According to the Brexit trade agreement (the Trade and Cooperation Agreement (TCA)), trade between the EU and the UK will remain quota and tariff free. ‘Quota free’ means that trade will not be restricted in quantity by the authorities on either side. ‘Tariff free’ means that customs duties will not be collected by the UK authorities on imports from the EU nor by the EU authorities on imports from the UK.

Article ‘GOODS .5: Prohibition of customs duties’ on page 20 of the agreement states that:

Except as otherwise provided for in this Agreement, customs duties on all goods originating in the other Party shall be prohibited.

This free-trade agreement was taken by many people to mean that trade would be unhindered, with no duties being payable. In fact, as many importers and exporters are finding, trade is not as ‘free’ as it was before January 2021. There are four sources of ‘friction’.

Tariffs on goods finished in the UK

This has become a major area of concern for many UK companies. When a good is imported into the UK from outside the EU and then has value added to it by processing, packaging, cleaning, remixing, preserving, refashioning, etc., under ‘rules of origin’ regulations, it can only count as a UK good if sufficient value or weight is added. The proportions vary by product, but generally goods must have approximately 50% UK content (or 80% of the weight of foodstuffs) to qualify for tariff-free access to the EU. For example, for a petrol car, 55% of its value must have been created in either the EU or UK. Thus cars manufactured in the UK which use many parts imported from Japan, China or elsewhere, may not qualify for tariff-free access to the EU.

In other cases, it is simply the question of whether the processing is deemed ‘sufficient’, rather than the imported inputs having a specific weight or value. For example, the grinding of pepper is regarded as a sufficient process and thus ground pepper can be exported from the UK to the EU tariff free. Another example is that of coal briquettes:

The process to transform coal into briquettes (including applying intense pressure) goes beyond the processes listed in ‘insufficient processing’ and so the briquettes can be considered ‘UK originating’ regardless of the originating status of the coal used to produce the briquettes.

In the case of many garments produced in the UK and then sold in retail chains, many of which have branches in both the UK and EU, generally both the weaving and cutting of fabric to make garments, as well as the sewing, must take place in the UK/EU for the garments to be tariff free when exported from the UK to the EU and vice versa.

Many UK firms exporting to the EU and EU firms exporting to the UK are finding that their products are now subject to tariffs because of insufficient processing being done in the UK/EU. Indeed, with complex international supply chains, this is a major problem for many importing and exporting companies.

Documentation

Rules of origin require that firms provide documentation itemising what parts of their goods come from outside the UK/EU. Then it has to be determined whether tariffs will be necessary on the finished product. This is time consuming and is an example of the increase in ‘red tape’ about which many firms are complaining. As the Evening Standard article states:

Exporters have to be able to provide evidence to prove the origin of their products’ ingredients. Next year, they will also have to provide suppliers’ declarations too, and EU officials may demand those retrospectively, so exporters need to have them now.

The increased paperwork and checks add to the costs of trade. Some EU companies are stating that they will no longer export to the UK and some UK companies that they will no longer export to the EU, or will have to set up manufacturing plants or distribution hubs in the EU to handle trade within the EU.

Other companies are adding charges to their products to cover the costs. As the Guardian article states:

“We bought a €47 [£42] shelf from Next for our bathroom,” said Thom Basely, who lives in Marseille. “On the morning it was supposed to be delivered we received an ‘import duty/tax’ demand for over €30, like a ransom note. It came as a complete surprise.”

In evidence given to the Treasury Select Committee (Q640) in May 2018, Sir Jon Thompson, then Chief Executive of HMRC, predicted that leaving the single market would involve approximately 200 million extra customs declarations on each side of the UK/EU border at a cost of £32.50 for each one, giving a total extra cost of approximately £6.5bn on each side of the border for companies trading with Europe. Although this was only an estimate, the extra ‘paperwork’ will represent a substantial cost.

VAT

Previously, goods could be imported into the UK without paying VAT in the UK on value added up to that point as VAT had already been collected in the EU. Similarly, goods exported to the EU would already have had VAT paid and hence would only be subject to the tax on additional value added. The UK was part of the EU VAT system and did not have to register for VAT in each EU country.

