Officials from Rugby Union’s Aviva Premiership recently announced that the salary cap used by the league would increase from £4.76 million to £5.1 million per team for the 2015-16 season. It is not the only professional sports league to use this type of regulation. The NFL currently has a salary cap of $133 million/team while in the NBA it is set at $63 million/team. What is the rationale for placing restrictions on the amount an organisation can pay its employees? How do these caps work in practice?

Officials from Rugby Union’s Aviva Premiership recently announced that the salary cap used by the league would increase from £4.76 million to £5.1 million per team for the 2015-16 season. It is not the only professional sports league to use this type of regulation. The NFL currently has a salary cap of $133 million/team while in the NBA it is set at $63 million/team. What is the rationale for placing restrictions on the amount an organisation can pay its employees? How do these caps work in practice?

A salary cap is a regulation that limits the amount that an organisation can pay its employees. Sanctions are usually imposed if the ceiling is broken.

It is hard to imagine this type of policy being introduced in most industries. For example there may have been a number of calls for much greater regulation of the big six firms in the energy market with the Labour party suggesting that prices should be frozen for 20 months. However in amongst all the calls for more intervention, nobody has suggested that limits should be placed on the wages that these firms pay their staff.

One example where the authorities are thinking of intervening on pay is the proposal by the European Union to introduce a cap on the size of bonuses that can be paid by firms in the banking industry. However this is more of a constraint on the method of remuneration rather than an absolute limit on the level of pay. If the policy was introduced there would be nothing preventing firms from increasing basic salaries in order to make up for any shortfall caused by the reduction in bonuses.

There is one sector of the economy where salary caps are widely used – professional team sports. There are a number of different ways they have been implemented. For example the Football Association once placed a limit on the amount that a club could pay an individual player. This was originally set at £4/week in 1901 and increased to £20/week before it was finally abolished in 1961.

In recent times it has been far more common for salary caps in professional sports leagues to place limits on the size of a team’s total wage bill rather than the amount that can be paid to an individual player. This is the case in the Aviva Premiership, the NFL and the NBA. Perhaps it would be more accurate to refer to these policies as a cap on payrolls rather than on salaries.

The Aviva Premiership gives the following 4 reasons for having the payroll cap that it first introduced in 1999:

|

|

| • |

To ensure the financial viability of the clubs; |

| • |

To ensure a competitive Aviva Premiership Rugby competition; |

| • |

To control inflationary pressures on clubs’ costs; |

| • |

To provide a level playing field for the clubs. |

It is claimed that the policy has helped the league to achieve these objectives as (a) more clubs are now breaking even and (b) compared with other rugby competitions it has the greatest number of games that finish with less than one score between the teams.

There are a number of different ways that a payroll cap can be implemented. With an absolute payroll scheme all the teams in the league, no matter what their size, face the same constraint. This is the policy adopted by the NFL, NBA and the Aviva Premiership. An alternative is to implement a percentage payroll cap. Examples of these can be found in League 1 and League 2 of the English Football League. League 1 teams can spend up to 60% of their turnover on wages while League 2 teams can spend up to 55% of their turnover on wages. Obviously this means that well supported clubs with a larger turnover can spend more on players’ wages than less well supported clubs with a smaller turnover.

Another way that payroll caps differ is whether they are ‘hard’ caps or ‘soft’ caps. With a ‘hard’ cap there are no exceptions to the scheme. All the teams’ payrolls must remain within the same limit set by the league officials. With a ‘soft’ cap the authorities identify some exceptions that enable clubs to exceed the limit. The payroll cap used in rugby union is an example of a soft cap and works in the following way.

