When did you last think about buying a new car? If not recently, then you may be in for a surprise next time you shop around for car deals. First, you will realise that the range of hybrid cars (i.e. cars that combine conventional combustion and electric engines) has widened significantly. The days when you only had a choice of Toyota Prius and another two or three hybrids are long gone! A quick search on the web returned 10 different models (although five of them belong to the Toyota Prius family), including Chevrolet Malibu, VW Jetta and Ford Fusion. And these are only the cars that are currently available in the UK market.

When did you last think about buying a new car? If not recently, then you may be in for a surprise next time you shop around for car deals. First, you will realise that the range of hybrid cars (i.e. cars that combine conventional combustion and electric engines) has widened significantly. The days when you only had a choice of Toyota Prius and another two or three hybrids are long gone! A quick search on the web returned 10 different models (although five of them belong to the Toyota Prius family), including Chevrolet Malibu, VW Jetta and Ford Fusion. And these are only the cars that are currently available in the UK market.

But the biggest surprise of all may be the number of purely (plug-) electric cars that are available to UK buyers these days. The table below provides a summary of total registrations of light-duty plug-electric cars by model in the UK, between 2010 and June 2016.

Source: Wikipedia, “Plug-in electric vehicles in the United Kingdom”

In 2010 there were nly 138 electric vehicles in total registered in the UK. They were indeed an unusual sight at that time – and good luck to you if you had one and you happened to run out of power in the middle of a journey. In 2011 this (small) number increased sevenfold – an increase that was driven mostly by the successful introduction of Nissan Leaf (635 electric Nissans were registered in the UK that year). And since then the number of electric vehicles registered in the country has increased with spectacular speed, at an average rate of 252% per year.

There is clearly strong interest in electric vehicles – an interest likely to increase as their price becomes more competitive. However, they are still very expensive items to buy, especially when compared with their conventional fuel-engine counterparts. What makes electric cars expensive? One thing is the cost of purchasing and maintaining a battery that can deliver a reasonable range. But the cost of batteries is falling, as more and more companies realise the potential of this new market and join the R&D race. As mentioned in a special report that was published recently in the FT:

The cost of lithium-ion batteries has fallen by 75 per cent over the past eight years, measured per kilowatt hour of output. Every time battery production doubles, costs fall by another 5 per cent to 8 per cent, according to analysts at Wood Mackenzie.

There is no doubt that more research will result in more efficient batteries, and will increase the interest in electric cars not only by consumers but also by producers, who already see the opportunity of this new global market.  Does this mean that prices will necessarily fall further? You might think so, but then you have to take into consideration the availability and cost of mining further raw materials to make these batteries (such as cobalt, which is one of the materials used in the making of lithium-ion batteries and nearly half of which is currently sourced from the Democratic Republic of Congo). This may lead to bottlenecks in the production of new battery units. In which case, the price of batteries (and, by extension, the price of electric cars) may not fall much further until some new innovation happens that changes either the material or its efficiency.

Does this mean that prices will necessarily fall further? You might think so, but then you have to take into consideration the availability and cost of mining further raw materials to make these batteries (such as cobalt, which is one of the materials used in the making of lithium-ion batteries and nearly half of which is currently sourced from the Democratic Republic of Congo). This may lead to bottlenecks in the production of new battery units. In which case, the price of batteries (and, by extension, the price of electric cars) may not fall much further until some new innovation happens that changes either the material or its efficiency.

The good news is that a lot of researchers are currently looking into these questions, and innovation will do what it always does: give solutions to problems that previously appeared insurmountable. They had better be fast because, according to estimates by Wood Mackenzie, the number of electric vehicles globally is expected to rise by over 50 times – from 2 million (in 2017) to over 125 million by 2035.

How many economists does it take to charge an electric car? I guess we are going to find out!

Articles

Information

Questions

- Using a demand and supply diagram, explain the relationship between the price of a battery and the market (equilibrium) price of a plug-in electric vehicle.

