With the bounce-back from the pandemic, many countries have experienced supply-chain problems. For example, the shortage of lorry drivers in the UK and elsewhere (see the blog Why is there a driver shortage in the UK?) has led to empty shelves, fuel shortages and rising prices. The problem has been exacerbated by a lack of stock holding. Holding minimum stocks has been part of the modern system of ‘just-in-time’ (JIT) supply-chain management.

With the bounce-back from the pandemic, many countries have experienced supply-chain problems. For example, the shortage of lorry drivers in the UK and elsewhere (see the blog Why is there a driver shortage in the UK?) has led to empty shelves, fuel shortages and rising prices. The problem has been exacerbated by a lack of stock holding. Holding minimum stocks has been part of the modern system of ‘just-in-time’ (JIT) supply-chain management.

JIT involves involves highly integrated and sophisticated supply chains. Goods are delivered to factories, warehouses and shops as they are needed – just in time. Provided firms can be sure that they will get their deliveries on time, they can hold minimum stocks. This enables them to cut down on warehousing and its associated costs. The just-in-time approach to supply-chain management was developed in the 1950s in Japan and since the 1980s has been increasingly adopted around the world, helped more recently by sophisticated ordering and tracking software.

If supply chains become unreliable, however, JIT can lead to serious disruptions. A hold-up in one part of the chain will have a ripple effect along the whole chain because there is little or no slack in the system. When the large container ship, the Ever Given, en route from Malaysia to Felixtowe, was wedged in the Suez canal for six days in March this year, the blockage caused shipping to be backed up. By day six, 367 container ships were waiting to transit the canal. The disruption to supply cost some £730m.

If supply chains become unreliable, however, JIT can lead to serious disruptions. A hold-up in one part of the chain will have a ripple effect along the whole chain because there is little or no slack in the system. When the large container ship, the Ever Given, en route from Malaysia to Felixtowe, was wedged in the Suez canal for six days in March this year, the blockage caused shipping to be backed up. By day six, 367 container ships were waiting to transit the canal. The disruption to supply cost some £730m.

JIT works well when sources of supply and logistics are reliable and when demand is predictable. The pandemic is causing many logistics and warehousing managers to consider building a degree of slack into their systems. This might involve companies having alternative suppliers they can call on, building in more spare capacity and having their own fleet of lorries or warehousing facilities that can be hired out when not needed but can be relied on at times of high demand.

When the ‘bounce back’ subsides, so may the current supply chain bottlenecks. But the rethinking that has been generated by the current problems may see new patterns emerge that make supply chains more flexible without becoming more expensive.

Articles

- What Is a Just-in-Time Supply Chain?

The Balance Small Business, Martin Murray (12/10/20)

- Why it’s high time to move on from ‘just-in-time’ supply chains

The Guardian, Kim Moody (11/10/21)

- Logistics Study Reveals Three Potential Cures To Global Supply Chain Problems

Forbes, Garth Friesen (20/9/21)

- Just-in-Time Manufacturing Needs Better Data

Supply & Demand Chain Executive, Paul Lachance (8/10/21)

- Just-in-time supply chains after the Covid-19 crisis

VoxEU, Frank Pisch (30/6/20)

- Plastics industry moves away from just-in-time logistics amid increased volatility

S&P Global, Miguel Cambeiro, Baoying Ng and George Griffiths (8/10/21)

- Just-in-time supply chains have left us dependent and with just-not-enough

CityAM, Tom Tugendhat MP (1/10/21)

- Supply chain havoc is getting worse — just in time for holiday shopping

Vox, Rebecca Heilweil (7/10/21)

- Ever Given and the Suez Canal: A list of affected ships and what delays mean for shippers

Supply Chain Dive, Matt Leonard (25/3/21)

Questions

- What are the costs and benefits of a just-in-time approach to logistics?

- Are current supply chain problems likely to be temporary or are there issues that are likely to persist?

- How might the JIT approach be reformed to make it more adaptable to supply chain disruptions?

So here we are, summer is over (or almost over if you’re an optimist) and we are sitting in front of our screens reminiscing about hot sunny days (at least I do)! There is no doubt, however: a lot happened in the world of politics and economics in the past three months. The escalation of the US-China trade war, the run on the Turkish lira, the (successful?) conclusion of the Greek bailout – these are all examples of major economic developments that took place during the summer months, and which we will be sure to discuss in some detail in future blogs. Today, however, I will introduce a topic that I am very interested in as a researcher: the liberalisation of energy markets in developing countries and, in particular, Mexico.

So here we are, summer is over (or almost over if you’re an optimist) and we are sitting in front of our screens reminiscing about hot sunny days (at least I do)! There is no doubt, however: a lot happened in the world of politics and economics in the past three months. The escalation of the US-China trade war, the run on the Turkish lira, the (successful?) conclusion of the Greek bailout – these are all examples of major economic developments that took place during the summer months, and which we will be sure to discuss in some detail in future blogs. Today, however, I will introduce a topic that I am very interested in as a researcher: the liberalisation of energy markets in developing countries and, in particular, Mexico.

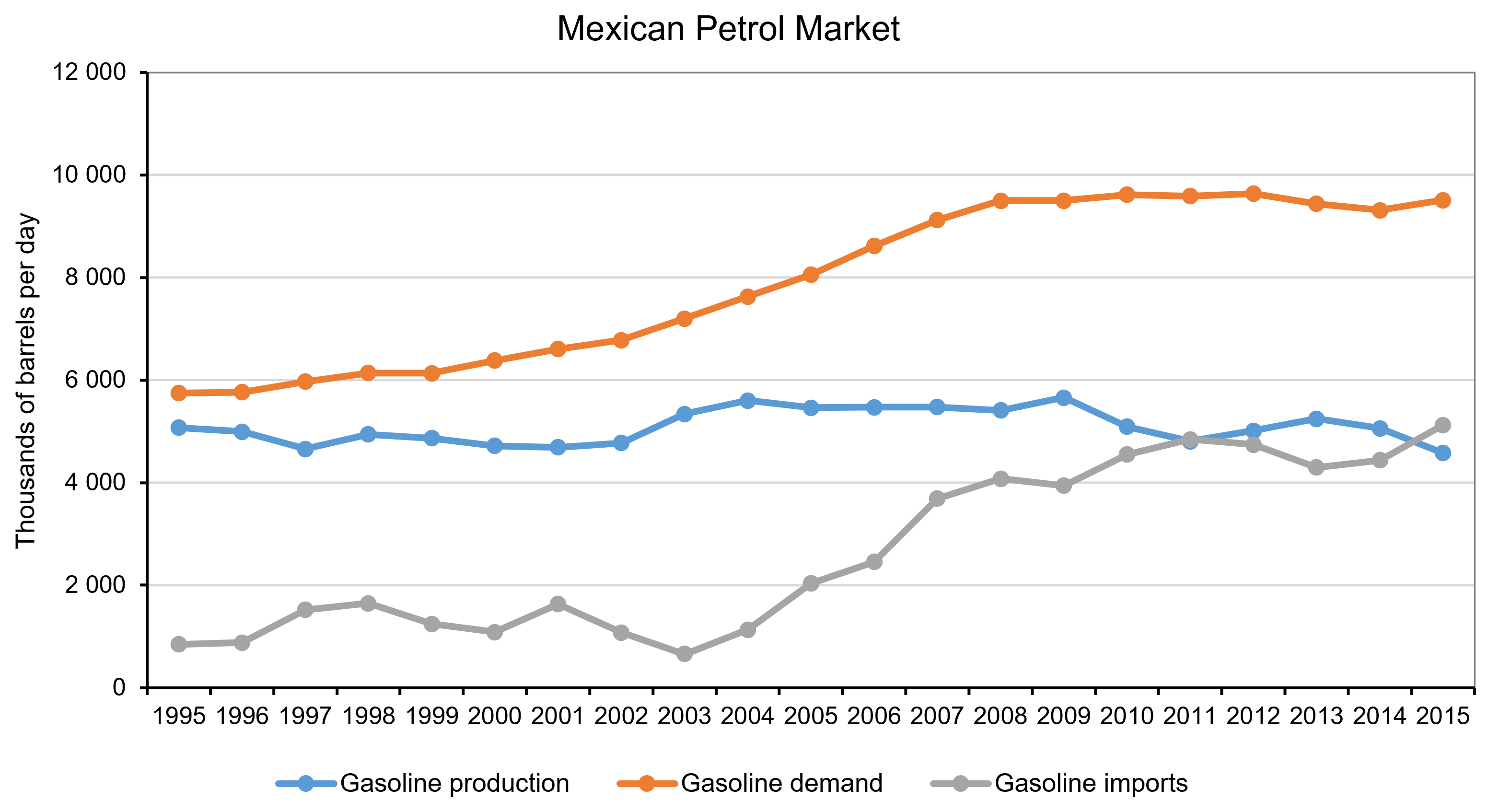

Why Mexico? Well, because it is a great example of a large developing economy that has been attempting to liberalise its energy market and reverse price setting and monopolistic practices that go back several decades. Until very recently, the price of petrol in Mexico was set and controlled by Pemex, a state monopolist. This put Pemex under pressure since, as a sole operator, it was responsible for balancing growing demand and costs, even to the detriment of its own finances.

The petrol (or ‘gasoline’) price liberalisation started in May 2017 and took place in stages – starting in the North part of Mexico and ending in November of the same year in the central and southern regions of the country. The main objective was to address the notable decrease in domestic oil production that put at risk the ability of the country to meet demand; as well as Mexico’s increasing dependency on foreign markets affected by the surge of the international oil price. The government has spent the past five years trying to create a stronger regulatory framework, while easing the financial burden on the state and halting the decline in oil reserves and production. Unsurprisingly, opening up a monopolistic market turns out to be a complex and bumpy process.

Source: Author’s calculations using data from the Energy Information Bank, Ministry of Energy, Mexico

Source: Author’s calculations using data from the Energy Information Bank, Ministry of Energy, Mexico

Despite all the reforms, retail petrol prices have kept rising. Although part of this price rise is demand-driven, an increasing number of researchers highlight the significance of the distribution of oil-related infrastructure in determining price outcomes at the federal and regional (state) level. Saturation and scarcity of both distribution and storage infrastructure are probably the two most significant impediments to opening the sector up to competition (Mexico Institute, 2018). You see, the original design of these networks and the deployment of the infrastructure was not aimed at maximising efficiency of distribution – the price was set by the monopolist and, in a way that was compliant with government policy (Mexico Institute, 2018). Economic efficiency was not always part of this equation. As a result, consumers located in better-deployed areas were subsidising the inherent logistics costs of less ‘well endowed’ regions by facing an artificially higher price than they would have in a competitive market.

But what about now? Do such differences in the allocation of infrastructure between regions lead to location-related differences in the price of petrol? If so, by how much? And, what policies should the government pursue to address such imbalances? These are all questions that I explore in one of my recent working papers titled ‘Widening the Gap: Lessons from the aftermath of the energy market reform in Mexico’ (with Hugo Vallarta) and I will be sharing some of the answers with you in a future blog.

Articles

Data

Questions

- Are state-owned monopolies effective in delivering successful market outcomes? Why yes, why no?

- In the case of Mexico, are you surprised about the complexities that were involved with opening up markets to competition? Explain why.

- Use Google to identify countries in which energy markets are controlled by state-owned monopolies.

Ginsters is a large producer of pasties in Cornwall. Most of its ingredients come from Cornwall, but the pasties are sold throughout Britain. But, not surprisingly, they are also sold in Cornwall. In fact, there is a large Tesco virtually next door to the Ginsters’ pasty plant and, as you can imagine, it does a good trade in Ginsters’ pasties, pies and sandwiches. After all, they are a local product.

But are they delivered directly from the Ginsters’ factory? No they are not. In fact, they are sent by lorry to the Avonmouth distribution depot, some 125 miles away, only to be sent back again to the Tesco supermarket next door! So does it make economic sense to incur all the costs of transporting the pasties 250 miles only to end up virtually where they started?

It is a similar story with Rodda’s Cornish clotted cream. It is made with Cornish milk but is also sold nationwide. In this case it is transported some 340 miles to get to another Tesco supermarket virtually next door to the Rodda plant.

The following articles and podcast consider the logistics of manufactured food distribution, and ask whether private costs are the only thing that should be taken into account when judging the sense of the system.

Articles

From here to eternity: 340-mile journey for clotted cream made two miles away Guardian, Steven Morris (3/9/10)

Food miles row as pasties travel 250 miles to the supermarket next door This is Cornwall (30/8/10)

Supermarket food mileage ‘completely bonkers’ BBC Today Programme, Tim Lang (30/8/10)

Supermarket food mileage ‘completely bonkers’ BBC Today Programme, Tim Lang (30/8/10)

Questions

- Why does Tesco’s distribution system for pasties, clotted cream and other products made in parts of the country away from large centres of population make sense in ‘conventional economic terms’?

- What economies of scale are there in pasty production and distribution?

- What externalities are involved in the distribution of Ginsters’ pasties?

- Consider the arguments for and against locating mass producers of food products nearer to the ‘centre of gravity’ of markets.