There are a number of elements to the scheme:

|

|

| • |

The senior salary cap; |

| • |

Excluded players; |

| • |

The academy credits. |

The senior salary cap is the major part of the regulation and the Aviva Premiership announced that this would increase from £4.76 million per team in the current season to £5.1 million per team for 2015-16. The Academy credits enable teams to exceed this £5.1 million limit if they train and develop younger players. The teams have to prove that they have young players that meet the following criteria:

The senior salary cap is the major part of the regulation and the Aviva Premiership announced that this would increase from £4.76 million per team in the current season to £5.1 million per team for 2015-16. The Academy credits enable teams to exceed this £5.1 million limit if they train and develop younger players. The teams have to prove that they have young players that meet the following criteria:

|

|

| • |

They are under the age of 24 before the season started; |

| • |

They joined the youth academy before their eighteenth birthday; |

| • |

They earn more than £30,000 per year. |

For a player who meets these conditions it is only their salary in excess of £30,000/year that is considered. For example if a young player was paid £50,000/year then only £20,000 of his wages would count towards the team’s payroll cap. The first £30,000 would not count. The Aviva Premiership recently announced that a home grown player credit would replace the academy credits. Under the new scheme the upper age limit will be removed and clubs can claim up to £400,000 in allowances. This means that teams could spend up to £5.5 million a year on wages if they train and develop younger players.

However other exceptions means that teams can exceed even this figure. The payroll cap arrangements allow teams to identify one player whose wages are not included when the payroll cap is calculated. In order to be nominated the exempted player has to meet certain criteria. In the 2015-16 season teams will be allowed to have two excluded players.

Sir Iain McGeechan has suggested that these changes will increase the effective salary cap to £7 million/year with some star players earning £1 million/season. However this would still be below the level of the basic salary cap in the French Rugby Union Super 14 League which is €10 million per season (approximately £8.5 million)

Premiership salary cap will leave small clubs playing catch-up The Telegraph (20/9/14)

Bath line up move for Australian Will Genia as new salary cap regulations come into effectThe Telegraph (15/9/14)

The salary cap in Rugby Union Law in Sport (15/4/14)

Barwell blasts salary cap ‘cheats’ ESPN (1/3/13)

Salary Cap changes confirmed Premiership Rugby (17/9/14)

What is meant by a salary cap in Sport and would this ever be used in English football? In Brief (accessed on 22/9/14)

Questions

- Draw a diagram to illustrate the impact of a salary cap on a perfectly competitive market and explain your answer.

- Which teams in the Aviva Premiership would be in favour of the increase in the salary cap and which teams would be opposed? Explain your answer.

- Do you think that an absolute or percentage salary cap would be more effective at maintaining competitive balance in a league? Which teams would be more in favour of an absolute salary cap?

- Why do think some leagues have introduced a ‘soft’ rather than a ‘hard’ salary caps?

- To what extent do you think that salary/payroll caps are consistent with European single market principles about the free movement of people?

- Officials from the Aviva Premiership provide the clubs with a long list of payments which must be counted as part of a player’s salary. These include holiday costs, school fees, payment for off-field activities on behalf of the club, payments in kind and signing on fees. Why do you think that the authorities provide such a large list?

- Find out the criteria that must be met in order for a player to be exempted from the team’s payroll calculations. Provide some reasons why you think these criteria were used.

The instability of the economy was clearly demonstrated by the events of the late 2000s. Economists have devoted considerable energies to understanding the determinants of the business cycle. Increasing attention is focused on the role that credit cycles play in contributing to or exacerbating cycles. Therefore, data on lending by banks is followed keenly by policymakers who wish to avoid the repeat of the pace of growth in credit seen in the period preceding the financial crisis. Interestingly, the latest data from the Bank of England show that lending by financial institutions to households (net of repayments) rose in July to its highest level since November 2009.

The instability of the economy was clearly demonstrated by the events of the late 2000s. Economists have devoted considerable energies to understanding the determinants of the business cycle. Increasing attention is focused on the role that credit cycles play in contributing to or exacerbating cycles. Therefore, data on lending by banks is followed keenly by policymakers who wish to avoid the repeat of the pace of growth in credit seen in the period preceding the financial crisis. Interestingly, the latest data from the Bank of England show that lending by financial institutions to households (net of repayments) rose in July to its highest level since November 2009.

