Microsoft’s Office suite is the market leader in the multi-billion dollar office software market. Although an oligopoly, thanks to strong network economies Microsoft has a virtual monopoly in many parts of the market. Network economies occur when it saves money and/or time for people to use the same product (software, in this case), especially within an organisation, such as a company or a government.

Microsoft’s Office suite is the market leader in the multi-billion dollar office software market. Although an oligopoly, thanks to strong network economies Microsoft has a virtual monopoly in many parts of the market. Network economies occur when it saves money and/or time for people to use the same product (software, in this case), especially within an organisation, such as a company or a government.

Despite the rise of open-source software, such as Apache’s OpenOffice and Google Docs, Microsoft’s Office products, such as Word, Excel and PowerPoint, still dominate the market. But are things about to change?

The UK government has announced that it will seek to abandon reliance on Microsoft Office in the public sector. Provided there are common standards within and across departments, it will encourage departments to use a range of software products, using free or low-cost alternatives to Microsoft products where possible. This should save hundreds of millions of pounds.

Will other governments around the world and other organisations follow suit? There is a lot of money to be saved on software costs. But will switching to alternatives impose costs of its own and will these outweigh the costs saved?

UK government to abandon Microsoft “oligopoly” for open source software Digital Spy, Mayer Nissim (29/1/14)

No, the government isn’t dumping Office, but it does want to start seeing other people ZDNet, Nick Heath (29/1/14)

UK government once again threatens to ditch Microsoft Office The Verge, Tom Warren (29/1/14)

UK government to abandon Microsoft Office in favour of open-source software PCR, Matthew Jarvis (29/1/14)

UK government plans switch from Microsoft Office to open source The Guardian (29/1/14)

Open source push ‘could save taxpayer millions’ The Telegraph, Matthew Sparkes (30/1/14)

Will Google Docs kill off Microsoft Office? CNN Money, Adrian Covert (13/11/13)

Questions

- Why has Microsoft retained a virtual monopoly of the office software market? How relevant are network economies to the decision of organisations and individuals not to switch?

- Identify other examples of network economies and how they impact on competition.

- How do competitors to Microsoft attempt to overcome the resistance of people to switching to their office software?

- What methods does Microsoft use to try to retain its position of market dominance?

- How does Apple compete with Microsoft in the office software market?

- What factors are likely to determine the success of Google Docs in capturing significant market share from Microsoft Office?

