evidence. The Fed, however, maintains that its caution reflects uncertainty about the global economy.

The second issue is whether Trump’s proposed policy is a wise one.

Caution about further rises in interest rates and further QT is very different from the strongly expansionary monetary policy that President Trump proposes. The economy is already growing at 3.2%, which is above the rate of growth in potential output, of around 1.8% to 2.0%. The output gap (the percentage amount that actual GDP exceeds potential GDP) is positive. The IMF forecasts that the gap will be 1.4% in 2019 and 1.3% in 2020 and 2021. This means that the economy is operating at above normal capacity working and this will eventually start to drive up inflation. Any further stimulus will exacerbate the problem of excess demand. And a large stimulus, as proposed by Donald Trump, will cause serious overheating in the medium term, even if it does stimulate growth in the short term.

For these reasons, the Fed resisted calls for a large cut in interest rates and a return to quantitative easing. Instead it chose to keep interest rates on hold at its meeting on 1 May 2019.

But if the Fed had done as Donald Trump would have liked, the economy would probably be growing very strongly at the time of the next US election in November next year. It would be a good example of the start of a political business cycle – something that is rarer nowadays with the independence of central banks.

What are the arguments for central bank independence?

Are there any arguments against central bank independence?

Explain what is meant by an ‘output gap’? Why is it important to be clear on what is meant by ‘potential output’?

Would there be any supply-side effects of a strong monetary stimulus to the US economy at the current time? If so, what are they?

Explain what is meant by the ‘political business’ cycle? Are governments in the UK, USA or the eurozone using macroeconomic policy to take advantage of the electoral cycle?

The Fed seems to be ending its programme of quantitative tightening (QT). Why might that be so and is it a good idea?

If inflation is caused by cost-push pressures, should central banks stick rigidly to inflation targets? Explain.

How are expectations likely to affect the success of a monetary stimulus?

Back in October, we examined the rise in oil prices. We said that, ‘With Brent crude currently at around $85 per barrel, some commentators are predicting the price could reach $100. At the beginning of the year, the price was $67 per barrel; in June last year it was $44. In January 2016, it reached a low of $26.’ In that blog we looked at the causes on both the demand and supply sides of the oil market. On the demand side, the world economy had been growing relatively strongly. On the supply side there had been increasing constraints, such as sanctions on Iran, the turmoil in Venezuela and the failure of shale oil output to expand as much as had been anticipated.

But what a difference a few weeks can make!

Brent crude prices have fallen from $86 per barrel in early October to just over $50 by the end of the year – a fall of 41 per cent. (Click here for a PowerPoint of the chart.) Explanations can again be found on both the demand and supply sides.

On the demand side, global growth is falling and there is concern about a possible recession (see the blog: Is the USA heading for recession?). The Bloomberg article below reports that all three main agencies concerned with the oil market – the U.S. Energy Information Administration, the Paris-based International Energy Agency and OPEC – have trimmed their oil demand growth forecasts for 2019. With lower expected demand, oil companies are beginning to run down stocks and thus require to purchase less crude oil. Fracking (Source: US Bureau of Land Management Environmental Assessment, public domain image)

On the supply side, US shale output has grown rapidly in recent weeks and US output has now reached a record level of 11.7 million barrels per day (mbpd), up from 10.0 mbpd in January 2018, 8.8 mbpd in January 2017 and 5.4 mbpd in January 2010. The USA is now the world’s biggest oil producer, with Russia producing around 11.4 mpbd and Saudi Arabia around 11.1 mpbd.

Total world supply by the end of 2018 of around 102 mbpd is some 2.5 mbpd higher than expected at the beginning of 2018 and around 0.5 mbpd greater than consumption at current prices (the remainder going into storage).

So will oil prices continue to fall? Most analysts expect them to rise somewhat in the near future. Markets may have overcorrected to the gloomy news about global growth. On the supply side, global oil production fell in December by 0.53 mbpd. In addition OPEC and Russia have signed an accord to reduce their joint production by 1.2 mbpd starting this month (January). What is more, US sanctions on Iran have continued to curb its oil exports.

But whatever happens to global growth and oil production, the future price will continue to reflect demand and supply. The difficulty for forecasters is in predicting just what the levels of demand and supply will be in these uncertain times.

