Policymakers around the world have used Gross Domestic Product as the main gauge of economic performance – and have often adopted policies that aim to maximise its rate of growth. Generation after generation of economists have committed significant time and effort to thinking about the factors that influence GDP growth, on the premise that an expanding and healthy economy is one that sees its GDP increasing every year at a sufficient rate.

But is economic output a good enough indicator of national economic wellbeing? Costanza et al (2014) (see link below) argue that, despite its merits, GDP can be a ‘misleading measure of national success’:

GDP measures mainly market transactions. It ignores social costs, environmental impacts and income inequality. If a business used GDP-style accounting, it would aim to maximize gross revenue — even at the expense of profitability, efficiency, sustainability or flexibility. That is hardly smart or sustainable (think Enron). Yet since the end of the Second World War, promoting GDP growth has remained the primary national policy goal in almost every country. Meanwhile, researchers have become much better at measuring what actually does make life worthwhile. The environmental and social effects of GDP growth is a misleading measure of national success. Countries should act now to embrace new metrics.

The limitations of GDP growth as a measure of economic wellbeing and national strength are becoming increasingly clear in today’s world. Some of the world’s wealthiest countries are plagued by discontent, with a growth in populism and social discontent – attitudes which are often fuelled by high rates of poverty and economic hardship. In a recent report titled ‘The Living Standards Audit 2018’ published by the Resolution Foundation, a UK economic thinktank (see link below), the authors found that child poverty rose in 2016–17 as a result of declining incomes of the poorest third of UK households:

While the economic profile of UK households has changed, living standards – with the exception of pensioner households – have mostly stagnated since the mid-2000s. Typical household incomes are not much higher than they were in 2003–04. This stagnation in living standards for many has brought with it a rise in poverty rates for low to middle income families. Over a third of low to middle income families with children are in poverty, up from a quarter in the mid-2000s, and nearly two-fifths say that they can’t afford a holiday away for their children once a year. On the other hand, the share of non-working families in poverty has fallen, though not by enough to prevent an overall rise in poverty since 2010.

Their projections also show that this rise in poverty was likely to have continued in 2017–18:

Although the increase in broad measures of inequality were relatively muted last year, our nowcast suggests that there was a pronounced rise in poverty (measured after housing costs[…]. The increase in overall poverty (from 22.1 to 23.2 per cent) was the largest since 1988. But this was dwarfed by the increase in child poverty, which rose from 30.3 per cent to 33.4 per cent. […]The fortunes of middle-income households diverged from those towards the bottom of the distribution and so a greater share of households, and children, found themselves below the poverty threshold.

A simple literature search on Scope (or even Google Scholar) shows that there has been a significant increase in the number of journal articles and reports in the last 10 years on this topic. We do talk more about the limitations of GDP, but we are still using it as the main measure of national economic performance.

Is it then time to stop focusing our attention on GDP growth exclusively and start considering broader metrics of social development? And what would such metrics look like? Both interesting questions that we will try to address in coming blogs.

Hearing before the Subcommittee on Interstate Commerce, Trade, and Tourism of the United States Senate Committee on Commerce, Science and Transportation (12/3/08)

Questions

What are the main strengths and weakness of using GDP as measure of economic performance?

Is high GDP growth alone enough to foster economic and social wellbeing? Explain your answer using examples.

Write a list of alternative measures that could be used alongside GDP-based metrics to measure economic and social progress. Explain your answer.

I admit it, the title of my blog today is a little bit misleading – but at the same time very appropriate for today’s topic. Nancy Sinatra certainly wasn’t thinking about emigration when she was singing this song – it had nothing to do with it, after all. It is, however, very relevant to economists: Indeed, there are many economics papers discussing the effects of skilled immigration on host and source economies and regions.

Economists often use the term ‘brain drain’ to describe the migration of highly skilled workers from poor/developing to rich/developed economies. Such flows are anything but unusual. As The Economist points out in a recent article, ‘[I]n the decade to 2010–11 the number of university-educated migrants in the G20, a group of large economies that hosts two-thirds of the world’s migrants, grew by 60% to 32m according to the OECD, a club of mostly rich countries.’.

The effects of international migration are found to be overwhelmingly positive for both skilled migrant workers and their hosts. This is particularly true for highly skilled workers (such as academics, physicians and other professionals), who, through emigration, get the opportunity to earn a significantly higher return on their skills that what they might have had in their home country. Very often their home country is saturated and oversupplied with skilled workers competing for a very limited number of jobs. Also, they get the opportunity to practise their profession – which they might not have had otherwise.

But what about their home countries? Are they worse off for such emigration?

There are different views when it comes to answering this question. One argument is that the prospect of international migration incentivises people in developing countries to accumulate skills (brain gain) – which they might not choose to do otherwise, if the expected return to skills was not high enough to warrant the effort and opportunity cost that comes with it. Beine et al (2011) find that:

Our empirical analysis predicts conditional convergence of human capital indicators. Our findings also reveal that skilled migration prospects foster human capital accumulation in low-income countries. In these countries, a net brain gain can be obtained if the skilled emigration rate is not too large (i.e. it does not exceed 20–30% depending on other country characteristics). In contrast, we find no evidence of a significant incentive mechanism in middle-income, and not surprisingly, high-income countries.

Other researchers find that emigration can have a significant negative effect on source economies (countries or regions) – especially if it affects a large share of the local workforce within a short time period. Ha et al (2016), analyse the effect of emigration on human capital formation and economic growth of Chinese provinces:

First, we find that permanent emigration is conducive to the improvement of both middle and high school enrollment. In contrast, while temporary emigration has a significantly positive effect on middle school enrollment it does not affect high school enrollment. Moreover, the different educational attainments of temporary emigrants have different effects on school enrollment. Specifically, the proportion of temporary emigrants with high school education positively affects middle school enrollment, while the proportion of temporary emigrants with middle school education negatively affects high school enrollment. Finally, we find that both permanent and temporary emigration has a detrimental effect on the economic growth of source regions.

So yes or no? Good or bad? As everything else in economics, the answer quite often is ‘it depends’.

World Development, Michel Beine, Ric Docquier and Cecily Oden-Defoort (Vol 39, No 4, pp 523–532, 2011)

Questions

‘The brain drain makes a bad situation worse, by stripping developing economies of their most valuable assets: skilled workers’. Discuss.

Using Google, find data on the inflows and outflows of skilled labour for a developing country of your choice. Explain your results.

‘Brain drain’ or ‘brain gain’? What is your personal view on this debate? Explain your opinion by using anecdotal evidence, personal experience and examples.

Referring to the previous question, write a critique of your answer.

The IMF has just published its six-monthly World Economic Outlook. This provides an assessment of trends in the global economy and gives forecasts for a range of macroeconomic indicators by country, by groups of countries and for the whole world.

This latest report is upbeat for the short term. Global economic growth is expected to be around 3.9% this year and next. This represents 2.3% this year and 2.5% next for advanced countries and 4.8% this year and 4.9% next for emerging and developing countries. For large advanced countries such rates are above potential economic growth rates of around 1.6% and thus represent a rise in the positive output gap or fall in the negative one.

But while the near future for economic growth seems positive, the IMF is less optimistic beyond that for advanced countries, where growth rates are forecast to decline to 2.2% in 2019, 1.7% in 2020 and 1.5% by 2023. Emerging and developing countries, however, are expected to see growth rates of around 5% being maintained.

For most countries, current favorable growth rates will not last. Policymakers should seize this opportunity to bolster growth, make it more durable, and equip their governments better to counter the next downturn.

By comparison with other countries, the UK’s growth prospects look poor. The IMF forecasts that its growth rate will slow from 1.8% in 2017 to 1.6% in 2018 and 1.5% in 2019, eventually rising to around 1.6% by 2023. The short-term figures are lower than in the USA, France and Germany and reflect ‘the anticipated higher barriers to trade and lower foreign direct investment following Brexit’.

The report sounds some alarm bells for the global economy.

The first is a possible growth in trade barriers as a trade war looms between the USA and China and as Russia faces growing trade sanctions. As Christine Lagarde, managing director of the IMF told an audience in Hong Kong:

Governments need to steer clear of protectionism in all its forms. …Remember: the multilateral trade system has transformed our world over the past generation. It helped reduce by half the proportion of the global population living in extreme poverty. It has reduced the cost of living, and has created millions of new jobs with higher wages. …But that system of rules and shared responsibility is now in danger of being torn apart. This would be an inexcusable, collective policy failure. So let us redouble our efforts to reduce trade barriers and resolve disagreements without using exceptional measures.

The second danger is a growth in world government and private debt levels, which at 225% of global GDP are now higher than before the financial crisis of 2007–9. With Trump’s policies of tax cuts and increased government expenditure, the resulting rise in US government debt levels could see some fiscal tightening ahead, which could act as a brake on the world economy. As Maurice Obstfeld , Economic Counsellor and Director of the Research Department, said at the Press Conference launching the latest World Economic Outlook:

Debts throughout the world are very high, and a lot of debts are denominated in dollars. And if dollar funding costs rise, this could be a strain on countries’ sovereign financial institutions.

In China, there has been a massive rise in corporate debt, which may become unsustainable if the Chinese economy slows. Other countries too have seen a surge in private-sector debt. If optimism is replaced by pessimism, there could be a ‘Minsky moment’, where people start to claw down on debt and banks become less generous in lending. This could lead to another crisis and a global recession. A trigger could be rising interest rates, with people finding it hard to service their debts and so cut down on spending.

The third danger is the slow growth in labour productivity combined with aging populations in developed countries. This acts as a brake on growth. The rise in AI and robotics (see the post Rage against the machine) could help to increase potential growth rates, but this could cost jobs in the short term and the benefits could be very unevenly distributed.

This brings us to a final issue and this is the long-term trend to greater inequality, especially in developed economies. Growth has been skewed to the top end of the income distribution. As the April 2017 WEO reported, “technological advances have contributed the most to the recent rise in inequality, but increased financial globalization – and foreign direct investment in particular – has also played a role.”

And the policy of quantitative easing has also tended to benefit the rich, as its main effect has been to push up asset prices, such as share and house prices. Although this has indirectly stimulated the economy, it has mainly benefited asset owners, many of whom have seen their wealth soar. People further down the income scale have seen little or no growth in their real incomes since the financial crisis.

For what reasons may the IMF forecasts turn out to be incorrect?

Why are emerging and developing countries likely to experience faster rates of economic growth than advanced countries?

What are meant by a ‘positive output gap’ and a ‘negative output gap’? What are the consequences of each for various macroeconomic indicators?

Explain what is meant by a ‘Minsky moment’. When are such moments likely to occur? Explain why or why not such a moment is likely to occur in the next two or three years?

For every debt owed, someone is owed that debt. So does it matter if global public and/or private debts rise? Explain.

What have been the positive and negative effects of the policy of quantitative easing?

What are the arguments for and against using tariffs and other forms of trade restrictions as a means of boosting a country’s domestic economy?

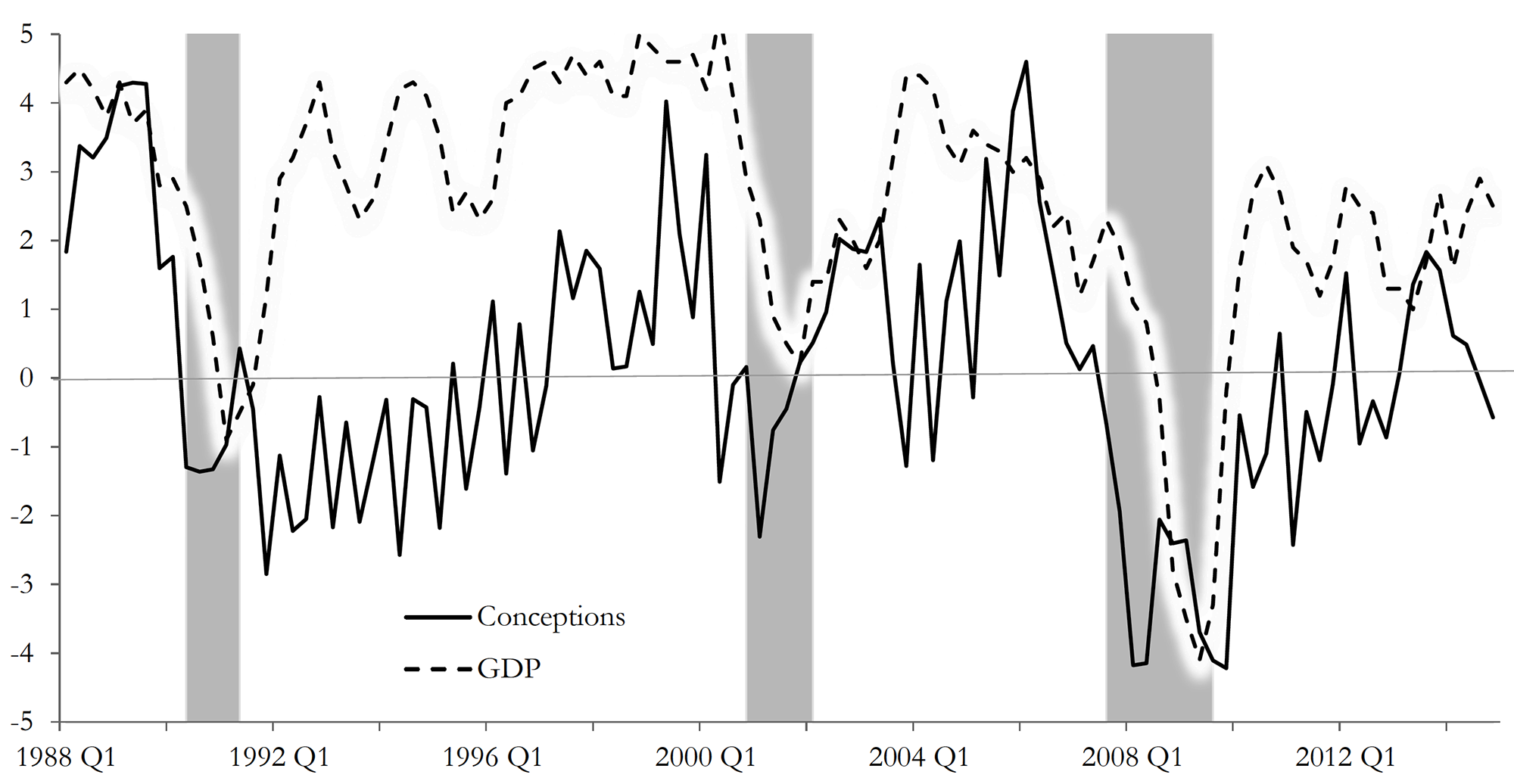

Would you start a family if you were pessimistic about the future of the economy? Buckles et al (2017) (see link below) believe that fewer of us would do so and, therefore, fertility rates could be used by investors and central banks as an early signal to pick up subtle changes in consumer confidence and overall economic climate.

Their study titled ‘Fertility is a leading economic indicator’ uses ‘live births’ data, sourced from US birth certificates, to explore if there is any association between fertility changes (measured as the rate of change in number of births) and GDP growth. Their results suggest that, in the case of the USA, there is: dips in fertility rates tend to precede by several quarters slowdown in economic activity. As the authors state:

The growth rate of conceptions declines prior to economic downturns and the decline occurs several quarters before recessions begin. Our measure of conceptions is constructed using live births; we present evidence suggesting that our results are indeed driven by changes in conceptions and not by changes in abortion or miscarriage. Conceptions compare well with or even outperform other economic indicators in anticipating recessions.

Conception and GDP Growth Rates (source Buckles et al p33: see below)

Although this is not the first piece of academic writing to claim that fertility has pro-cyclical qualities (see for instance, Adsera (2004, 2011), Adsera and Menendez (2011), Currie and Schwandt (2014) and Chatterjee and Vogle (2016) linked below), it is, to the best of our knowledge, the most recent paper (in terms of data used) to depict this relationship and to explore the suitability of fertility as a macroeconomic indicator to predict recessions.

Economies, after all, are groups of people who participate actively in day-to-day production and consumption activities – as consumers, workers and business leaders. Changes in their environment should affect their expectations about the future.

Are people, however, forward-looking enough to guide their current behaviours by their expectations of future economic outcomes? They may be, according to the findings of this study.

Did you know, for instance, that sales of ties tend to increase in economic downturns, as men buy more ties to show that they are working harder, in fear of losing their job[1]? But this is probably a topic for another blog.

Give two reasons why fertility rates may be a good indicator of economic activity.

Give two reasons why fertility rates may NOT be a good indicator of economic activity.

Do a literature search to identify and explain an ‘unorthodox’ macroeconomic indicator of your choice, and how it has been used to track economic activity.

On 8 February, the Bank of England issued a statement that was seen by many as a warning for earlier and speedier than previously anticipated increases in the UK base rate. Mark Carney, the governor of the Bank of England, referred in his statement to ‘recent forecasts’ which make it more likely that ‘monetary policy would need to be tightened somewhat earlier and by a somewhat greater extent over the forecast period than anticipated at the time of the November report’.

A similar picture emerges on the other side of the Atlantic. With labour markets continuing to deliver spectacularly high rates of employment (the highest in the last 17 years), there are also now signs that wages are on an upward trajectory. According to a recent report from the US Bureau of Labor Statistics, US wage growth has been stronger than expected, with average hourly earnings rising by 2.9 percent – the strongest growth since 2009.

These statements have coincided with a week of sharp corrections and turbulence in the world’s largest capital markets, as investors become increasingly conscious of the threat of rising inflation – and the possibility of tighter monetary policy.

The Dow Jones plunged from an all-time high of 26,186 points on 1 February to 23,860 a week later – losing more than 10 per cent of its value in just five trading sessions (suffering a 4.62 percentag fall on 5 February alone – the worst one-day point fall since 2011). European and Asian markets followed suit, with the FTSE-100, DAX and NIKKEI all suffering heavy losses in excess of 5 per cent over the same period.

But why should higher inflationary expectations fuel a sell-off in global capital markets? After all, what firm wouldn’t like to sell its commodities at a higher price? Well, that’s not entirely true. Investors know that further increases in inflation are likely to be met by central banks hiking interest rates. This is because central banks are unlikely to be willing or able to allow inflation rates to rise much above their target levels.

The Bank of England, for instance, sets itself an inflation target of 2%. The actual ongoing rate of inflation reported in the latest quarterly Inflation Report is 3% (50 per cent higher than the target rate).

Any increase in interest rates is likely to have a direct impact on both the demand and the supply side of the economy.

Consumers (the demand side) would see their cost of borrowing increase. This could put pressure on households that have accumulated large amounts of debt since the beginning of the recession and could result in lower consumer spending.

Firms (the supply side) are just as likely to suffer higher borrowing costs, but also higher operational costs due to rising wages – both of which could put pressure on profit margins.

It now seems more likely that we are coming towards the end of the post-2008 era – a period that saw the cost of money being driven down to unprecedentedly low rates as the world’s largest economies dealt with the aftermath of the Great Recession.

For some, this is not all bad news – as it takes us a step closer towards a more historically ‘normal’ equilibrium. It remains to be seen how smooth such a transition will be and to what extent the high-leveraged world economy will manage to keep its current pace, despite the increasingly hawkish stance in monetary policy by the world’s biggest central banks.

Using supply and demand diagrams, explain the likely effect of an increase in interest rates to equilibrium prices and output. Is it good news for investors and how do you expect them to react to such hikes? What other factors are likely to influence the direction of the effect?

Do you believe that the current ultra-low interest rates could stay with us for much longer? Explain your reasoning.

What is likely to happen to the exchange rate of the pound against the US dollar, if the Bank of England increases interest rates first?

Why do stock markets often ‘overshoot’ in responding to expected changes in interest rates or other economic variables

Policymakers around the world have used Gross Domestic Product as the main gauge of economic performance – and have often adopted policies that aim to maximise its rate of growth. Generation after generation of economists have committed significant time and effort to thinking about the factors that influence GDP growth, on the premise that an expanding and healthy economy is one that sees its GDP increasing every year at a sufficient rate.

Policymakers around the world have used Gross Domestic Product as the main gauge of economic performance – and have often adopted policies that aim to maximise its rate of growth. Generation after generation of economists have committed significant time and effort to thinking about the factors that influence GDP growth, on the premise that an expanding and healthy economy is one that sees its GDP increasing every year at a sufficient rate.  The limitations of GDP growth as a measure of economic wellbeing and national strength are becoming increasingly clear in today’s world. Some of the world’s wealthiest countries are plagued by discontent, with a growth in populism and social discontent – attitudes which are often fuelled by high rates of poverty and economic hardship. In a recent report titled ‘The Living Standards Audit 2018’ published by the Resolution Foundation, a UK economic thinktank (see link below), the authors found that child poverty rose in 2016–17 as a result of declining incomes of the poorest third of UK households:

The limitations of GDP growth as a measure of economic wellbeing and national strength are becoming increasingly clear in today’s world. Some of the world’s wealthiest countries are plagued by discontent, with a growth in populism and social discontent – attitudes which are often fuelled by high rates of poverty and economic hardship. In a recent report titled ‘The Living Standards Audit 2018’ published by the Resolution Foundation, a UK economic thinktank (see link below), the authors found that child poverty rose in 2016–17 as a result of declining incomes of the poorest third of UK households: I admit it, the title of my blog today is a little bit misleading – but at the same time very appropriate for today’s topic. Nancy Sinatra certainly wasn’t thinking about emigration when she was

I admit it, the title of my blog today is a little bit misleading – but at the same time very appropriate for today’s topic. Nancy Sinatra certainly wasn’t thinking about emigration when she was  But what about their home countries? Are they worse off for such emigration?

But what about their home countries? Are they worse off for such emigration? The IMF has just published its six-monthly

The IMF has just published its six-monthly  The short-term figures are lower than in the USA, France and Germany and reflect ‘the anticipated higher barriers to trade and lower foreign direct investment following Brexit’.

The short-term figures are lower than in the USA, France and Germany and reflect ‘the anticipated higher barriers to trade and lower foreign direct investment following Brexit’. The second danger is a growth in

The second danger is a growth in