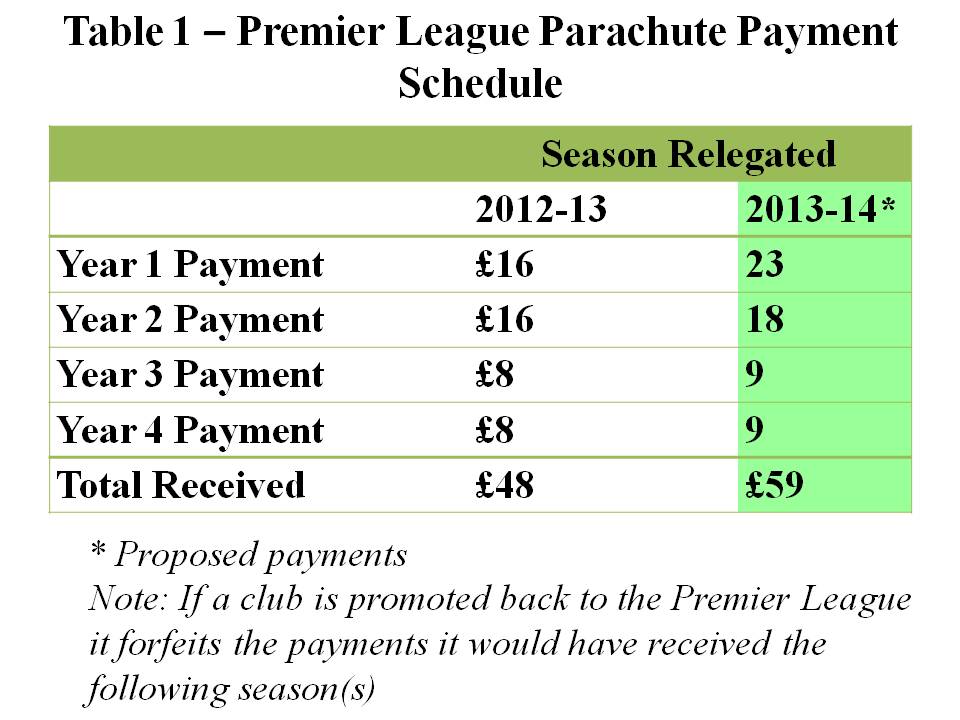

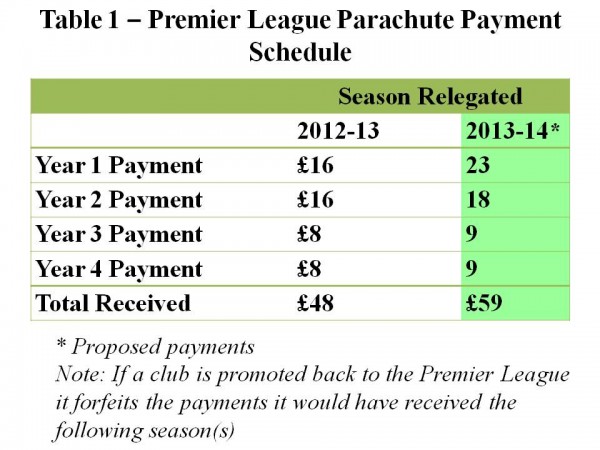

The English Premier League (EPL) has negotiated a record TV deal which will generate £5.5 billion of revenue over the next 3 years – beginning in the season 2013–14. This represents a 70% increase on the previous deal. Controversy has arisen over some initial proposals put forward by the EPL as to how the money will be spent. The owners of the clubs in the Championship of the English Football League (EFL) are particularly concerned about the size of the proposed payments to the three teams relegated from the EPL.

The English Premier League (EPL) has negotiated a record TV deal which will generate £5.5 billion of revenue over the next 3 years – beginning in the season 2013–14. This represents a 70% increase on the previous deal. Controversy has arisen over some initial proposals put forward by the EPL as to how the money will be spent. The owners of the clubs in the Championship of the English Football League (EFL) are particularly concerned about the size of the proposed payments to the three teams relegated from the EPL.

Some 30 years ago the money generated from the sale of television rights was equally shared between all the teams in the then four divisions of the English Football League (EFL). In 1992 the top division of the English Football League broke away and formed the English Premier League (EPL). This newly formed EPL negotiated a separate television deal and kept the majority of the money. However, some payments were and still are made to the teams in the EFL and to organisations such as the League Managers Association and Professional Footballers Association. For example in 2011-–12 the EPL donated £189.4 million of the £1.2 billion generated from that year’s TV deal.

The majority of the money donated by the EPL is spent in two main ways. First, some money is redistributed to all the teams in the EFL: i.e. The Championship, League 1 and League 2. These are known as ‘solidarity payments’ and in 2011–12 the EPL spent £49.8 million on this scheme. Each club in the Championship received £2.3 million. It has been proposed that the amount paid into this scheme should be increased by 5% in the season 2013–14. Second, a relatively large amount of money is paid over a four-year period to the three teams relegated each season from the EPL into the Championship. These are known as ‘parachute payments’ and in the season 2011–12 the EPL spent £90.9 million on this scheme. The rationale for having parachute payments is to help the relegated teams adjust their wage bills to the much lower revenue streams that come from playing in the Championship. Proposed changes to the scheme are outlined in Table 1.

The chairmen of the football league clubs met on the 20th March 2013 and a number of them expressed concerns about the relatively large increase in the parachute payments compared to the solidarity payments. They were particularly concerned that the changes to the funding would damage the competitive balance of the Championship.

The chairmen of the football league clubs met on the 20th March 2013 and a number of them expressed concerns about the relatively large increase in the parachute payments compared to the solidarity payments. They were particularly concerned that the changes to the funding would damage the competitive balance of the Championship.

Competitive balance refers to how the most talented players are distributed amongst the teams in a league. For example, are the majority of the most talented footballers playing for just a couple of the teams? In this case the league is competitively imbalanced and the teams with the best players will tend to win far more games than the other teams. The outcome of the league will be very predictable. If the most talented players were more evenly spread across all the teams in the league, then it would be more competitively balanced. Matches and the outcome of the league would become more unpredictable.

Does the level of competitive balance matter? Some sports economists have argued that it may have a significant impact on the success of the league. This is because fans may value the unpredictability of the results. It follows that closer and more unpredictable results will generate higher match-day attendances and increase the revenues of the clubs.

This is an interesting argument and is the opposite of what economic theory would predict for most markets. For example, the standard prediction would be that as firms outperform their rivals, they generate more revenue and profit. If they manage to drive all their rivals out of business, they would become a pure monopoly and make large abnormal profits. However in professional team sports the outcome may differ significantly. If the unpredictability of the league is highly valued by fans, then teams will generate more revenue when they have strong and evenly matched rivals.