The idea of credit cycles is not new. But, the financial crisis of the late 2000s has helped to reignite analysis and interest. Many economists have revisited the work of Hyman Minsky (1919–1996), an American economist, who argued that financial cycles are an inherent part of the economic cycle and contribute to fluctuations in real GDP. Notably, he argued that credit extended to households and businesses is pro-cyclical so that flows of credit extended by banks are larger when the growth of the economy’s output is stronger. Since credit flows are dependent on the phase of the business cycle, they are said to be endogenous to the path of output. The key point here is that there is an inherent mechanism within the economy which is potentially destabilising.

Banks, it is argued, may use the growth of the economy’s output as an indicator of the riskiness of its lending. Households and businesses may undertake a similar assessment. After a period of sustained growth banks and investors become more confident about the future path of the economy and, consequently, in the returns of assets. This means that there is a role for psychology in understanding the business cycle.

If we look at the chart, this period of heightened confidence may correspond with the period starting from the late 1990s. Between 1998 and 2007 the average monthly net flow of credit to private non-financial corporations and households was £9.4 billion. In other words, households and businesses were acquiring a staggering £9.4 billion of additional debt from banks each month. But, this was as high as £14.0 billion per month in 2007. (Click here for a PowerPoint of the chart.)

If we look at the chart, this period of heightened confidence may correspond with the period starting from the late 1990s. Between 1998 and 2007 the average monthly net flow of credit to private non-financial corporations and households was £9.4 billion. In other words, households and businesses were acquiring a staggering £9.4 billion of additional debt from banks each month. But, this was as high as £14.0 billion per month in 2007. (Click here for a PowerPoint of the chart.)

What helped to fuel the impact of heightened confidence on credit provision was financial innovation. In particular, the bundling of assets, such as mortgages, to form financial instruments which could then be purchased by investors helped to provide financial institutions with further funds for lending. This is the process of securitisation. The result was that during the 2000s as households and businesses began to acquire larger debts their financial well-being became increasingly stretched. This was hastened by central banks raising interest rates. The intention was to dampen the rising rate of inflation, partly attributable to rising global commodity prices, such as oil. Suddenly, euphoria was replaced with pessimism.

Some argue that a Minsky moment had occurred. Many countries then witnessed a balance sheet recession. As individual households and businesses try and improve their own financial well-being they collectively contribute to its worsening. For instance, large-scale attempts to sell assets, such as shares or property, only help to cause their value to decline.

A global response to the events of the financial crisis has been for policy-makers to pay more attention to the aggregate level of credit provision. The chart shows that lending in 2014 is more robust than it has been form some time. Across the first seven months of 2014 the average monthly net flow of credit extended by banks to households and businesses (private non-financial corporations) has been £2.2 billion.

However, the 2014-rebound of credit is wholly attributable to lending to households. Net lending to households has averaged £2.7 billion per month while businesses have been repaying credit to banks to the tune of £437 million per month – something that businesses have collectively done in each year from 2009. While net lending to households remains considerably lower than pre-financial crisis levels, it will be something that policymakers will be watching very closely. This, in turn, means that they will be paying particular interest to the housing and mortgage markets.

Articles

Appetite for loans picks up again, say major banks BBC News (23/9/14)

Business lending by UK banks is down by £941m Herald Scotland, Ian McConnell (27/8/14)

How bank lending fell by £365 BILLION in five years… much to the delight of controversial payday loan firms Mail, Louise Eccles (7/09/14)

U.K.’s Big Banks Cut Lending by $595 Billion, KPMG Says Bloomberg, Richard Partington (8/9/14)

UK banks’ home loan approvals fall to 12-month low – BBA Reuters, Andy Bruce and Tom Heneghan (23/9/14)

Data

Bankstats (Monetary and Financial Statistics) – Latest Tables Bank of England

Statistical Interactive Database Bank of England

Questions

- What is meant by the term the business cycle?