- List all non-price factors that influence demand for plug-in electric vehicles. Briefly explain each.

- Should the government subsidise the development and production of electric car batteries? Explain the advantages and disadvantages of such intervention and take a position.

I admit it, the title of my blog today is a little bit misleading – but at the same time very appropriate for today’s topic. Nancy Sinatra certainly wasn’t thinking about emigration when she was singing this song – it had nothing to do with it, after all. It is, however, very relevant to economists: Indeed, there are many economics papers discussing the effects of skilled immigration on host and source economies and regions.

I admit it, the title of my blog today is a little bit misleading – but at the same time very appropriate for today’s topic. Nancy Sinatra certainly wasn’t thinking about emigration when she was singing this song – it had nothing to do with it, after all. It is, however, very relevant to economists: Indeed, there are many economics papers discussing the effects of skilled immigration on host and source economies and regions.

Economists often use the term ‘brain drain’ to describe the migration of highly skilled workers from poor/developing to rich/developed economies. Such flows are anything but unusual. As The Economist points out in a recent article, ‘[I]n the decade to 2010–11 the number of university-educated migrants in the G20, a group of large economies that hosts two-thirds of the world’s migrants, grew by 60% to 32m according to the OECD, a club of mostly rich countries.’.

The effects of international migration are found to be overwhelmingly positive for both skilled migrant workers and their hosts. This is particularly true for highly skilled workers (such as academics, physicians and other professionals), who, through emigration, get the opportunity to earn a significantly higher return on their skills that what they might have had in their home country. Very often their home country is saturated and oversupplied with skilled workers competing for a very limited number of jobs. Also, they get the opportunity to practise their profession – which they might not have had otherwise.

But what about their home countries? Are they worse off for such emigration?

But what about their home countries? Are they worse off for such emigration?

There are different views when it comes to answering this question. One argument is that the prospect of international migration incentivises people in developing countries to accumulate skills (brain gain) – which they might not choose to do otherwise, if the expected return to skills was not high enough to warrant the effort and opportunity cost that comes with it. Beine et al (2011) find that:

Our empirical analysis predicts conditional convergence of human capital indicators. Our findings also reveal that skilled migration prospects foster human capital accumulation in low-income countries. In these countries, a net brain gain can be obtained if the skilled emigration rate is not too large (i.e. it does not exceed 20–30% depending on other country characteristics). In contrast, we find no evidence of a significant incentive mechanism in middle-income, and not surprisingly, high-income countries.

Other researchers find that emigration can have a significant negative effect on source economies (countries or regions) – especially if it affects a large share of the local workforce within a short time period. Ha et al (2016), analyse the effect of emigration on human capital formation and economic growth of Chinese provinces:

First, we find that permanent emigration is conducive to the improvement of both middle and high school enrollment. In contrast, while temporary emigration has a significantly positive effect on middle school enrollment it does not affect high school enrollment. Moreover, the different educational attainments of temporary emigrants have different effects on school enrollment. Specifically, the proportion of temporary emigrants with high school education positively affects middle school enrollment, while the proportion of temporary emigrants with middle school education negatively affects high school enrollment. Finally, we find that both permanent and temporary emigration has a detrimental effect on the economic growth of source regions.

So yes or no? Good or bad? As everything else in economics, the answer quite often is ‘it depends’.

Articles

- Open future: What educated people from poor countries make of the “brain drain” argument

The Economist, R.S. (27/8/18)

- Brain drain, brain gain, and economic growth in China

China Economic Review, Wei Ha, Junjian Yi and Junsen Zhang (April 2016)

- A Panel Data Analysis of the Brain Gain

World Development, Michel Beine, Ric Docquier and Cecily Oden-Defoort (Vol 39, No 4, pp 523–532, 2011)

Questions

- ‘The brain drain makes a bad situation worse, by stripping developing economies of their most valuable assets: skilled workers’. Discuss.

