The growth of emerging economies, such as China, India and Brazil brings with it both good and bad news for the once dominant countries of the West. With growth rates in China reaching double digits and a much greater resilience to the credit crunch and its aftermath in these emerging nations, they became the hope of the recovery for the West. But, is it only benefits that emerge from the growth in countries like China?

The growth of emerging economies, such as China, India and Brazil brings with it both good and bad news for the once dominant countries of the West. With growth rates in China reaching double digits and a much greater resilience to the credit crunch and its aftermath in these emerging nations, they became the hope of the recovery for the West. But, is it only benefits that emerge from the growth in countries like China?

Chinese business has grown and expanded into all areas, especially technology, but countries such as the USA have been reluctant to allow mergers and takeovers of some of their businesses. Notably, the takeovers that have been resisted have been in key sectors, particularly oil, energy and technology. However, it seems as though pork is an industry that is less important or, at least, a lower risk to national security.

Smithfield Foods is a US giant, specialising in the production and selling of pork. A takeover by China’s Shuanghui International Holdings has been approved (albeit reluctantly) by the US Committee on Foreign Investment. While the takeover could still run into obstacles, this Committee’s approval is crucial, as it alleviates concerns over the impact on national security. The value of the deal is some $7.1bn, including the debt that Shuangui will have to take on. While some see this takeover as good news, others are more concerned, identifying the potential negative impact it may have on prices and standards in the USA. Zhijun Yang, Shuanghui’s Chief Executive said:

Smithfield Foods is a US giant, specialising in the production and selling of pork. A takeover by China’s Shuanghui International Holdings has been approved (albeit reluctantly) by the US Committee on Foreign Investment. While the takeover could still run into obstacles, this Committee’s approval is crucial, as it alleviates concerns over the impact on national security. The value of the deal is some $7.1bn, including the debt that Shuangui will have to take on. While some see this takeover as good news, others are more concerned, identifying the potential negative impact it may have on prices and standards in the USA. Zhijun Yang, Shuanghui’s Chief Executive said:

This transaction will create a leading global animal protein enterprise. Shuanghui International and Smithfield have a long and consistent track record of providing customers around the world with high-quality food, and we look forward to moving ahead together as one company.

The date of September 24th looks to be the decider, when a shareholder meeting is scheduled to take place. There is still resistance to the deal, but if it goes ahead it will certainly help other Chinese companies looking for the ‘OK’ from US regulators for their own business deals. The following articles consider the controversy and impact of this takeover.

US clears Smithfield’s acquisition by China’s Shuanghui Penn Energy, Reuters, Lisa Baertlein and Aditi Shrivastava (10/9/13)

Chinese takeover of US Smithfield Foods gets US security approval Telegraph (7/9/13)

US clears Smithfield acquisition by China’s Shuanghui Reuters (7/9/13)

Go-ahead for Shuanghui’s $4.7bn Smithfield deal Financial Times, Gina Chon (6/9/13)

US security panel approves Smithfield takeover Wall Street Journal, William Mauldin (6/9/13)

Questions

- What type of takeover would you classify this as? Explain your answer.

- Why have other takeovers in oil, energy and technology not met with approval?

- Some people have raised concerns about the impact of the takeover on US pork prices. Using a demand and supply diagram, illustrate the possible effects of this takeover.

- What do you think will happen to the price of pork in the US based on you answer to question 3?

- Why do Smithfield’s shareholders have to meet before the deal can go ahead?

- Is there likely to be an impact on share prices if the deal does go ahead?

On 5 and 6 April, there was a conference on conscious capitalism in San Francisco. In January, a new book, Conscious Capitalism: Liberating the Heroic Spirit of Business, by John Mackey and Rajendra Sisodia, was published. Many in the business world are enthusiastic about this seemingly new approach to business, which focuses on broader social, environmental and ethical goals, rather than simple profit maximisation.

On 5 and 6 April, there was a conference on conscious capitalism in San Francisco. In January, a new book, Conscious Capitalism: Liberating the Heroic Spirit of Business, by John Mackey and Rajendra Sisodia, was published. Many in the business world are enthusiastic about this seemingly new approach to business, which focuses on broader social, environmental and ethical goals, rather than simple profit maximisation.

