When people take out loans they typically do so to spend and with the UK economy in its current state, many would argue that this is a good thing. The ‘payday loan’ industry took advantage of the weak economy and the squeezed households in the UK and for the past few years, we have seen constant adverts that will appeal to many households. But, is the industry as competitive as the adverts would have us believe?

When people take out loans they typically do so to spend and with the UK economy in its current state, many would argue that this is a good thing. The ‘payday loan’ industry took advantage of the weak economy and the squeezed households in the UK and for the past few years, we have seen constant adverts that will appeal to many households. But, is the industry as competitive as the adverts would have us believe?

An inquiry into this industry has been on-going for some time, and it has now been referred to the Competition Commission, due to ‘deep-rooted problems with the way competition works’. For some, a payday loan is a short term form of finance, but for others it has become a way of living that has led to a debt spiral. Frank McKillop, policy manager at Abcul said:

There is a clear demand for instant credit and across the country we are increasingly seeing members who have debts with multiple payday lenders and a record of rolling over debts, or going to one payday lender to clear the debt to another.

One problem identified by the OFT is that customers have found it difficult to compare costs and this has led, in some cases, to customers paying back significantly more than they originally thought. Customers being unable to repay loans will ring warning bells for many people, with no-one wanting a return to the height of the credit crunch.

The OFT has criticized payday loan companies for competing not on costs, but on the speed of approval and using certain unapproved tactics as part of their advertising. The selling point of such companies is that you can have the money in a very short time period. However, the criticism is that this leads to loans being given to those who are unable to afford them. Key credit checks are not being done and with late night texts being sent to often financially vulnerable people, it is no wonder that complaints have been received. In a statement, the OFT said:

The OFT has criticized payday loan companies for competing not on costs, but on the speed of approval and using certain unapproved tactics as part of their advertising. The selling point of such companies is that you can have the money in a very short time period. However, the criticism is that this leads to loans being given to those who are unable to afford them. Key credit checks are not being done and with late night texts being sent to often financially vulnerable people, it is no wonder that complaints have been received. In a statement, the OFT said:

The competitive pressure to approve loans quickly may give firms an incentive to skimp on the affordability assessment which is designed to prevent irresponsible lending and protect consumers.

[the business models of companies were] predicated on making loans which are unaffordable, leading to borrowers paying far more than expected through rollovers, additional interest and other charges.

While payday loans are legal and there are many companies offering them, it is what they are competing over, which seems to be in question. The industry itself has begun to change its practices, providing more information to customers, only allowing loans to be rolled over three times and the potential to freeze repayments if the customer gets into financial difficulty. If more stringent checks are completed and hence timing does not become the only grounds for competition, then the problems above may become less significant. With the ongoing OFT inquiry into the practices of the payday loan industry and the continuing demand for such financing, it is likely that we will see much more of both the good and the bad that it has to offer. The following articles consider the investigation.

Webcasts

Balls warns against payday loans ‘blank cheque’ BBC News (27/6/13)

Balls warns against payday loans ‘blank cheque’ BBC News (27/6/13)

Payday lender investigation could be delayed by bureaucracy Telegraph, Steve Hawkes (27/6/13)

Payday lenders to face ‘tougher restrictions’ on advertising BBC News, Simon Gompertz (1/7/13)

Payday lending rates BBC News, Julio Martino and Stella Creasy (2/7/13)

Articles

Regulator to investigate payday loan industry Financial Times, Elaine Moore and Robert Cookson (27/6/13)

Q&A: Payday loans BBC News (31/5/13)

Payday loans: reining in an industry that is a law unto itself Guardian (27/6/13)

Payday loans industry to face competition inquiry BBC News (27/6/13)

Payday loans firms face competition inquiry Sky News (27/6/13)

Payday loans market faces competition inquiry Guardian, Hilary Osborne (27/6/13)

OFT refers payday loans to Competition Commission Scotsman, Jane Bradley (27/6/13)

Five reasons why we all need to worry about payday lenders Telegraph, Emma Simon (27/6/13)

OFT documents

Payday lending compliance review Office of Fair Trading (27/6/13)

Questions

- Into which market structure would you place the payday loans industry? Make sure you justify your answer.