- Using Google, find data on the inflows and outflows of skilled labour for a developing country of your choice. Explain your results.

- ‘Brain drain’ or ‘brain gain’? What is your personal view on this debate? Explain your opinion by using anecdotal evidence, personal experience and examples.

- Referring to the previous question, write a critique of your answer.

So here we are, summer is over (or almost over if you’re an optimist) and we are sitting in front of our screens reminiscing about hot sunny days (at least I do)! There is no doubt, however: a lot happened in the world of politics and economics in the past three months. The escalation of the US-China trade war, the run on the Turkish lira, the (successful?) conclusion of the Greek bailout – these are all examples of major economic developments that took place during the summer months, and which we will be sure to discuss in some detail in future blogs. Today, however, I will introduce a topic that I am very interested in as a researcher: the liberalisation of energy markets in developing countries and, in particular, Mexico.

So here we are, summer is over (or almost over if you’re an optimist) and we are sitting in front of our screens reminiscing about hot sunny days (at least I do)! There is no doubt, however: a lot happened in the world of politics and economics in the past three months. The escalation of the US-China trade war, the run on the Turkish lira, the (successful?) conclusion of the Greek bailout – these are all examples of major economic developments that took place during the summer months, and which we will be sure to discuss in some detail in future blogs. Today, however, I will introduce a topic that I am very interested in as a researcher: the liberalisation of energy markets in developing countries and, in particular, Mexico.

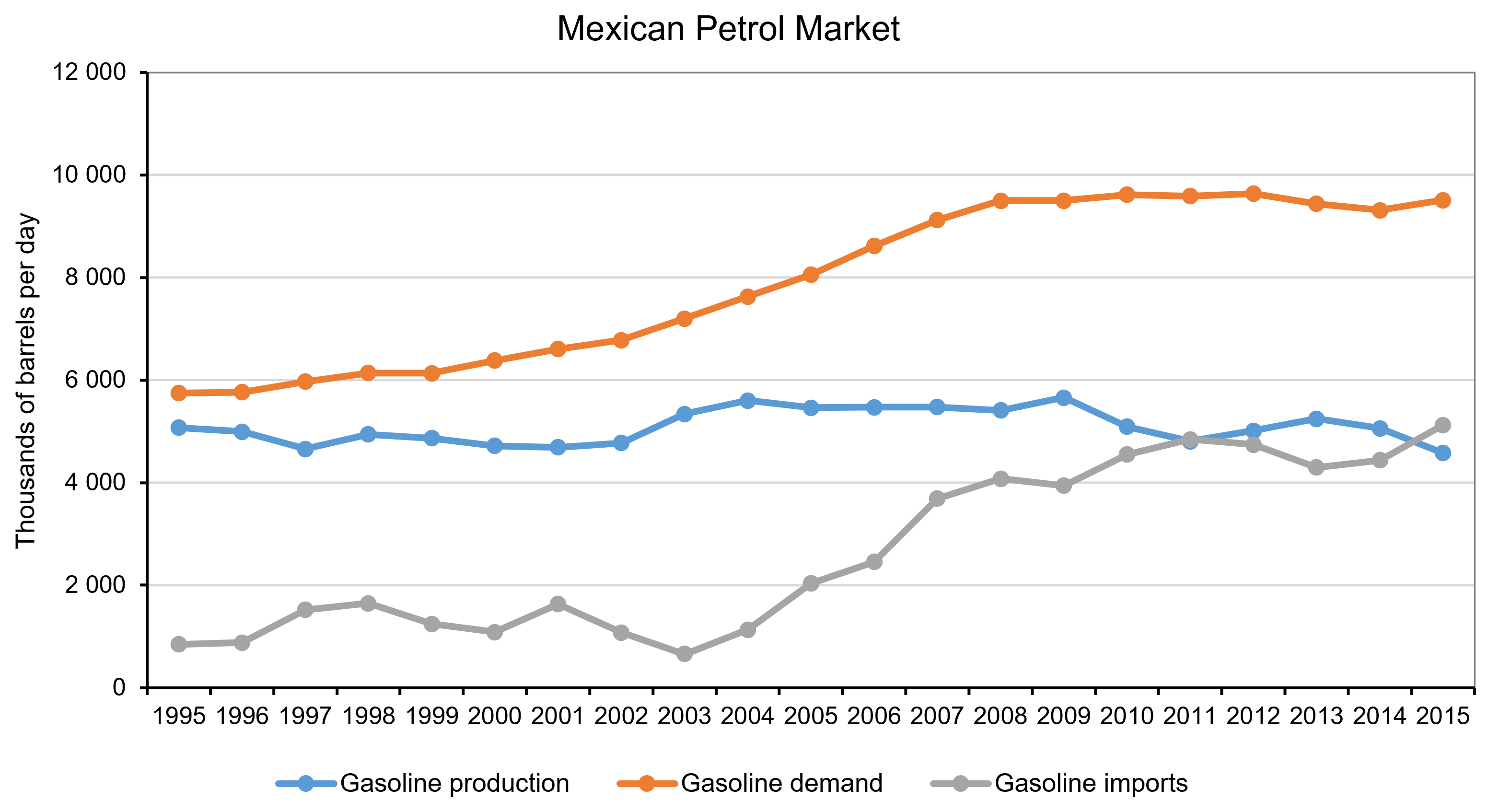

Why Mexico? Well, because it is a great example of a large developing economy that has been attempting to liberalise its energy market and reverse price setting and monopolistic practices that go back several decades. Until very recently, the price of petrol in Mexico was set and controlled by Pemex, a state monopolist. This put Pemex under pressure since, as a sole operator, it was responsible for balancing growing demand and costs, even to the detriment of its own finances.

The petrol (or ‘gasoline’) price liberalisation started in May 2017 and took place in stages – starting in the North part of Mexico and ending in November of the same year in the central and southern regions of the country. The main objective was to address the notable decrease in domestic oil production that put at risk the ability of the country to meet demand; as well as Mexico’s increasing dependency on foreign markets affected by the surge of the international oil price. The government has spent the past five years trying to create a stronger regulatory framework, while easing the financial burden on the state and halting the decline in oil reserves and production. Unsurprisingly, opening up a monopolistic market turns out to be a complex and bumpy process.

Source: Author’s calculations using data from the Energy Information Bank, Ministry of Energy, Mexico

Source: Author’s calculations using data from the Energy Information Bank, Ministry of Energy, Mexico

Despite all the reforms, retail petrol prices have kept rising. Although part of this price rise is demand-driven, an increasing number of researchers highlight the significance of the distribution of oil-related infrastructure in determining price outcomes at the federal and regional (state) level. Saturation and scarcity of both distribution and storage infrastructure are probably the two most significant impediments to opening the sector up to competition (Mexico Institute, 2018). You see, the original design of these networks and the deployment of the infrastructure was not aimed at maximising efficiency of distribution – the price was set by the monopolist and, in a way that was compliant with government policy (Mexico Institute, 2018). Economic efficiency was not always part of this equation. As a result, consumers located in better-deployed areas were subsidising the inherent logistics costs of less ‘well endowed’ regions by facing an artificially higher price than they would have in a competitive market.

But what about now? Do such differences in the allocation of infrastructure between regions lead to location-related differences in the price of petrol? If so, by how much? And, what policies should the government pursue to address such imbalances? These are all questions that I explore in one of my recent working papers titled ‘Widening the Gap: Lessons from the aftermath of the energy market reform in Mexico’ (with Hugo Vallarta) and I will be sharing some of the answers with you in a future blog.

Articles

Data

Questions

- Are state-owned monopolies effective in delivering successful market outcomes? Why yes, why no?

- In the case of Mexico, are you surprised about the complexities that were involved with opening up markets to competition? Explain why.

- Use Google to identify countries in which energy markets are controlled by state-owned monopolies.

The Economist is probably not the kind of newspaper that you will read more than once per issue – certainly not two years after its publication date. That is because, by definition, financial news articles are ephemeral: they have greater value, the more recent they are – especially in the modern financial world, where change can be strikingly fast. To my surprise, however, I found myself reading again an article on inequality that I had first read two years ago – and it is (of course) still relevant today.

The Economist is probably not the kind of newspaper that you will read more than once per issue – certainly not two years after its publication date. That is because, by definition, financial news articles are ephemeral: they have greater value, the more recent they are – especially in the modern financial world, where change can be strikingly fast. To my surprise, however, I found myself reading again an article on inequality that I had first read two years ago – and it is (of course) still relevant today.

The title of the article was ‘You may be higher in the global wealth pyramid than you think’ and it discusses exactly that: how much wealth does it take for someone to be considered ‘rich’? The answer to this question is of course, ‘it depends’. And it does depend on which group you compare yourself against. Although this may feel obvious, some of the statistics that are presented in this article may surprise you.

According to the article

If you had $2200 to your name (adding together your bank deposits, financial investments and property holdings, and subtracting your debts) you might not think yourself terribly fortunate. But you would be wealthier than half the world’s population, according to this year’s Global Wealth Report by the Crédit Suisse Research Institute. If you had $71 560 or more, you would be in the top tenth. If you were lucky enough to own over $744 400 you could count yourself a member of the global 1% that voters everywhere are rebelling against.

For many (including yours truly) these numbers may come as a surprise when you first see them. $2200 in today’s exchange rate is about £1640. And this is wealth, not income – including all earthly possessions (net of debt). £1640 of wealth is enough to put you ahead of half of the planet’s population. Have a $774 400 (£556 174 – about the average price of a two-bedroom flat in London) and – congratulations! You are part of the global richest 1% everyone is complaining about…

Such comparisons are certainly thought provoking. They show how unevenly wealth is distributed across countries. They also show that countries which are more open to trade are more likely to have benefited the most from it. Take a closer look at the statistics and you will realise that you are more likely to be rich (compared to the global average) if you live in one of these countries.

Of course, wealth inequality does not happen only across countries – it happens also within countries. You can own a two-bedroom flat in London (and be, therefore, part of the 1% global elite), but having to live on a very modest budget because your income (which is a flow variable, as opposed to wealth, which is a stock variable) has not grown fast enough in relation to other parts of the national population.

Of course, wealth inequality does not happen only across countries – it happens also within countries. You can own a two-bedroom flat in London (and be, therefore, part of the 1% global elite), but having to live on a very modest budget because your income (which is a flow variable, as opposed to wealth, which is a stock variable) has not grown fast enough in relation to other parts of the national population.

Would you be better off if there were less trade? Certainly not – you would probably be even poorer, as trade theories (and most of the empirical evidence I am aware of) assert. Why do we then talk so much about trade wars and trade restrictions recently? Why do we elect politicians who advocate such restrictions? It is probably easier to answer these questions using political than economic theory (although game theory may have some interesting insights to offer – have you heard of the ‘Chicken game‘?). But as I am neither political scientists nor a game theorist, I will just continue to wonder about it.

Articles and information

Questions

- Were you surprised by the statistics mentioned in this report? Explain why.

- Do you think that income inequality is a natural consequence of economic growth? Are there pro-growth policies that can be used to tackle it?

- Identify three ways in which widening income inequality can hurt economies (and societies).

How much do you know about cryptocurrencies? Even if you don’t know much you are very likely to have heard about the most popular member of the family: Bitcoin. Bitcoin (BTC) has been around for some time now (see the blog Bubbling Bitcoin). It was first released in 2009 by its inventor (the mysterious Satoshi Nakamoto, whose real identity still remains unknown), and since then it has gradually increased in popularity.

How much do you know about cryptocurrencies? Even if you don’t know much you are very likely to have heard about the most popular member of the family: Bitcoin. Bitcoin (BTC) has been around for some time now (see the blog Bubbling Bitcoin). It was first released in 2009 by its inventor (the mysterious Satoshi Nakamoto, whose real identity still remains unknown), and since then it has gradually increased in popularity.

According to the Bitcoin Market Journal (a specialised blog, commenting on trends in digital currencies – primarily Bitcoin), there are currently about 29 million digital wallets holding at least 0.001 BTC, although some individual users may own multiple wallets.

Although BTC is the most popular digital currency (and the first one to become widely recognisable), it is certainly not the only one. There are currently more than 400 recognisable cryptocurrencies traded in special digital exchanges (twice this number if you count smaller, less successful ones) with a total capitalisation of $700 billion at its peak (January 3, 2018) – although since then the market has lost a significant part of this value (but it’s still worth 100s of billion of US dollars).

If you have heard about Bitcoin before, chances are you first searched for it sometime between December 2017 and January 2018; that is when the value of Bitcoin soared to $20 000 a piece. A search on Google Trends (a Google utility that shows how many people have searched over a period of time for a certain term – in this case “Bitcoin”) shows this very clearly.

So what do people do with Bitcoin and other cryptocurrencies? The truth is that the majority of users use them for speculative purposes: they buy and sell them, in the hope of making a profit. Due to its extreme volatility (it is very common for the price of the larger cryptocurrencies to fluctuate by 10–20% daily) and the unregulated nature of the cryptocurrency market, it is hardly surprising that most users treat them as very high-risk commodity. This is also why digital currencies tend to attract attention (and new users) when their price soars.

However, cryptocurrencies are not only used for speculation. They can also be used to facilitate transactions. Indeed, according to Wikipedia, there are currently more than 100 000 merchants accepting BTC as a form of payment (online or offline with wallet readers). Financial technology (‘Fintech’) is catching up with this market and some new companies try to compete with the traditional payment networks (Mastercard, Visa and others) by launching plastic cards linked with crypto-wallets (primarily Bitcoin).

Santander bank has expressed an interest in exploring this market further. It is certain that if the market for cryptocurrencies keeps growing at this pace, there will be a lot more challenger fintech firms launching new products that will make it easier to use digital currencies in everyday life.

Cryptocurrencies, therefore, are likely to have a significant impact on the way we pay for our transactions. They can be used to lower transaction costs (e.g. by simplifying the process of sending money abroad), speed up the processing of payments, facilitate microfinancing and transactions in some of the poorest places on earth – where the closest bank may be 50 miles away or further from where people live).

Cryptocurrencies, therefore, are likely to have a significant impact on the way we pay for our transactions. They can be used to lower transaction costs (e.g. by simplifying the process of sending money abroad), speed up the processing of payments, facilitate microfinancing and transactions in some of the poorest places on earth – where the closest bank may be 50 miles away or further from where people live).

But there is a dark side to these products. They have been linked to tax-evasion for instance, as many people who trade digital currencies fail to declare capital gains to national tax authorities. They can be used to overcome capital controls and other restrictions imposed by national governments (the case of Greece comes to mind as a recent example).

They have also been blamed for facilitating illegal trading activities, such as in drugs and weapons, due to the anonymity that some of these coins are thought to offer to their users – although quite often they are much easier to trace than their users believe.

Cryptocurrencies do have the potential to change the way we live. They also have the potential to become the biggest Ponzi scheme in the history of mankind.

Over the next few months, I will write a number of blogs to explore the literature on the economics of cryptocurrencies, and discuss some of the major challenges that needs to be overcome if this technology is to become mainstream.

Articles and information

Questions

- How much do you know about Bitcoin and other cryptocurrencies? When did you first find out about them and what triggered your interest?

- Would you be willing to accept payment in BTC? Why yes? Why no?

- Identify five ways in which the use of cryptocurrencies can benefit or damage the global economy.