Last week was a rough week for Britain. The “Beast from the East” and storm Emma swept through the country, bringing with them unusually heavy snowfall, which resulted in severe disruption across nearly all parts of the country. Some recent estimates put the cost of these extreme weather conditions at up to £1 billion per day. The construction industry suffering the biggest hit as work came to a halt for the best part of the week. Losses for the industry were estimated to be up to £2 billion.

Closed restaurants, empty shops and severely disrupted transport networks were all part of the effect that this extreme weather had on the overall economy. According to Howard Archer, chief economic adviser of the EY ITEM Club (a UK forecasting group):

It is possible that the severe weather [of the last few days] could lead to GDP growth being reduced by 0.1 percentage point in Q1 2018 and possibly 0.2 percentage points if the severe weather persist.

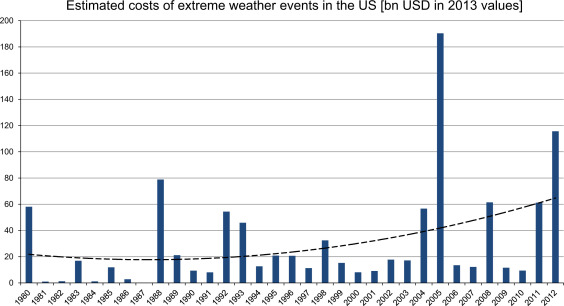

Source: Jahn (2015), Figure 2

As the occurrence of freak weather increases across the globe due to climate change, so does the economic cost of these events. The figure above shows the estimated costs of extreme weather events in the USA between 1980 and 2012 and it is reproduced from Jahn (see link below), who also fits a quadratic trend to show that these costs have been increasing over time. He goes on to characterise the impact of different types of extreme weather (including cold waves, heat waves, storms and others) on different sectors of the local economy – ranging from tourism and agriculture, to housing and the insurance sector.

Linnenluecke et al (linked below) argue that extreme weather caused by climate change could influence the decision of firms on where to locate and could lead to a reshuffle of economic activity across the world and have important policy implications. As the authors explain:

Climate change-related relocation has been given consideration in policy-oriented discussions, but not in management decisions. The effects of climate change and extreme weather events have been considered as peripheral or as a risk factor, but not as a determining factor in firm relocation processes…. This paper therefore [provides] insights for understanding how firms can enhance strategic decision-making in light of understanding and assessing their vulnerability as well as likely impacts that climate change may have on relocation decisions.

The likelihood and associated costs of extreme weather events could therefore become an increasingly important matter for discussion amongst economists and policy makers. Such weather events are likely to have profound economic implications for the world.

The Winter Olympics are full on as athletes from all over the world compete against each other, hoping to set new world records, win medals and be known as Olympians. Pyeongchang, the South Korean county that hosts the 2018 Winter games, enjoys a large influx of tourists – estimated at 80,000 people a day. This is certainly an unusually large number of tourists for a region that has a regular winter-time population of no more than 45,000 people.

Having such a high number of visitors to the Winter Olympics, and even more to the larger Summer Olympics, is not an unusual occurrence, however, and it is often mentioned as one of the benefits of being a host to the Olympic Games.

Baade and Matheson (see link below) distinguish between three key benefits of hosting the Olympic Games: “the short-run benefits of tourist spending during the Games; the long-run benefits or the ‘Olympic legacy’, which might include improvements in infrastructure and increased trade, foreign investment, or tourism after the Games; and intangible benefits such as the ‘feel-good effect’ or civic pride”.

On these grounds, a number of studies have been authored, attempting to analyse some or all of these benefits, distinguishing between short-term and long-term effects. Müller (see link below), uses data from the 2014 Oympic Games in Sochi, Russia, to assess the net economic outcome for the host region. He concludes that any short-term economic benefits caused by the investment influx (before and during the games) could not offset the long-term costs, leading to an estimated net loss of $1.2 billion per year.

Zimbalist (2015) and Szymanski (2011) report similar results when analysing data from the London Games (2012) and past major sporting events (Games and FIFA World Cup). Kasimati (2003) points out the significant economic benefits that host regions tend to enjoy for years after hosting the games, but argues that the overall effect depends on a number of factors (including pre-existing infrastructure and location).

The jury is, therefore, still out on what is the overall economic effect of being host to this ancient institution. But I must now dash as women’s hockey is soon to start. “Let everyone shine”.

Using supply and demand diagrams, explain whether you would expect hotel room prices to change during the hosting of a major sports event, such as the Winter Olympics.

List three economic (or economics-related) arguments in favour of and against the hosting of the Olympic games. Relate your answer to the empirical evidence presented in the literature.

Why is it so difficult to estimate with accuracy the net economic effect of the Olympic Games?

On 15 January 2018, Carillion went into liquidation. It was a major construction, civil engineering and facilities management company in the UK and was involved in a large number of public- and private-sector projects. Many of these were as a partner in a joint venture with other companies.

It was the second largest supplier of construction and maintenance services to Network Rail, including HS2. It was also involved in the building of hospitals, including the new Royal Liverpool University Hospital and Midland Metropolitan Hospital in Smethwick. It also provided maintenance, cleaning and catering services for many schools, universities, hospitals, prisons, government departments and local authorities. In addition it was involved in many private-sector projects.

Much of the work on the projects awarded to Carillion was then outsourced to other companies, many of which are small construction, maintenance, equipment and service companies. A large number of these may themselves be forced to close as projects cease and many bills remain unpaid.

Many of the public-sector projects in which Carillion was involved were awarded under the Public Finance Initiative (PFI). Under the scheme, the government or local authority decides the service it requires, and then seeks tenders from the private sector for designing, building, financing and running projects to provide these services. The capital costs are borne by the private sector, but then, if the provision of the service is not self-financing, the public sector pays the private firm for providing it. Thus, instead of the public sector being an owner of assets and provider or services, it is merely an enabler, buying services from the private sector. The system is known as a Public Private Partnership.

Clearly, there are immediate benefits to the public finances from using private, rather than public, funds to finance a project. Later, however, there is potentially an extra burden of having to buy the services from the private provider at a price that includes an element for profit. What is hoped is that the costs to the taxpayer of these profits will be more than offset by gains in efficiency.

Critics, however, claim that PFI projects have resulted in poorer quality of provision and that cost control has often been inadequate, resulting in a higher burden for the taxpayer in the long term. What is more, many of the projects have turned out to be highly profitable, suggesting that the terms of the original contracts were too lax.

There was some modification to the PFI process in 2012 with the launching of the government’s modified PFI scheme, dubbed PF2. Most of the changes were relatively minor, but the government would act as a minority public equity co-investor in PF2 projects, with the public sector taking stakes of up to 49 per cent in individual private finance projects and appointing a director to the boards of each project. This, it was hoped, would give the government greater oversight of projects.

With the demise of Carillion, there has been considerable debate over outsourcing by the government to the private sector and of PFI in particular. Is PFI the best model for funding public-sector investment and the running of services in the public sector?

On 18 January 2018, the National Audit Office published an assessment of PFI and PF2. The report stated that there are currently 716 PFI and PF2 projects either under construction or in operation, with a total capital value of £59.4 billion. In recent years, however, ‘the government’s use of the PFI and PF2 models has slowed significantly, reducing from, on average, 55 deals each year in the five years to 2007-08 to only one in 2016-17.’

Should the government have closer oversight of private providers? The government has been criticised for not heeding profit warnings by Carillion and continuing to award it contracts.

Should the whole system of outsourcing and PFI be rethought? Should more construction and services be brought ‘in-house’ and directly provided by the public-sector organisation, or at least managed directly by it with a direct relationship with private-sector providers? The articles below consider these issues.

Why did Carillion go into liquidation? Could this have been foreseen?

Identify the projects in which Carillion has been involved.

What has the government proposed to deal with the problems created by Carillion’s liquidation?

What are the advantages and disadvantages of the Private Finance Initiative?

Why have the number and value of new PFI projects declined significantly in recent years?

How might PFI projects be tightened up so as to retain the benefits and minimise the disadvantages of the system?

Why have PFI cost reductions proved difficult to achieve? (See paragraphs 2.7 to 2.17 in the National Audit Office report.)

How would you assess whether PFI deals represent value for money?

What are the arguments for and against public-sector organisations providing services, such as cleaning and catering, directly themselves rather than outsourcing them to private-sector companies?

Does outsourcing reduce risks for the public-sector organisation involved?

The linked articles below look at the state of the railways in Britain and whether renationalisation would be the best way of securing more investment, better services and lower fares.

Rail travel and rail freight involve significant positive externalities, as people and goods transported by rail reduce road congestion, accidents and traffic pollution. In a purely private rail system with no government support, these externalities would not be taken into account and there would be a socially sub-optimal use of the railways. If all government support for the railways were withdrawn, this would almost certainly result in rail closures, as was the case in the 1960s, following the publication of the Beeching Report in 1963.

Also the returns on rail investment are generally long term. Such investment may not, therefore, be attractive to private rail operators seeking shorter-term returns.

These are strong arguments for government intervention to support the railways. But there is considerable disagreement over the best means of doing so.

One option is full nationalisation. This would include both the infrastructure (track, signalling, stations, bridges, tunnels and marshalling yards) and the trains (the trains themselves – both passenger and freight – and their operation).

At present, the infrastructure (except for most stations) is owned, operated, developed and maintained by Network Rail, which is a non-departmental public company (NDPB) or ‘Quango’ (Quasi-autonomous non-governmental organisation, such as NHS trusts, the Forestry Commission or the Office for Students. It has no shareholders and reinvests its profits in the rail infrastructure. Like other NDPBs, it has an arm’s-length relationship with the government. Network Rail is answerable to the government via the Department for Transport. This part of the system, therefore, is nationalised – if the term ‘nationalised organisations’ includes NDPBs and not just full public corporations such as the BBC, the Bank of England and Post Office Ltd.

Train operating companies, however, except in Northern Ireland, are privately owned under a franchise system, with each franchise covering specific routes. Each of the 17 passenger franchises is awarded under a competitive tendering system for a specific period of time, typically seven years, but with some for longer. Some companies operate more than one franchise.

Companies awarded a profitable franchise are required to pay the government for operating it. Companies awarded a loss-making franchise are given subsidies by the government to operate it. In awarding franchises, the government looks at the level of payments the bidders are offering or the subsidies they are requiring.

But this system has come in for increasing criticism, with rising real fares, overcrowding on many trains and poor service quality. The Labour Party is committed to taking franchises into public ownership as they come up for renewal. Indeed, there is considerable public support for nationalising the train operating companies.

The main issue is which system would best address the issues of externalities, efficiency, quality of service, fares and investment. Ultimately it depends on the will of the government. Under either system the government plays a major part in determining the level of financial support, operating criteria and the level of investment. For this reason, many argue that the system of ownership is less important than the level and type of support given by the government and how it requires the railways to be run.

What categories of market failure would exist in a purely private rail system with no government intervention?

What types of savings could be made by nationalising train operating companies?

The franchise system is one of contestable monopolies. In what ways are they contestable and what benefits does the system bring? Are there any costs from the contestable nature of the system?

Is it feasible to have franchises that allow more than one train operator to run on most routes, thereby providing some degree of continuing competition?

How are rail fares determined in Britain?

Would nationalising the train operating companies be costly to the taxpayer? Explain.

What determines the optimal length of a franchise under the current system?

What role does leasing play in investment in rolling stock?

What are the arguments for and against the government’s decision in November 2017 to allow the Virgin/Stagecoach partnership to pull out of the East Coast franchise three years early because it found the agreed payments to the government too onerous?

Could the current system be amended in any way to meet the criticisms that it does not adequately take into account the positive externalities of rail transport and the need for substantial investment, while also encouraging excessive risk taking by bidding companies at the tendering stage?

Do you want to get drunk this festive season in the most tax efficient way: i.e. minimise the amount of tax you pay for the volume of alcohol that you drink? Do tax rates vary or are all alcoholic drinks taxed in the same or similar way?

The UK government imposes two different types of tax on alcohol. One is a specific or fixed tax per unit, referred to as excise duty or excise tax. This varies depending on the type of alcohol and is the focus of this blog. The other is VAT, which is 20% of the price for all alcoholic drinks. The price on which VAT is based includes the impact of the excise tax.

How does the implementation of excise tax differ between alcoholic drinks? Both the tax rate itself and the unit of output on which it is based vary: i.e. the volume of liquid vs the volume of pure alcohol within the liquid.

For example, with lager, beer and spirits the excise tax depends on the units of alcohol in the drink rather than the number of litres. The tax works in the following way. It is based on the alcohol by volume or ABV of the lager, beer or spirit. This is often displayed on the bottle or can. ABV is the percentage of the drink that is pure alcohol. Therefore, if a one-litre bottle of lager has an ABV of 1%, then 10ml of the bottle contains pure alcohol. Ten millilitres of pure alcohol is one unit of alcohol. If a one litre bottle of lager had an ABV of 5% it contains 5 units of alcohol.

Excise duties on spirits are the simplest of all the alcohol taxes. The rate for 2017/18 is 28.74p for each percentage of ABV or unit of alcohol in a one-litre bottle. Most spirits have an ABV of 40%. This means that there are 40 units of alcohol in a litre bottle and the excise tax payable on that bottle is £11.50 (40 × 28.74p). If a litre bottle had an ABV of 57%, such as Woods Navy Rum, then the excise tax would be or £16.38 (57 × 28.74p). Although the volume of liquid is the same in each case, the excise tax has increased by £4.88 because the alcohol content has increased.

For cider and wine the system is quite different. Within certain bands of alcoholic strength, the excise duty is based on the volume of the drink rather than by its ABV. For example, the excise tax on a litre of cider with an ABV of between 1.2% and 7.5% is 40.38p. This has the effect of reducing the tax rate per unit of alcohol as the alcoholic content of the cider increases (up to a limit of 7.5%). For example, the rate of excise tax per unit of alcohol for a litre bottle of cider with an ABV of 2% is 20.19p (40.38/2) whereas for a litre bottle of cider with an ABV of 7.5% it is just 5.39p (40.38/7.5). Wine is taxed in a similar way. A litre of wine with an ABV of between 5.5% and 15% is taxed at 288.65p per litre.

The excise tax rates per unit of alcohol for different drinks are illustrated below.

Drink

ABV

Excise tax per unit of alcohol

Beer/lager

5%

19.08p

Beer/lager

8%

24.77p

Spirits

1-100%

28.74p

Wine

12.5%

21.90p

Wine

15%

19.24p

Cider

5%

8.08p

Cider

7.5%

5.39p

The table clearly shows that cider with an ABV of 7.5 per cent is by far the most tax effective way of consuming alcohol.

Although this blog is a rather light-hearted look at excise tax, it does help to illustrate the strange anomalies of the system used in the UK. Research by the Institute for Fiscal Studies (IFS) has indicated that heavier drinkers are more likely to switch between different alcoholic products in response to price changes. They also tend to drink products with more units of alcohol in them: i.e. spirits such as whisky and gin. For these reasons, the IFS has suggested that the excise tax rates on cider and spirits should be increased.

In the November budget, the Chancellor announced plans to introduce a new excise tax rate on still cider with an ABV of between 6.9% and 7.5%.

The excise taxes on cider and wine are based on the volume of liquid because of the European Community Directive 92/84/EEC. It will be interesting to see if the government changes this system to one based on alcohol content once the UK had left the European Union.

Explain the difference between an ad valorem tax and a specific tax.

Illustrate the impact of an ad valorem tax and a specific tax on a demand and supply diagram.

What is the excise tax rate per unit of alcohol on a litre bottle of cider with an ABV of 6%?

What is the economic rationale for imposing excise tax on alcohol?

How will the external costs of consuming alcohol differ from those of smoking cigarettes? Draw a marginal external cost of consumption curve for both products to illustrate the difference.

Compare the impact of increasing excise tax rates on cider and spirits with introducing a minimum unit price for alcohol.

In April 2012 the government in England and Wales imposed a ban on ‘below cost’ pricing of alcohol. Explain how this policy works and what impact you think it has had.

Last week was a rough week for Britain. The “Beast from the East” and storm Emma swept through the country, bringing with them unusually heavy snowfall, which resulted in severe disruption across nearly all parts of the country. Some recent estimates put the cost of these extreme weather conditions at up to £1 billion per day. The construction industry suffering the biggest hit as work came to a halt for the best part of the week. Losses for the industry were estimated to be up to £2 billion.

Last week was a rough week for Britain. The “Beast from the East” and storm Emma swept through the country, bringing with them unusually heavy snowfall, which resulted in severe disruption across nearly all parts of the country. Some recent estimates put the cost of these extreme weather conditions at up to £1 billion per day. The construction industry suffering the biggest hit as work came to a halt for the best part of the week. Losses for the industry were estimated to be up to £2 billion.