As the Washington Times review linked to below states:

“Conscious Capitalism” promotes a business culture that embodies “trust, accountability, caring, transparency, integrity, loyalty and egalitarianism.” The management ideal of “Conscious Capitalism” contains four key elements of “decentralization, empowerment, innovation and collaboration.” Above all, this exemplary form of business practice relies on careful attention to four tenets: higher purpose and core values, stakeholder integration, conscious leadership and conscious culture and management.

So how realistic is this vision of caring capitalism? There may be a few inspiring businesspeople, truly committed to improving the interests of the various stakeholders of their business and society more generally, but could it become a model for business in general? And if so, does this require education, monitoring and regulation? Or can a libertarian approach to business generate an environment where conscious and caring capitalists flourish and succeed better than those with a more narrow focus on profit?

So how realistic is this vision of caring capitalism? There may be a few inspiring businesspeople, truly committed to improving the interests of the various stakeholders of their business and society more generally, but could it become a model for business in general? And if so, does this require education, monitoring and regulation? Or can a libertarian approach to business generate an environment where conscious and caring capitalists flourish and succeed better than those with a more narrow focus on profit?

The following videos and articles discuss conscious capitalism and the arguments of those, such as John Mackey, founder and co-CEO of Whole Food Market, who advocate it.

Webcasts

Conscious capitalism The Economist, John Mackey (15/3/13)

Conscious capitalism The Economist, John Mackey (15/3/13)

Conscious Capitalism: Heroes of the Business World Conscious capitalism, April in San Francisco (5/4/13)

It’s Not Corporate Social Responsibility Conscious capitalism, John Mackey (Jan 13)

Articles, reviews and information

Conscious Capitalism: Creating a New Paradigm for Business Whole Planet Foundation, John Mackey

Companies that Practice “Conscious Capitalism” Perform 10x Better Harvard Business Review, Tony Schwartz (4/4/13)

4 Ways to Become a (More) Conscious Capitalist Inc., Francesca Louise Fenzi (8/4/13)

The New Management Paradigm & John Mackey’s Whole Foods Forbes, Steve Denning (5/1/13)

Book Review: ‘Conscious Capitalism’ Washington Times, Anthony j. Sadar (20/3/13)

Book Review: Whole Foods Co-CEO John Mackey’s Conscious Capitalism Huffington Post, Christine Bader (28/1/13)

Chicken Soup for a Davos Soul Wall Street Journal, Alan Murray (16/1/13)

Conscious business Wikipedia

Questions

- What are the features of conscious capitalism?

- Do firms “get the shareholders they deserve”?

- How might firms that are not pursuing conscious capitalism be persuaded to become more conscious and more caring?

- How does conscious capitalism differ from corporate social responsibility?

- What would you understand by “conscious consumers”? How might their behaviour differ from other consumers?

- Why might firms engaging in conscious capitalism become more profitable than firms that have a simple aim of profit maximisation?

- What reforms, both internal within a firm and in the legal environment, does John Mackey advocate? Do you agree with his suggestions? What else do you suggest?