- What is the role of the (a) the OFT and (b) the Competition Commission? Do these authorities overlap?

- What part does advertising play in this industry?

- To what extent is the payday loan industry a possible cause of another credit crunch?

- Why has the OFT referred this industry to the Competition Commission?

- To what extent are payday loans an essential part of an economy?

If you ask most people whether they like paying tax, the answer would surely be a resounding ‘no’. If asked would you like to pay less tax, most would probably say ‘yes’. Evidence of this can be seen in the behaviour of individuals and of companies, as they aim to reduce their tax bill, through both legal and illegal methods.

If you ask most people whether they like paying tax, the answer would surely be a resounding ‘no’. If asked would you like to pay less tax, most would probably say ‘yes’. Evidence of this can be seen in the behaviour of individuals and of companies, as they aim to reduce their tax bill, through both legal and illegal methods.

Our tax revenues are used for many different things, ranging from the provision of merit goods to the redistribution of income, so for most people they don’t object to paying their way. However, maintaining profitability and increasing disposable income is a key objective for companies and individuals, especially in weak economic times. Some high profile names have received media coverage due to accusations of both tax avoidance and tax evasion. Starbucks, Amazon, Googe and Apple are just some of the big names that have been accused of paying millions of pounds/dollars less in taxation than they should, due to clever (and often legal) methods of avoiding tax.

The problem of tax avoidance has become a bigger issue in recent years with the growth of globalisation. Multinationals have developed to dominate the business world and business/corporation tax rates across the global remain very different. Thus, it is actually relatively easy for companies to reduce their tax burden by locating their headquarters in low tax countries or ensuring that business contracts etc. are signed in these countries. By doing this, any profits are subject to the lower tax rate and are thus such companies are accused of depriving the government of tax revenue. Apple is currently answering questions posed by a US Senate Committee, having been accused of structuring its business to create ‘the holy grail of tax avoidance’.

The problem of tax avoidance has become a bigger issue in recent years with the growth of globalisation. Multinationals have developed to dominate the business world and business/corporation tax rates across the global remain very different. Thus, it is actually relatively easy for companies to reduce their tax burden by locating their headquarters in low tax countries or ensuring that business contracts etc. are signed in these countries. By doing this, any profits are subject to the lower tax rate and are thus such companies are accused of depriving the government of tax revenue. Apple is currently answering questions posed by a US Senate Committee, having been accused of structuring its business to create ‘the holy grail of tax avoidance’.

Many may consider the above and decide that these companies have done little wrong. After all, many schemes aimed at tax avoidance are legal and are often just a clever way of using the system. However, in a business environment dominated by the likes of Google, Apple and Amazon, the impact of tax avoidance may not just be on the government’s coffers. Indeed John McCain, one of the Committee members asked:

…Couldn’t one draw the conclusion that you and Apple have an unfair advantage over domestic based corporations and companies, in other words, smaller companies in this country that don’t have the same ability that you do to locate in Ireland or other countries overseas?

The concern is that with such ability to avoid huge amounts of taxation, large companies will inevitably compete smaller ones out of the market. Local businesses, without the ability to re-locate to other parts of the world, pay their full tax bills, but multinationals legally (in most cases) manage to avoid paying their own share. With a harsh economic climate continuing globally, these large companies that aim to further increase their profitability through such means as tax avoidance will naturally bear the wrath of smaller businesses and individuals that are struggling to get by. It’s likely that this topic will remain in the media for some time. The following articles consider some of the companies accused of participating in tax avoidance schemes and the consequences of doing so.