- What does it mean for the determinants of the business cycle to be endogenous? What about if they are exogenous?

- Outline the ways in which the financial system can impact on the spending behaviour of households. Repeat the exercise for businesses.

- How might uncertainty affect spending and saving by households and businesses?

- What does it mean if bank lending is pro-cyclical?

- Why might lending be pro-cyclical?

- How might the differential between borrowing and saving interest rates vary over the business cycle?

- Explain what you understand by net lending to households or firms. How does net lending affect their stock of debt?

Many of you reading the articles on this website will be just about to start, or will have just started, studying economics at university. For some of you this will involve building on the knowledge you obtained prior to university, whereas for others it will be the first time you have ever studied the subject before. Will studying economics change the way you behave? Should it come with a health warning?

Many of you reading the articles on this website will be just about to start, or will have just started, studying economics at university. For some of you this will involve building on the knowledge you obtained prior to university, whereas for others it will be the first time you have ever studied the subject before. Will studying economics change the way you behave? Should it come with a health warning?

Can studying economics change the way you think and behave? The subject is often sold to prospective students on the grounds that it can. For example it is stated on the Economics Network’s Why Study Economics? website that

The economic way of thinking can help us make better choices

However, is it possible that studying economics could change people’s behaviour in a way that would be to the detriment of society? Some observers have argued that it can. They have suggested that students might be influenced by some of the assumptions that are made in traditional economic theory.

As social scientists, economists are always trying to analyse human behaviour. However, people vary in many different ways and have very diverse preferences. If we want to build a theory that predicts how people will behave and respond in different situations, then some type of simplifying assumptions are inevitable.

Traditionally one of the key simplifying assumptions that economists have used in their theories of human behaviour is that people make decisions in their own self-interest. There is some debate about exactly what self-interest means. For example it could be argued that giving £10 to charity is acting in your own self-interest if it gives you more pleasure than spending that £10 on yourself. However, in many of the economic theories that you first study in economics a narrow meaning of self-interest tends to be used. This is clearly illustrated by the following quote from Milgrom and Roberts. Referring to economic theory they state that:

It is often assumed that people behave as if they were entirely motivated by narrow, selfish concerns

It is important to make it clear that economists are not assuming that people behave in a selfish manner all of the time. Instead, they are assuming that the people in their theories are acting in a selfish manner. The value of making this assumption is whether the predictions about human behaviour that follow from using it are supported by evidence from the real world.

Some researchers have argued that when people study economic theory built on this assumption it makes them more likely to behave in a selfish way. The evidence for this comes from a range of research papers. Here are some findings:

Economics students were more likely than those studying other subjects to recommend the most expensive plumber to a student society if that plumber offered the student a side payment.

Students took part in an experiment in a computer room where they could either keep the money they had been given or donate it to a public good. On average the economics students kept more of the money.

Economics professors gave less money to charity than professors of other subjects such as psychology and sociology.

Some studies also found that selfish people were more likely to choose economics as a subject to study and became more selfish after they had studied it for some time.

If you are about to begin your study of economics then perhaps you should take care that your behaviour outside the classroom is not being unduly influenced by some of the assumptions you are learning about inside the classroom. On a more practical note perhaps you should avoid sharing a restaurant bill or buying rounds of drinks when in the company of other economists!!!

However on a brighter note, the evidence in these papers can be interpreted in a number of different ways. There are even some studies that found economics students were less selfish than those on other courses.

Re-Post: Does Studying Economics Make You Selfish? The Splintered Mind (21/11/12)

Does studying economics make you more selfish? BBC (22/10/13)

Does Studying Economics Breed Greed? Huffington Post (22/10/13)

The Dismal Education The New York Times (16/12/11)

Does Economics Make You a Bad Person? Conversable Economist (31/3/14)

Economists aren’t all bad FT Magazine (11/4/14)

Questions

- What is an economic model? Why is it necessary to make simplifying assumptions?