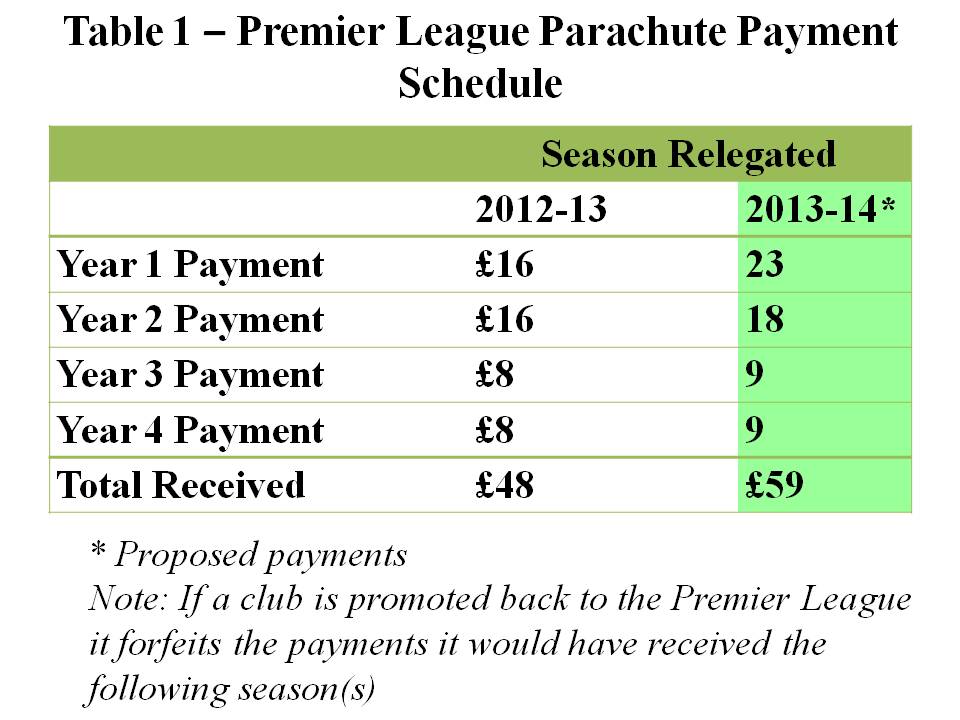

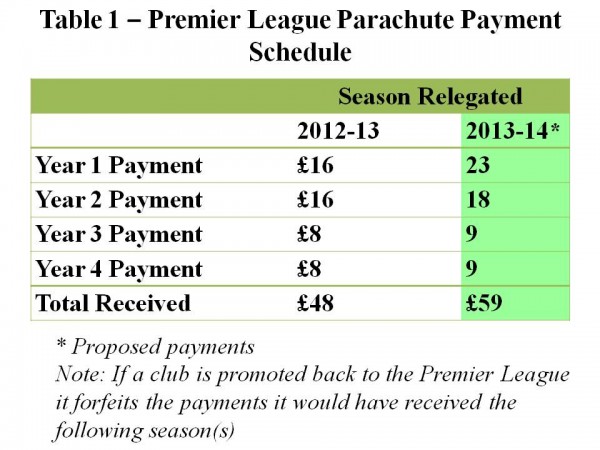

The English Premier League (EPL) has negotiated a record TV deal which will generate £5.5 billion of revenue over the next 3 years – beginning in the season 2013–14. This represents a 70% increase on the previous deal. Controversy has arisen over some initial proposals put forward by the EPL as to how the money will be spent. The owners of the clubs in the Championship of the English Football League (EFL) are particularly concerned about the size of the proposed payments to the three teams relegated from the EPL.

The English Premier League (EPL) has negotiated a record TV deal which will generate £5.5 billion of revenue over the next 3 years – beginning in the season 2013–14. This represents a 70% increase on the previous deal. Controversy has arisen over some initial proposals put forward by the EPL as to how the money will be spent. The owners of the clubs in the Championship of the English Football League (EFL) are particularly concerned about the size of the proposed payments to the three teams relegated from the EPL.

Some 30 years ago the money generated from the sale of television rights was equally shared between all the teams in the then four divisions of the English Football League (EFL). In 1992 the top division of the English Football League broke away and formed the English Premier League (EPL). This newly formed EPL negotiated a separate television deal and kept the majority of the money. However, some payments were and still are made to the teams in the EFL and to organisations such as the League Managers Association and Professional Footballers Association. For example in 2011-–12 the EPL donated £189.4 million of the £1.2 billion generated from that year’s TV deal.

The majority of the money donated by the EPL is spent in two main ways. First, some money is redistributed to all the teams in the EFL: i.e. The Championship, League 1 and League 2. These are known as ‘solidarity payments’ and in 2011–12 the EPL spent £49.8 million on this scheme. Each club in the Championship received £2.3 million. It has been proposed that the amount paid into this scheme should be increased by 5% in the season 2013–14. Second, a relatively large amount of money is paid over a four-year period to the three teams relegated each season from the EPL into the Championship. These are known as ‘parachute payments’ and in the season 2011–12 the EPL spent £90.9 million on this scheme. The rationale for having parachute payments is to help the relegated teams adjust their wage bills to the much lower revenue streams that come from playing in the Championship. Proposed changes to the scheme are outlined in Table 1.

