This rather strange question has been central to a storm that has been brewing between various celebrity chefs, including Jamie Oliver and Hugh Fearnley-Whittingstall, and the supermarkets. Supermarkets say that consumers don’t want irregular shaped vegetables, such as carrots, parsnips and potatoes. ‘Nonsense’, say their critics.

This rather strange question has been central to a storm that has been brewing between various celebrity chefs, including Jamie Oliver and Hugh Fearnley-Whittingstall, and the supermarkets. Supermarkets say that consumers don’t want irregular shaped vegetables, such as carrots, parsnips and potatoes. ‘Nonsense’, say their critics.

At the centre of the storm are the farmers, who find a large proportion of their vegetables are rejected by the supermarkets. And these are vegetables which are not damaged or bad – simply not of the required shape. Although these rejected vegetables have been described as ‘wonky’, in fact many are not wonky at all, but simply a little too large or too small, or too short or too long. Most of these vegetables are simply wasted – ploughed back into the ground, or at best used for animal feed.

And it’s not just shape; it’s colour too. Many producers of apples find a large proportion being rejected because they are too red or not red enough.

But do consumers really want standardised fruit vegetables? Are the supermarkets correct? Are they responding to demand? Or are they attempting to manipulate demand?

But do consumers really want standardised fruit vegetables? Are the supermarkets correct? Are they responding to demand? Or are they attempting to manipulate demand?

Supermarkets claim that they are just responding to what consumers want. Their critics say that they are setting ludicrously rigid cosmetic standards which are of little concern to consumers. As Hugh Fearnley-Whittingstall states:

‘It’s only when you see the process of selection on the farm, how it has been honed and intensified, it just looks mad. There are many factory line systems where you have people looking for faults on the production line; in this system you’re looking for the good ones.

What we’re asking supermarkets to do is to relax their cosmetic standards for the vegetables that all get bagged up and sold together. It’s about slipping a few more of the not-so-perfect ones into the bag.’

In return, consumers must be prepared to let the supermarkets know that they are against these cosmetic standards and are perfectly happy to buy slightly more irregular fruit and vegetables. Indeed, this is beginning to happen through social media.  The pressure group 38 degrees has already taken up the cause.

The pressure group 38 degrees has already taken up the cause.

But perhaps consumers ‘voting with their feet’ is what will change supermarkets’ behaviour. With the rise of small independent greengrocers, many from Eastern Europe, there is now intense competition in the fruit and vegetables market in many towns and cities. Perhaps supermarkets will be forced to sell slightly less cosmetically ‘perfect’ produce at a lower price to meet this competition.

Videos

Hugh’s War on Waste Episode 1 BBC on YouTube, Hugh Fearnley-Whittingstall (2/11/15)

Hugh’s War on Waste Episode 1 BBC on YouTube, Hugh Fearnley-Whittingstall (2/11/15)

Hugh’s War on Waste Episode 2 BBC on YouTube, Hugh Fearnley-Whittingstall (9/11/15)

Articles

Hugh Fearnley-Whittingstall rejects Morrisons’ ‘pathetic’ wonky veg trial The Guardian, Adam Vaughan (9/11/15)

Jamie Oliver leads drive to buy misshapen fruit and vegetables The Guardian, Rebecca Smithers (1/1/15)

Hugh Fearnley-Whittingstall’s war over wonky parsnips The Telegraph, Patrick Foster (30/10/15)

Asda extends ‘wonky’ fruit and veg range Resource, Edward Perchard (4/11/15)

Wearne’s last farmer shares memories and laments loss of farming community in Langport area Western Gazette, WGD Mumby (8/11/15)

Viewpoint: The rejected vegetables that aren’t even wonky BBC News Magazine (28/10/15)

Viewpoint: The supermarkets’ guilty secret about unsold food BBC News Magazine (6/11/15)

Questions

- What market failures are there is the market for fresh fruit and vegetables?

- Supermarkets are oligopsonists in the wholesale market for fruit and vegetables. What is the implication of this for (a) farmers; (b) consumers?

- Is there anything that (a) consumers and (b) the government can do to stop the waste of fruit and vegetables grown for supermarkets?

- How might supermarkets estimate the demand for fresh fruit and vegetables and its price elasticity?

