The linked article below, by Evan Davis, assesses the state of economics. He argues that economics has had some major successes over the years in providing a framework for understanding how economies function and how to increase incomes and well-being more generally.

The linked article below, by Evan Davis, assesses the state of economics. He argues that economics has had some major successes over the years in providing a framework for understanding how economies function and how to increase incomes and well-being more generally.

Over the last few decades, economists have …had an influence over every aspect of our lives. …And during this era in which economists have reigned, the world has notched up some marked successes. The reduction in the proportion of human beings living in abject poverty over the last thirty years has been extraordinary.

With the development of concepts such as opportunity cost, the prisoners’ dilemma, comparative advantage and the paradox of thrift, economics has helped to shape the way policymakers perceive economic issues and policies.

These concepts are ‘threshold concepts’. Understanding and being able to relate and apply these core economic concepts helps you to ‘think like an economist’ and to relate the different parts of the subject to each other. Both Economics (10th edition) and Essentials of Economics (8th edition) examine 15 of these threshold concepts. Each time a threshold concept is used in the text, a ‘TC’ icon appears in the margin with the appropriate number. By locating them in this way, you can see their use in a variety of contexts.

But despite the insights provided by traditional economics into the various problems that society faces, the discipline of economics has faced criticism, especially since the financial crisis, which most economists did not foresee.

Even Davis identifies two major shortcomings of the discipline – both beginning with ‘C’. ‘One is complexity, the other is community.’

Even Davis identifies two major shortcomings of the discipline – both beginning with ‘C’. ‘One is complexity, the other is community.’

In terms of complexity, the criticism is that economic models are often based on simplistic assumptions, such as ‘rational maximising behaviour’. This might make it easier to express the models mathematically, but mathematical elegance does not necessarily translate into predictive accuracy. Such models do not capture the ‘messiness’ of the real world.

These models have a certain theoretical elegance but there is now an increasing sense that economies do not evolve along a well-defined mathematical path, but in a far more messy way. The individual players within the economy face radical uncertainty; they adapt and learn as they go; they watch what everybody else does. The economy stumbles along in a process of slow discovery, full of feedback loops.

As far as ‘community’ is concerned, people do not just act as self-interested individuals. Their actions are often governed by how other people behave and also by how their own actions will affect other people, such as family, friends, colleagues or society more generally.

And the same applies to firms. They will be influenced by various other firms, such as competitors, trend setters and suppliers and also by a range of stakeholders – not just shareholders, but also workers, customers, local communities, etc. A firm’s aim is thus unlikely to be simple short-term profit maximisation.

And the same applies to firms. They will be influenced by various other firms, such as competitors, trend setters and suppliers and also by a range of stakeholders – not just shareholders, but also workers, customers, local communities, etc. A firm’s aim is thus unlikely to be simple short-term profit maximisation.

And this broader set of interests translates into policy. The neoliberal free-market, laissez-faire approach to policy is challenged by the desire to take account of broader questions of equity, community and social justice. However privately efficient a free market is, it does not take account of the full social and environmental costs and benefits of firms’ and consumers’ actions or a fair distribution of income and wealth.

It would be wrong, however, to say that economics has not responded to these complexities and concerns. The analysis of externalities, income distribution, incentives, herd behaviour, uncertainty, speculation, cumulative causation and institutional values and biases are increasingly embedded in the economics curriculum and in economic research. What is more, behavioural economics is becoming increasingly mainstream in examining the behaviour of consumers, workers, firms and government. We have tried to reflect these developments in successive editions of our four textbooks.

Article

Questions

- Write a brief defence of traditional economic analysis (i.e. that based on the assumption of ‘rational economic behaviour’).

- What are the shortcomings of traditional economic analysis?

- What is meant by ‘behavioural economics’ and how does it address the concerns raised in Evan Davis’ article?

- How is herd behaviour relevant to explaining macroeconomic fluctuations?

- Identify various stakeholder groups of an energy company. What influence are they likely to have on the company’s behaviour?

- In an era of social media, web-based information and e-commerce, why might it be necessary to rethink the concept of GDP and its measurement?

- What is meant by an efficient stock market? Why may the stock market not be efficient?

The UK Chancellor of the Exchequer, Philip Hammond, announced in the Budget this week that national insurance contributions (NICs) for self-employed people will rise from 9% to 11% by 2019. These are known as ‘Class 4’ NICs. The average self-employed person will pay around £240 more per year, but those on incomes over £45,000 will pay £777 more per year. Many of the people affected will be those working in the so-called ‘gig economy’. This sector has been growing rapidly in recent years and now has over 4 million people working in it.

