The UK signed three trade deals in May – one with the USA, one with India and one with the EU. It is hoped by the government that these trade deals will provide a welcome boost to the UK economy.

The deal with the USA reduced tariffs on UK car exports to the USA from 27.5% to 10%, and on steel and aluminium exports from 25% to 0%. Pharmaceutical exports would also get more favourable treatment and there would be ‘reciprocal market access on beef’ (but with no lowering of food standards). Nevertheless, President Trump’s baseline tariff of 10% on most goods remains, as with other countries. However, a ruling by the US Court of International Trade has found that the Trump’s use of emergency powers to justify the sweeping use of tariffs is wrong. The Trump administration is appealing against the ruling and until the appeal is heard, the tariffs have been reinstated. Also, on May 30, the Trump administration announced that tariffs on steel and aluminium imports would rise from 25% to 50%. It remained to be seen whether this would affect the deal to reduce the rate to zero for British steel and aluminium imports.

The deal with India involves a reduction in tariffs on UK exports – some to zero – and simplified trade rules, faster customs clearance, less paperwork and the freedom for UK businesses to provide telecommunications and construction services. In return, tariffs will be reduced to zero on 99% of Indian exports to the UK. The UK government estimates that deal will result in trade between the two countries increasing by over 30%, with the UK’s GDP expanding by around 0.1 percentage points per year.

UK-EU trade

Perhaps the most significant new trade deal, however, is with the EU. This is a major advance on the current post-Brexit Trade and Cooperation Agreement (TCA). Under the TCA, there are no tariffs or quotas on UK goods exports to the EU or EU goods exports to the UK. However, to ensure that it is EU and UK business that benefits from these ‘trade preferences’, firms must show that their products fulfil ‘rules of origin’ requirements.

Under rules of origin requirements, when a good is imported into the UK from outside the EU and then has value added to it by processing, packaging, cleaning, remixing, preserving, refashioning, etc., it can only count as a UK good if sufficient value or weight is added. The proportions vary by product, but generally goods must have approximately 50 per cent UK content (or 80 per cent of the weight of foodstuffs) to qualify for tariff-free access to the EU. As a result, many goods exported to the EU with a proportion of imported components face tariffs.

Also, the TCA does not include free trade in services. The UK is a major exporter of services, including legal, financial, accounting, IT and engineering. It has a positive trade in services balance with the EU, unlike its negative trade in goods balance. Although some of the barriers which apply to other non-EU countries have been reduced for the UK in the TCA, UK service providers still face barriers which impose costs. For example, some EU countries limit the time that businesspeople providing services can stay in their countries to six months in any twelve. Also, since Brexit, UK artists and musicians have faced restrictions when touring and working in the EU. They can only work up to 90 out of every 180 days. This causes problems for longer tours and for musicians and crew who work in multiple bands or orchestras.

Perhaps the greatest barrier to trade under the TCA has been the large range of non-tariff measures (NTMs), such as customs checks, rules-of-origin and other paperwork, meeting various regulations and standards, and sanitary and phytosanitary checks on foodstuffs, plants and animals. Both the OBR and the Bank of England estimate that these post-Brexit trade restrictions are reducing UK GDP by around 4% and will continue to do so unless trade with the EU becomes freer.

The new UK-EU trade deal

The deal struck in mid-May reduces many of the administrative barriers to trade. Perhaps the most significant are the border checks on food, animal and plant shipments to and from the EU. Many of these checks will be scrapped. The new sanitary and phytosanitary (SPS) agreement allows many UK food products to be exported that previously were banned or proved too administratively costly. To achieve this free movement, the UK will generally follow EU standards, or similar standards so as to avoids harming EU trade. UK food exporters have generally welcomed the deal.

British steel exports to the EU will be protected from new EU rules and tariffs. This should save UK steel some £25m per year. Also, the EU has agreed to recognise UK carbon emissions caps, meaning that UK exports to the EU will avoid around £800m of carbon border taxes.

The post-Brexit fishing deal between the UK and EU, which saw a reduction of 25% in EU fishing quotas in UK waters, will be extended for another 12 years. Many UK fishers, however, had hoped for scrapping EU access to UK waters. The deal also allows various sea foods, including certain shellfish, to be exported to the EU for the first time since Brexit.

Other elements of the deal include a new security and defence partnership, the use of e-gates for UK travellers to the EU and an agreement to work towards a young person’s mobility scheme, allowing young people from the UK/EU to work and travel freely in the EU/UK again for a period of time.