- What can supermarkets do with unsold food? What incentives are there for supermarkets not to throw it away but to make good use of it?

- Could appropriate marketing persuade people to be less concerned about the appearance of fruit and vegetables? What form might this marketing take?

The recent low price of oil has been partly the result of faltering global demand but mainly the result of increased supply from shale oil deposits. The increased supply of shale oil has not been offset by a reduction in OPEC production. Quite the opposite: OPEC has declared that it will not cut back production even if the price of oil were to fall to $30 per barrel.

The recent low price of oil has been partly the result of faltering global demand but mainly the result of increased supply from shale oil deposits. The increased supply of shale oil has not been offset by a reduction in OPEC production. Quite the opposite: OPEC has declared that it will not cut back production even if the price of oil were to fall to $30 per barrel.

We looked at the implications for the global economy in the post, A crude indicator of the economy (Part 2). We also looked at the likely effect on oil prices over the longer term and considered what the long-run supply curve might look like. Here we examine the long-run effect on prices in more detail. In particular, we look at the arguments of two well-known commentators, Jim O’Neill and Anatole Kaletsky, both of whom have articles on the Project Syndicate site. They disagree about what will happen to oil prices and to energy markets more generally in 2015 and beyond.

Jim O’Neill argues that with shale oil production becoming unprofitable at the low prices of late 2014/early 2015, the oil price will rise. He argues that a good indicator of the long-term equilibrium price of oil is the five-year forward price, which is much less subject to speculation and is more reflective of the fundamentals of demand and supply. The five-year forward price is around $80 per barrel – a level to which O’Neill thinks oil prices are heading.

Anatole Kaletsky disagrees. He sees $50 per barrel as a more likely long-term equilibrium price. He argues that new sources of oil have made the oil market much more competitive. The OPEC cartel no longer has the market power it had from the mid 1970s to the mid 1980s and from the mid 2000s, when surging Chinese demand temporarily created a global oil shortage and strengthened OPEC’s control of prices. Instead, the current situation is more like the period from 1986 to 2004 when North Sea and Alaskan oil development undermined OPEC’s power and made the oil market much more competitive.

Anatole Kaletsky disagrees. He sees $50 per barrel as a more likely long-term equilibrium price. He argues that new sources of oil have made the oil market much more competitive. The OPEC cartel no longer has the market power it had from the mid 1970s to the mid 1980s and from the mid 2000s, when surging Chinese demand temporarily created a global oil shortage and strengthened OPEC’s control of prices. Instead, the current situation is more like the period from 1986 to 2004 when North Sea and Alaskan oil development undermined OPEC’s power and made the oil market much more competitive.

Kaletsky argues that in a competitive market, price will equal the marginal cost of the highest cost producer necessary to balance demand and supply. The highest cost producers in this case are the shale oil producers in the USA. As he says:

Under this competitive logic, the marginal cost of US shale oil would become a ceiling for global oil prices, whereas the costs of relatively remote and marginal conventional oilfields in OPEC and Russia would set a floor. As it happens, estimates of shale-oil production costs are mostly around $50, while marginal conventional oilfields generally break even at around $20. Thus, the trading range in the brave new world of competitive oil should be roughly $20 to $50.

So who is right? Well, we will know in twelve months or more! But, in the meantime, try to use economic analysis to judge the arguments by answering the questions below.

The Price of Oil in 2015 Project Syndicate, Jim O’Neill (7/1/15)

A New Ceiling for Oil Prices Project Syndicate, Anatole Kaletsky (14/1/15)

Questions

- For what reasons might the five-year forward price of oil be (a) a good indicator and (b) a poor indicator of the long-term price of oil?

- Under O’Neill’s analysis, what would the long-term supply curve of oil look like?

- Are shale oil producers price takers? Explain.

- Draw a diagram showing the marginal and average cost curves of a swing shale oil producer. Put values on the vertical axis to demonstrate Kaletsky’s arguments. Also put average and marginal revenue on the diagram and show the amount of profit at the maximum-profit point.

- Why are shale oil producers likely to have much higher long-run average costs than short-run variable costs? How does this affect Kaletsky’s arguments?

- Under Kaletsky’s analysis, what would the long-term supply curve of oil look like?

- Criticise Kaletsky’s arguments from O’Neill’s point of view.

