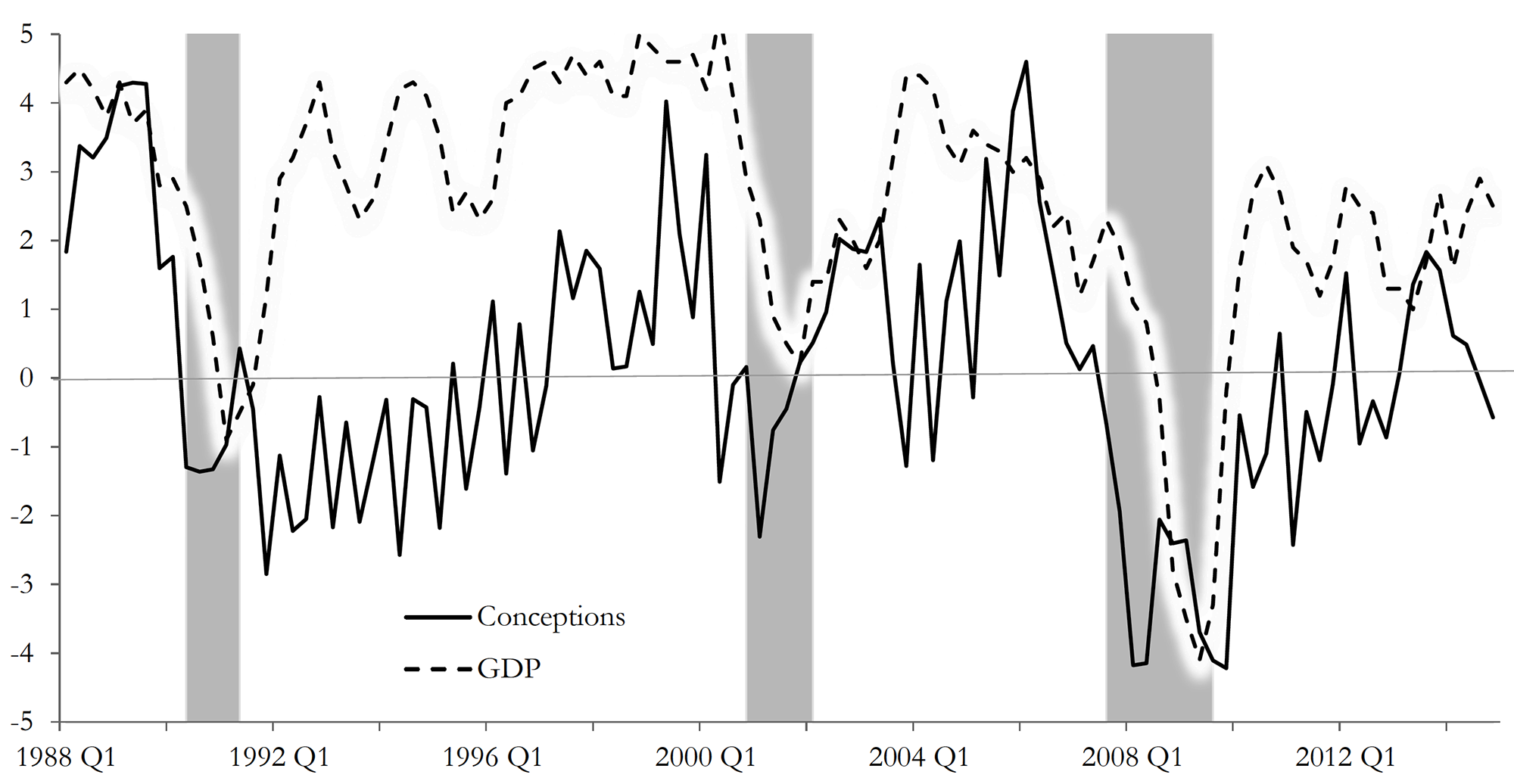

Would you start a family if you were pessimistic about the future of the economy? Buckles et al (2017) (see link below) believe that fewer of us would do so and, therefore, fertility rates could be used by investors and central banks as an early signal to pick up subtle changes in consumer confidence and overall economic climate.

Their study titled ‘Fertility is a leading economic indicator’ uses ‘live births’ data, sourced from US birth certificates, to explore if there is any association between fertility changes (measured as the rate of change in number of births) and GDP growth. Their results suggest that, in the case of the USA, there is: dips in fertility rates tend to precede by several quarters slowdown in economic activity. As the authors state:

The growth rate of conceptions declines prior to economic downturns and the decline occurs several quarters before recessions begin. Our measure of conceptions is constructed using live births; we present evidence suggesting that our results are indeed driven by changes in conceptions and not by changes in abortion or miscarriage. Conceptions compare well with or even outperform other economic indicators in anticipating recessions.

