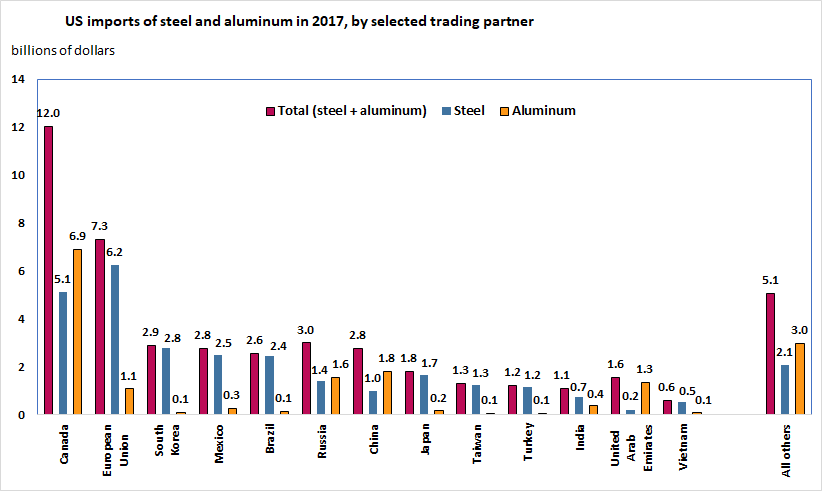

The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

Source: Bown (2018), Figure 1

A number of economists and policymakers are worried that such policies restrict trade and are likely to provoke retaliation by the affected trade partners. In recent statements, the EU has pledged to take counter-measures if the bloc is affected by these policies. In a recent press conference, the Commissioner for Trade, Cecilia Malmstrom, stated that:

We have made it clear that a move that hurts the EU and puts thousands of European jobs in jeopardy will be met with a firm and proportionate response.

She added that, ‘I truly hope that this will not happen. A trade war has no winners.’

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.

A number of studies have attempted to estimate the effect of trade restrictions and tariff wars on welfare: see for instance Anderson and Wincoop (2001), Syropoulos (2002), Fellbermayr et al. (2013). The results vary widely, depending on the case. However, there seems to be consensus that the more similar (in terms of size and industry composition) the adversaries are, the more mutually damaging a trade war is likely to be (and, therefore, less likely to happen).

As Miyagiwa et al (2016, p43) explain:

A country initiates contingent protection policy against a trading partner only if the latter has a considerably smaller domestic market than its own, while avoiding confrontation with a country having a substantially larger domestic market than its own.

As both Canada and the EU are very large advanced market economies, it remains to be seen how much risk (and potential damage to the local and global economy) US trade policymakers are willing to take.

Since running for election, Donald Trump has vowed to ‘put America first’. One of the economic policies he has advocated for achieving this objective is the imposition of tariffs on imports which, according to him, unfairly threaten American jobs. On March 8 2018, he signed orders to impose new tariffs on metal imports. These would be 25% on steel and 10% on aluminium.

His hope is that, by cutting back on imports of steel and aluminium, the tariffs could protect the domestic industries which are facing stiff competition from the EU, South Korea, Brazil, Japan and China. They are also facing competition from Canada and Mexico, but these would probably be exempt provided negotiations on the revision of NAFTA rules goes favourably for the USA.

Assuming there were no retaliation from other countries, jobs would be gained in the steel and aluminium industries. According to a report by The Trade Partnership (see link below), the tariffs would increase employment in these industries by around 33 000. However, the higher price of these metals would cause job losses in the industries using them. In fact, according to the report, more than five jobs would be lost for every one gained. The CNN Money article linked below gives example of the US industries that will be hit.

But the costs are likely to be much greater than this. Accorinding to the law of comparative advantage, trade is a positive-sum game, with a net gain to all parties engaged in trade. Unless trade restrictions are used to address a specific market distortion in the trade process itself, restricting trade will lead to a net loss in overall benefit to the parties involved.

Clearly there will be loss to steel and aluminium exporters outside the USA. There will also be a net loss to their countries unless these metals had a higher cost of production than in the USA, but were subsidised by governments so that they could be exported profitably.

But perhaps the biggest cost will arise from possible retaliation by other countries. A trade war would compound the net losses as the world moves further from trade based on comparative advantage.

Already, many countries are talking about retaliation. For example, the EU is considering a ‘reciprocal’ tariff of 25% on cranberries, bourbon and Harley-Davidsons, all produced in politically sensitive US states (see the first The Economist article below). ‘As Jean-Claude Juncker, president of the European Commission, puts it, “We can also do stupid”.’ In fact, this is quite a politically astute move to put pressure on Mr Trump.