- Criticise O’Neill’s arguments from Kaletsky’s point of view.

- Will OPEC’s policy of not cutting back production help to restore its position of market power?

- Why might the fall in the oil price below $50 in early 2015 represent ‘overshooting’? Why does overshooting often occur in volatile markets?

The market structure in which firms operate has important implications for prices, products, suppliers and profits. In competitive markets, we expect to see low prices, many firms competing with new innovations and firm behavior that is in, or at least not against the public interest. As a firm becomes dominant in a market, its behavior is likely to change and consumers and suppliers can be adversely affected. Is this the case with Amazon?

The market structure in which firms operate has important implications for prices, products, suppliers and profits. In competitive markets, we expect to see low prices, many firms competing with new innovations and firm behavior that is in, or at least not against the public interest. As a firm becomes dominant in a market, its behavior is likely to change and consumers and suppliers can be adversely affected. Is this the case with Amazon?

Much attention has been given to the dispute centering around Amazon and its actions in the market for e-books, where it holds close to two thirds of the market share. Critics of Amazon suggest that this is just one example of Amazon using its monopoly power to exploit consumers and suppliers, including the publishers and their authors. Although Amazon is not breaking any laws, there are suggestions that its behavior is ‘brutal’ and is taking advantage of consumers, suppliers and its workforce.

But rather than criticizing the actions of a monopolist like Amazon, should we instead be praising the company and its ability to compete other firms out of the market? One of the main reasons why consumers use Amazon to buy goods is that prices are cheap. So, in this respect, perhaps Amazon is not acting against consumers’ interests, as under a monopoly we typically expect low output and high prices, relative to a model of perfect competition. The question of the methods used to keep prices so low is another matter. Two conflicting views on Amazon can be seen from Annie Lowrey and Franklin Foer, who respectively said:

“Amazon relentlessly drives down prices for goods and services and delivers them fast and cheap. It ploughs its profits into price cuts and innovation rather than putting them in the hands of its investors. That benefits millions of families – full stop.”

“In effect, we’ve been thrust back 100 years to a time when the law was not up to the task of protecting the threats to democracy posed by monopoly; a time when the new nature of the corporation demanded a significant revision of government.”

So, with Amazon we have an interesting case of a monopolist, where many aspects of its behaviour fit exactly into the mould of the traditional monopolist. But, some of the outcomes we observe indicate a more competitive market. Paul Krugman has been relatively blunt in his opinion that Amazon’s dominance is bad for America. His comments are timely, given the recognition for Jean Tirole’s work in considering the problems faced when trying to regulate any firm that has significant market power. He has been awarded the Nobel Prize in Economics. I’ll leave you to decide where you place this company on the traditional spectrum of market structures, as you read the following articles.

Amazon: Monopoly or capitalist success story? BBC News, Kierran Petersen (14/10/14)

Why the Justice Department won’t go after Amazon, even though Paul Krugman thinks it’s hurting America Business Insider, Erin Fuchs (20/10/14)

Is Amazon a monopoly? The Week, Sergio Hernandez (19/11/14)

Big, bad Amazon The Economist (20/10/14)

Questions

- What are the typical characteristics of a monopoly? To what extent does Amazon fit into this market structure?

- Why does Paul Krugman suggest that Amazon is hurting America?

- How does Amazon’s behaviour with regard to (a) its suppliers and (b) its workers affect its profitability? Would it be able to behave in this way if it were a smaller company?

- Why is Amazon able to charge its customers such low prices? Why does it do this, given its market power?

- Is there an argument for more regulation of firms with such dominance in a market, as is the case with Amazon?

- The debate over e-books is ingoing. What is the argument for publishers to be able to set a minimum price? What is the argument against this?

- Should customers boycott Amazon in a protest over the alleged working conditions of Amazon factory employees?

Merlin Entertainments PLC is one of the largest operator of visitor attractions in the world and owns over a third of the most popular theme parks in Europe. It runs the four most visited parks in England – Alton Towers, Legoland Windsor, Thorpe Park and Chessington World of Adventures as well as the most popular theme park in Italy – Gardaland. Alton Towers alone had 2.5 million visitors in 2013. Anybody thinking of going to one of these attractions is faced with a wide range of different entry fees .

Merlin Entertainments PLC is one of the largest operator of visitor attractions in the world and owns over a third of the most popular theme parks in Europe. It runs the four most visited parks in England – Alton Towers, Legoland Windsor, Thorpe Park and Chessington World of Adventures as well as the most popular theme park in Italy – Gardaland. Alton Towers alone had 2.5 million visitors in 2013. Anybody thinking of going to one of these attractions is faced with a wide range of different entry fees .

Theme parks and tourist attractions have market power so their owners have to make some interesting pricing decisions. They have to tackle the same dilemma that confronts any seller that faces a downward sloping demand curve for its goods/services.

One option for the firm would be to increase the entry fee. This would produce higher profits per visitor as some of the surplus from the transaction previously enjoyed by the consumer will be extracted by the seller and converted into producer surplus. Unfortunately for the business the higher price, all other things equal, will also result in fewer visitors. Some people will be deterred from visiting because of the higher price and the seller will lose out on potential revenue.

An alternative strategy would be for the theme park to reduce its entry fee. All other things equal, this will increase the number of visitors. However, it would also mean that the profit per customer would fall. The frustrating issue for the seller is that some of its customers, who would still have visited the attraction at the higher price, are now able to get a better deal.

This dilemma exists if the seller has to charge all of its different customers the same entry fee. If it could charge a higher entry fee to those customers who would be willing to pay more and a lower entry fee to those who would be willing to pay less then it could make more money. Extra revenue could be obtained from those additional sales that take place at the lower price while more consumer surplus could be extracted from those still paying the higher price.

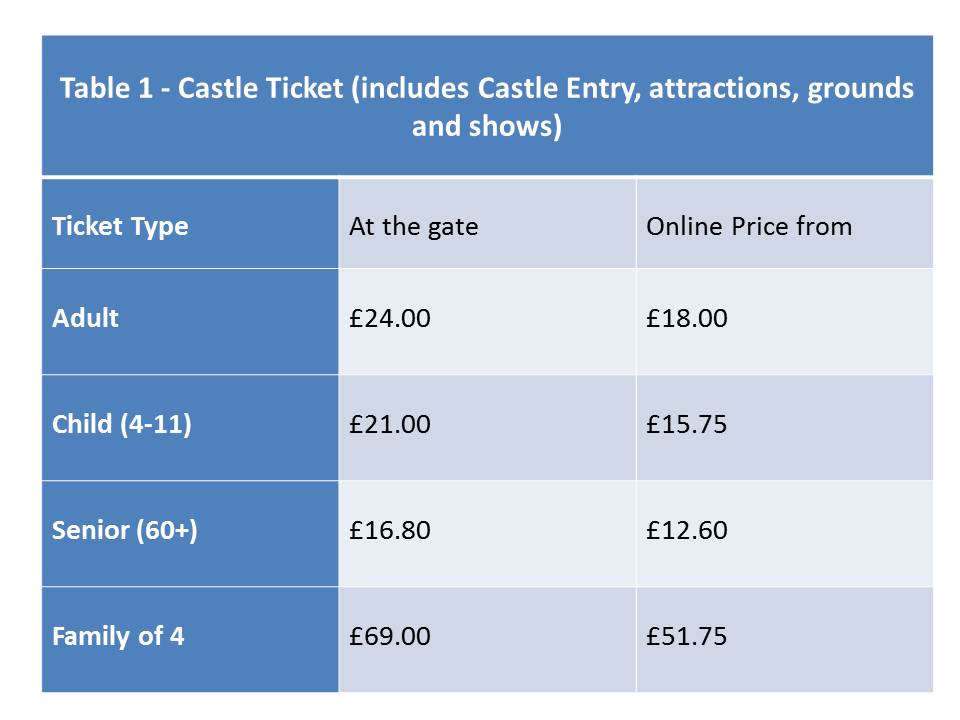

Is it possible for a firm to charge different prices to different customers for the same or a similar good or service? Table 1 below shows the entry fees for Warwick Castle, another tourist attraction owned by Merlin Entertainments PLC.

It can immediately be seen from this table that some groups of customers pay a different entry fee from others. For example adults have to pay £24 to enter on the day while people aged 60 and over pay a lower price £16.80. The entry fee for children aged between 4 and 11 is £21.00 while those aged 3 and under go for free. Students aged 16-18 can gain entry for a price of £13.50 if they can provide valid ID and purchase the tickets from the visitbritainshop website.