Conception and GDP Growth Rates (source Buckles et al p33: see below)

Although this is not the first piece of academic writing to claim that fertility has pro-cyclical qualities (see for instance, Adsera (2004, 2011), Adsera and Menendez (2011), Currie and Schwandt (2014) and Chatterjee and Vogle (2016) linked below), it is, to the best of our knowledge, the most recent paper (in terms of data used) to depict this relationship and to explore the suitability of fertility as a macroeconomic indicator to predict recessions.

Economies, after all, are groups of people who participate actively in day-to-day production and consumption activities – as consumers, workers and business leaders. Changes in their environment should affect their expectations about the future.

Are people, however, forward-looking enough to guide their current behaviours by their expectations of future economic outcomes? They may be, according to the findings of this study.

Did you know, for instance, that sales of ties tend to increase in economic downturns, as men buy more ties to show that they are working harder, in fear of losing their job[1]? But this is probably a topic for another blog.

Give two reasons why fertility rates may be a good indicator of economic activity.

Give two reasons why fertility rates may NOT be a good indicator of economic activity.

Do a literature search to identify and explain an ‘unorthodox’ macroeconomic indicator of your choice, and how it has been used to track economic activity.

The Winter Olympics are full on as athletes from all over the world compete against each other, hoping to set new world records, win medals and be known as Olympians. Pyeongchang, the South Korean county that hosts the 2018 Winter games, enjoys a large influx of tourists – estimated at 80,000 people a day. This is certainly an unusually large number of tourists for a region that has a regular winter-time population of no more than 45,000 people.

Having such a high number of visitors to the Winter Olympics, and even more to the larger Summer Olympics, is not an unusual occurrence, however, and it is often mentioned as one of the benefits of being a host to the Olympic Games.

Baade and Matheson (see link below) distinguish between three key benefits of hosting the Olympic Games: “the short-run benefits of tourist spending during the Games; the long-run benefits or the ‘Olympic legacy’, which might include improvements in infrastructure and increased trade, foreign investment, or tourism after the Games; and intangible benefits such as the ‘feel-good effect’ or civic pride”.

On these grounds, a number of studies have been authored, attempting to analyse some or all of these benefits, distinguishing between short-term and long-term effects. Müller (see link below), uses data from the 2014 Oympic Games in Sochi, Russia, to assess the net economic outcome for the host region. He concludes that any short-term economic benefits caused by the investment influx (before and during the games) could not offset the long-term costs, leading to an estimated net loss of $1.2 billion per year.

Zimbalist (2015) and Szymanski (2011) report similar results when analysing data from the London Games (2012) and past major sporting events (Games and FIFA World Cup). Kasimati (2003) points out the significant economic benefits that host regions tend to enjoy for years after hosting the games, but argues that the overall effect depends on a number of factors (including pre-existing infrastructure and location).

The jury is, therefore, still out on what is the overall economic effect of being host to this ancient institution. But I must now dash as women’s hockey is soon to start. “Let everyone shine”.

Using supply and demand diagrams, explain whether you would expect hotel room prices to change during the hosting of a major sports event, such as the Winter Olympics.

List three economic (or economics-related) arguments in favour of and against the hosting of the Olympic games. Relate your answer to the empirical evidence presented in the literature.

Why is it so difficult to estimate with accuracy the net economic effect of the Olympic Games?

These are challenging times for business. Economic growth has weakened markedly over the past 18 months with output currently growing at an annual rate of around 1.5 per cent, a percentage point below the long-term average. Spending power continues to be squeezed, with the annual rate of inflation in October reported to be running at 3.1 per cent compared to annual earnings growth of 2.5 per cent (see the squeeze continues). Moreover, consumer confidence remains fragile with households continuing to express particular concerns about the general economy and unemployment.

Here, we update our blog of July 2016 which, following the UK vote to leave the European Union, noted the fears for UK growth as confidence fell sharply. Consumer confidence is frequently identified by macro-economists as an important source of economic volatility. Indeed many macro models use a change in consumer confidence as a means of illustrating how economic shocks affect a range of macro variables, including growth, employment and inflation. Many economists agree that, in the short term at least, falling levels of confidence adversely affect activity because aggregate demand falls as households spend less.

The European Commission’s confidence measure is collated from questions in a monthly survey. In the UK around 2000 individuals are surveyed. Across the EU as a whole over 41 000 people are surveyed. In the survey individuals are asked a series of 12 questions which are designed to provide information on spending and saving intentions. These questions include perceptions of financial well-being, the general economic situation, consumer prices, unemployment, saving and the undertaking of major purchases.