The UK Chancellor of the Exchequer, Philip Hammond, announced in the Budget this week that national insurance contributions (NICs) for self-employed people will rise from 9% to 11% by 2019. These are known as ‘Class 4’ NICs. The average self-employed person will pay around £240 more per year, but those on incomes over £45,000 will pay £777 more per year. Many of the people affected will be those working in the so-called ‘gig economy’. This sector has been growing rapidly in recent years and now has over 4 million people working in it.

Workers in the gig economy are self employed, but are often contracted to an employer. They are paid by the job (or ‘gig’: like musicians), rather than being paid a wage. Much of the work is temporary, although many in the gig economy, such as taxi drivers and delivery people stick with the same job. The gig economy is just one manifestation of the growing flexibility of labour markets, which have also seen a rise in temporary employment, part-time employment and zero-hour contracts.

Working in the gig economy provides a number of benefits for workers. Workers have greater flexibility in their choice of hours and many work wholly or partly from home. Many do several ‘gigs’ simultaneously, which gives variety and interest.

Working in the gig economy provides a number of benefits for workers. Workers have greater flexibility in their choice of hours and many work wholly or partly from home. Many do several ‘gigs’ simultaneously, which gives variety and interest.

In terms of economic theory, this flexibility gives workers a greater opportunity to work the optimal amount of time. This optimum involves working up to the point where the marginal benefit from work, in terms of pay and enjoyment, equals the marginal cost, in terms of effort and sacrificed leisure.

For firms using people from the gig economy, it has a number of advantages. They are generally cheaper to employ, as they do not need to be paid sick pay, holiday pay or redundancy; they are not entitled to parental leave; there are no employers’ national insurance contributions to pay (which are at a rate of 13.8% for employers); the minimum wage does not apply to such workers as they are not paid a ‘wage’. Also the firm using such workers has greater flexibility in determining how much work individuals should do: it chooses the amount of service it buys in a similar way that consumers decide how much to buy.

Many of these advantages to firms are disadvantages to the workers in the gig economy. Many have little bargaining power, whereas many firms using their services do. It is not surprising then that the Chancellor’s announcement of a 2 percentage point rise in NICs for such people has met with such dismay by the people affected. They will still pay less than employed people, but they claim that this is now not enough to compensate for the lack of benefits they receive from the state or from the firms paying for their services.

Many of these advantages to firms are disadvantages to the workers in the gig economy. Many have little bargaining power, whereas many firms using their services do. It is not surprising then that the Chancellor’s announcement of a 2 percentage point rise in NICs for such people has met with such dismay by the people affected. They will still pay less than employed people, but they claim that this is now not enough to compensate for the lack of benefits they receive from the state or from the firms paying for their services.

Some of the workers in the gig economy can be seen as budding entrepreneurs. If you have a specialist skill, you may use working in the gig economy as the route to setting up your own business and employing other people. A self-employed plumber may set up a plumbing company; a management consultant may set up a management consultancy agency. Another criticism of the rise in Class 4 NICs is that this will discourage such budding entrepreneurs and have longer-term adverse supply-side effects on the economy.

As far as the government is concerned, there is a worry about people moving from employment to self-employment as it tends to reduce tax revenues. Not only will considerably less NIC be paid by previous employers, but the scope for tax evasion is greater in self-employment. There is thus a trade-off between the extra output and small-scale investment that self-employment might bring and the lower NIC/tax revenue for the government.

As far as the government is concerned, there is a worry about people moving from employment to self-employment as it tends to reduce tax revenues. Not only will considerably less NIC be paid by previous employers, but the scope for tax evasion is greater in self-employment. There is thus a trade-off between the extra output and small-scale investment that self-employment might bring and the lower NIC/tax revenue for the government.

Articles

Thriving in the gig economy Philippine Daily Inquirer, Michael Baylosis (10/3/17)

6 charts that show how the ‘gig economy’ has changed Britain – and why it’s not a good thing Business Insider, Ben Moshinsky (21/2/17)

What is the ‘gig’ economy? BBC News, Bill Wilson (10/2/17)

Great Freelance, Contract and Part-Time Jobs for 2017 CareerCast (10/3/17)

We have the laws for a fairer gig economy, we just need to enforce them The Guardian, Stefan Stern (7/2/17)

The gig economy will finally have to give workers the rights they deserve Independent, Ben Chu (12/2/17)

Gig economy chiefs defend business model BBC News (22/2/17)

Spring Budget 2017 tax rise: What’s the fuss about? BBC News, Kevin Peachey (9/3/17)

Self-employed hit by national insurance hike in budget The Guardian, Simon Goodley and Heather Stewart (8/3/17)

What national insurance is – and where it goes The Conversation, Jonquil Lowe (10/3/17)

Britain’s tax raid on gig economy misses the mark Reuters, Carol Ryan (9/3/17)

Economics collides with politics in Philip Hammond’s budget The Economist (9/3/17)

UK government publications

Contract types and employer responsibilities – 5. Freelancers, consultants and contractors GOV.UK

Spring Budget 2017 GOV.UK (8/3/17)

Spring Budget 2017: documents HM Treasury (8/3/17)

National Insurance contributions (NICs) HMRC and HM Treasury (8/3/17)

Questions

- Give some examples of work which is generally or frequently done in the gig economy.

- What are the advantages and disadvantages to individuals from working in the gig economy?

- What are the advantages and disadvantages to firms from using the services of people in the gig economy rather than employing people?

- In the case of employed people, both the employees and the employers have to pay NICs. Would it be fair for both such elements to be paid by self-employed people on their own income?

- Discuss ways in which the government might tax the firms which buy the services of people in the gig economy.

- How does the rise of the gig economy affect the interpretation of unemployment statistics?

- What factors could cause a substantial growth in the gig economy over the coming years?

Many of you reading the articles on this website will be just about to start, or will have just started, studying economics at university. For some of you this will involve building on the knowledge you obtained prior to university, whereas for others it will be the first time you have ever studied the subject before. Will studying economics change the way you behave? Should it come with a health warning?

Many of you reading the articles on this website will be just about to start, or will have just started, studying economics at university. For some of you this will involve building on the knowledge you obtained prior to university, whereas for others it will be the first time you have ever studied the subject before. Will studying economics change the way you behave? Should it come with a health warning?

Can studying economics change the way you think and behave? The subject is often sold to prospective students on the grounds that it can. For example it is stated on the Economics Network’s Why Study Economics? website that

The economic way of thinking can help us make better choices

However, is it possible that studying economics could change people’s behaviour in a way that would be to the detriment of society? Some observers have argued that it can. They have suggested that students might be influenced by some of the assumptions that are made in traditional economic theory.

As social scientists, economists are always trying to analyse human behaviour. However, people vary in many different ways and have very diverse preferences. If we want to build a theory that predicts how people will behave and respond in different situations, then some type of simplifying assumptions are inevitable.

Traditionally one of the key simplifying assumptions that economists have used in their theories of human behaviour is that people make decisions in their own self-interest. There is some debate about exactly what self-interest means. For example it could be argued that giving £10 to charity is acting in your own self-interest if it gives you more pleasure than spending that £10 on yourself. However, in many of the economic theories that you first study in economics a narrow meaning of self-interest tends to be used. This is clearly illustrated by the following quote from Milgrom and Roberts. Referring to economic theory they state that:

It is often assumed that people behave as if they were entirely motivated by narrow, selfish concerns

It is important to make it clear that economists are not assuming that people behave in a selfish manner all of the time. Instead, they are assuming that the people in their theories are acting in a selfish manner. The value of making this assumption is whether the predictions about human behaviour that follow from using it are supported by evidence from the real world.

Some researchers have argued that when people study economic theory built on this assumption it makes them more likely to behave in a selfish way. The evidence for this comes from a range of research papers. Here are some findings:

Economics students were more likely than those studying other subjects to recommend the most expensive plumber to a student society if that plumber offered the student a side payment.

Students took part in an experiment in a computer room where they could either keep the money they had been given or donate it to a public good. On average the economics students kept more of the money.

Economics professors gave less money to charity than professors of other subjects such as psychology and sociology.

Some studies also found that selfish people were more likely to choose economics as a subject to study and became more selfish after they had studied it for some time.

If you are about to begin your study of economics then perhaps you should take care that your behaviour outside the classroom is not being unduly influenced by some of the assumptions you are learning about inside the classroom. On a more practical note perhaps you should avoid sharing a restaurant bill or buying rounds of drinks when in the company of other economists!!!

However on a brighter note, the evidence in these papers can be interpreted in a number of different ways. There are even some studies that found economics students were less selfish than those on other courses.