In this example, the company has allocated people into different categories by age (i.e. senior, adult, student, older children and younger children) and has set the entry fee that customers in each group have to pay.

The table also shows that if customers purchase on- line then they can get the tickets more cheaply. The entry fee for each category is 25% lower if the ticket is booked seven days in advance i.e. the prices shown in the last column in the table. If the booking is made between 2-6 days in advance then the discount is only 10% i.e. an adult ticket would cost £21.60. The on-line discounts are open to everyone. People are given the choice to either book on-line in advance or pay on the day. This is different from a situation where you are placed into a category by the firm. For example the customer cannot choose whether they are over 60!

If people are prepared to spend more time searching on the internet then other cheaper prices can also be obtained. Once again these offers are open to anyone willing to spend the time and effort in order to find them.

All the ticket prices above give people access to exactly the same attractions on the day. They do not give the visitor access to two of the attractions at the castle – the Dragon Tower and Castle Dungeon. Entry to the Dragon Tower would cost an adult on the day an extra £1.80 while entry to the Castle Dungeon would cost an extra £5.40.

Warwick Castle Ticket Prices Warwick Castle (accessed on 04/09/14)

Alton Towers Alton Towers (accessed on 08/09/14)

Warwick Castle Tickets visitbritainshop (accessed on 02/09/14)

Global Attractions Attendance Report teaconnect (accessed on 05/09/14)

Merlin Entertainments Merlin Entertainments (accessed on 08/09/14)

Questions

- What pricing decisions do firms have to make if they operate in a perfectly competitive market?

- Explain why an individual tourist attraction will have a downward sloping demand curve

- Paying an entry fee and an extra payment per attraction is known as what type of pricing? What advantages does this type of price strategy have for the seller?

- How would you calculate the profit per customer? What factors other than the entrance fee would determine the profit made per customer in a theme park or tourist attractions?

- Paying a different price depending on which category you have been assigned to by the seller is known as what type of pricing strategy? Can this type of pricing strategy ever be in the interests of society?

- In the example used in the case, customers are assigned to different categories by age. Can you think of any other ways that firms could categorise their customers?

- Given the category customers have been assigned to they can pay different prices depending on whether they buy the tickets on line. What is the price strategy called when customers can choose from a variety of pricing options for the same or similar product? Can you think of any different methods that could be used by the seller to carry out this type of pricing strategy?

The draw for the lucrative group stages of the Champions League was made on Thursday 28th August. The 32 remaining clubs in the competition were allocated into eight groups of four teams. 74% percent of the respondents to a BBC survey thought that Manchester City had the toughest draw, while only 3.7% thought that Chelsea had the hardest draw. How did the Premier League champions end up in a much tougher group than the teams that finished in 3rd and 4th place? Was it purely by chance?

The draw for the lucrative group stages of the Champions League was made on Thursday 28th August. The 32 remaining clubs in the competition were allocated into eight groups of four teams. 74% percent of the respondents to a BBC survey thought that Manchester City had the toughest draw, while only 3.7% thought that Chelsea had the hardest draw. How did the Premier League champions end up in a much tougher group than the teams that finished in 3rd and 4th place? Was it purely by chance?

The unpredictability of a sporting contest depends not only on differences in the talent/motivation of the participants involved, but also on how the contest is designed and structured. The Champions League is an interesting case. The title of the competition would suggest that the participating clubs are all league champions from the 54 football associations spread across Europe. However, out of the 32 clubs which made it to the group stage, only 18 were actually the champions of their own domestic league.

22 teams automatically qualify for the group stages, while the other ten qualify via a knock-out stage of the competition. Of the 22 teams which gain automatic qualification only thirteen are league champions. The other nine places are allocated to teams which finished either 2nd or 3rd in their domestic leagues.

The inclusion of teams which did not win their domestic league occurs because UEFA allocates places in the Champions League by ranking the sporting performance of the 54 different football associations in Europe. This measure of performance, known as a Country’s Coefficient, is based on the results of the teams from each football association in both the Champions League and Europa League over the previous five years. If UEFA ranks a football association in one of the top three positions, then the teams that finish 1st , 2nd and 3rd in those leagues automatically qualify for the group stage of the Champions League. England is currently ranked in 2nd place behind Spain, which explains why Chelsea, which finished 3rd in the Premier League, obtained automatic qualification. The teams that finished 4th in these three top ranked leagues also gain entry to the final knock-out round of the competition. This is how Arsenal gained qualification for the group stage by narrowly defeating Besiktas from the Turkish League.

Teams from the lower ranked football associations have to win through more knock-out games in order to reach the lucrative group stage. For example the league champions from the bottom six countries (Faroe Islands, Wales, Armenia, Andorra, San Marino and Gibraltar) would have to win through four two-leg knock-out games. The league champions from Scotland would have to win through three as their football association is ranked in 24th place.

A draw takes place in order to allocate the remaining 32 teams to the leagues in the group stages. It is interesting how this allocation occurs because it is not a completely random process. UEFA ranks individual teams as well as countries. Real Madrid is currently ranked in 1st place while Port Talbot Town from the Welsh league is in 449th place. The top eight ranked teams still left in the competition are placed in pot 1, the 9th to 16th ranked clubs are placed in pot 2 and so on. One team from each pot is then drawn out at random and placed in a group. Therefore each group contains one club from pot 1, 1 club from pot 2, 1 club from pot 3 and 1 from pot 4.

The problem for Manchester City is that the seeding of each team is predominately determined by its performance in the Champions and Europa league over the previous five years. Once a team has made it to the group stages, its performance in its own domestic league has no impact on how it is seeded. This means that although Arsenal only finished 4th in the Premier League, it is placed in pot 1 for the draw because of its results in the Champions League over the previous five years. It therefore avoids the other top seeded clubs such as Real Madrid, Barcelona and Bayern Munich. Chelsea is also in pot 1, so was also more likely to get a favourable draw. Manchester City was seeded in pot 2 because it had only been in the Champions League for the last three years, so had not accumulated as many points as the teams who have been in the competition for longer.

Unfortunately for Manchester City, it was drawn in the same group as one of the strongest pot 1 teams – Bayern Munich. It was also unlucky to end up with one of the strongest teams in pot 4. Roma was runners up in the Italian league so was given an automatic place in the group stage. However it received a relatively low seeding as it is the first time it has been in the Champions league since 2010–11.

How much does the seeding matter? Since 1999–2000, when the group stage was expanded to 32 clubs, 86% of the top seeded teams have successfully qualified from the group stage into the last 16. Eleven of the last 16 winners were also from pot 1.

Articles

UEFA Rankings – Club coefficients 2014/15 UEFA (29/8/14)

UEFA Rankings – Country coefficients 2014/15 UEFA (29/8/14)

UEFA Rankings – Coefficients Overview UEFA (29/8/14)

Explained: The UEFA Champions League draw The Indian Empress (28/8/14)

Questions

- Uefa awards ranking points to teams based on their sporting performance. For example teams receive two ranking points for a victory against any team. This is different from the system used to rank national teams where the quality of the team defeated also influences the number of points awarded. What impact would it have if more ranking points were awarded in the Champions League for victories against higher ranked clubs?

- The Uefa system for ranking countries and teams is based on performance in European competitions over the previous 5 years. The performance in each year is weighted equally. What impact might it have if victories from the previous year were more heavily weighted than those from 4 or 5 years ago?

- The draw for the group stages of the Champions League could be made using a completely random process without any seeding. What impact might this have on the amount of money that firms in England, Spain and Italy would be willing to pay to secure the media rights?

- Can you think of any other elements of the design of the tournament that might have an impact on the predictability of the outcome?

This rather strange question has been central to a storm that has been brewing between various celebrity chefs, including Jamie Oliver and Hugh Fearnley-Whittingstall, and the supermarkets. Supermarkets say that consumers don’t want irregular shaped vegetables, such as carrots, parsnips and potatoes. ‘Nonsense’, say their critics.

This rather strange question has been central to a storm that has been brewing between various celebrity chefs, including Jamie Oliver and Hugh Fearnley-Whittingstall, and the supermarkets. Supermarkets say that consumers don’t want irregular shaped vegetables, such as carrots, parsnips and potatoes. ‘Nonsense’, say their critics. The pressure group 38 degrees has already taken up the cause.

The pressure group 38 degrees has already taken up the cause.