Now, VAT has to be paid on the goods as they are imported or released from a customs warehouse – similar to a customs duty. This is therefore likely to involve additional administration costs – the same as those with non-EU imports.

Services

The UK is a major exporter of services, including legal, financial, accounting, IT and engineering. It has a positive trade in services balance with the EU, unlike its negative trade in goods balance. Yet, the Brexit deal does not include free trade in services. Some of the barriers to other non-EU countries have been reduced for the UK in the TCA, but UK service providers will still face new barriers which will impose costs. For example, some EU countries will limit the time that businesspeople providing services can stay in their countries to six months in any twelve. Some will not recognise UK qualifications, unlike when the UK was a member of the single market.

The financial services supplied by City of London firms are a major source of export revenue, with about 40% of these revenues coming from the EU. Now outside the single market, these firms have lost their ‘passporting rights’. These allowed such firms to sell their services into the EU without the need for additional regulatory clearance. The alternative now is for such firms to be granted ‘equivalence’ by the EU. This has not yet been negotiated and even if it were, does not cover the full range of financial services. It excludes, for example, banking services such as lending and deposit taking.

Conclusions

Leaving the single market has introduced a range of frictions in trade. These are causing severe problems to some importers and exporters in the short term. Some EU goods are now unavailable in the UK or only so at significantly higher prices. Some exporters are finding that the frictions are too great to make their exports profitable. However, it remains to be seen how quickly accounting and logistical systems can adjust to improve trade flows between the UK and the EU.

But some of these frictions, as itemised above, will remain. According to the law of comparative advantage, these restrictions on trade will lead to a loss of GDP. And these losses will not be spread evenly throughout the UK economy: firms and their employees which rely heavily on UK–EU trade will be particularly hard hit.

If something is imported to the UK from outside the UK and then is refashioned in the UK and exported to the EU but, according to the rules of origin has insufficient value added in the UK, does this mean that such as good will be subject to tariffs twice? Explain.

Are tariffs exactly the same as customs duties? Is the distinction made in the Guardian article a correct one?

Is it in the nature of a free-trade deal that it is not the same as a single-market arrangement?

Find out what arrangement Switzerland has with the EU. How does it differ from the UK/EU trade deal?

What are the advantages and disadvantages of the Swiss/EU agreement over the UK/EU one?

Are the frictions in UK–EU trade likely to diminish over time? Explain.

Find out what barriers to trade in services now exist between the UK and EU. How damaging are they to UK services exports?

The EU has recently signed two trade deals after many years of negotiations. The first is with Mercosur, the South American trading and economic co-operation organisation, currently consisting of Brazil, Argentina, Uruguay and Paraguay – a region of over 260m people. The second is with Vietnam, which should result in tariff reductions of 99% of traded goods. This is the first deal of its kind with a developing country in Asia. These deals follow a recent landmark deal with Japan.

At a time when protectionism is on the rise, with the USA involved in trade disputes with a number of countries, such as China and the EU, deals to cut tariffs and other trade restrictions are seen as a positive development by those arguing that freer trade results in a net gain to the participants. The law of comparative advantage suggests that trade allows countries to consume beyond their production possibility curves. What is more, the competition experienced through increased trade can lead to greater efficiency and product development.

It is estimated that the deal with Mercosur could result in a saving of some €4bn per annum in tariffs on EU exports.

But although there is a net economic gain from greater trade, some sectors will lose as consumers switch to cheaper imports. Thus the agricultural sector in many parts of the EU is worried about cheaper food imports from South America. What is more, increased trade could have detrimental environmental impacts. For example, greater imports of beef from Brazil into the EU could result in more Amazonian forest being cut down to graze cattle.

But provided environmental externalities are internalised within trade deals and provided economies are given time to adjust to changing demand patterns, such large-scale trade deals can be of significant benefit to the participants. In the case of the EU–Mercosur agreement, according to the EU Reporter article, it:

…upholds the highest standards of food safety and consumer protection, as well as the precautionary principle for food safety and environmental rules and contains specific commitments on labour rights and environmental protection, including the implementation of the Paris climate agreement and related enforcement rules.