But cannot countries appeal to the WTO? Possibly, but this route might take some time. What is more, the USA has attempted to get around WTO rules by justifying the tariffs on ‘national security’ grounds – something allowed under Article XXI of WTO rules, provided it can be justified. This could possibly deter countries from retaliating, but it is probably unlikely. In the current climate, there seems to be a growing mood for flouting, or at least loosely interpreting, WTO rules.

Each January, world political and business leaders gather at the ski resort of Davos in Switzerland for the World Economic Forum. They discuss a range of economic and political issues with the hope of guiding policy.

This year, leaders meet at a time when the global political context has and is changing rapidly. This year the focus is on ‘Creating a Shared Future in a Fractured World’. As the Forum’s website states:

The global context has changed dramatically: geostrategic fissures have re-emerged on multiple fronts with wide-ranging political, economic and social consequences. Realpolitik is no longer just a relic of the Cold War. Economic prosperity and social cohesion are not one and the same. The global commons cannot protect or heal itself.

One of the main ‘fissures’ which threatens social cohesion is the widening gap between the very rich and the rest of the world. Indeed, inequality and poverty is one of the main agenda items at the Davos meeting and the Forum website includes an article titled, ‘We have built an unequal world. Here’s how we can change it’ (see second link in the Articles below). The article shows how the top 1% captured 27% of GDP growth between 1980 and 2016.

The first Guardian article below identifies seven different policy options to tackle the problem of inequality of income and wealth and asks you to say, using a drop-down menu, which one you think is most important. Perhaps it’s something you would like to do.

With the Conservatives having lost their majority in Parliament in the recent UK election, there is renewed discussion of the form that Brexit might take. EU states are members of the single market and the customs union. A ‘hard Brexit’ involves leaving both and this was the government’s stance prior to the election. But there is now talk of a softer Brexit, which might mean retaining membership of the single market and/or customs union.

The single market

Belonging to the single market means accepting the free movement of goods, services, capital and labour. It also involves tariff-free trade within the single market and adopting a common set of rules and regulations over trade, product standards, safety, packaging, etc., with disputes settled by the European Court of Justice. Membership of the single market involves paying budgetary contributions. Norway and Iceland are members of the single market.

The single market brings huge benefits from free trade with no administrative barriers from customs checks and paperwork. But it would probably prove impossible to negotiate remaining in the single market with an opt out on free movement of labour. Controlling immigration from EU countries was a key part of the Leave campaign.

The customs union

This involves all EU countries adopting the same tariffs (customs duties) on imports from outside the EU. These tariffs are negotiated by the European Commission with non-EU countries on a country-by-country basis. Goods imported from outside the EU are charged tariffs in the country of import and can then be sold freely around the EU with no further tariffs.

Remaining a member of the customs union would allow the UK to continue trading freely in the EU, subject to meeting various non-tariff regulations. It would also allow free ‘borderless’ trade between Northern Ireland and the Republic of Ireland. However, being a member of the customs union would prevent the UK from negotiating separate trade deals with non-EU countries. The ability to negotiate such deals has been argued to be one of the main benefits of leaving the EU.

Free(r) trade area

The UK could negotiate a trade deal with the EU. But it is highly unlikely that such a deal could be in place by March 2019, the date when the UK is scheduled to leave the EU. At that point, trade barriers would be imposed, including between the two parts of the island of Ireland. Such deals are very complex, especially in the area of services, which are the largest category of UK exports. Negotiating tariff-free or reduced-tariff trade is only a small part of the problem; the biggest part involves negotiating product standards, regulations and other non-tariff barriers.

All the above options thus involve serious problems and the government will be pushed from various sides, not least within the Conservative Party, for different degrees of ‘softness’ or ‘hardness’ of Brexit. What is more, the pressure from business for free trade with the EU is likely to grow. Brexit may mean Brexit, but just what form it will take is very unclear.

Explain the trading agreement between Norway and the EU.

How does the Norwegian arrangement with the EU differ from the Turkish one?

What are meant by the terms ‘hard Brexit’ and ‘soft Brexit’?

How does a customs union differ from a free trade area?

Is it possible to have (a) a customs union without a single market; (b) a single market without a customs union?

To what extent is it in the EU’s interests to negotiate a deal with the UK which lets it maintain access to the customs union without having free movement of labour?

The EU insists that talks about future trading arrangements between the UK and the EU can take place only after sufficient progress has been made on the terms of the ‘divorce’. What elements are included in the divorce terms?

If agreement is not reached by 29 March 2019, what happens and what would be the consequences?

Will a hung parliament, or at least a government supported by the DUP on a confidence and supply basis, make it more or less likely that there will be a hard Brexit?

For what reasons may the EU favour (a) a hard Brexit; (b) a soft Brexit?

One of President Trump’s main policy slogans has been ‘America first’. As Trump sees it, a manifestation of a country’s economic strength is its current account balance. He would love the USA to have a current account surplus. As it is, it has the largest current account deficit in the world (in absolute terms) of $481 billion in 2016 or 2.6% of GDP. This compares with the UK’s $115bn or 4.4% of GDP. Germany, by contrast, had a surplus in 2016 of $294bn or 8.5% of GDP.

However, he looks at other countries’ current account surpluses suspiciously – they may be a sign, he suspects, of ‘unfair play’. Germany’s surplus of over $50bn with the USA is particularly in his sights. Back in January, as President-elect, he threatened to put a 35% tariff on imports of German cars.

In practice, Germany is governed by eurozone rules, which prevent it from subsidising exports. And it does not have its own currency to manipulate. What is more, it is relatively open to imports from the USA. The EU imposes an average tariff of just 3% on US imports and importers also have to add VAT (19% in the case of Germany) to make them comparably priced with goods produced within the EU.

So why does Germany have such a large current account surplus? The article below explores the question and dismisses the claim that it’s the result of currency manipulation or discrimination against imports. The article states that the reason for the German surplus is that:

… it saves more than it invests. The correspondence of savings minus investment with exports minus imports is not an economic theory; it’s an accounting identity. Germans collectively spend less than they produce, and the difference necessarily shows up as net exports.

But why do the Germans save so much? The answer given is that, with an aging population, Germans are sensibly saving now to support themselves in old age. If Germany were to reduce its current account surplus, this would entail either the government reducing its budget surplus, or people reducing the amount they save, or some combination of the two. This is because a current account surplus, which consists of exports and other incomes from abroad (X) minus imports and any other income flowing abroad (M), must equal the surplus of saving (S) plus taxation (T) over investment (I) plus government expenditure (G). In terms of withdrawals and injections, given that:

I + G + X = S + T + M

then, rearranging the terms,

X – M = (S + T) – (I + G).

If German people are reluctant to reduce the amount they save, then an alternative is for the German government to reduce taxation or increase government expenditure. In the run-up to the forthcoming election on 24 September, Chancellor Merkel’s centre-right CDU party advocates cutting taxes, while the main opposition party, the SPD, advocates increasing government expenditure, especially on infrastructure. The article considers the arguments for these two approaches.

Why does Germany have such a large current account surplus?

What are the costs and benefits to Germany of having a large current account surplus?

What is meant by ‘mercantilism’? Why is its justification fallacious?

If Germany had its own currency, would it be a good idea for it to let that currency appreciate?

What are meant by ‘resource crowding out’ and ‘financial crowding out’? Why might the policies of tax cuts advocated by the CDU result in crowding out? What form would it take and why?

Compare the relative benefits of the policies advocated by the CDU and SPD to reduce Germany’s budget surplus.

Would other countries, such as the USA, benefit from a reduction in Germany’s current account surplus?

Is what ways would the USA gain and lose from restricting imports from Germany? Would it be a net gain or loss? Explain.

The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.

Assuming there were no retaliation from other countries, jobs would be gained in the steel and aluminium industries. According to a report by The Trade Partnership (see link below), the tariffs would increase employment in these industries by around 33 000. However, the higher price of these metals would cause job losses in the industries using them. In fact, according to the report, more than five jobs would be lost for every one gained. The CNN Money article linked below gives example of the US industries that will be hit.

Assuming there were no retaliation from other countries, jobs would be gained in the steel and aluminium industries. According to a report by The Trade Partnership (see link below), the tariffs would increase employment in these industries by around 33 000. However, the higher price of these metals would cause job losses in the industries using them. In fact, according to the report, more than five jobs would be lost for every one gained. The CNN Money article linked below gives example of the US industries that will be hit. But perhaps the biggest cost will arise from possible retaliation by other countries. A trade war would compound the net losses as the world moves further from trade based on comparative advantage.

But perhaps the biggest cost will arise from possible retaliation by other countries. A trade war would compound the net losses as the world moves further from trade based on comparative advantage.