The responses elicit either negative or positive responses. For example, respondents may feel that over the next 12 months the financial situation of their household will improve a little or a lot, stay the same or deteriorate a little or a lot. A weighted balance of positive over negative replies can be calculated. The balance can vary from -100, when all respondents choose the most negative option, to +100, when all respondents choose the most positive option.

The European Commission’s principal consumer confidence indicator is the average of the balances of four of the twelve questions posed: the financial situation of households, the general economic situation, unemployment expectations (with inverted sign) and savings, all over the next 12 months. These forward-looking balances are seasonally adjusted. The aggregate confidence indicator is thought to track developments in households’ spending intentions and, in turn, likely movements in the rate of growth of household consumption.

Chart 1 shows the consumer confidence indicator for the UK. The long-term average of –8.6 shows that negative responses across the four questions typically outweigh positive responses. In November 2017 the confidence balance stood at -5.2 roughly on par with its value in the previous two months, though marginally up on values of close to -7 over the summer. However, as recently as the beginning of 2016 the aggregate confidence score was running at around +4. In this context, current levels do constitute a significant change in consumer sentiment, changes which do ordinarily mark similar turning points in economic activity.(Click here to download a PowerPoint of the chart.)

Chart 2 allows to look behind the European Commission’s headline confidence indicator for the UK by looking at its four component balances. From it, we can see a deterioration in all four components. However, by far the most significant change in the individual confidence balances has been the sharp deterioration in expectations for the general economy. In November the forward-looking general economic situation stood at -25.5, compared to its long-run average of -11.6. (Click here to download a PowerPoint of the chart.)

The fall in UK consumer confidence is even more stark when compared to developments in consumer confidence across the whole of the European Union and in the 19 countries that make up the Euro area. Chart 3 shows how UK consumer confidence recovered relatively more strongly following the financial crisis of the late 2000s. The headline confidence indicator rose strongly from the middle of 2013 and was consistently in positive territory during 2014, 2015 and into 2016. The fall in consumer confidence in the UK has seen the headline confidence measure fall below that for the EU and the euro area. (Click here to download a PowerPoint of the chart.)

Consumer (and business) confidence is closely linked to uncertainty. The circumstances following the UK vote to leave the EU have undoubtedly created the conditions for acute uncertainty. Uncertainty breeds caution. Economists sometimes talk about spending being affected by two conflicting motives: prudence and impatience. While impatience creates a desire for spending now, prudence pushes us towards saving and insuring ourselves against uncertainty and unforeseen events. The worry is that the twin forces of fragile confidence and squeezed real earning are weighting heavily in favour of prudence and patience (a reduction in impatience). Going forward, this could create the conditions for a sustained period of subdued growth which, if it were to impact heavily on firms’ investment plans, could adversely impact on the economy’s productive potential. The hope is that the Brexit negotiations can move apace to reduce uncertainty and limit uncertainty’s adverse impact on economic activity.

Draw up a series of factors that you think might affect consumer confidence.

Explain what you understand by a positive and a negative demand-side shock. How might changes in consumer confidence generate demand shocks?

Analyse the ways in which consumer confidence might affect economic activity.

Which of the following statements is likely to be more accurate: (a) Consumer confidence drives economic activity or (b) Economic activity drives consumer confidence?

What macroeconomic indicators would those compiling the consumer confidence indicator expect the indicator to predict?

Analyse the possible short-term and longer-term economic implications of a fall in consumer confidence.

How might uncertainty affect consumer confidence?

What do the concepts of impatience and prudence mean in the context of consumer spending? When consumer confidence falls which of these might become more significant for consumer spending?

The latest edition of the IMF’s Fiscal Monitor, ‘Tackling Inequality’ challenges conventional wisdom that policies to reduce inequality will also reduce economic growth.

While some inequality is inevitable in a market-based economic system, excessive inequality can erode social cohesion, lead to political polarization, and ultimately lower economic growth.

The IMF looks at three possible policy alternatives to reduce inequality without damaging economic growth

The first is a rise in personal income tax rates for top earners. Since top rates have been cut in most countries, with the OECD average falling from 62% to 35% over the past 30 years, the IMF maintains that there is considerable scope of raising top rates, with the optimum being around 44%. Evidence suggests that income tax elasticity is low at most countries’ current top rates, meaning that a rise in top income tax rates would only have a small disincentive effect on earnings.

An increased progressiveness of income tax should be backed by sufficient taxes on capital to prevent income being reclassified as capital. Different types of wealth tax, such as inheritance tax, could also be considered. Countries should also reduce the opportunities for tax evasion.

The second policy alternative is a universal basic income for all people. This could be achieved by various means, such as tax credits, child benefits and other cash benefits, or minimum wages plus benefits for the unemployed or non-employed.

The third is better access to health and education, both for their direct effect on reducing inequality and for improving productivity and hence people’s earning potential.

In all three cases, fiscal policy can help through a combination of taxes, benefits and public expenditure on social infrastructure and human capital.

But a major problem with using increased tax rates is international competition, especially with corporation tax rates. Countries are keen to attract international investment by having corporation tax rates lower than their rivals. But, of course, countries cannot all have a lower rate than each other. The attempt to do so simply leads to a general lowering of corporation tax rates (see chart in The Economist article) – to a race to the bottom. The Nash equilibrium rate of such a game is zero!

Referring to the October 2017 Fiscal Monitor, linked above, what arguments does the IMF use for suggesting that the optimal top rate of income tax is considerably higher than the current OECD average?

What are the arguments for introducing a universal basic income? Should this depend on people’s circumstances, such as the number of their children, assets, such as savings or property, and housing costs?

Find out the details of the UK government’s Universal Credit. Does this classify as a universal basic income?

Why may governments reject the IMF’s policy recommendations to tackle inequality?

In what sense can better access to health and education be seen as a means of reducing inequality? How is inequality being defined in this case?

Find out what the UK Labour Party’s policy is on rates of income tax for top earners. Is this consistent with the IMF’s policy recommendations?

What does the IMF report suggest about the shape of the Laffer curve?

Explain what is meant by tax elasticity and how it relates to the Laffer curve?

On the 15th June, the Bank of England’s Monetary Policy Committee decided to keep Bank Rate on hold at its record low of 0.25%. This was not a surprise – it was what commentators had expected. What was surprising, however, was the split in the MPC. Three of its current eight members voted to raise the rate.

At first sight, raising the rate might seem the obvious thing to do. CPI inflation is currently 2.9% – up from 2.7% in April and well above the target of 2% – and is forecast to go higher later this year. According to the Bank of England’s own forecasts, even at the 24-month horizon inflation is still likely to be a little above the 2% target.

Those who voted for an increase of 0.25 percentage points to 0.5% saw it as modest, signalling only a very gradual return to more ‘normal’ interest rates. However, the five who voted to keep the rate at 0.25% felt that it could dampen demand too much.

The key argument is that inflation is not of the demand-pull variety. Aggregate demand is subdued. Real wages are falling and hence consumer demand is likely to fall too. Thus many firms are cautious about investing, especially given the considerable uncertainties surrounding the nature of Brexit. The prime cause of the rise in inflation is the fall in sterling since the Brexit vote and the effect of higher import costs feeding through into retail prices. In other words, the inflation is of the cost-push variety. In such cirsumstances dampening demand further by raising interest rates would be seen by most economists as the wrong response. As the minutes of the MPC meeting state:

Attempting to offset fully the effect of weaker sterling on inflation would be achievable only at the cost of higher unemployment and, in all likelihood, even weaker income growth. For this reason, the MPC’s remit specifies that, in such exceptional circumstances, the Committee must balance any trade-off between the speed at which it intends to return inflation sustainably to the target and the support that monetary policy provides to jobs and activity.

The MPC recognises that the outlook is uncertain. It states that it stands ready to respond to circumstances as they change. If demand proves to be more resilient that it currently expects, it will raise Bank Rate. If not, it is likely to keep it on hold to continue providing a modest stimulus to the economy. However, it is unlikely to engage in further quantitative easing unless the economic outlook deteriorates markedly.

What is the mechanism whereby a change in Bank Rate affects other interest artes?

Use an aggregate demand and supply diagram to illustrate the difference between demand-pull and cost-push inflation.

If the exchange rate remains at around 10–15% below the level before the Brexit vote, will inflation continue to remain above the Bank of England’s target, or will it reach a peak relatively soon and then fall back? Explain.

For what reason might aggregate demand prove more buoyant that the MPC predicts?

Would a rise in Bank Rate from 0.25% to 0.5% have a significant effect on aggregate demand? What role could expectations play in determining the nature and size of the effect?

Why are real wage rates falling at a time when unemployment is historically very low?

What determines the amount that higher prices paid by importers of products are passed on to consumers?

Would you start a family if you were pessimistic about the future of the economy? Buckles et al (2017) (see link below) believe that fewer of us would do so and, therefore, fertility rates could be used by investors and central banks as an early signal to pick up subtle changes in consumer confidence and overall economic climate.

Would you start a family if you were pessimistic about the future of the economy? Buckles et al (2017) (see link below) believe that fewer of us would do so and, therefore, fertility rates could be used by investors and central banks as an early signal to pick up subtle changes in consumer confidence and overall economic climate.