The size of the EU market and its economic power puts it in a strong position to get the best trade deals for its member states. As EU Trade Commissioner, Cecilia Malmström stated:

Over the past few years the EU has consolidated its position as the global leader in open and sustainable trade. Agreements with 15 countries have entered into force since 2014, notably with Canada and Japan. This agreement adds four more countries to our impressive roster of trade allies.

Outside the EU, the UK will have less power to negotiate similar deals.

Draw a diagram to illustrate the gains for a previously closed economy from engaging in trade by specialising in products in which it has a comparative advantage.

Distinguish between trade creation and trade diversion from a trade deal with another country or group of countries.

Which sectors in the EU and which sectors in the Mercosur countries and Vietnam are likely to benefit the most from the respective trade deals?

Which sectors in the EU and which sectors in the Mercosur countries and Vietnam are likely to lose from the respective trade deals?

Are the EU–Mercosur and the EU–Vietnam trade deals likely to lead to net trade creation or net trade diversion?

What are the potential environmental dangers from a trade deal between the EU and Mercosur? To what extent have these dangers been addressed in the recent draft agreement?

Will the UK benefit from the EU’s trade deals with Mercosur and Vietnam?

An agreement in principle was reached on September 30 between the USA, Canada and Mexico over a new trade deal to replace the North American Free Trade Agreement (NAFTA). President Trump had described NAFTA as ‘the worst trade deal maybe ever signed anywhere, but certainly ever signed in this country.’ The new deal, named the United States-Mexico-Canada Agreement, or USMCA, is the result of 14 months of negotiations, which have often been fractious. A provisional bilateral agreement was made between the USA and Mexico in August. At the same time, President Trump threatened a trade war with Canada if it did not reach a trade agreement with the USA (and Mexico). The new USMCA must be ratified by lawmakers in all three countries before it can come into force. This could take a few months.

So is USMCA a radical departure from NAFTA? Does the USA stand to gain substantially, as President Trump claims? In fact, USMCA is little different from NAFTA. It could best be described as a relatively modest reworking of NAFTA. So what are the changes?

The first change affects the car industry. From 2020, 75% of the components of any vehicle crossing between the USA and Canada or Mexico must be made within one or more of the three countries to qualify for tariff-free treatment. The aim is to boost production within the region. But the main change here is merely an increase in the proportion from the current 62.5%.

A more significant change affecting the car industry concerns wages. Between 40% and 45% of a vehicle’s components must be made by workers earning at least US$16 per hour. This is some three times more than the average wage currently earned by Mexican car workers. Although it will benefit such workers, it will reduce Mexico’s competitive advantage and could hence lead to some diversion of production away from Mexico. Also, it could push up the price of cars.

The agreement has also strengthened various standards inadequately covered in NAFTA. According to The Conversation article:

The new agreement includes stronger protections for patents and trademarks in areas such as biotech, financial services and domain names – all of which have advanced considerably over the past quarter century. It also contains new provisions governing the expansion of digital trade and investment in innovative products and services.

Separately, negotiators agreed to update labor and environmental standards, which were not central to the 1994 accord and are now typical in modern trade agreements. Examples include enforcing a minimum wage for autoworkers, stricter environmental standards for Mexican trucks and lots of new rules on fishing to protect marine life.

Another area where the USMCA agreement has made changes concerns trade in dairy products. This particularly affects Canada, which has agreed to allow more US dairy products tariff-free into Canada (see the CNN article at the end of the list of articles below). New higher quotas will give US dairy farmers access to 3.6% of Canada’s dairy market. They will still pay tariffs on dairy exports to Canada that exceed the quotas, ranging from 200% to 300%.

The other significant change for consumers in Mexico and Canada is a rise in the value of duty-free imports they can bring in from the USA, including online transactions. As the first BBC article listed below states:

The new agreement raises duty-free shopping limits to $100 to enter Mexico and C$150 ($115) to enter Canada without facing import duties – well above the $50 previously allowed in Mexico and C$20 permitted by Canada. That’s good news for online shoppers in Mexico and Canada – as well as shipping firms and e-commerce companies, especially giants like Amazon.

Despite these changes, USMCA is very similar to NAFTA. It is still a preferential trade deal between the three countries, but certainly not a completely free trade deal – but nor was NAFTA.

And for the time being, US tariffs on Mexican and Canadian steel and aluminium imports remain in place. Perhaps, with the conclusion of the USMCA agreement, the Trump administration will now, as promised, consider lifting these tariffs.

What have been the chief gains and losses for the USA from USMCA?

What have been the chief gains and losses for Mexico from USMCA?

What have been the chief gains and losses for Canada from USMCA?

What are the economic gains from free trade?

Why might a group of countries prefer a preferential trade deal with various restrictions on trade rather than a completely free trade deal between them?

Distinguish between trade creation and trade diversion.

In what areas, if any, might USMCA result in trade diversion?

If the imposition of tariffs results in a net loss from a decline in trade, why might it be in the interests of a country such as the USA to impose tariffs?

Donald Trump has threatened to pull out of the World Trade Organization. ‘If they don’t shape up, I would withdraw from the WTO,’ he said. He argues that the USA is being treated very badly by the WTO and that the organisation needs to ‘change its ways’.

Historically, the USA has done relatively well compared with other countries in trade disputes brought to the WTO. However, President Trump does not like being bound by an international organisation which prohibits the unilateral imposition of tariffs that are not in direct retaliation against a trade violation by other countries. Such tariffs have been imposed by the Trump administration on steel and aluminium imports. This has led to retaliatory tariffs on US imports by the EU, China and Canada – something that is permitted under WTO rules.

Whether or not the USA does withdraw from the WTO, Trump’s threats bring into question the power of the WTO and other countries’ compliance with WTO rules. With the rise in protectionist sentiments around the world, the power of the WTO would seem to be on the wane.

Even if the USA does not withdraw from the WTO, it is succeeding in weakening the organisation. Appeals cases have to be heard by an ‘appellate body’, consisting of at least three judges drawn from a list of seven, each elected for four years. But the USA has the power to block new appointees – and has done so. As Larry Elliott states in the first article below:

The list of judges is already down to four and will be down to the minimum of three when the Mauritian member, Shree Baboo Chekitan Servansing, retires at the end of September. Two more members will go by the end of next year, at which point the appeals process will come to a halt.

This raises the question of the implication of a ‘no-deal’ Brexit – something that seems more likely as the UK struggles to reach a trade agreement with the EU. Leaving without a deal would mean ‘reverting to WTO rules’. But if these rules are being ignored by powerful countries such as the USA and possibly China, and if the appeals procedure has ground to a halt, this could leave the UK without the safety net of international trade rules. Outside the EU – the world’s most powerful trade bloc – the UK could find itself having to accept poor trade terms with the USA and other large countries.

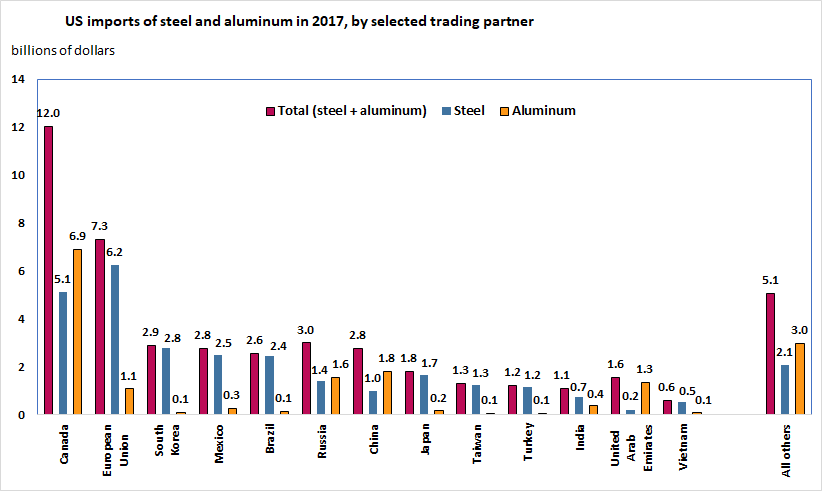

The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

Source: Bown (2018), Figure 1

A number of economists and policymakers are worried that such policies restrict trade and are likely to provoke retaliation by the affected trade partners. In recent statements, the EU has pledged to take counter-measures if the bloc is affected by these policies. In a recent press conference, the Commissioner for Trade, Cecilia Malmstrom, stated that:

We have made it clear that a move that hurts the EU and puts thousands of European jobs in jeopardy will be met with a firm and proportionate response.

She added that, ‘I truly hope that this will not happen. A trade war has no winners.’

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.

A number of studies have attempted to estimate the effect of trade restrictions and tariff wars on welfare: see for instance Anderson and Wincoop (2001), Syropoulos (2002), Fellbermayr et al. (2013). The results vary widely, depending on the case. However, there seems to be consensus that the more similar (in terms of size and industry composition) the adversaries are, the more mutually damaging a trade war is likely to be (and, therefore, less likely to happen).

As Miyagiwa et al (2016, p43) explain:

A country initiates contingent protection policy against a trading partner only if the latter has a considerably smaller domestic market than its own, while avoiding confrontation with a country having a substantially larger domestic market than its own.

As both Canada and the EU are very large advanced market economies, it remains to be seen how much risk (and potential damage to the local and global economy) US trade policymakers are willing to take.

According to the Brexit trade agreement (the Trade and Cooperation Agreement (TCA)), trade between the EU and the UK will remain quota and tariff free. ‘Quota free’ means that trade will not be restricted in quantity by the authorities on either side. ‘Tariff free’ means that customs duties will not be collected by the UK authorities on imports from the EU nor by the EU authorities on imports from the UK.

According to the Brexit trade agreement (the Trade and Cooperation Agreement (TCA)), trade between the EU and the UK will remain quota and tariff free. ‘Quota free’ means that trade will not be restricted in quantity by the authorities on either side. ‘Tariff free’ means that customs duties will not be collected by the UK authorities on imports from the EU nor by the EU authorities on imports from the UK.  This has become a major area of concern for many UK companies. When a good is imported into the UK from outside the EU and then has value added to it by processing, packaging, cleaning, remixing, preserving, refashioning, etc., under ‘rules of origin’ regulations, it can only count as a UK good if sufficient value or weight is added. The proportions vary by product, but generally goods must have approximately 50% UK content (or 80% of the weight of foodstuffs) to qualify for tariff-free access to the EU. For example, for a petrol car, 55% of its value must have been created in either the EU or UK. Thus cars manufactured in the UK which use many parts imported from Japan, China or elsewhere, may not qualify for tariff-free access to the EU.

This has become a major area of concern for many UK companies. When a good is imported into the UK from outside the EU and then has value added to it by processing, packaging, cleaning, remixing, preserving, refashioning, etc., under ‘rules of origin’ regulations, it can only count as a UK good if sufficient value or weight is added. The proportions vary by product, but generally goods must have approximately 50% UK content (or 80% of the weight of foodstuffs) to qualify for tariff-free access to the EU. For example, for a petrol car, 55% of its value must have been created in either the EU or UK. Thus cars manufactured in the UK which use many parts imported from Japan, China or elsewhere, may not qualify for tariff-free access to the EU.  The increased paperwork and checks add to the costs of trade. Some EU companies are stating that they will no longer export to the UK and some UK companies that they will no longer export to the EU, or will have to set up manufacturing plants or distribution hubs in the EU to handle trade within the EU.

The increased paperwork and checks add to the costs of trade. Some EU companies are stating that they will no longer export to the UK and some UK companies that they will no longer export to the EU, or will have to set up manufacturing plants or distribution hubs in the EU to handle trade within the EU. The financial services supplied by City of London firms are a major source of export revenue, with about 40% of these revenues coming from the EU. Now outside the single market, these firms have lost their ‘passporting rights’. These allowed such firms to sell their services into the EU without the need for additional regulatory clearance. The alternative now is for such firms to be granted ‘equivalence’ by the EU. This has not yet been negotiated and even if it were, does not cover the full range of financial services. It excludes, for example, banking services such as lending and deposit taking.

The financial services supplied by City of London firms are a major source of export revenue, with about 40% of these revenues coming from the EU. Now outside the single market, these firms have lost their ‘passporting rights’. These allowed such firms to sell their services into the EU without the need for additional regulatory clearance. The alternative now is for such firms to be granted ‘equivalence’ by the EU. This has not yet been negotiated and even if it were, does not cover the full range of financial services. It excludes, for example, banking services such as lending and deposit taking. The EU has recently signed two trade deals after many years of negotiations. The first is with

The EU has recently signed two trade deals after many years of negotiations. The first is with  But although there is a net economic gain from greater trade, some sectors will lose as consumers switch to cheaper imports. Thus the agricultural sector in many parts of the EU is worried about cheaper food imports from South America. What is more, increased trade could have detrimental

But although there is a net economic gain from greater trade, some sectors will lose as consumers switch to cheaper imports. Thus the agricultural sector in many parts of the EU is worried about cheaper food imports from South America. What is more, increased trade could have detrimental  An agreement in principle was reached on September 30 between the USA, Canada and Mexico over a new trade deal to replace the North American Free Trade Agreement (NAFTA). President Trump had described NAFTA as ‘the worst trade deal maybe ever signed anywhere, but certainly ever signed in this country.’ The new deal, named the United States-Mexico-Canada Agreement, or USMCA, is the result of 14 months of negotiations, which have often been fractious. A provisional bilateral agreement was made

An agreement in principle was reached on September 30 between the USA, Canada and Mexico over a new trade deal to replace the North American Free Trade Agreement (NAFTA). President Trump had described NAFTA as ‘the worst trade deal maybe ever signed anywhere, but certainly ever signed in this country.’ The new deal, named the United States-Mexico-Canada Agreement, or USMCA, is the result of 14 months of negotiations, which have often been fractious. A provisional bilateral agreement was made  Another area where the USMCA agreement has made changes concerns trade in dairy products. This particularly affects Canada, which has agreed to allow more US dairy products tariff-free into Canada (see the CNN article at the end of the list of articles below). New higher quotas will give US dairy farmers access to 3.6% of Canada’s dairy market. They will still pay tariffs on dairy exports to Canada that exceed the quotas, ranging from 200% to 300%.

Another area where the USMCA agreement has made changes concerns trade in dairy products. This particularly affects Canada, which has agreed to allow more US dairy products tariff-free into Canada (see the CNN article at the end of the list of articles below). New higher quotas will give US dairy farmers access to 3.6% of Canada’s dairy market. They will still pay tariffs on dairy exports to Canada that exceed the quotas, ranging from 200% to 300%.

Donald Trump has threatened to pull out of the World Trade Organization. ‘If they don’t shape up, I would withdraw from the WTO,’ he said. He argues that the USA is being treated very badly by the WTO and that the organisation needs to ‘change its ways’.

Donald Trump has threatened to pull out of the World Trade Organization. ‘If they don’t shape up, I would withdraw from the WTO,’ he said. He argues that the USA is being treated very badly by the WTO and that the organisation needs to ‘change its ways’. Whether or not the USA does withdraw from the WTO, Trump’s threats bring into question the power of the WTO and other countries’ compliance with WTO rules. With the rise in protectionist sentiments around the world, the power of the WTO would seem to be on the wane.

Whether or not the USA does withdraw from the WTO, Trump’s threats bring into question the power of the WTO and other countries’ compliance with WTO rules. With the rise in protectionist sentiments around the world, the power of the WTO would seem to be on the wane. This raises the question of the implication of a ‘no-deal’ Brexit – something that seems more likely as the UK struggles to reach a trade agreement with the EU. Leaving without a deal would mean ‘reverting to WTO rules’. But if these rules are being ignored by powerful countries such as the USA and possibly China, and if the appeals procedure has ground to a halt, this could leave the UK without the safety net of international trade rules. Outside the EU – the world’s most powerful trade bloc – the UK could find itself having to accept poor trade terms with the USA and other large countries.

This raises the question of the implication of a ‘no-deal’ Brexit – something that seems more likely as the UK struggles to reach a trade agreement with the EU. Leaving without a deal would mean ‘reverting to WTO rules’. But if these rules are being ignored by powerful countries such as the USA and possibly China, and if the appeals procedure has ground to a halt, this could leave the UK without the safety net of international trade rules. Outside the EU – the world’s most powerful trade bloc – the UK could find itself having to accept poor trade terms with the USA and other large countries. The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.