Is Apple’s tax avoidance rational? BBC News, Robert Peston (21/5/13)

Apple’s Tim Cook defends tax strategy in Senate BBC News (21/5/13)

Senator accuses Apple of ‘highly questionable’ billion-dollar tax avoidance scheme The Guardian, Dominic Rushe (21/5/13)

Apple’s Tim Cook faces tax avoidance questions Sky News (21/5/13)

EU leaders look to end Apple-style tax avoidance schemes Reuters, Luke Baker and Mark John (21/5/13)

Apple Chief Tim Cook defends tax practices and denies avoidance Financial Times, James Politi (21/5/13)

Apple CEO Tim Cook tells Senate: tiny tax bill isn’t our fault, it’s yours Independent, Nikhil Kumar (21/5/13)

Miliband promises action on Google tax avoidance The Telegraph (19/5/13)

Google is cheating British tax payers out of millions…what they are doing is just immoral’: Web giant accused of running ‘scandalous’ tax avoidance scheme by whistleblower Mail Online, Becky Evans (19/5/13)

Multinational CEOs tell David Cameron to rein in tax avoidance rhetoric The Guardian, Simon Bowers, Lawrie Holmes and Rajeev Syal (20/5/13)

Fury at corporate tax avoidance leads to call for a global response The Guardian, Tracy McVeigh (18/5/13)

Questions

- What is the difference between tax evasion and tax avoidance? Is it rational to engage in such schemes?

- What are tax revenues used for?

- Why are multinationals more able to engage in tax avoidance schemes?

- Is the problem of tax avoidance a negative consequence of globalisation?

- How might the actions of large multinationals who are avoiding paying large amounts of tax affect the competitiveness of the global market place?

- Is there justification for a global policy response to combat the issue of tax avoidance?

- What are the costs and benefits to a country of having a low rate of corporation tax?

- How would a more ‘reasonable’ tax on foreign earnings allow the ‘free movement of capital back to the US’?

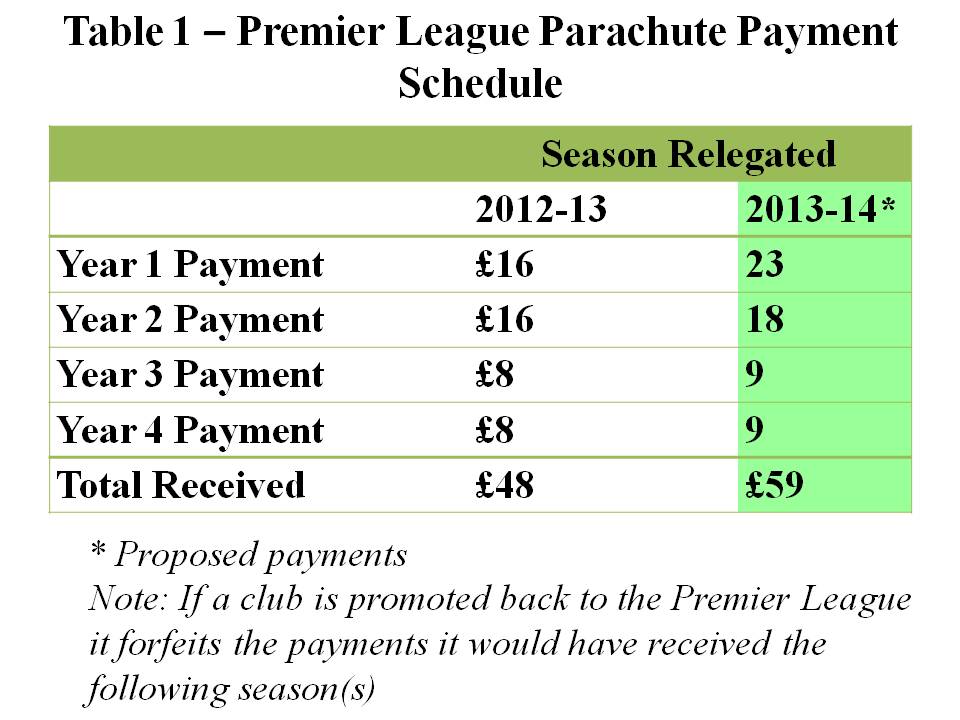

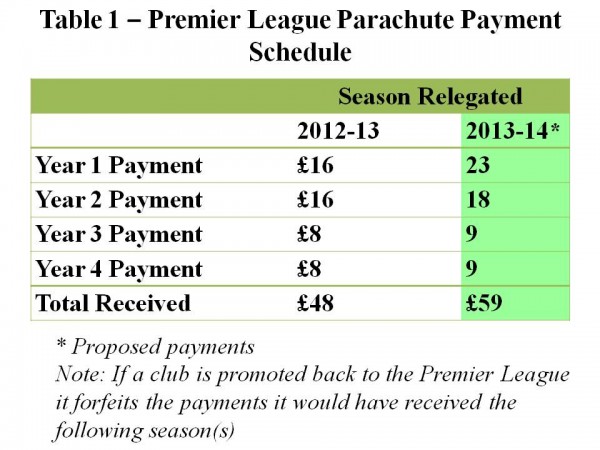

The English Premier League (EPL) has negotiated a record TV deal which will generate £5.5 billion of revenue over the next 3 years – beginning in the season 2013–14. This represents a 70% increase on the previous deal. Controversy has arisen over some initial proposals put forward by the EPL as to how the money will be spent. The owners of the clubs in the Championship of the English Football League (EFL) are particularly concerned about the size of the proposed payments to the three teams relegated from the EPL.

The English Premier League (EPL) has negotiated a record TV deal which will generate £5.5 billion of revenue over the next 3 years – beginning in the season 2013–14. This represents a 70% increase on the previous deal. Controversy has arisen over some initial proposals put forward by the EPL as to how the money will be spent. The owners of the clubs in the Championship of the English Football League (EFL) are particularly concerned about the size of the proposed payments to the three teams relegated from the EPL.

Some 30 years ago the money generated from the sale of television rights was equally shared between all the teams in the then four divisions of the English Football League (EFL). In 1992 the top division of the English Football League broke away and formed the English Premier League (EPL). This newly formed EPL negotiated a separate television deal and kept the majority of the money. However, some payments were and still are made to the teams in the EFL and to organisations such as the League Managers Association and Professional Footballers Association. For example in 2011-–12 the EPL donated £189.4 million of the £1.2 billion generated from that year’s TV deal.

The majority of the money donated by the EPL is spent in two main ways. First, some money is redistributed to all the teams in the EFL: i.e. The Championship, League 1 and League 2. These are known as ‘solidarity payments’ and in 2011–12 the EPL spent £49.8 million on this scheme. Each club in the Championship received £2.3 million. It has been proposed that the amount paid into this scheme should be increased by 5% in the season 2013–14. Second, a relatively large amount of money is paid over a four-year period to the three teams relegated each season from the EPL into the Championship. These are known as ‘parachute payments’ and in the season 2011–12 the EPL spent £90.9 million on this scheme. The rationale for having parachute payments is to help the relegated teams adjust their wage bills to the much lower revenue streams that come from playing in the Championship. Proposed changes to the scheme are outlined in Table 1.

The chairmen of the football league clubs met on the 20th March 2013 and a number of them expressed concerns about the relatively large increase in the parachute payments compared to the solidarity payments. They were particularly concerned that the changes to the funding would damage the competitive balance of the Championship.

The chairmen of the football league clubs met on the 20th March 2013 and a number of them expressed concerns about the relatively large increase in the parachute payments compared to the solidarity payments. They were particularly concerned that the changes to the funding would damage the competitive balance of the Championship.

Competitive balance refers to how the most talented players are distributed amongst the teams in a league. For example, are the majority of the most talented footballers playing for just a couple of the teams? In this case the league is competitively imbalanced and the teams with the best players will tend to win far more games than the other teams. The outcome of the league will be very predictable. If the most talented players were more evenly spread across all the teams in the league, then it would be more competitively balanced. Matches and the outcome of the league would become more unpredictable.