An agreement in principle was reached on September 30 between the USA, Canada and Mexico over a new trade deal to replace the North American Free Trade Agreement (NAFTA). President Trump had described NAFTA as ‘the worst trade deal maybe ever signed anywhere, but certainly ever signed in this country.’ The new deal, named the United States-Mexico-Canada Agreement, or USMCA, is the result of 14 months of negotiations, which have often been fractious. A provisional bilateral agreement was made between the USA and Mexico in August. At the same time, President Trump threatened a trade war with Canada if it did not reach a trade agreement with the USA (and Mexico). The new USMCA must be ratified by lawmakers in all three countries before it can come into force. This could take a few months.

So is USMCA a radical departure from NAFTA? Does the USA stand to gain substantially, as President Trump claims? In fact, USMCA is little different from NAFTA. It could best be described as a relatively modest reworking of NAFTA. So what are the changes?

The first change affects the car industry. From 2020, 75% of the components of any vehicle crossing between the USA and Canada or Mexico must be made within one or more of the three countries to qualify for tariff-free treatment. The aim is to boost production within the region. But the main change here is merely an increase in the proportion from the current 62.5%.

A more significant change affecting the car industry concerns wages. Between 40% and 45% of a vehicle’s components must be made by workers earning at least US$16 per hour. This is some three times more than the average wage currently earned by Mexican car workers. Although it will benefit such workers, it will reduce Mexico’s competitive advantage and could hence lead to some diversion of production away from Mexico. Also, it could push up the price of cars.

The agreement has also strengthened various standards inadequately covered in NAFTA. According to The Conversation article:

The new agreement includes stronger protections for patents and trademarks in areas such as biotech, financial services and domain names – all of which have advanced considerably over the past quarter century. It also contains new provisions governing the expansion of digital trade and investment in innovative products and services.

Separately, negotiators agreed to update labor and environmental standards, which were not central to the 1994 accord and are now typical in modern trade agreements. Examples include enforcing a minimum wage for autoworkers, stricter environmental standards for Mexican trucks and lots of new rules on fishing to protect marine life.

Another area where the USMCA agreement has made changes concerns trade in dairy products. This particularly affects Canada, which has agreed to allow more US dairy products tariff-free into Canada (see the CNN article at the end of the list of articles below). New higher quotas will give US dairy farmers access to 3.6% of Canada’s dairy market. They will still pay tariffs on dairy exports to Canada that exceed the quotas, ranging from 200% to 300%.

The other significant change for consumers in Mexico and Canada is a rise in the value of duty-free imports they can bring in from the USA, including online transactions. As the first BBC article listed below states:

The new agreement raises duty-free shopping limits to $100 to enter Mexico and C$150 ($115) to enter Canada without facing import duties – well above the $50 previously allowed in Mexico and C$20 permitted by Canada. That’s good news for online shoppers in Mexico and Canada – as well as shipping firms and e-commerce companies, especially giants like Amazon.

Despite these changes, USMCA is very similar to NAFTA. It is still a preferential trade deal between the three countries, but certainly not a completely free trade deal – but nor was NAFTA.

And for the time being, US tariffs on Mexican and Canadian steel and aluminium imports remain in place. Perhaps, with the conclusion of the USMCA agreement, the Trump administration will now, as promised, consider lifting these tariffs.

What have been the chief gains and losses for the USA from USMCA?

What have been the chief gains and losses for Mexico from USMCA?

What have been the chief gains and losses for Canada from USMCA?

What are the economic gains from free trade?

Why might a group of countries prefer a preferential trade deal with various restrictions on trade rather than a completely free trade deal between them?

Distinguish between trade creation and trade diversion.

In what areas, if any, might USMCA result in trade diversion?

If the imposition of tariffs results in a net loss from a decline in trade, why might it be in the interests of a country such as the USA to impose tariffs?

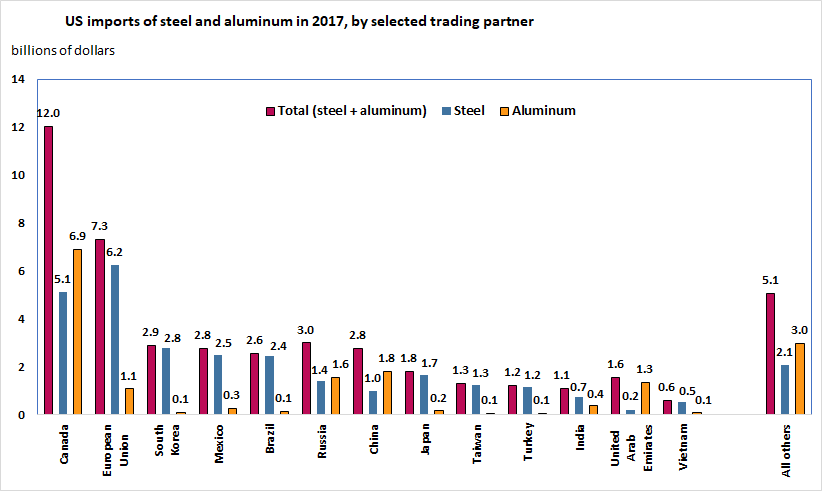

The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

Source: Bown (2018), Figure 1

A number of economists and policymakers are worried that such policies restrict trade and are likely to provoke retaliation by the affected trade partners. In recent statements, the EU has pledged to take counter-measures if the bloc is affected by these policies. In a recent press conference, the Commissioner for Trade, Cecilia Malmstrom, stated that:

We have made it clear that a move that hurts the EU and puts thousands of European jobs in jeopardy will be met with a firm and proportionate response.

She added that, ‘I truly hope that this will not happen. A trade war has no winners.’

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.

A number of studies have attempted to estimate the effect of trade restrictions and tariff wars on welfare: see for instance Anderson and Wincoop (2001), Syropoulos (2002), Fellbermayr et al. (2013). The results vary widely, depending on the case. However, there seems to be consensus that the more similar (in terms of size and industry composition) the adversaries are, the more mutually damaging a trade war is likely to be (and, therefore, less likely to happen).

As Miyagiwa et al (2016, p43) explain:

A country initiates contingent protection policy against a trading partner only if the latter has a considerably smaller domestic market than its own, while avoiding confrontation with a country having a substantially larger domestic market than its own.

As both Canada and the EU are very large advanced market economies, it remains to be seen how much risk (and potential damage to the local and global economy) US trade policymakers are willing to take.

Since running for election, Donald Trump has vowed to ‘put America first’. One of the economic policies he has advocated for achieving this objective is the imposition of tariffs on imports which, according to him, unfairly threaten American jobs. On March 8 2018, he signed orders to impose new tariffs on metal imports. These would be 25% on steel and 10% on aluminium.

His hope is that, by cutting back on imports of steel and aluminium, the tariffs could protect the domestic industries which are facing stiff competition from the EU, South Korea, Brazil, Japan and China. They are also facing competition from Canada and Mexico, but these would probably be exempt provided negotiations on the revision of NAFTA rules goes favourably for the USA.

Assuming there were no retaliation from other countries, jobs would be gained in the steel and aluminium industries. According to a report by The Trade Partnership (see link below), the tariffs would increase employment in these industries by around 33 000. However, the higher price of these metals would cause job losses in the industries using them. In fact, according to the report, more than five jobs would be lost for every one gained. The CNN Money article linked below gives example of the US industries that will be hit.

But the costs are likely to be much greater than this. Accorinding to the law of comparative advantage, trade is a positive-sum game, with a net gain to all parties engaged in trade. Unless trade restrictions are used to address a specific market distortion in the trade process itself, restricting trade will lead to a net loss in overall benefit to the parties involved.

Clearly there will be loss to steel and aluminium exporters outside the USA. There will also be a net loss to their countries unless these metals had a higher cost of production than in the USA, but were subsidised by governments so that they could be exported profitably.

But perhaps the biggest cost will arise from possible retaliation by other countries. A trade war would compound the net losses as the world moves further from trade based on comparative advantage.

Already, many countries are talking about retaliation. For example, the EU is considering a ‘reciprocal’ tariff of 25% on cranberries, bourbon and Harley-Davidsons, all produced in politically sensitive US states (see the first The Economist article below). ‘As Jean-Claude Juncker, president of the European Commission, puts it, “We can also do stupid”.’ In fact, this is quite a politically astute move to put pressure on Mr Trump.

But cannot countries appeal to the WTO? Possibly, but this route might take some time. What is more, the USA has attempted to get around WTO rules by justifying the tariffs on ‘national security’ grounds – something allowed under Article XXI of WTO rules, provided it can be justified. This could possibly deter countries from retaliating, but it is probably unlikely. In the current climate, there seems to be a growing mood for flouting, or at least loosely interpreting, WTO rules.

Donald Trump has suggested that the Fed should cut interest rates by 1 percentage point and engage in a further round of quantitative easing. He wants to see monetary policy used to give a substantial boost to US economic growth at a time when inflation is below target. In a pair of tweets just before the meeting of the Fed to decide on interest rates, he said:

Donald Trump has suggested that the Fed should cut interest rates by 1 percentage point and engage in a further round of quantitative easing. He wants to see monetary policy used to give a substantial boost to US economic growth at a time when inflation is below target. In a pair of tweets just before the meeting of the Fed to decide on interest rates, he said: Since December 2015 the Fed has been raising interest rates by 0.25 percentage points at a time in a series of steps, so that the federal funds rate stands at between 2.25% and 2.5% (see chart). And since October 2017, it has also been engaged in quantitative tightening. In recent months it has been selling up to $50 billion of assets per month from its holdings of around $4000 billion and so far has reduced them by around £500 billion. It has, however, announced that the programme of QT will end in the second half of 2019.

Since December 2015 the Fed has been raising interest rates by 0.25 percentage points at a time in a series of steps, so that the federal funds rate stands at between 2.25% and 2.5% (see chart). And since October 2017, it has also been engaged in quantitative tightening. In recent months it has been selling up to $50 billion of assets per month from its holdings of around $4000 billion and so far has reduced them by around £500 billion. It has, however, announced that the programme of QT will end in the second half of 2019. The second issue is whether Trump’s proposed policy is a wise one.

The second issue is whether Trump’s proposed policy is a wise one. For these reasons, the Fed resisted calls for a large cut in interest rates and a return to quantitative easing. Instead it chose to keep interest rates on hold at its meeting on 1 May 2019.

For these reasons, the Fed resisted calls for a large cut in interest rates and a return to quantitative easing. Instead it chose to keep interest rates on hold at its meeting on 1 May 2019. Trump Urges Steep Fed Rate Cut as Central Bankers Hold Meeting

Trump Urges Steep Fed Rate Cut as Central Bankers Hold Meeting Back in October, we examined the

Back in October, we examined the  Brent crude prices have fallen from $86 per barrel in early October to just over $50 by the end of the year – a fall of 41 per cent. (Click

Brent crude prices have fallen from $86 per barrel in early October to just over $50 by the end of the year – a fall of 41 per cent. (Click  An agreement in principle was reached on September 30 between the USA, Canada and Mexico over a new trade deal to replace the North American Free Trade Agreement (NAFTA). President Trump had described NAFTA as ‘the worst trade deal maybe ever signed anywhere, but certainly ever signed in this country.’ The new deal, named the United States-Mexico-Canada Agreement, or USMCA, is the result of 14 months of negotiations, which have often been fractious. A provisional bilateral agreement was made

An agreement in principle was reached on September 30 between the USA, Canada and Mexico over a new trade deal to replace the North American Free Trade Agreement (NAFTA). President Trump had described NAFTA as ‘the worst trade deal maybe ever signed anywhere, but certainly ever signed in this country.’ The new deal, named the United States-Mexico-Canada Agreement, or USMCA, is the result of 14 months of negotiations, which have often been fractious. A provisional bilateral agreement was made  Another area where the USMCA agreement has made changes concerns trade in dairy products. This particularly affects Canada, which has agreed to allow more US dairy products tariff-free into Canada (see the CNN article at the end of the list of articles below). New higher quotas will give US dairy farmers access to 3.6% of Canada’s dairy market. They will still pay tariffs on dairy exports to Canada that exceed the quotas, ranging from 200% to 300%.

Another area where the USMCA agreement has made changes concerns trade in dairy products. This particularly affects Canada, which has agreed to allow more US dairy products tariff-free into Canada (see the CNN article at the end of the list of articles below). New higher quotas will give US dairy farmers access to 3.6% of Canada’s dairy market. They will still pay tariffs on dairy exports to Canada that exceed the quotas, ranging from 200% to 300%. The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.

Assuming there were no retaliation from other countries, jobs would be gained in the steel and aluminium industries. According to a report by The Trade Partnership (see link below), the tariffs would increase employment in these industries by around 33 000. However, the higher price of these metals would cause job losses in the industries using them. In fact, according to the report, more than five jobs would be lost for every one gained. The CNN Money article linked below gives example of the US industries that will be hit.

Assuming there were no retaliation from other countries, jobs would be gained in the steel and aluminium industries. According to a report by The Trade Partnership (see link below), the tariffs would increase employment in these industries by around 33 000. However, the higher price of these metals would cause job losses in the industries using them. In fact, according to the report, more than five jobs would be lost for every one gained. The CNN Money article linked below gives example of the US industries that will be hit. But perhaps the biggest cost will arise from possible retaliation by other countries. A trade war would compound the net losses as the world moves further from trade based on comparative advantage.

But perhaps the biggest cost will arise from possible retaliation by other countries. A trade war would compound the net losses as the world moves further from trade based on comparative advantage.