The elements of the deal concerned with trade represent freer trade, but not totally free trade. The UK is not rejoining the customs union or single market. Nevertheless, strong supporters of Brexit have criticised the deal as a movement towards greater alignment of standards and thus a dilution of UK sovereignty. Supporters of greater alignment, on the other hand, argue that the deal does not go far enough and that even freer trade and less red tape would bring greater benefits to the UK.

Outline the main elements of (a) the UK-US trade deal, (b) the UK-India trade deal and (c) the UK-EU trade deal. How much is it claimed that each deal will add to UK GDP?

What trade barriers remain in each of the three deals?

What elements are missing from the UK-EU trade deal that campaigners have been pushing for?

Under what circumstances do free trade deals lead to (a) trade creation; (b) trade diversion?

Would you expect the UK-EU trade deal on balance to lead to trade creation or trade diversion? Explain why.

The EU has recently signed two trade deals after many years of negotiations. The first is with Mercosur, the South American trading and economic co-operation organisation, currently consisting of Brazil, Argentina, Uruguay and Paraguay – a region of over 260m people. The second is with Vietnam, which should result in tariff reductions of 99% of traded goods. This is the first deal of its kind with a developing country in Asia. These deals follow a recent landmark deal with Japan.

At a time when protectionism is on the rise, with the USA involved in trade disputes with a number of countries, such as China and the EU, deals to cut tariffs and other trade restrictions are seen as a positive development by those arguing that freer trade results in a net gain to the participants. The law of comparative advantage suggests that trade allows countries to consume beyond their production possibility curves. What is more, the competition experienced through increased trade can lead to greater efficiency and product development.

It is estimated that the deal with Mercosur could result in a saving of some €4bn per annum in tariffs on EU exports.

But although there is a net economic gain from greater trade, some sectors will lose as consumers switch to cheaper imports. Thus the agricultural sector in many parts of the EU is worried about cheaper food imports from South America. What is more, increased trade could have detrimental environmental impacts. For example, greater imports of beef from Brazil into the EU could result in more Amazonian forest being cut down to graze cattle.

But provided environmental externalities are internalised within trade deals and provided economies are given time to adjust to changing demand patterns, such large-scale trade deals can be of significant benefit to the participants. In the case of the EU–Mercosur agreement, according to the EU Reporter article, it:

…upholds the highest standards of food safety and consumer protection, as well as the precautionary principle for food safety and environmental rules and contains specific commitments on labour rights and environmental protection, including the implementation of the Paris climate agreement and related enforcement rules.

The size of the EU market and its economic power puts it in a strong position to get the best trade deals for its member states. As EU Trade Commissioner, Cecilia Malmström stated:

Over the past few years the EU has consolidated its position as the global leader in open and sustainable trade. Agreements with 15 countries have entered into force since 2014, notably with Canada and Japan. This agreement adds four more countries to our impressive roster of trade allies.

Outside the EU, the UK will have less power to negotiate similar deals.

Draw a diagram to illustrate the gains for a previously closed economy from engaging in trade by specialising in products in which it has a comparative advantage.

Distinguish between trade creation and trade diversion from a trade deal with another country or group of countries.

Which sectors in the EU and which sectors in the Mercosur countries and Vietnam are likely to benefit the most from the respective trade deals?

Which sectors in the EU and which sectors in the Mercosur countries and Vietnam are likely to lose from the respective trade deals?

Are the EU–Mercosur and the EU–Vietnam trade deals likely to lead to net trade creation or net trade diversion?

What are the potential environmental dangers from a trade deal between the EU and Mercosur? To what extent have these dangers been addressed in the recent draft agreement?

Will the UK benefit from the EU’s trade deals with Mercosur and Vietnam?

The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

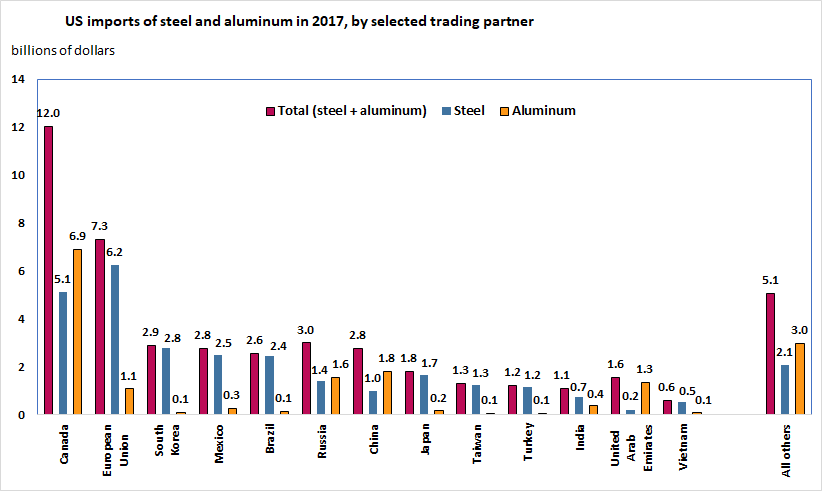

Source: Bown (2018), Figure 1

A number of economists and policymakers are worried that such policies restrict trade and are likely to provoke retaliation by the affected trade partners. In recent statements, the EU has pledged to take counter-measures if the bloc is affected by these policies. In a recent press conference, the Commissioner for Trade, Cecilia Malmstrom, stated that:

We have made it clear that a move that hurts the EU and puts thousands of European jobs in jeopardy will be met with a firm and proportionate response.

She added that, ‘I truly hope that this will not happen. A trade war has no winners.’

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.

A number of studies have attempted to estimate the effect of trade restrictions and tariff wars on welfare: see for instance Anderson and Wincoop (2001), Syropoulos (2002), Fellbermayr et al. (2013). The results vary widely, depending on the case. However, there seems to be consensus that the more similar (in terms of size and industry composition) the adversaries are, the more mutually damaging a trade war is likely to be (and, therefore, less likely to happen).

As Miyagiwa et al (2016, p43) explain:

A country initiates contingent protection policy against a trading partner only if the latter has a considerably smaller domestic market than its own, while avoiding confrontation with a country having a substantially larger domestic market than its own.

As both Canada and the EU are very large advanced market economies, it remains to be seen how much risk (and potential damage to the local and global economy) US trade policymakers are willing to take.

In the light of the Brexit vote and the government’s position that the UK will leave the single market and customs union, there has been much discussion of the need for the UK to achieve trade deals. Indeed, a UK-US trade deal was one of the key issues on Theresa May’s agenda when she met Donald Trump just a week after his inauguration.

But what forms can a trade deal take? What does achieving one entail? What are likely to be the various effects on different industries – who will be the winners and losers? And what role does comparative advantage play? The articles below examine these questions.

Given that up until Brexit, the UK already has free trade with the rest of the EU, there is a lot to lose if barriers are erected when the UK leaves. In the meantime, it is vital to start negotiating new trade deals, a process that can be extremely difficult and time-consuming.

A far as new trade arrangements with the EU are concerned, these cannot be agreed until after the UK leaves the EU, in approximately two years’ time, although the government is keen that preliminary discussions take place as soon as Article 50 is triggered, which the government plans to do by the end of March.

What elements would be included in a UK-US trade deal?

Explain the gains from trade that can result from exploiting comparative advantage.

Explain the statement in the article that allowing trade to be determined by comparative advantage is ‘often politically unacceptable, as governments generally look to protect jobs and tax revenues, as well as to protect activities that fund innovation’.

Why is it difficult to work out in advance the likely effects on trade of a trade deal?

What would be the benefits and costs to the UK of allowing all countries’ imports into the UK tariff free?

What are meant by ‘trade creation’ and ‘trade diversion’? What determines the extent to which a trade deal will result in trade creation or trade diversion?

Theresa May has said that the UK will quit the EU single market and seek to negotiate new trade deals, both with the EU and with other countries. As she said, “What I am proposing cannot mean membership of the single market.” It would also mean leaving the customs union, which sets common external tariffs for goods imported into the EU.

The single market guarantees free movement of goods, services, labour and capital between EU members. There are no internal tariffs and common rules and regulations concerning products, production and trade. By leaving the single market, the UK will be able to restrict immigration from EU countries, as it is currently allowed to do from non-EU countries.

A customs union is a free trade area with common external tariffs and uniform methods of handling imports. There are also no, or only minimal, checks and other bureaucracies at borders between members. The EU customs union means that individual EU countries are not permitted to do separate trade deals with non-EU countries.

Once the UK has left the EU, probably in around two years’ time, it will then be able to have different trade arrangements from the EU with countries outside the EU. Leaving the customs union would mean that the UK would face the EU’s common external tariff or around 5% on most goods, and 10% on cars.

Leaving the EU single market and customs union has been dubbed ‘hard Brexit’. Most businesses and many politicians had hoped that elements of the single market could be retained, such as tariff-free trade between the UK and the EU and free movement of capital. However, by leaving the single market, access to it will depend on the outcome of negotiations.

Negotiations will take place once Article 50 – the formal notice of leaving – has been invoked. The government has said that it will do this by the end of March this year. Then, under EU legislation, there will be up to two years of negotiations, at which point the UK will leave the EU.

The articles look at the nature of the EU single market and customs union and at the implications for the UK of leaving them.

Explain the difference between a free-trade area, a customs union, a common market and a single market.

What arrangement does Norway have with the EU?

How would the UK’s future relationship with the EU differ from Norway’s?

Distinguish between trade creation and trade diversion from joining a customs union. Who loses from trade diversion?

Will leaving the EU mean that trade which was diverted can be reversed?

What will determine the net benefits from new trade arrangements compared with the current situation of membership of the EU?

What are the possible implications of hard Brexit for (a) inward investment and (b) companies currently in the UK of relocating to other parts of the EU? Why is the magnitude of such effects extremely hard to predict?

Explain what is meant by ‘passporting rights’ for financial services firms. Why are they unlikely still to have such rights after Brexit?

Discuss the argument put forward in The Conversation article that ‘Theresa May’s hard Brexit hinges on a dated vision of global trade’.

The UK signed three trade deals in May – one with the USA, one with India and one with the EU. It is hoped by the government that these trade deals will provide a welcome boost to the UK economy.

The UK signed three trade deals in May – one with the USA, one with India and one with the EU. It is hoped by the government that these trade deals will provide a welcome boost to the UK economy. Perhaps the most significant new trade deal, however, is with the EU. This is a major advance on the current post-Brexit Trade and Cooperation Agreement (TCA). Under the TCA, there are no tariffs or quotas on UK goods exports to the EU or EU goods exports to the UK. However, to ensure that it is EU and UK business that benefits from these ‘trade preferences’, firms must show that their products fulfil ‘rules of origin’ requirements.

Perhaps the most significant new trade deal, however, is with the EU. This is a major advance on the current post-Brexit Trade and Cooperation Agreement (TCA). Under the TCA, there are no tariffs or quotas on UK goods exports to the EU or EU goods exports to the UK. However, to ensure that it is EU and UK business that benefits from these ‘trade preferences’, firms must show that their products fulfil ‘rules of origin’ requirements. Also, the TCA does not include free trade in services. The UK is a major exporter of services, including legal, financial, accounting, IT and engineering. It has a positive trade in services balance with the EU, unlike its negative trade in goods balance. Although some of the barriers which apply to other non-EU countries have been reduced for the UK in the TCA, UK service providers still face barriers which impose costs. For example, some EU countries limit the time that businesspeople providing services can stay in their countries to six months in any twelve. Also, since Brexit, UK artists and musicians have faced restrictions when touring and working in the EU. They can only work up to 90 out of every 180 days. This causes problems for longer tours and for musicians and crew who work in multiple bands or orchestras.

Also, the TCA does not include free trade in services. The UK is a major exporter of services, including legal, financial, accounting, IT and engineering. It has a positive trade in services balance with the EU, unlike its negative trade in goods balance. Although some of the barriers which apply to other non-EU countries have been reduced for the UK in the TCA, UK service providers still face barriers which impose costs. For example, some EU countries limit the time that businesspeople providing services can stay in their countries to six months in any twelve. Also, since Brexit, UK artists and musicians have faced restrictions when touring and working in the EU. They can only work up to 90 out of every 180 days. This causes problems for longer tours and for musicians and crew who work in multiple bands or orchestras. The post-Brexit fishing deal between the UK and EU, which saw a reduction of 25% in EU fishing quotas in UK waters, will be extended for another 12 years. Many UK fishers, however, had hoped for scrapping EU access to UK waters. The deal also allows various sea foods, including certain shellfish, to be exported to the EU for the first time since Brexit.

The post-Brexit fishing deal between the UK and EU, which saw a reduction of 25% in EU fishing quotas in UK waters, will be extended for another 12 years. Many UK fishers, however, had hoped for scrapping EU access to UK waters. The deal also allows various sea foods, including certain shellfish, to be exported to the EU for the first time since Brexit. The EU has recently signed two trade deals after many years of negotiations. The first is with

The EU has recently signed two trade deals after many years of negotiations. The first is with  But although there is a net economic gain from greater trade, some sectors will lose as consumers switch to cheaper imports. Thus the agricultural sector in many parts of the EU is worried about cheaper food imports from South America. What is more, increased trade could have detrimental

But although there is a net economic gain from greater trade, some sectors will lose as consumers switch to cheaper imports. Thus the agricultural sector in many parts of the EU is worried about cheaper food imports from South America. What is more, increased trade could have detrimental  The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.