It has been reported that further discussions about the distribution of the money will take place this month with the owners of the championship clubs arguing that there should be smaller increases in parachute payments and much larger increases in solidarity payments. Representatives of the EPL have argued that the parachute payments do not distort competition and make the championship predictable. They point out that at present only one of the top six teams in the championship (Hull) receives parachute payments, while only one of the teams promoted from the Championship in the season 2012–13 (West Ham) received these payments.

Articles

Premier League warned over rich and poor split in wake of TV deal The Guardian, Owen Gibson (19/3/13)

Championship clubs angered by Premier League parachute boost Daily Mail, Charles Sale (6/2/13)

Football league is to lessen the advantage of parachute payments The Guardian, Owen Gibson (20/3/13)

Championship clubs warn Premier League over hike in parachute payments for relegated teams The Independent, Majid Mohamed (20/3/13)

Increased parachute payments could lead to a salary cap in the Championship The Post, A. Stockhausen (21/3/13)

Scudamore:Parachute payment system fair Eurosport, Andy Eckardt (22/3/13)

Parachute payments more than a softened landing The Daisy Cutter, Richard Brook (21/3/13)

Questions

- What factors will influence the size of the attendance at a football match?

- To what extent do you think that the money generated from the sale of television rights should be equally shared between all the clubs in the English Premier League and the English Football League

- Can you think of any ways of measuring the competitive balance of a football league?

- Explain why a very competitively imbalanced league may reduce the revenue for all the clubs in that league?.

- In traditional economic theory it is assumed that firms aim to maximise their profits. What do you think is the objective of a typical football club in the English Premier League?

Cartels are formal collusive agreements between firms, typically to fix prices, restrict output or divide up markets. As in the case of monopoly, the lack of competition may harm consumers, who are likely to have to pay higher prices. This, as economic theory demonstrates, results in a reduction in overall welfare.

Cartels are formal collusive agreements between firms, typically to fix prices, restrict output or divide up markets. As in the case of monopoly, the lack of competition may harm consumers, who are likely to have to pay higher prices. This, as economic theory demonstrates, results in a reduction in overall welfare.

For this reason competition authorities throughout the world now impose substantial fines on firms found to be involved in collusive activities and participants also face the threat of substantial jail sentences.

One of the most famous cartels is the Organization of Petroleum Exporting Countries (OPEC). This is an agreement between 12 countries to limit their production of oil. The OPEC cartel has been in place for over 50 years. Arguably, the intergovernmental nature of the cartel and political ramifications of intervening have meant that OPEC has been able to operate free from prosecution for so long.

However, very interestingly Freedom Watch, a US public interest group founded by a former US Department of Justice lawyer, has this week filed a lawsuit against OPEC for violation of competition laws. Quoted in the above press release, Larry Klayman, the founder of Freedom Watch, says that:

These artificially-inflated crude oil prices fall hard on the backs of Americans, many of whom cannot afford to buy gasoline during these severely depressed economic times.

Furthermore, how some of the members use the profits gained from the cartel is also called into question. He also goes on to suggest that the lack of intervention from US government agencies may be because the leaders of both political parties:

… line their pockets from big oil interests and are just sitting back and not doing anything.

This is not the first time that Freedom Watch has served a lawsuit on OPEC. In 2008, at an OPEC meeting in Florida:

In a bold move in front of members of the news media, Freedom Watch Chairman and Chief Legal Counsel Larry Klayman literally jumped out from behind a line of TV cameras and microphones on Friday, October 24, to serve a complaint on an OPEC oil minister.

That complaint was unsuccessful.

It will be fascinating to see the outcome of this latest case and, if successful, the implications for OPEC – updates to appear on this blog in due course.

Articles

Profile: Opec, club of oil producing states BBC News (01/02/12)

OPEC accused of conspiracy against consumers WND World, Bob Unruh (09/05/12)

Freedom Watch Attorney Sues OPEC Oil Minister for Economic Terrorism Conservative Crusader, Jim Kouri (31/10/08)

Lawsuits

Lawsuit brought by Freedom Watch inc. against OPEC (7/5/12)

Lawsuit brought by Freedom Watch inc. against OPEC (9/6/08)

Questions

- Why are cartels so severely punished?

- Why might it be important to punish the individuals involved as well as fine the cartel members?

- Why is fixing the price of oil particularly harmful for the economy?

- Why do you think the OPEC cartel has survived for so long?

- What do you think might be the long term implications of the lawsuit for OPEC?

Last year, we felt the cost of the cold weather and whilst we haven’t seen such low temperatures this year, gas shortages are also emerging. Across Eastern Europe, temperatures have fallen well below -30ºC and so demand for gas has unsurprisingly increased.

Last year, we felt the cost of the cold weather and whilst we haven’t seen such low temperatures this year, gas shortages are also emerging. Across Eastern Europe, temperatures have fallen well below -30ºC and so demand for gas has unsurprisingly increased.

Thanks to these low temperatures, Russian gas supplies are running low and several countries have seen their deliveries of gas fall. However, the Russian gas monopoly, Gazprom has said that supplies have not been cut and that it has been exporting more gas during these cold times. The blame, according to Alexander Medvedev (the Deputy CEO of Gazprom), lies with the Ukraine taking gas at a pace significantly above contracted levels. The following articles consider this issue.

Russia, Ukraine argue over gas as EU reports shortage Reuters (2/2/12)

Freezing Europe hit by Russian gas shortage BBC News (4/2/12)

Gazprom says ‘Perplexed’ by EU supply drop as Ukraine takes gas Bloomberg BusinessWeek, Anna Shiryaevskaya (3/2/12)

Gazprom cuts gas supplies amid cold snap Financial Times, Guy Chazan (3/2/12)

Gazprom ‘unable to pump extra gas to Europe’ Associated Press (4/2/12)

Questions

- Using a demand and supply diagram, illustrate what we would expect to see with a gas shortage.

- What has been the cause of this current gas shortage? Use a diagram to illustrate the causes.

- What would you expect to happen to prices following this gas shortage?

- Gazprom is said to be a monopoly: what are the characteristics of a monopoly?

- As there are other gas suppliers, how can Gazprom be said to be a monopolist?

In many parts of the UK, bus services are run by a single operator. In other parts, it is little different, with the main operator facing competition on only a very limited number of routes. Over the whole of England, Scotland and Wales there are 1245 bus operators, but the ‘big five’ (Arriva, FirstGroup, Go-Ahead, National Express and Stagecoach) carry some 70% of passengers. Generally these five companies do not compete with each other, but, instead, operate as monopolies, or near monopolies, in their own specific areas. On average, the largest operator in an urban area runs 69% of local bus services.

Given this lack of competition and potential abuse of monopoly power, the Office of Fair Trading referred local bus services in Great Briatin (excluding London) to the Competition Commission (CC) in January 2010. The CC has just published its final report. Paragraph 5 of the summary to the report states:

We concluded that there were four features of local bus markets which mean that effective head-to-head competition is uncommon and which limit the effectiveness of potential competition and new entry. These features are the existence of: high levels of concentration; barriers to entry and expansion; customer conduct in deciding which bus to catch; and operator conduct by which operators avoid competing with other operators in ‘Core Territories’ (certain parts of an operator’s network which it regards as its ‘own’ territory) leading to geographic market segregation.

And paragraph 8 states:

We decided on a package of remedies with three main elements to address the AECs [adverse effects on competition] that we found. First, the remedies include market-opening measures to reduce barriers to entry and expansion, thereby reducing market concentration and providing an environment in which competition is likely to be sustained. By reducing barriers to entry and expansion, we also expect it to become harder for operators to sustain a coordinated outcome. Second, the remedies include measures to promote competition in relation to the tendering of contracts for supported services. Third, we made recommendations about the wider policy and regulatory environment, including emphasizing compliance with and effective enforcement of competition law.

The following articles look at the findings of the report and at the potential for improving the service to passengers, in terms of quality, frequency and price.

Articles

Competition regulator outlines bus market shake-up The Telegraph (20/12/11)

Bus market not competitive, Competition Commission says BBC News (20/12/11)

Passengers ‘need more bus rivalry’ Press Association (20/12/11)

Competition Commission publications

CC sets out Future Destination for Bus Market Competition Commission News Release (20/12/11)

Bus Market Inquiry: Final Report, Case Studies and Appendices Competition Commission (20/12/11)

Local Bus Services: Accompanying Documents Competition Commission (20/12/11)

Questions

- What are the barriers to entry in the market for local bus services?

- In what circumstances are local bus services a natural monopoly? Is this generally the case?

- In a non-regulated bus market, how could established operators use predatory pricing to drive out new entrants?

- How may offering reductions for return tickets reduce competition on routes where there is a large operator and one or more smaller ones?

- What practices can established large operators use to drive out smaller competitors?

- Go through the four reasons given by the CC why head-to-head competition in local bus markets is uncommon and in each case consider what remedies could be adopted by the regulator or by local authorities.

- Which of the remedies proposed by the CC involve encouraging more competition and which involve tighter regulation?