The chairmen of the football league clubs met on the 20th March 2013 and a number of them expressed concerns about the relatively large increase in the parachute payments compared to the solidarity payments. They were particularly concerned that the changes to the funding would damage the competitive balance of the Championship.

The chairmen of the football league clubs met on the 20th March 2013 and a number of them expressed concerns about the relatively large increase in the parachute payments compared to the solidarity payments. They were particularly concerned that the changes to the funding would damage the competitive balance of the Championship.

Competitive balance refers to how the most talented players are distributed amongst the teams in a league. For example, are the majority of the most talented footballers playing for just a couple of the teams? In this case the league is competitively imbalanced and the teams with the best players will tend to win far more games than the other teams. The outcome of the league will be very predictable. If the most talented players were more evenly spread across all the teams in the league, then it would be more competitively balanced. Matches and the outcome of the league would become more unpredictable.

Does the level of competitive balance matter? Some sports economists have argued that it may have a significant impact on the success of the league. This is because fans may value the unpredictability of the results. It follows that closer and more unpredictable results will generate higher match-day attendances and increase the revenues of the clubs.

This is an interesting argument and is the opposite of what economic theory would predict for most markets. For example, the standard prediction would be that as firms outperform their rivals, they generate more revenue and profit. If they manage to drive all their rivals out of business, they would become a pure monopoly and make large abnormal profits. However in professional team sports the outcome may differ significantly. If the unpredictability of the league is highly valued by fans, then teams will generate more revenue when they have strong and evenly matched rivals.

It has been reported that further discussions about the distribution of the money will take place this month with the owners of the championship clubs arguing that there should be smaller increases in parachute payments and much larger increases in solidarity payments. Representatives of the EPL have argued that the parachute payments do not distort competition and make the championship predictable. They point out that at present only one of the top six teams in the championship (Hull) receives parachute payments, while only one of the teams promoted from the Championship in the season 2012–13 (West Ham) received these payments.

Articles

Premier League warned over rich and poor split in wake of TV deal The Guardian, Owen Gibson (19/3/13)

Championship clubs angered by Premier League parachute boost Daily Mail, Charles Sale (6/2/13)

Football league is to lessen the advantage of parachute payments The Guardian, Owen Gibson (20/3/13)

Championship clubs warn Premier League over hike in parachute payments for relegated teams The Independent, Majid Mohamed (20/3/13)

Increased parachute payments could lead to a salary cap in the Championship The Post, A. Stockhausen (21/3/13)

Scudamore:Parachute payment system fair Eurosport, Andy Eckardt (22/3/13)

Parachute payments more than a softened landing The Daisy Cutter, Richard Brook (21/3/13)

Questions

- What factors will influence the size of the attendance at a football match?

- To what extent do you think that the money generated from the sale of television rights should be equally shared between all the clubs in the English Premier League and the English Football League

- Can you think of any ways of measuring the competitive balance of a football league?

- Explain why a very competitively imbalanced league may reduce the revenue for all the clubs in that league?.

- In traditional economic theory it is assumed that firms aim to maximise their profits. What do you think is the objective of a typical football club in the English Premier League?

Few people have £18bn worth of funds to spend. But someone that does is Warren Buffett and a Brazilian firm, who look set to purchase Heinz for this sum. Heinz, known for things like baked beans and ketchup already has an exceptionally strong brand and is cash rich – these are two ingredients which Warren Buffett likes and have undoubtedly played their part in securing what looks to be a tasty deal.

Few people have £18bn worth of funds to spend. But someone that does is Warren Buffett and a Brazilian firm, who look set to purchase Heinz for this sum. Heinz, known for things like baked beans and ketchup already has an exceptionally strong brand and is cash rich – these are two ingredients which Warren Buffett likes and have undoubtedly played their part in securing what looks to be a tasty deal.

The company’s Board has already approved the deal, but shareholders still need to have their say and have been offered $72.50 per share. 650 million bottles of Heinz ketchup are sold every year and its baked beans, at the least in the UK, are second to none. Products like this have given Heinz its global brand name and have provided the opportunity to shareholders to make significant gains. Its Chairman said:

The Heinz brand is one of the most respected brands in the global food industry and this historic transaction provides tremendous value to Heinz shareolders.

This statement was certainly reciprocated by Warren Buffett when he spoke to CNBC, saying:

It is our kind of company … I’ve sampled it many times … Anytime we see a deal is attractive and it’s our kind of business and we’ve got the money, I’m ready to do.

The deal therefore looks to be profitable to both sides, but is there more to it? An investigation has already been launched by the Securities and Exchange Commission as to whether information about this purchase was leaked early and was used to make money. Insider trading occurs when someone is given information early about a merger such as the one described above. They then use this information, before it is made public, to buy up a company’s stock. It is incredibly difficult to prosecute and huge amounts of money can be made by hedge funds, amongst others. This is certainly one aspect of the deal to keep your eye on.

The deal therefore looks to be profitable to both sides, but is there more to it? An investigation has already been launched by the Securities and Exchange Commission as to whether information about this purchase was leaked early and was used to make money. Insider trading occurs when someone is given information early about a merger such as the one described above. They then use this information, before it is made public, to buy up a company’s stock. It is incredibly difficult to prosecute and huge amounts of money can be made by hedge funds, amongst others. This is certainly one aspect of the deal to keep your eye on.

So, what does the future hold for Warren Buffett and Heinz? Buffett likes to extract extra value from companies he purchases and has in the past split up his businesses to create separate trading companies. However, given his taste for ketchup and his appreciation for strong global brands, it’s unlikely that we’ll see a change to the recipe of any of the well-known products. The following articles consider the takeover and the case of insider trading.

Will Buffet ‘squeeze value’ from Heinz BBC News (15/2/13)

Heinz-Buffett deal: will anyone spill the beans on insider trading? The Guardian, Heidi Moore (15/2/13)

Heinz bought by Warren Buffett’s Berkshire Hathaway for $28bn BBC News (14/2/13)

Traders sued over Heinz share bets Independent, Nikhil Kumar (16/2/13)

Heinz deal brings it back to its roots Financial Times, Alan Rappeport, Dan McCrum and Anoushka Sakoui (14/2/13)

Beanz means Buffet: Heinz purchased in $28bn takeover The Guardian, Dominic Rush (14/2/13)

US SEC sues over Heinz option trading before buyout Reuters (15/2/13)

Warren Buffet and Brazil’s ‘Sage’ Jorge Leman strike £18bn Heinz deal The Telegraph, Richard Blackden (15/2/13)

Questions

- What type of take-over would you class this as?

- Consider the Boston matrix – in which category would you place Heinz when you think about its market share and market growth?

- Why is a company that has a global brand and that is cash rich so tempting?

- Given your answer to question 3, why have other investors not taken an interest in purchasing Heinz?

- If you were a shareholder in Heinz, what factors would you consider when deciding whether or not to vote for the takeover?

- What growth strategy has Heinz used to establish its current position in the global market place?

- What is insider trading? Explain how early information can be used to make money in the case of Heinz.

- Explain how the share price of $72.50 is set. How does the market have a role?

Original post

Starbucks’ UK sales in 2011 were worth £398m. Costa’s UK sales were worth £377m. But while Costa paid £15m in corporation tax in 2011/12, Starbucks paid nothing! In fact since opening its first coffee shop in the UK in 1998 it has paid just £8.6m in taxes on UK sales of £3bn.

How is this possible? Let’s look at Starbuck’s 2011 UK sales. Even though these were worth £398 million, its costs were recorded as £426.2m, giving a loss of £28.2m. Costa, by contrast, reported a taxable profit of £49.7m.

So is Starbucks a commercial failure in the UK, recording year after year of losses? Not at all. Starbucks regards the UK as a highly profitable part of its business. As the Independent article below states:

…in its briefings to stock market investors and analysts during the past 12 years, Seattle-based Starbucks has consistently stated that its UK unit is “profitable” and three years ago even promoted its UK head, Cliff Burrows, to run its vastly larger US operation.

So how can reported UK losses be reconciled with a profitable UK operation? The answer lies in transfer pricing.

Transfer pricing refers to the prices a company charges itself when goods or services are transferred within the company but from one country to another. By varying the transfer prices, a company can choose where to make its profits. Thus if Starbucks’ US operation charges high prices to its UK operation for various services, such as royalties for the use of branding or for management services, or lends money to its UK operation at high interest rates, Starbucks’ profits will rise in the USA and fall in the UK.

Transfer pricing refers to the prices a company charges itself when goods or services are transferred within the company but from one country to another. By varying the transfer prices, a company can choose where to make its profits. Thus if Starbucks’ US operation charges high prices to its UK operation for various services, such as royalties for the use of branding or for management services, or lends money to its UK operation at high interest rates, Starbucks’ profits will rise in the USA and fall in the UK.

Companies employ tax advisers (see for example) and ‘transfer pricing managers’ to help them move their profits from high tax countries to low tax countries. In Starbuck’s case, by charging its UK operation high prices for such things as ‘use of its logo’ it has chosen to move all its profits out of the UK and thus avoid UK corporation tax.

Apart from denying the UK government tax revenues, the practice by Starbucks distorts competition as competing UK companies, such as Costa, AMT, Caffè Ritazza and the many small independents, do not have the same opportunity for transfer pricing and do pay UK corporation tax. As the Guardian article by Richard Murphy below states:

Apart from denying the UK government tax revenues, the practice by Starbucks distorts competition as competing UK companies, such as Costa, AMT, Caffè Ritazza and the many small independents, do not have the same opportunity for transfer pricing and do pay UK corporation tax. As the Guardian article by Richard Murphy below states:

We do have homegrown coffee shops in the UK. A lot of them. And they have to pay their taxes in full here in the UK. They can’t make payments to offshore entities for the use of their logos or advice on how to add hot water to coffee just to avoid tax: they have to pay in full on what they earn in this country. What Starbucks is doing may be legal, but what it also shows is that business does not operate on a level playing field in the UK.

And, as some of the articles below demonstrate, it’s not just Starbucks. Amazon, Facebook and Google have also been accused of avoiding taxes in the UK by engaging in forms of transfer pricing.

Update

On 12 November senior executives from Starbucks, Google and Amazon appeared before the House of Commons Public Accounts Committee to give evidence on their non-payment of corporation tax and their apparent lack of profits in the UK. As you will see from the videos, the MPs were unimpressed by the answers they received.

At the G20 finance ministers meeting in Mexico the previous week, George Osborne, the UK Chancellor, and Wolfgang Schäuble, the German Finance Minister, called for “concerted international co-operation to strengthen international tax standards that at the minute may mean international companies can pay less tax than they would otherwise owe”.

There seems to be mounting international pressure on multinationals to cease using transfer pricing as a means of avoiding paying taxes. Whether it will be successful remains to be seen.

Further Update (June 2013)

In June 2013, After continuing criticism of its tax avoidance policies, Starbucks agreed to pay £10m in corporation tax tin 2013/14 and a further £10m in 2014/15.

Articles for original post

Starbucks UK tax bill comes under scrutiny The Telegraph, Helia Ebrahimi (15/10/12)

Good bean counters? Starbucks has paid no tax in UK since 2009 Independent, Martin Hickman (16/10/12)

Special Report: How Starbucks avoids UK taxes Reuters, Tom Bergin (15/10/12)

Business Starbucks ‘paid no UK income tax’ since 2009 Channel 4 News (16/10/12)

Starbucks ‘paid just £8.6m UK tax in 14 years’ BBC News, Vicki Young (16/10/12)

Starbucks’ tax payment is ‘unfair’ say independent cafes BBC News, Joe Lynam (16/10/12)

Starbucks ‘paid just £8.6m UK tax in 14 years’ BBC News (16/10/12)

What the Starbucks tax expose means for ordinary companies Tax Research UK, Richard Murphy (16/10/12)

Starbucks ‘pays £8.6m tax on £3bn sales’ The Guardian, Simon Neville (15/10/12)

How much tax do Starbucks, Facebook and the biggest US companies pay in the UK The Guardian Datablog (16/10/12)

Amazon: £7bn sales, no UK corporation tax The Guardian, Ian Griffiths (4/4/12)

Facebook criticised for £238,000 UK tax bill last year BBC Radio 1 Newsbeat, Dan Cairns (11/10/12)

U.S. Companies Dodge $60 Billion in Taxes With Global Odyssey Bloomberg, Jesse Drucker (13/5/10)

EBay ‘pays £1.2m in UK tax’ on sales of £800m BBC News (21/10/12)

Articles for update

Starbucks, Google and Amazon grilled over tax avoidance BBC News (12/11/12)

Companies have ‘social responsibility’ to pay tax BBC Today Programme (12/11/12)

MPs slam Starbucks, Amazon and Google on tax Reuters, Tom Bergin (12/11/12)

A highly taxing session for the men from Amazon, Google and Starbucks The Guardian, Simon Hoggart (12/11/12)

Starbucks is leeching tax revenue from UK The Telegraph, Lord Myners (12/11/12)

UK and Germany agree crackdown on tax loopholes for multinationals The Guardian, Patrick Wintour and Dan Milmo (5/11/12)

Britain, Germany target tax from multinationals Deutsche Welle (5/11/12)

HMRC unable to stop multinational tax avoidance accountancylive, Sharon Khin (6/11/12)

Starbucks ‘planning changes to tax policy’ BBC News (3/12/12)

Articles for further update

Starbucks pays UK corporation tax for first time since 2009 BBC News (22/6/13)

Starbucks pays corporation tax, promising the Exchequer £20m over two years IndependentHeather Saul (2/6/13)

Starbucks pays first tax since 2008 The Telegraph, Kamal Ahmed (22/6/13)

Report of Public Accounts Committee

Tax avoidance by multinational companies UK Parliament (3/12/12)

Questions

- Explain how a multinational company can use transfer pricing as a means of reducing its overall tax liability.

- Why may transfer pricing lead to an inefficient allocation of resources?

- What policies can governments adopt to clamp down on the use of transfer pricing to limit their tax liability in their country?

- What insights are shed by game theory in explaining why it may be very difficult to reach international agreement to clamp down on tax avoidance?

- Is it immoral for companies to seek to minimise their tax liability? What are the limits of economics as a discipline in establishing an answer to this question?

The growth of emerging economies, such as China, India and Brazil brings with it both good and bad news for the once dominant countries of the West. With growth rates in China reaching double digits and a much greater resilience to the credit crunch and its aftermath in these emerging nations, they became the hope of the recovery for the West. But, is it only benefits that emerge from the growth in countries like China?

The growth of emerging economies, such as China, India and Brazil brings with it both good and bad news for the once dominant countries of the West. With growth rates in China reaching double digits and a much greater resilience to the credit crunch and its aftermath in these emerging nations, they became the hope of the recovery for the West. But, is it only benefits that emerge from the growth in countries like China? Smithfield Foods is a US giant, specialising in the production and selling of pork. A takeover by China’s Shuanghui International Holdings has been approved (albeit reluctantly) by the US Committee on Foreign Investment. While the takeover could still run into obstacles, this Committee’s approval is crucial, as it alleviates concerns over the impact on national security. The value of the deal is some $7.1bn, including the debt that Shuangui will have to take on. While some see this takeover as good news, others are more concerned, identifying the potential negative impact it may have on prices and standards in the USA. Zhijun Yang, Shuanghui’s Chief Executive said:

Smithfield Foods is a US giant, specialising in the production and selling of pork. A takeover by China’s Shuanghui International Holdings has been approved (albeit reluctantly) by the US Committee on Foreign Investment. While the takeover could still run into obstacles, this Committee’s approval is crucial, as it alleviates concerns over the impact on national security. The value of the deal is some $7.1bn, including the debt that Shuangui will have to take on. While some see this takeover as good news, others are more concerned, identifying the potential negative impact it may have on prices and standards in the USA. Zhijun Yang, Shuanghui’s Chief Executive said: