As we reported in New Build: Foundations for a successful housing policy? the Autumn Statement heralded significant reforms to Stamp Duty – the UK tax on house purchases. The result is the introduction of a graduated system of tax, along the lines of the income tax system. A similar regime will continue to operate in Scotland when the Land and Buildings Transactions Tax replaces Stamp Duty next April. Here we consider the impact on the effective rates of tax following the changes to Stamp Duty.

As we reported in New Build: Foundations for a successful housing policy? the Autumn Statement heralded significant reforms to Stamp Duty – the UK tax on house purchases. The result is the introduction of a graduated system of tax, along the lines of the income tax system. A similar regime will continue to operate in Scotland when the Land and Buildings Transactions Tax replaces Stamp Duty next April. Here we consider the impact on the effective rates of tax following the changes to Stamp Duty.

Under the old system any house purchase involving a property whose value was £125,000 or less incurred no Stamp Duty liability. Thereafter, one of five tax rates applied: 1% above £125,000 to £250,000, 3% above £250,000 to £500,000, 4% above £500,000 to £1m, 5% above £1m to £2m and 7 per cent for properties over £2m. The important point was that the whole of the purchase price was subject to one of these five progressively higher tax rates.

The new system sees the introduction of a graduated system of tax which means that the amount paid by house purchasers will be dependent upon the proportion of the value of the property that falls in each of the tax bands. Again, for properties up to £125,000 there will be no liability. There will then be four bands: 1% above £125,000 to £250,000, 5% above £250,000 up to £925,000, 10% above £925,000 up to £150,000 and 12% above £150,000.

One significant impact of the changes is that the liability will be more proportionate to the value of the property. To see this we can compare the average rate of tax under the new and old tax system. The average rate of tax is simply the amount of the tax liability relative to the price of the property.

From Chart 1 we can see how the new average rate of tax under rises progressively with the price of the property. (Click here to download a PowerPoint of the chart). Under the old system, the profile of the average rate of tax looks like a series of steps with a slab at each tax rate. Unsurprisingly, the system was sometimes referred as the ‘slab system’.

From Chart 1 we can see how the new average rate of tax under rises progressively with the price of the property. (Click here to download a PowerPoint of the chart). Under the old system, the profile of the average rate of tax looks like a series of steps with a slab at each tax rate. Unsurprisingly, the system was sometimes referred as the ‘slab system’.

A second significant change will be the removal of the significant spikes in the marginal rate of tax around each of the tax bands. For example, the tax liability on a property costing £125,001 was £1,250.01 compared with a zero liability on a property costing £125,000. Therefore, a £1 rise in the price of property was accompanied by a £1,250.01 rise in the purchase tax. In percentage terms this is a marginal rate of tax of 125,001. Chart 1 shows how the marginal rates now match the progressively higher tax rates that become payable between each threshold.

The principle of removing the significant distortions to pricing created by the old system of Stamp Duty is likely to receive general approval. However, there may be some unease around the short-term implications for house prices of the bands and rates under the new system. This is largely because nobody purchasing a property at £937,000 or less will see their tax liability rise. The reduction in the liability raises concerns about a potential boost to house prices.

Chart 2 show the percentage change in the Stamp Duty liability for properties of up to £2.5 million. (Click here to download a PowerPoint of the chart.) The average UK house price, excluding London, is currently £235,000. The stamp duty saving in this case is £150 or 6.4 per cent.

Chart 2 show the percentage change in the Stamp Duty liability for properties of up to £2.5 million. (Click here to download a PowerPoint of the chart.) The average UK house price, excluding London, is currently £235,000. The stamp duty saving in this case is £150 or 6.4 per cent.

But there are more significant savings than this from the reforms, including in London where inflationary pressures in the housing market have been more significant. Here annual price inflation ran at close to 20 per cent in the second and third quarters of the year. Given that the average house price in London is currently £510,000, this means a Stamp Duty saving of £4,900 or 24 per cent. Of course, for premium London markets (and other similar markets elsewhere) a quite different effect could arise. The liability on a £2m property rises by 53.75 per cent. Nonetheless, for most markets it is the boost to prices that is most concerning.

In the East Midlands, which is a good barometer of the market in the rest of the country, there will be a saving of £610 or 32 per cent on the current average property purchase of £189,000. Therefore, even in markets where house price inflation is more subdued there is the potential that the changes to the Stamp Duty system will, in the short term at least, boost housing demand and fuel house price growth.

Stamp Duty/Land and Buildings Transactions Tax

Rates and allowances: Stamp Duty Land Tax Gov.UKLand and Buildings Transaction Tax Revenue Scotland

Autumn Statement

Autumn Statement: documents Gov.UK

Articles

The home owners cashing in on stamp duty reforms Telegraph, Dan Hyde (2/12/14)

Christmas comes early for estate agents after stamp duty changes Guardian, Nigel Bunyan (7/12/14)

Stamp duty: House price boom and mansion bust Telegraph, Anna White (6/12/14)

£200m house deal stampede by wealthy to beat stamp duty hike: Reforms spark one of busiest periods for estate agents in 25 years Daily Mail Online, Louise Eccles and Ruth Lythe (5/12/14)

Stamp duty changes boost housing market and push up prices Guardian, Hilary Osborne (5/12/14)

Stamp Duty revamp blow to SNP property tax reforms Scotsman, Tom Peterkin and Jane Bradley (4/12/14)

Autumn Statement: What do stamp duty changes mean? BBC News, (3/12/14)

Autumn Statement: What do stamp duty changes mean? BBC News, (3/12/14)

Data

House Price Indices: Data Tables Office for National Statistics

Questions

- What is the tax base of Stamp Duty and the Land and Buildings Transaction Tax?

- How does Stamp Duty distort choices?

- Under the old Stamp Duty system, why might a seller be reluctant to put their property on the market at £251,000?

- What is meant by the average and marginal rates of tax?

- What is meant by a progressive tax?

- What is the connection between the average rate of tax and how progressive a tax is?

- Calculate the marginal rates of tax (in percentage terms) under the old Stamp Duty system following a £1 rise which results in a property’s value moving into the next tax band (start with a £1 rise from £125,000 to £125,001).

- Using a demand-supply diagram show the effect of the Stamp Duty reforms on house prices in most UK housing markets. What characteristics of supply would make the change in price particularly large?

- Are there any housing markets where demand could fall following the introduction of the reforms to Stamp Duty? Illustrate the possible effects using a demand-supply diagram.

- How might an economist go about evaluating the Stamp Duty reforms? What factors will affect the judgement formed?

The housing market was at the heart of the 2014 Autumn Statement. Perhaps most eyecatching were the reforms to stamp duty. Stamp Duty is a tax on house purchases. Overnight we have seen the introduction of a graduated system of tax, along the lines of the income tax system – similar to the model to be adopted in Scotland from next April under the Land and Buildings Transactions Tax. For the rest of the UK, there will be five tax bands, including a zero rate band for property values up to £125,000. The total tax liability will be dependent upon the proportion of the value of the property that falls in each taxable band.

The housing market was at the heart of the 2014 Autumn Statement. Perhaps most eyecatching were the reforms to stamp duty. Stamp Duty is a tax on house purchases. Overnight we have seen the introduction of a graduated system of tax, along the lines of the income tax system – similar to the model to be adopted in Scotland from next April under the Land and Buildings Transactions Tax. For the rest of the UK, there will be five tax bands, including a zero rate band for property values up to £125,000. The total tax liability will be dependent upon the proportion of the value of the property that falls in each taxable band.

But, alongside the Stamp Duty announcement, the Autumn Statement was noteworthy for its references to new build. New build is clearly central to UK housing policy.

The Autumn Statement reaffirmed the government’s wish to see house building play a central role in easing pressures on the housing market. Over the past 40 years or more UK house prices have been characterised by considerable volatility and by a significant real increase. This can be seen clearly in the chart.  Actual (nominal) house prices across the UK have grown an average rate of 10 per cent per year. Even if we strip out the effect of economy-wide inflation, we are still left with an increase of around 3.5 per cent per year. (Click here to download a PowerPoint of the chart).

Actual (nominal) house prices across the UK have grown an average rate of 10 per cent per year. Even if we strip out the effect of economy-wide inflation, we are still left with an increase of around 3.5 per cent per year. (Click here to download a PowerPoint of the chart).

The economics point to supply-side problems that mean demand pressures feed directly into house prices. The commitment to build has now seen the announcement of a new garden city near Bicester in Oxfordshire. This is set to provide 13,000 or more new homes. The government has also pledged £100 million to the Ebbsfleet Garden City project to provide the infrastructure and land remediation necessary to bring in more private-sector developers to help deliver an expected 15,000 new homes.

An interesting development in housing policy is the willingness of government to consider being more actively involved itself in house building. The development of former barracks at Northstowe in Cambridgeshire will be spearheaded by the Homes and Communities Agency which will lead on the planning and construction of up to 10,000 new homes. This signals, at least on paper, that government is prepared to think more broadly about the way in which it works with the private sector in helping to deliver new homes.

An interesting development in housing policy is the willingness of government to consider being more actively involved itself in house building. The development of former barracks at Northstowe in Cambridgeshire will be spearheaded by the Homes and Communities Agency which will lead on the planning and construction of up to 10,000 new homes. This signals, at least on paper, that government is prepared to think more broadly about the way in which it works with the private sector in helping to deliver new homes.

The desire to facilitate new build appears to make some economic sense. But, the politics of delivering on new homes is considerably more difficult since the prospect of new developments naturally raises considerable local concerns. Furthermore, it does not deal with fundamental questions around the existing housing market stock. In particular, how we can further increase investment in our existing housing stock, especially given the significant land constraints that face a country like the UK. As yet, the debate around how to improve what we already have has not really taken place.

Autumn Statement

Autumn Statement: documents Gov.UK

Articles

Autumn Statement: Government will build tens of thousands of new homes Independent, Nigel Morris (2/12/14)

Government could build and sell new homes on public sector land Guardian, Patrick Wintour (2/12/14)

Bicester chosen as new garden city with 13,000 homes BBC News, (2/12/14)

Nick Clegg reveals coalition plan for new garden city in Oxfordshire Guardian, (2/12/14)

State to build new homes for first time in generation Telegraph, Steven Swinford (2/12/14)

Data

House Price Indices: Data Tables Office for National Statistics

Questions

- Explain the distinction between real and nominal house prices.

- Would you expect real house price inflation to always be less than nominal house price inflation?

- What factors are likely to affect housing demand?

- What factors are likely to affect housing supply?

- Show using a demand-supply diagram the impact of rising incomes on the demand for a particular housing market characterised by a price inelastic supply.

- Would we expect all housing markets to exhibit similar characteristics of housing demand and supply?

- What is the economic rationale for the government’s new build policy?

- What other measures could be introduced to try and alleviate the long-term pressure on real house prices?

- How might we go about assessing the affordability of housing?

- Would a policy which reduced for the stamp duty payment of most buyers help to curb inflationary pressures in the housing market? Explain your answer using a demand-supply diagram.

The typical UK high street is changing. Some analysts have been arguing for some time that high streets are dying, with shops unable to face the competition from large supermarkets and out-of-town malls. But it’s not all bad news for the high street: while some types of shop are disappearing, others are growing in number.

The typical UK high street is changing. Some analysts have been arguing for some time that high streets are dying, with shops unable to face the competition from large supermarkets and out-of-town malls. But it’s not all bad news for the high street: while some types of shop are disappearing, others are growing in number.

Part of the reason for this is the rise in online shopping; part is the longer-term effects of the recession. One consequence of this has been a shift in demand from large supermarkets (see the blog, Supermarket wars: a pricing race to the bottom). Many people are using local shops more, especially the deep discounters, but also the convenience stores of the big supermarket chains, such as Tesco Express and Sainsbury’s Local. Increasingly such stores are opening in shops and pubs that have closed down. As The Guardian article states:

The major supermarket chains are racing to open high street outlets as shoppers move away from the big weekly trek to out-of-town supermarkets to buying little, local and often.

Some types of shop are disappearing, such as video rental stores, photographic stores and travel agents. But other types of businesses are on the increase. In addition to convenience stores, these include cafés, coffee shops, bars, restaurants and takeaways; betting shops, gyms, hairdressers, phone shops and tattoo parlours. It seems that people are increasingly seeing their high streets as social places.

Then, reflecting the widening gap between rich and poor and the general desire of people to make their money go further, there has been a phenomenal rise in charity shops and discount stores, such as Poundland and Poundworld.

So what is the explanation? Part of it is a change in tastes and fashions, often reflecting changes in technology, such as the rise in the Internet, digital media, digital photography and smart phones. Part of it is a reflection of changes in incomes and income distribution. Part of it is a rise in highly competitive businesses, which challenge the previous incumbents.

But despite the health of some high streets, many others continue to struggle and the total number of high street stores across the UK is still declining.

What is clear is that the high street is likely to see many more changes. Some may die altogether, but others are likely to thrive if new businesses are sufficiently attracted to them or existing ones adapt to the changing market.

How the rise of tattoo parlours shows changing face of Britain’s high streets The Guardian, Zoe Wood and Sarah Butler (7/10/14)

The changing face of the British High Street: Tattoo parlours and convenience stores up, but video rental shops and travel agents down Mail Online, Dan Bloom (8/10/14)

High Street footfall struggles in August Fresh Business Thinking, Jonathan Davies (15/9/14)

Ghost town Britain: Internet shopping boom sees 16 high street stores close every day Mail Online, Sean Poulter (8/10/14)

Questions

- Which of the types of high street store are likely to have a high income elasticity of demand? How will this affect their future?

- What factors other than the types of shops and other businesses affect the viability of high streets?

- What advice would you give your local council if it was keen for high streets in its area to thrive?

- Why are many large superstores suffering a decline in sales? Are these causes likely to be temporary or long term?

- How are technological developments affecting high street sales?

- What significant changes in tastes/fashions are affecting the high street?

- Are you optimistic or pessimistic about the future of high streets? Explain.

Merlin Entertainments PLC is one of the largest operator of visitor attractions in the world and owns over a third of the most popular theme parks in Europe. It runs the four most visited parks in England – Alton Towers, Legoland Windsor, Thorpe Park and Chessington World of Adventures as well as the most popular theme park in Italy – Gardaland. Alton Towers alone had 2.5 million visitors in 2013. Anybody thinking of going to one of these attractions is faced with a wide range of different entry fees .

Merlin Entertainments PLC is one of the largest operator of visitor attractions in the world and owns over a third of the most popular theme parks in Europe. It runs the four most visited parks in England – Alton Towers, Legoland Windsor, Thorpe Park and Chessington World of Adventures as well as the most popular theme park in Italy – Gardaland. Alton Towers alone had 2.5 million visitors in 2013. Anybody thinking of going to one of these attractions is faced with a wide range of different entry fees .

Theme parks and tourist attractions have market power so their owners have to make some interesting pricing decisions. They have to tackle the same dilemma that confronts any seller that faces a downward sloping demand curve for its goods/services.

One option for the firm would be to increase the entry fee. This would produce higher profits per visitor as some of the surplus from the transaction previously enjoyed by the consumer will be extracted by the seller and converted into producer surplus. Unfortunately for the business the higher price, all other things equal, will also result in fewer visitors. Some people will be deterred from visiting because of the higher price and the seller will lose out on potential revenue.

An alternative strategy would be for the theme park to reduce its entry fee. All other things equal, this will increase the number of visitors. However, it would also mean that the profit per customer would fall. The frustrating issue for the seller is that some of its customers, who would still have visited the attraction at the higher price, are now able to get a better deal.

This dilemma exists if the seller has to charge all of its different customers the same entry fee. If it could charge a higher entry fee to those customers who would be willing to pay more and a lower entry fee to those who would be willing to pay less then it could make more money. Extra revenue could be obtained from those additional sales that take place at the lower price while more consumer surplus could be extracted from those still paying the higher price.

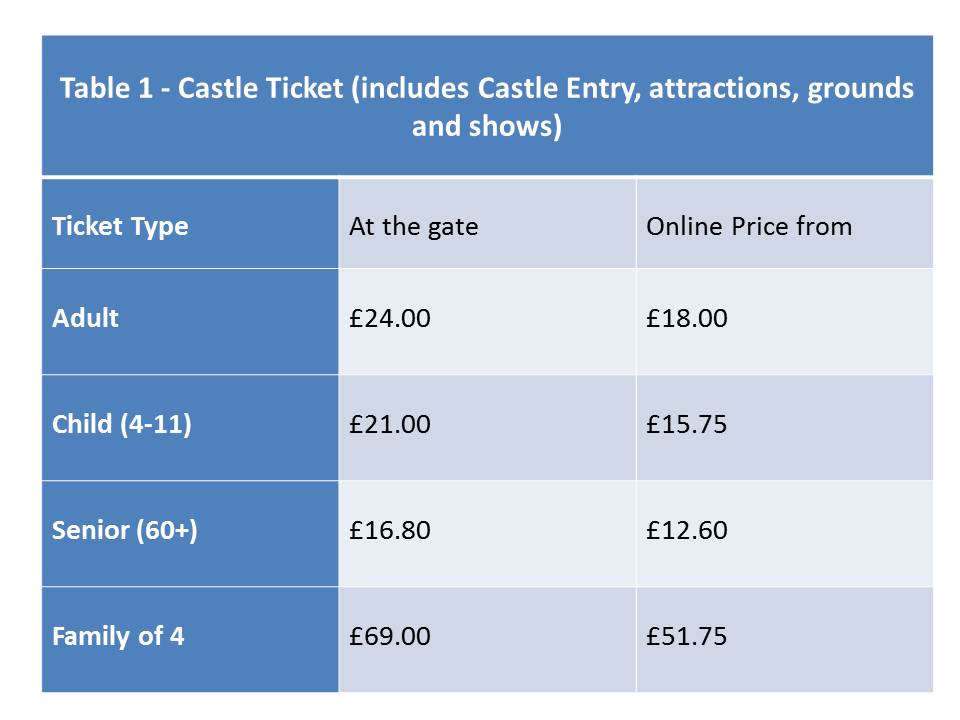

Is it possible for a firm to charge different prices to different customers for the same or a similar good or service? Table 1 below shows the entry fees for Warwick Castle, another tourist attraction owned by Merlin Entertainments PLC.

It can immediately be seen from this table that some groups of customers pay a different entry fee from others. For example adults have to pay £24 to enter on the day while people aged 60 and over pay a lower price £16.80. The entry fee for children aged between 4 and 11 is £21.00 while those aged 3 and under go for free. Students aged 16-18 can gain entry for a price of £13.50 if they can provide valid ID and purchase the tickets from the visitbritainshop website.

In this example, the company has allocated people into different categories by age (i.e. senior, adult, student, older children and younger children) and has set the entry fee that customers in each group have to pay.

The table also shows that if customers purchase on- line then they can get the tickets more cheaply. The entry fee for each category is 25% lower if the ticket is booked seven days in advance i.e. the prices shown in the last column in the table. If the booking is made between 2-6 days in advance then the discount is only 10% i.e. an adult ticket would cost £21.60. The on-line discounts are open to everyone. People are given the choice to either book on-line in advance or pay on the day. This is different from a situation where you are placed into a category by the firm. For example the customer cannot choose whether they are over 60!

If people are prepared to spend more time searching on the internet then other cheaper prices can also be obtained. Once again these offers are open to anyone willing to spend the time and effort in order to find them.

All the ticket prices above give people access to exactly the same attractions on the day. They do not give the visitor access to two of the attractions at the castle – the Dragon Tower and Castle Dungeon. Entry to the Dragon Tower would cost an adult on the day an extra £1.80 while entry to the Castle Dungeon would cost an extra £5.40.

Warwick Castle Ticket Prices Warwick Castle (accessed on 04/09/14)

Alton Towers Alton Towers (accessed on 08/09/14)

Warwick Castle Tickets visitbritainshop (accessed on 02/09/14)

Global Attractions Attendance Report teaconnect (accessed on 05/09/14)

Merlin Entertainments Merlin Entertainments (accessed on 08/09/14)

Questions

- What pricing decisions do firms have to make if they operate in a perfectly competitive market?

- Explain why an individual tourist attraction will have a downward sloping demand curve

- Paying an entry fee and an extra payment per attraction is known as what type of pricing? What advantages does this type of price strategy have for the seller?

- How would you calculate the profit per customer? What factors other than the entrance fee would determine the profit made per customer in a theme park or tourist attractions?

- Paying a different price depending on which category you have been assigned to by the seller is known as what type of pricing strategy? Can this type of pricing strategy ever be in the interests of society?

- In the example used in the case, customers are assigned to different categories by age. Can you think of any other ways that firms could categorise their customers?

- Given the category customers have been assigned to they can pay different prices depending on whether they buy the tickets on line. What is the price strategy called when customers can choose from a variety of pricing options for the same or similar product? Can you think of any different methods that could be used by the seller to carry out this type of pricing strategy?

They may not have been happy about it but the executives of Manchester City have finally agreed a settlement with UEFA after it was judged that the club had broken Financial Fair Play (FFP) rules. The club had initially indicated that they might take their case to the Club Financial Control Body’s adjudicatory chamber. For details about FFP, see previous article on the website: What does ‘fair play’ mean for the big teams in Europe?They have also now accepted the sanctions for breaking these rules which appear to be very similar in magnitude to those imposed on Paris St-Germain. UEFA have also judged that seven other clubs have failed to meet their financial requirements.

They may not have been happy about it but the executives of Manchester City have finally agreed a settlement with UEFA after it was judged that the club had broken Financial Fair Play (FFP) rules. The club had initially indicated that they might take their case to the Club Financial Control Body’s adjudicatory chamber. For details about FFP, see previous article on the website: What does ‘fair play’ mean for the big teams in Europe?They have also now accepted the sanctions for breaking these rules which appear to be very similar in magnitude to those imposed on Paris St-Germain. UEFA have also judged that seven other clubs have failed to meet their financial requirements.

Why did Manchester City fail the FFP rules when they appeared to be so confident that they would meet them? To understand this requires some discussion of a number of exemptions put in place by UEFA in the implementation of the FFP guidelines.

One of the key aims of FFP is to force the clubs who compete in European competitions to break even. However UEFA allow clubs to make some losses before any sanctions are applied. For the current monitoring period the clubs are allowed to make a cumulative loss of up to €45 million (approximately £37 million) over a two year period from 2011-2013 before any penalties are imposed. This permitted loss is referred to by UEFA as the ‘acceptable deviation’ from breaking even.

Manchester City reported losses in their financial accounts of £97million in 2011-12 and £51.6 million in 2012-13. At first sight this cumulative loss of nearly £149 million over the two year period would suggest that the club failed to meet the FFP regulations by a wide margin i.e. £112 million over the acceptable deviation. However the size of either the profit or loss reported in a club’s final accounts is different from the figure that is used by UEFA when assessing whether the teams have met the FFP criteria. UEFA exclude any costs incurred by the clubs on

– Youth development and community projects

– Building/developing their stadiums

Imagine a situation where after deducting these costs, Manchester City’s losses fell to £75 million in 2011-12 and £35 million in 2012-13. Once again it would still look as if they have failed to meet the FFP guidelines by a large margin. However there is another set of costs that can be excluded if a number of conditions are met. These are the wage costs in 2011-12 of those players who had signed contracts with the club before 1st June 2010. This exemption was introduced by UEFA because a number of clubs complained that they would struggle to meet the rules because of the nature of the players’ contracts. It is quite common for these to be of a 4 or 5 year duration. The teams argued that they were already committed to paying some players very large salaries in 2011-12 because of deals that were agreed long before the FFP rules were introduced. UEFA accepted this argument but only allowed the wage costs to be exempted from the FFP calculations on two conditions:

1. The club could show that the size of its losses were falling over time and that they had a clear strategy in place so that they would be able to comply with FFP regulations in future years.

2. The cumulative loss in excess of the acceptable deviation was caused by losses incurred in the 2011-12 period.

As there is a downward trend in the size of the losses being made by Manchester City they would appear to meet the first condition. It would also be important for them to convince UEFA that they had policies in place to reduce the losses below the permitted levels in the future. In the example above the second criterion is also met as the loss in 2012-13 of £35 million was lower than the acceptable deviation of £37 million. Therefore the reason why the cumulative permitted loss would be broken is because of the impact of the £75 million loss in 2011-12.

However there is another element to the second condition. The club also has to show that the sole reason for the loss in 2011-12 was because of the wage costs they were already committed to – i.e. from the contracts signed before the 1st June 2010. If these wage costs are smaller than the losses reported in that period then they cannot be exempted from the FFP calculations as they can only partly explain the loss.

Reports in the press have suggested that approximately £80 million of Manchester City’s wage bill in 2011-12 was caused by contracts that were signed with players before the 1st June 2010. If this was true then in the example above they would have met the FFP requirements as the £80 million of wages could fully account for the £75 million loss in the 2011-12 season. This would mean that the £80 million could be exempted from the FFP calculation and City would have made a cumulative loss of £35 million which was less than the acceptable deviation of £37 million.

If the wages paid to the players from the contracts signed prior to 1st June 2010 could not fully account for the losses in 2011-12 then they could not be deducted in the FFP calculations. For example imagine if after deducting the costs of youth/community projects and infrastructure spending that Manchester City’s loss had been £85 million in 2011-12 instead of £75 million. The wages bill of £80 million could not fully account for this loss of and hence the £80 million wage bill would be counted in the calculations. The cumulative loss would now be £120 million (£85 million + £35 million) and the acceptable deviation would have been exceeded by £83 million.

Unfortunately for Manchester City this appears to be more or less what happened. As part of the FFP process UEFA also examined deals struck between the club and other organisations in which the owner had an interest. These are referred to by UEFA as Related Party Transactions (RPTs). It would seem that the accountants at UEFA came to the conclusion that some of these RPTs were at above market prices. Interestingly some press reports have indicated that the £35 million a year deal with Etihad was judged to be fine. It was a number of secondary sponsorship deals which were considered to be above fair market values. Once adjustments were made to take account of this it looks as if the re-calculated losses for 2011-12 were greater than the £80 million of wages. With these wage costs not exempted from the calculation, Manchester City have been judged to have missed the FFP conditions by a wide margin.

The following quote is taken from a statement released by the club:

At the heart of the discussions is a fundamental disagreement between the club’s and UEFA’s respective interpretations of the FFP regulations on players purchased before 2010.

The following sanctions have been imposed:

– A £49 million fine to be withheld from UEFA prize money over the next three seasons. (£32 million is suspended and depends on their financial performance in future years)

– A limit on the squad size for the Champions League – 21 instead of 25 players

– Spending limited on transfers this summer to £49 million plus any revenue received in transfer fees from the sale of players

– A freeze on the wage bill of the Champions League squad for the next two seasons

It will be interesting to see if these penalties significantly constrain Manchester City’s ability to compete with the other big teams in Europe next season.

Articles

Manchester City accept world-record £50m fine for breach of Uefa Financial Fair Play rules The Telegraph, (16/5/14)

Manchester City facing £50m fine for breaching Uefa’s Financial Fair Play regulations The Telegraph, (6/5/14)

A beginner’s guide to UEFA’s financial fair play regulations SB Nation, (30/04/14)

Financial Fair Play Explained Financial Fair Play 2012

Man City to act swiftly in transfer market – Khaldoon Al Mubarak BBC Sport, (20/5/14)

Manchester City fined and squad capped for FFP breach BBC Sport, (16/5/14)

Manchester City facing Uefa sanctions over finances BBC Sport, (6/5/14)

Paris St-Germain’s £167m deal fails Uefa financial fair play rules BBC Sport, (1/5/14)

Manchester City and PSG breach Uefa FFP rules BBC Sport, (28/4/14)

Financial Fair Play: What rules have Manchester City broken and what are the likely sanctions? The Mirror, (6/5/14)

We’re innocent! Manchester City on the attack over FFP penalties The Express, (21/5/14)

Man City facing double UEFA punishment for breaching financial fair play rules talkSPORT, (6/5/14) .

Questions

- What are barriers to entry? Give 4 examples.

- What impact do barriers to entry have on a market? Draw a diagram to illustrate your answer.

- To what extent do you think that the UEFA Fair Play Rules act as a barrier to entry?

- What impact do you think the FFP rules will have on the marginal revenue product of the most talented players? Draw a diagram to illustrate your answer.

- Can you think of any methods that a club might use to try and circumvent a rule that attempts to restrict the size of its wage bill.

As we reported in New Build: Foundations for a successful housing policy? the Autumn Statement heralded significant reforms to Stamp Duty – the UK tax on house purchases. The result is the introduction of a graduated system of tax, along the lines of the income tax system. A similar regime will continue to operate in Scotland when the Land and Buildings Transactions Tax replaces Stamp Duty next April. Here we consider the impact on the effective rates of tax following the changes to Stamp Duty.

As we reported in New Build: Foundations for a successful housing policy? the Autumn Statement heralded significant reforms to Stamp Duty – the UK tax on house purchases. The result is the introduction of a graduated system of tax, along the lines of the income tax system. A similar regime will continue to operate in Scotland when the Land and Buildings Transactions Tax replaces Stamp Duty next April. Here we consider the impact on the effective rates of tax following the changes to Stamp Duty.