Does the level of competitive balance matter? Some sports economists have argued that it may have a significant impact on the success of the league. This is because fans may value the unpredictability of the results. It follows that closer and more unpredictable results will generate higher match-day attendances and increase the revenues of the clubs.

This is an interesting argument and is the opposite of what economic theory would predict for most markets. For example, the standard prediction would be that as firms outperform their rivals, they generate more revenue and profit. If they manage to drive all their rivals out of business, they would become a pure monopoly and make large abnormal profits. However in professional team sports the outcome may differ significantly. If the unpredictability of the league is highly valued by fans, then teams will generate more revenue when they have strong and evenly matched rivals.

It has been reported that further discussions about the distribution of the money will take place this month with the owners of the championship clubs arguing that there should be smaller increases in parachute payments and much larger increases in solidarity payments. Representatives of the EPL have argued that the parachute payments do not distort competition and make the championship predictable. They point out that at present only one of the top six teams in the championship (Hull) receives parachute payments, while only one of the teams promoted from the Championship in the season 2012–13 (West Ham) received these payments.

Articles

Premier League warned over rich and poor split in wake of TV deal The Guardian, Owen Gibson (19/3/13)

Championship clubs angered by Premier League parachute boost Daily Mail, Charles Sale (6/2/13)

Football league is to lessen the advantage of parachute payments The Guardian, Owen Gibson (20/3/13)

Championship clubs warn Premier League over hike in parachute payments for relegated teams The Independent, Majid Mohamed (20/3/13)

Increased parachute payments could lead to a salary cap in the Championship The Post, A. Stockhausen (21/3/13)

Scudamore:Parachute payment system fair Eurosport, Andy Eckardt (22/3/13)

Parachute payments more than a softened landing The Daisy Cutter, Richard Brook (21/3/13)

Questions

- What factors will influence the size of the attendance at a football match?

- To what extent do you think that the money generated from the sale of television rights should be equally shared between all the clubs in the English Premier League and the English Football League

- Can you think of any ways of measuring the competitive balance of a football league?

- Explain why a very competitively imbalanced league may reduce the revenue for all the clubs in that league?.

- In traditional economic theory it is assumed that firms aim to maximise their profits. What do you think is the objective of a typical football club in the English Premier League?

In 2009, the European Commission investigated Microsoft’s practice of bundling its own browser, Internet Explorer, with new copies of Windows. It found that this was an abuse of market power and created an unfair barrier to entry of other browsers, such as Firefox.

In 2009, the European Commission investigated Microsoft’s practice of bundling its own browser, Internet Explorer, with new copies of Windows. It found that this was an abuse of market power and created an unfair barrier to entry of other browsers, such as Firefox.

An agreement was reached that Microsoft would include a ‘choice screen’ in which users in the EU would be given a full list of alternative browsers and asked which they would like to install. On making their selection, a link would take them to the browser site to download the installation program. This screen would be available until 2014. Between March 2010, when the choice screen was first provided and November of the same year, 84 million browsers were downloaded through it.

In May 2011, however, the screen was no longer present on new Windows 7 purchases. The Commission took some time to realise this: indeed it was Microsoft’s rivals that pointed it out. The screen reappeared some 13 months later, after some 15m copies of Windows software had been sold.

For this lapse, the Commission has just fined Microsoft €561m. Commission Vice President in charge of competition policy, Joaquín Almunia, said:

For this lapse, the Commission has just fined Microsoft €561m. Commission Vice President in charge of competition policy, Joaquín Almunia, said:

In 2009, we closed our investigation about a suspected abuse of dominant position by Microsoft due to the tying of Internet Explorer to Windows by accepting commitments offered by the company. Legally binding commitments reached in antitrust decisions play a very important role in our enforcement policy because they allow for rapid solutions to competition problems. Of course, such decisions require strict compliance. A failure to comply is a very serious infringement that must be sanctioned accordingly.

This may seem unduly harsh, given that Internet Explorer’s share of the browser market has fallen dramatically. In 2009, it had around 50% of the European market, with its main rival at the time, Mozilla’s Firefox, having just under 40%. By 2013, Internet Explorer’s share has fallen to around 24% and Firefox’s to around 29%. Google’s Chrome, which was just starting up in 2009, has seen its share of the European market rise to around 35% and is now the market leader. Partly this is due to the rise in tablets and smartphones, a large proportion of which use Google’s Android operating system and the Chrome browser.

This may seem unduly harsh, given that Internet Explorer’s share of the browser market has fallen dramatically. In 2009, it had around 50% of the European market, with its main rival at the time, Mozilla’s Firefox, having just under 40%. By 2013, Internet Explorer’s share has fallen to around 24% and Firefox’s to around 29%. Google’s Chrome, which was just starting up in 2009, has seen its share of the European market rise to around 35% and is now the market leader. Partly this is due to the rise in tablets and smartphones, a large proportion of which use Google’s Android operating system and the Chrome browser.

Not surprisingly, the European Commission is investigating Google to see whether it is abusing a dominant position. Is Google’s case, it’s not just about its share of the browser market, it’s more about its share of the search market, which in the EU is around 90% (compared with around 65% in the USA). As The Economist article below states:

The Commissioner believes that Google may be favouring its own specialised services (eg, for flights or hotels) at rivals’ expense; that its deals with publishers may unfairly exclude competitors; and that it prevents advertisers from taking their data elsewhere.

Joaquín Almunia asked Google to respond to these concerns by January 31. Google delivered its suggestions on the deadline, but we await to hear precisely what it said and how the Commission will respond. It is understood that Google’s proposal is for clearly labelling its own products on its search engine.

Articles

Microsoft Fined $732 Million By EU Over Browser eWeek, Michelle Maisto (6/3/13)

Microsoft faces hefty EU fine The Guardian (6/3/13)

Sin of omission The Economist (9/3/13)

Microsoft fined by European Commission over web browser BBC News (6/3/13)

EU commissioner Joaquin Almunia announces Microsoft fine BBC News (6/3/13)

Microsoft’s European Fine Comes in an Era of Browser Diversity Forbes, J.P. Gownder (6/3/13)

Life after Firefox: Can Mozilla regain its mojo? BBC News, Dave Lee (11/4/12)

Google responds to European commission’s antitrust chief The Guardian, Charles Arthur (31/1/13)

Google May Clinch EU Settlement After ‘Summer,’ Almunia Says Bloomberg Businessweek, Stephanie Bodoni and Aoife White (22/2/13)

European Commission Press Release

Antitrust: Commission fines Microsoft for non-compliance with browser choice commitments Europa (6/3/13)

Questions

- Why did Microsoft’s share of the browser market continue to decline between May 2011 and June 2012?

- Why would it matter if Microsoft had market power in the browser market, given that it’s free for anyone to download a browser?

- In what ways might Google be abusing a dominant position in the market?

- Can Mozilla regain its mojo?

- According to the second Guardian article, the Microsoft-backed lobby group Icomp said “To be seen as a success, any settlement must … include specific measures to restore competition and allow other parties to compete effectively on a level playing field with Google in the key markets of search and search advertising.” Give examples of such measures and assess how successful they might be.

- Would “clearly labelling its own products on its search engine” be enough to ensure adequate competition?

The Big Four are well known: Deloitte, Ernst and Young, KPMG and PWC. They act as auditors for 90% of the UK’s stock-market listed companies. They have a very close relationship with the companies that they audit and because of this have faced criticism of not warning of the financial crisis. A further accusation is that the relationship between auditors and managers has become blurred.

The Big Four are well known: Deloitte, Ernst and Young, KPMG and PWC. They act as auditors for 90% of the UK’s stock-market listed companies. They have a very close relationship with the companies that they audit and because of this have faced criticism of not warning of the financial crisis. A further accusation is that the relationship between auditors and managers has become blurred.

In some sense, there is a problem of divorce of ownership from control. The companies that are audited by the Big Four have shareholders who are interested in profits and their dividends. But they employ managers who are responsible for the day-to-day running of the business. However, there are concerns that the auditors have become more concerned with meeting the interests of the managers and not of the shareholders. It has been suggested that the company’s management tend to ‘present their accounts in the most favourable light, whereas shareholder interests can be quite different.’ Laura Carstensen, the chair of the Audit Investigation Group said:

It is clear that there is significant dissatisfaction amongst some institutional investors with the relevance and extent of reporting in audited financial reports … management may have incentives to present their accounts in the most favourable light, whereas shareholder interests can be quite different.

The Big Four have been criticised for limiting competition in the industry. The Competition Commission has said that companies typically stay with the same auditing firm and this acts to limit competition. One suggestion to encourage competition is to enforce rotation of Auditors. However, the Big Four have said that the market remains competitive, ‘healthy and robust’ and that any enforcement as noted above would not be in the public interest. Other, smaller auditing companies have praised the preliminary report of the Competition Commission. One firm said:

The Big Four have been criticised for limiting competition in the industry. The Competition Commission has said that companies typically stay with the same auditing firm and this acts to limit competition. One suggestion to encourage competition is to enforce rotation of Auditors. However, the Big Four have said that the market remains competitive, ‘healthy and robust’ and that any enforcement as noted above would not be in the public interest. Other, smaller auditing companies have praised the preliminary report of the Competition Commission. One firm said:

No one solution will achieve market correction, but rather a combination of tendering requirements, encouragement of transparency and dialogue between auditors, companies and investors, and reform of outdated exclusionary practices should provide a backdrop for a healthier FTSE 350 audit market.

The report is not yet final, but the future of the Big Four is somewhat uncertain, especially with the European Commission’s desire to break them up. The following articles look at this industry.

Big Four accountants reject claims over high prices and poor competition The Guardian, Josephine Moulds and David Feeney (22/2/13)

Competition Commission raps Big Four accountants BBC News (22/2/13)

Big Four’s rivals welcome audit shake-up Financial Times, Adam Jones (22/2/13)

UK’s “Big Four” accountants under fire from watchdog Reuters, Huw Jones (22/2/13)

Big Four chastised by Competition Commission The Telegraph, Helia Ebrahimi (22/2/13)

The uncompetitive culture of auditing’s big four remains undented The Guardian, Prem Sikka (23/2/13)

Big Four accountants ‘in closed club on audits’ Independent, Mark Leftly (23/2/13)

Questions

- What is the role of the Competition Commission?

- Explain with other examples the problem of the divorce of ownership from control. How might the interest of shareholders and managers differ? Can they ever be aligned?

- Is market share a good measure of the competitiveness of an industry?

- What are the benefits of competition?

- Why has the regulator suggested that the Big Four are limiting competition?

- What solutions have been proposed by the Competition Commission? Explain how they are likely to stimulate competition in this market.

The OFT has criticized payday loan companies for competing not on costs, but on the speed of approval and using certain unapproved tactics as part of their advertising. The selling point of such companies is that you can have the money in a very short time period. However, the criticism is that this leads to loans being given to those who are unable to afford them. Key credit checks are not being done and with late night texts being sent to often financially vulnerable people, it is no wonder that complaints have been received. In a statement, the OFT said:

The OFT has criticized payday loan companies for competing not on costs, but on the speed of approval and using certain unapproved tactics as part of their advertising. The selling point of such companies is that you can have the money in a very short time period. However, the criticism is that this leads to loans being given to those who are unable to afford them. Key credit checks are not being done and with late night texts being sent to often financially vulnerable people, it is no wonder that complaints have been received. In a statement, the OFT said: