So here we are, summer is over (or almost over if you’re an optimist) and we are sitting in front of our screens reminiscing about hot sunny days (at least I do)! There is no doubt, however: a lot happened in the world of politics and economics in the past three months. The escalation of the US-China trade war, the run on the Turkish lira, the (successful?) conclusion of the Greek bailout – these are all examples of major economic developments that took place during the summer months, and which we will be sure to discuss in some detail in future blogs. Today, however, I will introduce a topic that I am very interested in as a researcher: the liberalisation of energy markets in developing countries and, in particular, Mexico.

So here we are, summer is over (or almost over if you’re an optimist) and we are sitting in front of our screens reminiscing about hot sunny days (at least I do)! There is no doubt, however: a lot happened in the world of politics and economics in the past three months. The escalation of the US-China trade war, the run on the Turkish lira, the (successful?) conclusion of the Greek bailout – these are all examples of major economic developments that took place during the summer months, and which we will be sure to discuss in some detail in future blogs. Today, however, I will introduce a topic that I am very interested in as a researcher: the liberalisation of energy markets in developing countries and, in particular, Mexico.

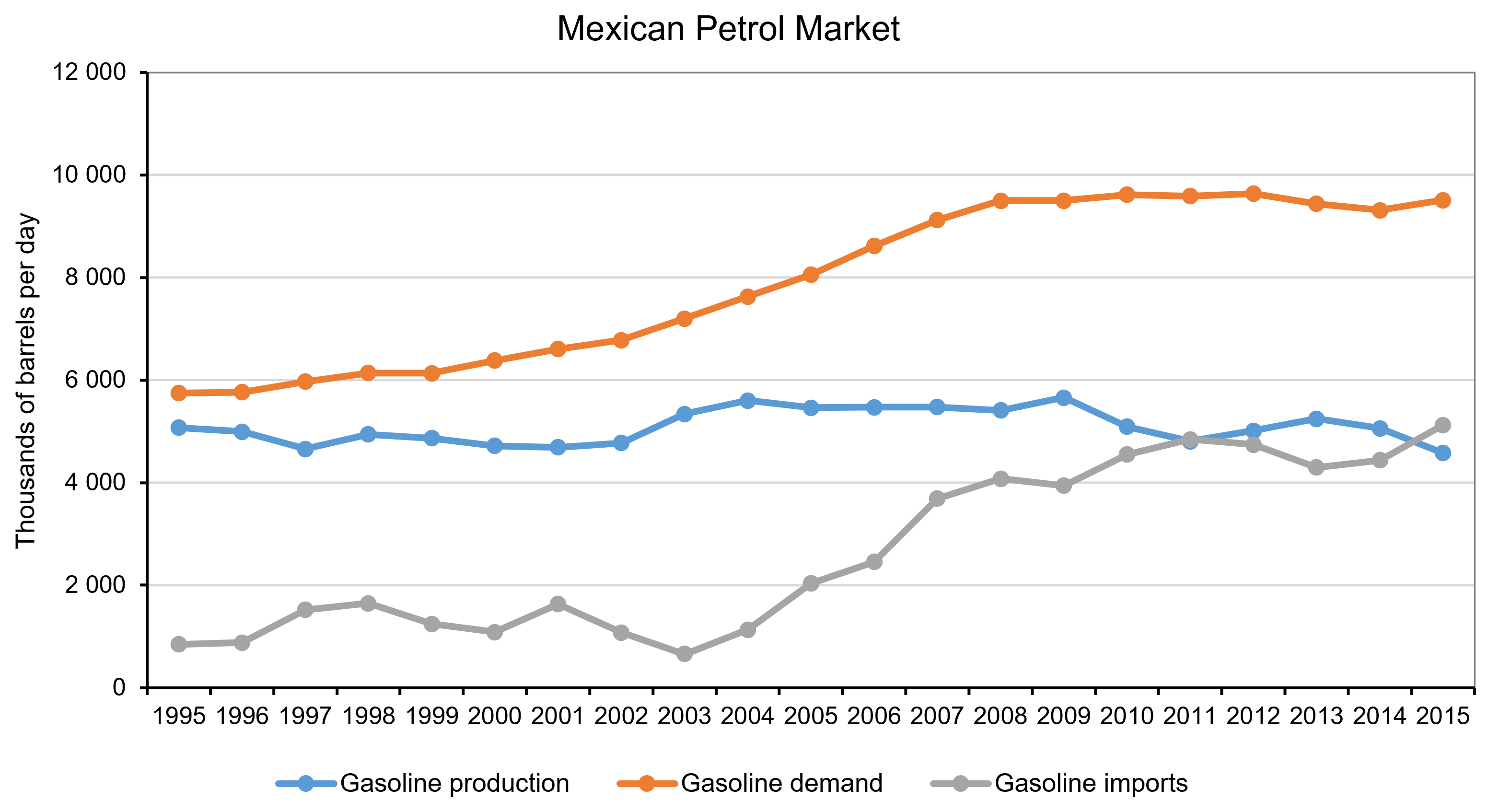

Why Mexico? Well, because it is a great example of a large developing economy that has been attempting to liberalise its energy market and reverse price setting and monopolistic practices that go back several decades. Until very recently, the price of petrol in Mexico was set and controlled by Pemex, a state monopolist. This put Pemex under pressure since, as a sole operator, it was responsible for balancing growing demand and costs, even to the detriment of its own finances.

The petrol (or ‘gasoline’) price liberalisation started in May 2017 and took place in stages – starting in the North part of Mexico and ending in November of the same year in the central and southern regions of the country. The main objective was to address the notable decrease in domestic oil production that put at risk the ability of the country to meet demand; as well as Mexico’s increasing dependency on foreign markets affected by the surge of the international oil price. The government has spent the past five years trying to create a stronger regulatory framework, while easing the financial burden on the state and halting the decline in oil reserves and production. Unsurprisingly, opening up a monopolistic market turns out to be a complex and bumpy process.

Source: Author’s calculations using data from the Energy Information Bank, Ministry of Energy, Mexico

Source: Author’s calculations using data from the Energy Information Bank, Ministry of Energy, Mexico

Despite all the reforms, retail petrol prices have kept rising. Although part of this price rise is demand-driven, an increasing number of researchers highlight the significance of the distribution of oil-related infrastructure in determining price outcomes at the federal and regional (state) level. Saturation and scarcity of both distribution and storage infrastructure are probably the two most significant impediments to opening the sector up to competition (Mexico Institute, 2018). You see, the original design of these networks and the deployment of the infrastructure was not aimed at maximising efficiency of distribution – the price was set by the monopolist and, in a way that was compliant with government policy (Mexico Institute, 2018). Economic efficiency was not always part of this equation. As a result, consumers located in better-deployed areas were subsidising the inherent logistics costs of less ‘well endowed’ regions by facing an artificially higher price than they would have in a competitive market.

But what about now? Do such differences in the allocation of infrastructure between regions lead to location-related differences in the price of petrol? If so, by how much? And, what policies should the government pursue to address such imbalances? These are all questions that I explore in one of my recent working papers titled ‘Widening the Gap: Lessons from the aftermath of the energy market reform in Mexico’ (with Hugo Vallarta) and I will be sharing some of the answers with you in a future blog.

Articles

Data

Questions

- Are state-owned monopolies effective in delivering successful market outcomes? Why yes, why no?

- In the case of Mexico, are you surprised about the complexities that were involved with opening up markets to competition? Explain why.

- Use Google to identify countries in which energy markets are controlled by state-owned monopolies.

The economic climate remains uncertain and, as we enter 2017, we look towards a new President in the USA, challenging negotiations in the EU and continuing troubles for High Street stores. One such example is Next, a High Street retailer that has recently seen a significant fall in share price.

The economic climate remains uncertain and, as we enter 2017, we look towards a new President in the USA, challenging negotiations in the EU and continuing troubles for High Street stores. One such example is Next, a High Street retailer that has recently seen a significant fall in share price.

Prices of clothing and footwear increased in December for the first time in two years, according to the British Retail Consortium, and Next is just one company that will suffer from these pressures. This retail chain is well established, with over 500 stores in the UK and Eire. It has embraced the internet, launching its online shopping in 1999 and it trades with customers in over 70 countries. However, despite all of the positive actions, Next has seen its share price fall by nearly 12% and is forecasting profits in 2017 to be hit, with a lack of growth in earnings reducing consumer spending and thus hitting sales.

The sales trends for Next are reminiscent of many other stores, with in-store sales falling and online sales rising. In the days leading up to Christmas, in-store sales fell by 3.5%, while online sales increased by over 5%. However, this is not the only trend that this latest data suggests. It also indicates that consumer spending on clothing and footwear is falling, with consumers instead spending more money on technology and other forms of entertainment. Kirsty McGregor from Drapers magazine said:

“I think what we’re seeing there is an underlying move away from spending so much money on clothing and footwear. People seem to be spending more money on going out and on technology, things like that.”

Furthermore, with price inflation expected to rise in 2017, and possibly above wage inflation, spending power is likely to be hit and it is spending on those more luxury items that will be cut. With Next’s share price falling, the retail sector overall was also hit, with other companies seeing their share prices fall as well, although some, such as B&M, bucked the trend. However, the problems facing Next are similar to those facing other stores.

But for Next there is more bad news. It appears that the retail chain has simply been underperforming for some time. We have seen other stores facing similar issues, such as BHS and Marks & Spencer. Neil Wilson from ETX Capital said:

“The simple problem is that Next is underperforming the market … UK retail sales have held up in the months following the Brexit vote but Next has suffered. It’s been suffering for a while and needs a turnaround plan … The brand is struggling for relevancy, and risks going the way of Marks & Spencer on the clothing front, appealing to an ever-narrower customer base.”

Brand identity and targeting customers are becoming ever more important in a highly competitive High Street that is facing growing competition from online traders. Next is not the first company to suffer from this and will certainly not be the last as we enter what many see as one of the most economically uncertain years since the financial crisis.

Next’s gloomy 2017 forecast drags down fashion retail shares The Guardian, Sarah Butler and Julia Kollewe (4/1/17)

Next shares plummet after ‘difficult’ Christmas trading The Telegraph, Sam Dean (4/1/17)

Next warns 2017 profits could fall up to 14% as costs grow Sky News, James Sillars (4/1/17)

Next warns on outlook as sales fall BBC News (4/1/17)

Next chills clothing sector with cut to profit forecast Reuters, James Davey (4/1/17)

Next shares drop after warning of difficult winter Financial Times, Mark Vandevelde (22/10/15)

Questions

- With Next’s warning of a difficult winter, its share price fell. Using a diagram, explain why this happened.

- Why have shares in other retail companies also been affected following Next’s report on its profit forecast for 2017?

- Which factors have adversely affected Next’s performance over the past year? Are they the same as the factors that have affected Marks & Spencer?

- Next has seen a fall in profits. What is likely to have caused this?

- How competitive is the UK High Street? What type of market structure would you say that it fits into?

- With rising inflation expected, what will this mean for consumer spending? How might this affect economic growth?

- One of the factors affecting Next is higher import prices. Why have import prices increased and what will this mean for consumer spending and sales?

An earlier post on this site described a recent row between Tesco and Unilever that erupted when Unilever attempted to raise the prices it charges Tesco for its products. Unilever justified this because its costs have increased as a result of the UK currency depreciation following the Brexit decision.

An earlier post on this site described a recent row between Tesco and Unilever that erupted when Unilever attempted to raise the prices it charges Tesco for its products. Unilever justified this because its costs have increased as a result of the UK currency depreciation following the Brexit decision.

It also appears that more general concerns that the fall in the value of sterling would lead to higher retail prices were prevalent around the time that the Tesco Unilever dispute came to light. Former Sainsbury’s boss, Justin King, made clear that British shoppers should be prepared for higher prices. He also said that:

Retailers’ margins are already squeezed. So there is no room to absorb input price pressures and costs will need to be passed on. But no one wants to be the first to break cover. No business wants to be the first to blame Brexit for a rise in prices. But once someone does, there will be a flood of companies because they will all be suffering.

It is interesting to consider further why the Tesco and Unilever case was the first to make the headlines and why their dispute was resolved so quickly. In addition, what are the more general implications for the retail prices consumers will have to pay?

Arguably, Unilever saw itself as having a strong hand in negotiations with Tesco because its product portfolio includes a wide variety of must-stock brands, including Pot Noodles, Marmite and Persil, that are found in 98% of UK households..

Unilever has been criticised for using the currency devaluation as an excuse to justify charging Tesco more, since most of its products are made in the UK. However, Unilever was quick to point outthat commodities it uses in the manufacture of products are priced in US dollars, so the currency devaluation can still affect the cost of products that it manufactures in the UK. In addition, Unilever’s chief financial officer, Graeme Pitkethly, insisted that price increases due to rising costs were a normal part of doing business:

We are taking price increases in the UK. That is a normal devaluation-led cycle.

On the other hand, even if the cost increases faced by Unilever are genuine, it is interesting to speculate whether it would have been so quick to adjust its prices downwards in response to a currency appreciation. After all, a commonly observed phenomenon across a range of markets is ‘rockets and feathers’ pricing behaviour i.e. prices going up from a cost increase more quickly than they go down following an equivalent cost decrease.

Compared to Unilever, some other suppliers are likely to have less bargaining power – in particular, those competing in highly fragmented markets and those producing less branded products. In such markets the suppliers may be forced to accept cost increases. For example, almost 50% of butter and cheese consumed in the UK comes from milk sourced from EU markets. Protecting such suppliers is one of the key roles of the Grocery code of conduct that the UK competition agency has put in place.

From Tesco’s point of view it will have benefited from good publicity by doing its best to protect consumers from price hikes. Helen Dickinson, chief executive of the British Retail Consortium, said:

Retailers are firmly on the side of consumers in negotiating with suppliers and improving efficiencies in the supply chain to control the inflationary pressure that is building through the devaluation of the pound.

However, it is also clear that Tesco had its own motives for resisting increased costs for Unilever’s products. In such situations both supplier and retailer should be keen to avoid a situation where they both impose their own substantial mark-ups at each stage of the supply chain. It is well established that this creates a double mark-up and not only harms consumers, but also the supplier and retailer themselves. Instead, the firms have an incentive to use more complex contractual arrangements to solve the problem. For example, suppliers may pay slotting allowances to get a place on the retailers’ shelves in exchange for lower retail mark-ups.

It has also been claimed that cutthroat competition in the supermarket industry, especially from discounter retailers Aldi and Lidl, made Tesco particularly keen to prevent price rises. Some arguments suggest that these discounters will be best placed to benefit from the currency devaluation as they sell more own brands, have a limited range, the leanest supply chains and benefit from substantial economies of scale. On the other hand, they source more of their products from abroad and it has been suggested that:

It has also been claimed that cutthroat competition in the supermarket industry, especially from discounter retailers Aldi and Lidl, made Tesco particularly keen to prevent price rises. Some arguments suggest that these discounters will be best placed to benefit from the currency devaluation as they sell more own brands, have a limited range, the leanest supply chains and benefit from substantial economies of scale. On the other hand, they source more of their products from abroad and it has been suggested that:

A fall in sterling will push prices up for everyone who sources products from Europe, but Aldi and Lidl will be affected more than most.

One prediction suggests that the overall impact of the currency depreciation on food prices will be an increase of around 3%. This may be particularly worrisome given concerns that the impact will fall most heavily on benefit claimants and other low-income households.

Outside of the food industry, Mike Rake, the chairman of BT, has highlighted the fact that:

Imported mobile phones and broadband home hubs were already 10% more expensive and the cost would have to be passed on to consumers in the near future.

It is therefore clear that the currency devaluation has the potential to create substantial tensions in the supply-chain agreements across a range of markets. The impact on the firms involved and on consumers will depend upon a wide range of factors, including the competitiveness of the markets, the nature of the firms involved and their bargaining power. Furthermore, evidence from an earlier currency depreciation in Latin America makes clear that the price elasticity of demand will be another factor that determines the impact price rises have.

Finally, it is also worth noting that a potential flip side of the currency depreciation is a boost for UK exports. However, it has been suggested that the manufacturing potential to take advantage of this in the UK is limited. In addition, even the manufacturing that does take place, for example in the car industry, often relies on components imported from abroad.

Articles

The Brexiteers’ Marmite conspiracy theories exposed their utter ignorance of how markets really work Independent, Ben Chu (16/10/16)

Tesco price dispute sends Unilever brand perceptions tumbling Marketing Week, Leonie Roderick (17/10/16)

Unilever and Tesco both benefit from their price row, but Brexit will bring more pain Marketing Week, Mark Ritson (19/10/16)

Why the Tesco v Unilever feud was good for British business campaign, Helen Edwards (20/10/16)

Questions

- What are some of the factors that affect a supplier’s bargaining power?

- How might the discount retailers respond to the currency devaluation?

- Use the figures from Latin America in the article cited above to calculate the price elasticity of demand.

- Explain why the price elasticity of demand is an important determinant of the effect of a price rise.

- Can you think of other examples of markets that may be particularly prone to price rises following a currency depreciation?

The articles below examine the rise of the sharing economy and how technology might allow it to develop. A sharing economy is where owners of property, equipment, vehicles, tools, etc. rent them out for periods of time, perhaps very short periods. The point about such a system is that the renter deals directly with the property owner – although sometimes initially through an agency. Airbnb and Uber are two examples.

The articles below examine the rise of the sharing economy and how technology might allow it to develop. A sharing economy is where owners of property, equipment, vehicles, tools, etc. rent them out for periods of time, perhaps very short periods. The point about such a system is that the renter deals directly with the property owner – although sometimes initially through an agency. Airbnb and Uber are two examples.

So far the sharing economy has not developed very far. But the development of smart technology will soon make a whole range of short-term renting contracts possible. It will allow the contracts to be enforced without the need for administrators, lawyers, accountants, bankers or the police. Payments will be made electronically and automatically, and penalties, too, could be applied automatically for not abiding by the contract.

One development that will aid this process is a secure electronic way of keeping records and processing payments without the need for a central authority, such as a government, a bank or a company. It involves the use of ‘blockchains‘ (see also). The technology, used in Bitcoin, involves storing data widely across networks, which allows the data to be shared. The data are secure and access is via individuals having a ‘private key’ to parts of the database relevant to them. The database builds in blocks, where each block records a set of transactions. The blocks build over time and are linked to each other in a logical order (i.e. in ‘chains’) to allow tracking back to previous blocks.

One development that will aid this process is a secure electronic way of keeping records and processing payments without the need for a central authority, such as a government, a bank or a company. It involves the use of ‘blockchains‘ (see also). The technology, used in Bitcoin, involves storing data widely across networks, which allows the data to be shared. The data are secure and access is via individuals having a ‘private key’ to parts of the database relevant to them. The database builds in blocks, where each block records a set of transactions. The blocks build over time and are linked to each other in a logical order (i.e. in ‘chains’) to allow tracking back to previous blocks.

Blockchain technology could help the sharing economy to grow substantially. It could significantly cut down the cost of sharing information about possible rental opportunities and demands, and allow minimal-cost secure transactions between owner and renter. As the IBM developerWorks article states:

Rather than use Uber, Airbnb or eBay to connect with other people, blockchain services allow individuals to connect, share, and transact directly, ushering in the real sharing economy. Blockchain is the platform that enables real peer-to-peer transactions and a true ‘sharing economy’.

Article

New technology may soon resurrect the sharing economy in a very radical form The Guardian, Ben Tarnoff (17/10/16)

Blockchain and the sharing economy 2.0 IBM developerWorks, Lawrence Lundy (12/5/16)

2016 is set to become the most interesting year yet in the life story of the sharing economy Nesta, Helen Goulden (Dec 2015)

Blockchain Explained Business Insider, Tina Wadhwa and Dan Bobkoff (16/10/16)

A parliament without a parliamentarian Interfluidity, Steve Randy Waldman (19/6/16)

Blockchain and open innovation: What does the future hold Tech City News, Jamie QIU (17/10/16)

Banks will not adopt blockchain fast Financial Times, Oliver Bussmann (14/10/16)

Blockchain-based IoT project does drone deliveries using Ethereum International Business Times, Ian Allison (14/10/16)

Questions

- What do you understand by the ‘sharing economy’?

- Give some current examples of the sharing economy? What other goods or services might be suitable for sharing if the technology allowed?

- How could blockchain technology be used to cut out the co-ordinating role carried out by companies such as Uber, eBay and Airbnb and make their respective services a pure sharing economy?

- Where could blockchain technology be used other than in the sharing economy?

- How can blockchain technology not only record property rights but also enforce them?

- What are the implications of blockchain technology for employment and unemployment? Explain.

- How might attitudes towards using the sharing economy develop over time and why?

- Referring to the first article above, what do you think of Toyota’s use of blockchain to punish people who fall behind on their car payments? Explain your thinking.

- Would the use of blockchain technology in the sharing economy make markets more competitive? Could it make them perfectly competitive? Explain.

A row erupted in mid-October between Tesco, the UK’s biggest supermarket, and Unilever, the Anglo-Dutch company. Unilever is the world’s largest consumer goods manufacturer with many well-known brands, including home care products, personal care products and food and drink. Unilever, which manufactures many of its products abroad and uses many ingredients from abroad in those manufactured in the UK, wanted to charge supermarkets 10% more for its products. It blamed the 16% fall in the value of sterling since the referendum in June (see the blog Sterling’s slide).

A row erupted in mid-October between Tesco, the UK’s biggest supermarket, and Unilever, the Anglo-Dutch company. Unilever is the world’s largest consumer goods manufacturer with many well-known brands, including home care products, personal care products and food and drink. Unilever, which manufactures many of its products abroad and uses many ingredients from abroad in those manufactured in the UK, wanted to charge supermarkets 10% more for its products. It blamed the 16% fall in the value of sterling since the referendum in June (see the blog Sterling’s slide).

Tesco refused to pay the increase and so Unilever halted deliveries of over 200 items. As a result, several major brands became unavailable on the Tesco website. The dispute was dubbed ‘Marmitegate’, after one of Unilever’s products.

This is a classic case of power on both sides of the market: a powerful oligopolist, Unilever, facing a powerful oligopsonist, Tesco. With rising costs for Unilever resulting from the falling pound, either Unilever had to absorb the costs, or Tesco had to be prepared to pay the higher prices demanded by Unilever, passing some or all of them onto customers, or there had to be a compromise, with the prices Tesco pays to Unilever rising, but by less than 10%. A compromise was indeed reached on 13 October, with different price increases for each of Unilever’s products depending on how much of the costs are in foreign currencies. Precise details of the deal remained secret.

This is a classic case of power on both sides of the market: a powerful oligopolist, Unilever, facing a powerful oligopsonist, Tesco. With rising costs for Unilever resulting from the falling pound, either Unilever had to absorb the costs, or Tesco had to be prepared to pay the higher prices demanded by Unilever, passing some or all of them onto customers, or there had to be a compromise, with the prices Tesco pays to Unilever rising, but by less than 10%. A compromise was indeed reached on 13 October, with different price increases for each of Unilever’s products depending on how much of the costs are in foreign currencies. Precise details of the deal remained secret.

An interesting dynamic in the dispute was that Tesco and Unilever were acting as ‘champions’ for retailers and suppliers respectively. Other supermarkets were also facing price rises by Unilever.  Their reactions were likely to depend on what Tesco did. Similarly, other suppliers were facing rising costs because of the falling pound. Their reactions might depend on how successful Unilever was in passing on its cost increases to retailers.

Their reactions were likely to depend on what Tesco did. Similarly, other suppliers were facing rising costs because of the falling pound. Their reactions might depend on how successful Unilever was in passing on its cost increases to retailers.

This example of ‘countervailing power’, or ‘bilateral oligopoly’, helps to illustrate just how much the consumer can gain when a powerful seller is confronted by a powerful buyer. The battle was been likened to that between two ‘gorillas’ of the industry. Its ramifications throughout industry will be interesting.

Podcasts and Webcasts

Tesco-Unilever row: Can unique shop explain ‘Marmitegate’? BBC News, Dougal Shaw (13/10/16)

Tesco-Unilever row: Can unique shop explain ‘Marmitegate’? BBC News, Dougal Shaw (13/10/16)

Tesco, Unilever in Brexit price clash Reuters, David Pollard (13/10/16)

Brexit price-rise warning to shoppers BBC News, Simon Jack (10/10/16)

Tesco in Brexit Pricing Spat With Unilever Wall Street Journal (13/10/16)

Tesco battles Unilever over prices Financial Times on YouTube (14/10/16)

Tesco vs Unilever: Who won? ITV News, Joel Hills (14/10/16)

Articles

Tesco removes Marmite and other Unilever brands in price row BBC News (13/10/16)

Marmite Brexit Shortage ‘Just The Beginning’ Of ‘Gorilla’ Grocery Battle As Pound Slumps Huffington Post, Louise Ridley (13/10/16)

Unilever sales increase despite dozens of its brands being removed from Tesco shelves Independent, Ben Chapman (13/10/16)

Tesco-Unilever price row: Why pound value slump has caused Marmite to disappear from shelves Independent, Zlata Rodionova (13/10/16)

Tesco pulls Marmite from online store amid Brexit price row with Unilever The Telegraph, Peter Dominiczak, Steven Swinford and Ashley Armstrong (13/10/16)

Tesco runs short on Marmite and household brands in price row with Unilever The Guardian, Sarah Butler (13/10/16)

Tesco pulls products over plunging pound Financial Times, Mark Vandevelde, Scheherazade Daneshkhu and Paul McClean (13/10/16)

Brexit means…higher prices The Economist, Buttonwood’s notebook (13/10/16)

Tesco, Unilever settle prices row after pound’s Brexit dive Reuters, James Davey and Martinne Geller (14/10/16)

Questions

- To what extent can Tesco and Unilever be seen a price leaders of their respective market segments?

- What would you advise other supermarkets to do over their pricing decisions when faced with increased prices from suppliers, and why?

- What would you advise manufacturers of other consumer goods sold in supermarkets to do in the light of the Tesco/Unilever dispute, and why?

- What determines the price elasticity of demand for branded products, such as Marmite, Persil, Dove soap, Hellmann’s mayonnaise, PG Tips tea and Wall’s ice cream?

- What factors will determine in the end just how much extra the consumer pays when supermarkets are faced with demands for higher prices from major suppliers?

- Give some other examples of firms in industries where there is a high degree of countervailing power.

- What are the macroeconomic implications of a depreciating exchange rate?

- If, over the long term, the pound remained 16% below its level in June 2016, would you expect the consumer prices index in the long term to be approximately 16% higher than it would have been if the pound had not depreciated? Explain why or why not.