- How are economic models judged? How important is it for the assumptions to accurately describe the real world?

- Try to find some jokes that have been made about the use of assumptions in economic theory.

- Can you think of any alternative explanations for the results found in the research papers referred to in the case?

- Try to find a research paper that finds evidence that economics students are less selfish than other students.

- What is a public good? Explain why someone with selfish preferences would not contribute to the public good.

The British love to talk about house prices. Stories about the latest patterns in prices regularly adorn the front pages of newspapers. We take this opportunity to update an earlier blog looking not only at house prices in the UK, but in other countries too (see the (not so) cool British housing market). This follows the latest data release from the ONS which shows the UK’s annual house price inflation rate ticking up from 10.2 per cent in June to 11.7 per cent in July and which contrasts markedly with the annual rate in July 2013 of 3.3 per cent.

The British love to talk about house prices. Stories about the latest patterns in prices regularly adorn the front pages of newspapers. We take this opportunity to update an earlier blog looking not only at house prices in the UK, but in other countries too (see the (not so) cool British housing market). This follows the latest data release from the ONS which shows the UK’s annual house price inflation rate ticking up from 10.2 per cent in June to 11.7 per cent in July and which contrasts markedly with the annual rate in July 2013 of 3.3 per cent.

The July annual house price inflation figure of 11.7 per cent for the UK is heavily influenced by the rates in London and the South East. In London house price inflation is running at 19.1 per cent while in the South East it is 12.2 per cent. Across the rest of the UK the average rate is 7.9 per cent, though this has to be seen in the context of the July 2013 rate of 0.8 per cent.

Chart 1 shows house price inflation rates across the home nations since the financial crisis of the late 2000s. It shows a rebound in house price inflation over the second half of 2013 and across 2014. In July 2014 house price inflation was running at 12.0 per cent in England, 7.6 per cent in Scotland, 7.4 per cent in Wales and 4.5 per cent in Northern Ireland. If we use the East Midlands as a more accurate barometer of England, annual house price inflation in July was 7.6 per cent – the same as across Scotland. (Click here for a PowerPoint of the chart.)

Chart 1 shows house price inflation rates across the home nations since the financial crisis of the late 2000s. It shows a rebound in house price inflation over the second half of 2013 and across 2014. In July 2014 house price inflation was running at 12.0 per cent in England, 7.6 per cent in Scotland, 7.4 per cent in Wales and 4.5 per cent in Northern Ireland. If we use the East Midlands as a more accurate barometer of England, annual house price inflation in July was 7.6 per cent – the same as across Scotland. (Click here for a PowerPoint of the chart.)

Consider a more historical perspective. The average annual rate of growth since 1970 is 9.7 per cent in the UK, 9.7 per cent in England (9.6 per cent in the East Midlands), 9.6 per cent in Wales, 8.8 per cent in Scotland and 8.7 per cent in Northern Ireland. Therefore, house prices in the home nations have typically grown by 9 to 10 per cent per annum. But, as recent experience shows, this has been accompanied by considerable volatility. An interest question is the extent to which these two characteristics of British house prices are unique to Britain. To address this question, let’s go international.

Chart 2 shows annual house price inflation rates for the UK and six other countries since 1996. Interestingly, it shows that house price volatility is a common feature of housing markets. It is not a uniquely British thing. It too shows shows something of a recovery in global house prices. However, the rebound in the UK and the USA does appear particularly strong compared with core eurozone economies, like the Netherlands and France, where the recovery is considerably more subdued. (Click here for a PowerPoint of the chart.)

Chart 2 shows annual house price inflation rates for the UK and six other countries since 1996. Interestingly, it shows that house price volatility is a common feature of housing markets. It is not a uniquely British thing. It too shows shows something of a recovery in global house prices. However, the rebound in the UK and the USA does appear particularly strong compared with core eurozone economies, like the Netherlands and France, where the recovery is considerably more subdued. (Click here for a PowerPoint of the chart.)

The chart captures very nicely the effect of the financial crisis and subsequent economic downturn on global house prices. Ireland saw annual rates of house price deflation exceed 24 per cent in 2009 compared with rates of deflation of 12 per cent in the UK. Denmark too suffered significant house price deflation with prices falling at an annual rate of 15 per cent in 2009.

House price volatility appears to be an inherent characteristic of housing markets worldwide. Consider now the extent to which house prices rise over the longer term. In doing so, we analyse real house price growth after having stripped out the effect of consumer price inflation. Real house price growth measures the growth of house prices relative to consumer prices.

Chart 3 shows real house prices since 1995 Q1. (Click here for a PowerPoint of the chart.) It shows that up to 2014 Q2, real house prices in the UK have risen by a factor of 2.4 This is a little less than in Sweden where prices are 2.6 times higher. Nonetheless, the increase in real house prices in the UK and Sweden is significantly higher than in the other countries in the sample. In particular, in the USA real house prices in 2014 Q2 were only 1.2 times higher than in 1995 Q1. Therefore, in America actual house prices, when viewed over the past 19 years or so, have grown only a little more quickly than consumer prices.

Chart 3 shows real house prices since 1995 Q1. (Click here for a PowerPoint of the chart.) It shows that up to 2014 Q2, real house prices in the UK have risen by a factor of 2.4 This is a little less than in Sweden where prices are 2.6 times higher. Nonetheless, the increase in real house prices in the UK and Sweden is significantly higher than in the other countries in the sample. In particular, in the USA real house prices in 2014 Q2 were only 1.2 times higher than in 1995 Q1. Therefore, in America actual house prices, when viewed over the past 19 years or so, have grown only a little more quickly than consumer prices.

The latest data on house prices suggest that house price volatility is not unique to the UK. The house price roller coaster is an international phenomenon. However, the rate of growth in UK house prices over the longer term, relative to consumer prices, is markedly quicker than in many other countries. It is this which helps to explain the amount of attention paid to the UK housing market. The ride continues.

Data

House Price Indices: Data Tables Office for National Statistics

Articles

Property prices in all regions of the UK grow at the fastest annual pace seen in seven years Independent, Gideon Spanier (16/9/14)

UK House Prices Have Not Soared This Fast In Seven Years The Huffington Post UK, Asa Bennett (16/9/14)

UK house prices hit new record as London average breaks £500,000 Guardian, Phillip Inman (6/12/14)

Six regions hit new house price peak, says ONS BBC News, (16/9/14)

Welsh house prices nearing pre-crisis peak BBC News, (16/9/14)

Questions

- What is meant by the annual rate of house price inflation? What about the annual rate of house price deflation?

- What factors are likely to affect housing demand?

- What factors are likely to affect housing supply?

- Explain the difference between nominal and real house prices. What does a real increase in house prices mean?

- How might we explain the recent differences between house price inflation rates in London and the South East relative to the rest of the UK?

- What might explain the very different long-term growth rates in real house prices in the USA and the UK?

- Why were house prices so affected by the financial crisis?

- What factors help explain the volatility in house prices?

- How might we go about measuring the affordability of housing?

- In what ways might house price patterns impact on the macroeconomy?

Merlin Entertainments PLC is one of the largest operator of visitor attractions in the world and owns over a third of the most popular theme parks in Europe. It runs the four most visited parks in England – Alton Towers, Legoland Windsor, Thorpe Park and Chessington World of Adventures as well as the most popular theme park in Italy – Gardaland. Alton Towers alone had 2.5 million visitors in 2013. Anybody thinking of going to one of these attractions is faced with a wide range of different entry fees .

Merlin Entertainments PLC is one of the largest operator of visitor attractions in the world and owns over a third of the most popular theme parks in Europe. It runs the four most visited parks in England – Alton Towers, Legoland Windsor, Thorpe Park and Chessington World of Adventures as well as the most popular theme park in Italy – Gardaland. Alton Towers alone had 2.5 million visitors in 2013. Anybody thinking of going to one of these attractions is faced with a wide range of different entry fees .

Theme parks and tourist attractions have market power so their owners have to make some interesting pricing decisions. They have to tackle the same dilemma that confronts any seller that faces a downward sloping demand curve for its goods/services.

One option for the firm would be to increase the entry fee. This would produce higher profits per visitor as some of the surplus from the transaction previously enjoyed by the consumer will be extracted by the seller and converted into producer surplus. Unfortunately for the business the higher price, all other things equal, will also result in fewer visitors. Some people will be deterred from visiting because of the higher price and the seller will lose out on potential revenue.

An alternative strategy would be for the theme park to reduce its entry fee. All other things equal, this will increase the number of visitors. However, it would also mean that the profit per customer would fall. The frustrating issue for the seller is that some of its customers, who would still have visited the attraction at the higher price, are now able to get a better deal.

This dilemma exists if the seller has to charge all of its different customers the same entry fee. If it could charge a higher entry fee to those customers who would be willing to pay more and a lower entry fee to those who would be willing to pay less then it could make more money. Extra revenue could be obtained from those additional sales that take place at the lower price while more consumer surplus could be extracted from those still paying the higher price.

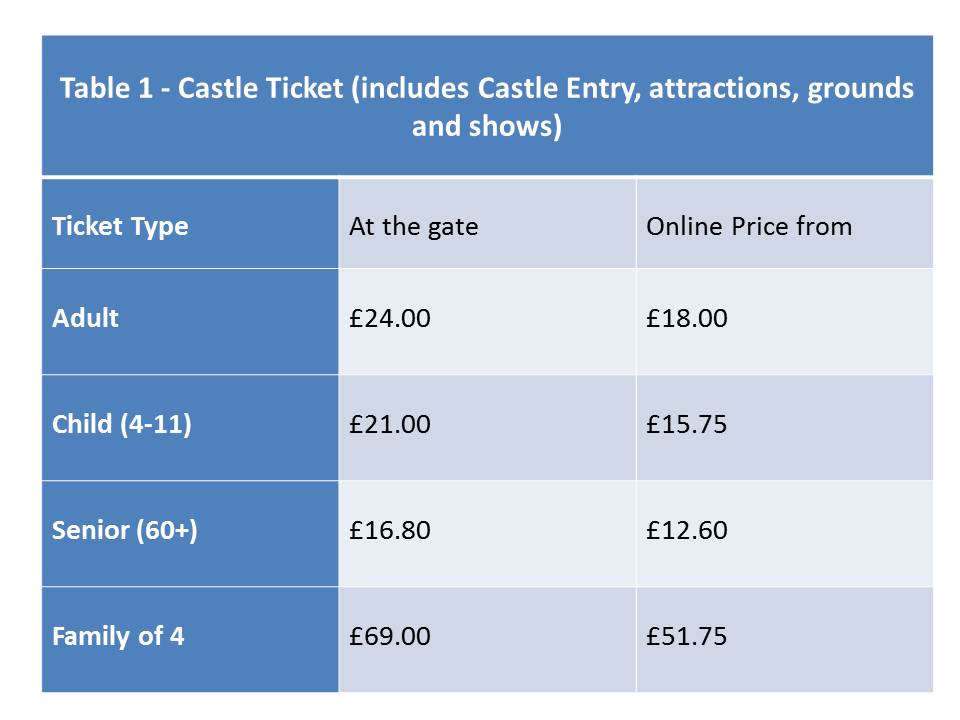

Is it possible for a firm to charge different prices to different customers for the same or a similar good or service? Table 1 below shows the entry fees for Warwick Castle, another tourist attraction owned by Merlin Entertainments PLC.