Re-Post: Does Studying Economics Make You Selfish? The Splintered Mind (21/11/12)

Does studying economics make you more selfish? BBC (22/10/13)

Does Studying Economics Breed Greed? Huffington Post (22/10/13)

The Dismal Education The New York Times (16/12/11)

Does Economics Make You a Bad Person? Conversable Economist (31/3/14)

Economists aren’t all bad FT Magazine (11/4/14)

Questions

- What is an economic model? Why is it necessary to make simplifying assumptions?

- How are economic models judged? How important is it for the assumptions to accurately describe the real world?

- Try to find some jokes that have been made about the use of assumptions in economic theory.

- Can you think of any alternative explanations for the results found in the research papers referred to in the case?

- Try to find a research paper that finds evidence that economics students are less selfish than other students.

- What is a public good? Explain why someone with selfish preferences would not contribute to the public good.

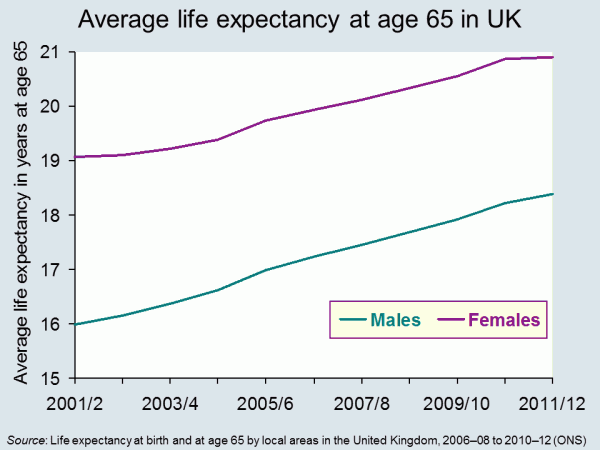

Life expectancy is increasing across the world and the latest set of figures from the Office for National Statistics show that in the UK it has passed 79 for boys born in 2010–12, and 82 for girls born then. In fact the prediction is that over a third of babies born in 2013 will live to more than 100. The data throws up some interesting questions. How well prepared are we for lives that last this long? And how evenly distributed is this increase in life expectancy? Pensions’ minister, Steve Webb, has called for better information on life expectancy to be shared. How would this impact on our decision making?

Life expectancy is increasing across the world and the latest set of figures from the Office for National Statistics show that in the UK it has passed 79 for boys born in 2010–12, and 82 for girls born then. In fact the prediction is that over a third of babies born in 2013 will live to more than 100. The data throws up some interesting questions. How well prepared are we for lives that last this long? And how evenly distributed is this increase in life expectancy? Pensions’ minister, Steve Webb, has called for better information on life expectancy to be shared. How would this impact on our decision making?

It seems reasonable to think that increasing life expectancy must be good news. And of course, for individuals it can be. In 1951 the average man retiring at 65, in England and Wales, could expect to live and draw a pension for another 12.1 years. By 2014 this had risen to 22 years.

But while we can look forward to longer life, for the government, it presents some challenges The first is that we just don’t save enough for our old age. This seems to be partly because we find it hard to make decisions that will have an impact so far in the future. There are a number of measures that have been put in place to encourage us to save more, including auto-enrolment into company pension schemes. This is being rolled out across businesses over the next three years. In the 2014 Budget, the Chancellor announced that people reaching retirement age will be able to draw all their pension as a cash lump sum, rather than having to take it as a regular income.

But while we can look forward to longer life, for the government, it presents some challenges The first is that we just don’t save enough for our old age. This seems to be partly because we find it hard to make decisions that will have an impact so far in the future. There are a number of measures that have been put in place to encourage us to save more, including auto-enrolment into company pension schemes. This is being rolled out across businesses over the next three years. In the 2014 Budget, the Chancellor announced that people reaching retirement age will be able to draw all their pension as a cash lump sum, rather than having to take it as a regular income.

Another concern for government is the variations that we find in life expectancy across the UK. The 2014 ONS data identified that life expectancy for men born in Glasgow in 2012 is 72.6, in East Dorset it is 82.9. 25% of those in Glasgow are not expected to live to 65. The gap in years of good health is even greater. This presents governments with a long-term problem. How do they achieve greater equality in this instance? Do they focus resources on the areas that need it most? Do they legislate to address behaviour? Or do they rely on the provision of good advice – on diet, exercise and other factors?

Information has a role to play in both areas identified above. In April 2014, Steve Webb, suggested that in order to make good decisions at the point of retirement, people need to understand more about what lies ahead. He said:

People tend to underestimate how long they’re likely to live, so we’re talking about averages, something very broad-brush. Based on your gender, based on your age, perhaps asking one or two basic questions, like whether you’ve smoked or not, you can tell somebody that they might, on average, live for another 20 years or so.

This suggestion has led to some concerns being expressed at what appears to be an over-simplistic approach. Estimates can only be based on a mix of averages modified by individual information. Would the projections be shared with pension providers? What would you do if you exceeded your forecast life expectancy – by a long way – and had spent all your money? Could you sue someone?

Will your pension pot last as long as you will? The Telegraph, Dan Hyde and Richard Dyson (23/4/2014)

Scientists invent death test that will tell us how long we have to live Metro (11/8/13)

Games host Glasgow has worst life expectancy in the UK The Guardian, Caroline Davies (16/4/2014)

Pensioners could get life expectancy guidance BBC News Politics (17/4/14)

ONS reveals gaps in life expectancy across the UK FT Adviser Pensions, Kevin White (23/4/14)

Health care aid for developing countries boosts life expectancy Health Canal, Ruth Ann Richter (22/4/14)

A third of babies born this year will live to 100 This is Money.co.uk, Adam Uren (11/12/13)

Questions

- Thinking about the UK, what are the factors that might explain variations in life expectancy across different regions? How might the government address these differences? Why would they want to do so?

- Do the same factors explain variations between countries? Who can address these differences? Who would want to do so?

- If you could have a reasonable prediction of your life expectancy at 65, would you want it? How would your behaviour change if you were predicted a longer than average life expectancy? How would it change if you were predicted a shorter than average life expectancy?

- If you could have an accurate prediction of your life expectancy at 18, how would your answers differ? If this were possible, would it present any problems?

How important are emotions when you go shopping? Many people go shopping when they ‘need’ to buy something, whether it be a new outfit, food/drink, a new DVD release, a gift, etc. Others, of course, simply go window shopping, often with no intention of buying. However, everyone at some point has made a so-called ‘impulse’ purchase.

How important are emotions when you go shopping? Many people go shopping when they ‘need’ to buy something, whether it be a new outfit, food/drink, a new DVD release, a gift, etc. Others, of course, simply go window shopping, often with no intention of buying. However, everyone at some point has made a so-called ‘impulse’ purchase.

There is only one article below, which is from the BBC and draws on data released from the National Employment Savings Trust’s survey. This report suggests that British people spend over £1 billion every year on impulse buys – purchases that are not needed, were not intended and are often regretted once the ‘high’ has worn off. Often, it is the way in which a product is advertised or positioned that leads to a spontaneous purchase – seeing chocolate bars/sweets at the tills; a product offered at a huge discount advertised in the window of a shop; 2 for 1 purchases; points for loyalty etc. All of these and more are simple techniques used by retailers to encourage the impulse buy. As consumer psychologist, Dr. James Intriligator says:

Retailers have clever ways of manipulating customers to spend more but if you stick to your plans you can avoid being affected by their tactics.

In other cases, it’s simply the frame of mind of the consumer that can lead to such purchases, such as being hungry when you’re food shopping or having an event to attend the next day and deciding to go window shopping, despite already having something to wear! Dr. Intriligator continues, saying:

Your ability to resist and make rational choices is diminished when your glucose levels are down … When you get irrational, you fall back on trusted brands, which often leads you to spend more money … Later in the shop, you’re more tired and less likely to resist [impulse buys]

But are such purchases irrational? One of the key assumptions made by economists (at least in traditional economics) is that consumers are rational. This implies that consumers weigh up marginal costs and benefits when making a decision, such as deciding whether or not to purchase a product. But, do impulse buys move away from this rational consumer approach? Is buying something because it makes you happy in the short term a rational decision? Behavioural economics is a relatively new ‘branch’ of economics that takes a closer look at the decisions of consumers and what’s behind their behaviour. The following article from the BBC considers the impulse buy and leaves you to consider the question of irrational consumers.

Article

How to stop buying on impulse BBC Consumer (30/5/13)

Questions

- If the marginal benefit of purchasing a television outweighs the marginal cost, what is the rational response?

- Using the concept of marginal cost and benefit, illustrate them on a diagram and explain how equilibrium should be reached.

- What is behavioural economics?

- What are the key factors that can be used to explain impulse buys?

- How can framing help to explain irrational purchases?

- If a product is advertised at a significant discount, what figure for elasticity is it likely to have to encourage further purchases in-store?

- Is bulk-buying always a bad thing?