It can immediately be seen from this table that some groups of customers pay a different entry fee from others. For example adults have to pay £24 to enter on the day while people aged 60 and over pay a lower price £16.80. The entry fee for children aged between 4 and 11 is £21.00 while those aged 3 and under go for free. Students aged 16-18 can gain entry for a price of £13.50 if they can provide valid ID and purchase the tickets from the visitbritainshop website.

In this example, the company has allocated people into different categories by age (i.e. senior, adult, student, older children and younger children) and has set the entry fee that customers in each group have to pay.

The table also shows that if customers purchase on- line then they can get the tickets more cheaply. The entry fee for each category is 25% lower if the ticket is booked seven days in advance i.e. the prices shown in the last column in the table. If the booking is made between 2-6 days in advance then the discount is only 10% i.e. an adult ticket would cost £21.60. The on-line discounts are open to everyone. People are given the choice to either book on-line in advance or pay on the day. This is different from a situation where you are placed into a category by the firm. For example the customer cannot choose whether they are over 60!

If people are prepared to spend more time searching on the internet then other cheaper prices can also be obtained. Once again these offers are open to anyone willing to spend the time and effort in order to find them.

All the ticket prices above give people access to exactly the same attractions on the day. They do not give the visitor access to two of the attractions at the castle – the Dragon Tower and Castle Dungeon. Entry to the Dragon Tower would cost an adult on the day an extra £1.80 while entry to the Castle Dungeon would cost an extra £5.40.

Warwick Castle Ticket Prices Warwick Castle (accessed on 04/09/14)

Alton Towers Alton Towers (accessed on 08/09/14)

Warwick Castle Tickets visitbritainshop (accessed on 02/09/14)

Global Attractions Attendance Report teaconnect (accessed on 05/09/14)

Merlin Entertainments Merlin Entertainments (accessed on 08/09/14)

Questions

- What pricing decisions do firms have to make if they operate in a perfectly competitive market?

- Explain why an individual tourist attraction will have a downward sloping demand curve

- Paying an entry fee and an extra payment per attraction is known as what type of pricing? What advantages does this type of price strategy have for the seller?

- How would you calculate the profit per customer? What factors other than the entrance fee would determine the profit made per customer in a theme park or tourist attractions?

- Paying a different price depending on which category you have been assigned to by the seller is known as what type of pricing strategy? Can this type of pricing strategy ever be in the interests of society?

- In the example used in the case, customers are assigned to different categories by age. Can you think of any other ways that firms could categorise their customers?

- Given the category customers have been assigned to they can pay different prices depending on whether they buy the tickets on line. What is the price strategy called when customers can choose from a variety of pricing options for the same or similar product? Can you think of any different methods that could be used by the seller to carry out this type of pricing strategy?

Officials from Rugby Union’s Aviva Premiership recently announced that the salary cap used by the league would increase from £4.76 million to £5.1 million per team for the 2015-16 season. It is not the only professional sports league to use this type of regulation. The NFL currently has a salary cap of $133 million/team while in the NBA it is set at $63 million/team. What is the rationale for placing restrictions on the amount an organisation can pay its employees? How do these caps work in practice?

Officials from Rugby Union’s Aviva Premiership recently announced that the salary cap used by the league would increase from £4.76 million to £5.1 million per team for the 2015-16 season. It is not the only professional sports league to use this type of regulation. The NFL currently has a salary cap of $133 million/team while in the NBA it is set at $63 million/team. What is the rationale for placing restrictions on the amount an organisation can pay its employees? How do these caps work in practice?  The senior salary cap is the major part of the regulation and the Aviva Premiership announced that this would increase from £4.76 million per team in the current season to £5.1 million per team for 2015-16. The Academy credits enable teams to exceed this £5.1 million limit if they train and develop younger players. The teams have to prove that they have young players that meet the following criteria:

The senior salary cap is the major part of the regulation and the Aviva Premiership announced that this would increase from £4.76 million per team in the current season to £5.1 million per team for 2015-16. The Academy credits enable teams to exceed this £5.1 million limit if they train and develop younger players. The teams have to prove that they have young players that meet the following criteria: