The Competition Commission (CC) recently completed their provisional investigation into the cement and concrete market in Great Britain (press release). They concluded that coordination between the main cement producers is resulting in high prices.

The Competition Commission (CC) recently completed their provisional investigation into the cement and concrete market in Great Britain (press release). They concluded that coordination between the main cement producers is resulting in high prices.

In contrast, to illegal cartels (see for example the recent post on this site), the firms in this market are not accused of doing anything illegal. Instead, the CC’s concern is with tacit collusion. Here, no illegal communication between firms takes place, firms simply do not compete intensely due to a mutual understanding that high prices are collectively beneficial.

Economic theory suggests that one key factor that facilitates tacit coordination is a low number of firms in the market. The UK cement market certainly meets this criteria as it is an oligopoly with just three main players plus a new entrant. The CC concluded that:

In a highly concentrated market where the product doesn’t vary, the established producers know too much about each other’s businesses and have concentrated on retaining their respective market shares rather than competing to the full.

They estimate that this cost consumers over £180m in a 3 year period.

Whilst tacit collusion is not illegal, competition authorities can try to prevent it from arising by intervening in mergers that they believe will make it more likely. In fact, the new entrant to the cement market came about due to sales required by the CC before they would allow a joint-venture between two of the main players to go ahead. Clearly the CC’s recent findings suggest that this intervention was not sufficient to ensure intense competition in the market. However, an additional tool available to the authorities in the UK is to be able to remedy harm to competition undercovered as a result of an investigation into the market. In some cases this may even involve breaking-up firms in the market (see for example the decision to force BAA to sell several airports).

When deciding on how to remedy the problem in the cement market, the CC will be keen to avoid the past mistakes of their Danish counterparts. In a famous case, in 1993 the Danish authorities attempted to increase competition in the concrete market by publishing individual sellers’ prices. The idea was that this would stimulate competition by encouraging buyers to shop around. However, evidence published here suggests that this in fact increased prices by around 15%! Why? The paper examines possible explanations and concludes that the information published by the competition authorities helped firms to monitor each others behaviour and therefore facilitated tacit coordination in the market. This is entirely consistent with economic theory which shows that another key factor which facilitates tacit coordination is market transparency.

When deciding on how to remedy the problem in the cement market, the CC will be keen to avoid the past mistakes of their Danish counterparts. In a famous case, in 1993 the Danish authorities attempted to increase competition in the concrete market by publishing individual sellers’ prices. The idea was that this would stimulate competition by encouraging buyers to shop around. However, evidence published here suggests that this in fact increased prices by around 15%! Why? The paper examines possible explanations and concludes that the information published by the competition authorities helped firms to monitor each others behaviour and therefore facilitated tacit coordination in the market. This is entirely consistent with economic theory which shows that another key factor which facilitates tacit coordination is market transparency.

The CC suggest that such monitoring is also possible in the GB market:

Established information channels such as price announcement letters can signal their plans, and tit-for-tat behaviour and cross-sales can be used to prevent or retaliate against any moves to disturb the overall balance between the different players in this market.

According to the above press release, the remedies the CC are considering include: the sale of capacity or plants by the leading players in the market, creation of buying groups, prohibition on price announcements and restrictions on the publication of industry level data. This suggests that the CC are well aware that reducing market transparency can play a key role in preventing coordination. It will be fascinating to, first, see what the CC opt for, then, what impact this has on competition in the industry.

Articles

Same product, same price? Competition in the UK Global Cement (22/05/13)

Competition Commission uncovers `serious problems’ in cement market Graham Huband, The Courier (22/05/13)

Competition Commission call for cement sell-off Mark Leftley, London Evening Standard (21/05/13)

Competition Commission documents

CC looks to break open cement market Competition Commission Press Release (21/5/13)

Aggregates, cement and ready-mix concrete market investigation Competition Commission core documents (various dates)

Questions

- Explain tacit collusion using a Prisoner’s dilemma game.

- Is cement the type of product where we might expect coordination to be most likely?

- Why is cement an important market in the UK economy?

- The first article above suggests that most of the management team at the new entrant came from the other main players in the market. Do you think this may significantly affect the likelihood of tacit collusion?

- Evaluate the pros and cons of the alternative remedies the CC are considering.

On 5 and 6 April, there was a conference on conscious capitalism in San Francisco. In January, a new book, Conscious Capitalism: Liberating the Heroic Spirit of Business, by John Mackey and Rajendra Sisodia, was published. Many in the business world are enthusiastic about this seemingly new approach to business, which focuses on broader social, environmental and ethical goals, rather than simple profit maximisation.

On 5 and 6 April, there was a conference on conscious capitalism in San Francisco. In January, a new book, Conscious Capitalism: Liberating the Heroic Spirit of Business, by John Mackey and Rajendra Sisodia, was published. Many in the business world are enthusiastic about this seemingly new approach to business, which focuses on broader social, environmental and ethical goals, rather than simple profit maximisation.

As the Washington Times review linked to below states:

“Conscious Capitalism” promotes a business culture that embodies “trust, accountability, caring, transparency, integrity, loyalty and egalitarianism.” The management ideal of “Conscious Capitalism” contains four key elements of “decentralization, empowerment, innovation and collaboration.” Above all, this exemplary form of business practice relies on careful attention to four tenets: higher purpose and core values, stakeholder integration, conscious leadership and conscious culture and management.

So how realistic is this vision of caring capitalism? There may be a few inspiring businesspeople, truly committed to improving the interests of the various stakeholders of their business and society more generally, but could it become a model for business in general? And if so, does this require education, monitoring and regulation? Or can a libertarian approach to business generate an environment where conscious and caring capitalists flourish and succeed better than those with a more narrow focus on profit?

So how realistic is this vision of caring capitalism? There may be a few inspiring businesspeople, truly committed to improving the interests of the various stakeholders of their business and society more generally, but could it become a model for business in general? And if so, does this require education, monitoring and regulation? Or can a libertarian approach to business generate an environment where conscious and caring capitalists flourish and succeed better than those with a more narrow focus on profit?

The following videos and articles discuss conscious capitalism and the arguments of those, such as John Mackey, founder and co-CEO of Whole Food Market, who advocate it.

Webcasts

Conscious capitalism The Economist, John Mackey (15/3/13)

Conscious capitalism The Economist, John Mackey (15/3/13)

Conscious Capitalism: Heroes of the Business World Conscious capitalism, April in San Francisco (5/4/13)

It’s Not Corporate Social Responsibility Conscious capitalism, John Mackey (Jan 13)

Articles, reviews and information

Conscious Capitalism: Creating a New Paradigm for Business Whole Planet Foundation, John Mackey

Companies that Practice “Conscious Capitalism” Perform 10x Better Harvard Business Review, Tony Schwartz (4/4/13)

4 Ways to Become a (More) Conscious Capitalist Inc., Francesca Louise Fenzi (8/4/13)

The New Management Paradigm & John Mackey’s Whole Foods Forbes, Steve Denning (5/1/13)

Book Review: ‘Conscious Capitalism’ Washington Times, Anthony j. Sadar (20/3/13)

Book Review: Whole Foods Co-CEO John Mackey’s Conscious Capitalism Huffington Post, Christine Bader (28/1/13)

Chicken Soup for a Davos Soul Wall Street Journal, Alan Murray (16/1/13)

Conscious business Wikipedia

Questions

- What are the features of conscious capitalism?

- Do firms “get the shareholders they deserve”?

- How might firms that are not pursuing conscious capitalism be persuaded to become more conscious and more caring?

- How does conscious capitalism differ from corporate social responsibility?

- What would you understand by “conscious consumers”? How might their behaviour differ from other consumers?

- Why might firms engaging in conscious capitalism become more profitable than firms that have a simple aim of profit maximisation?

- What reforms, both internal within a firm and in the legal environment, does John Mackey advocate? Do you agree with his suggestions? What else do you suggest?

The English Premier League (EPL) has negotiated a record TV deal which will generate £5.5 billion of revenue over the next 3 years – beginning in the season 2013–14. This represents a 70% increase on the previous deal. Controversy has arisen over some initial proposals put forward by the EPL as to how the money will be spent. The owners of the clubs in the Championship of the English Football League (EFL) are particularly concerned about the size of the proposed payments to the three teams relegated from the EPL.

The English Premier League (EPL) has negotiated a record TV deal which will generate £5.5 billion of revenue over the next 3 years – beginning in the season 2013–14. This represents a 70% increase on the previous deal. Controversy has arisen over some initial proposals put forward by the EPL as to how the money will be spent. The owners of the clubs in the Championship of the English Football League (EFL) are particularly concerned about the size of the proposed payments to the three teams relegated from the EPL.

Some 30 years ago the money generated from the sale of television rights was equally shared between all the teams in the then four divisions of the English Football League (EFL). In 1992 the top division of the English Football League broke away and formed the English Premier League (EPL). This newly formed EPL negotiated a separate television deal and kept the majority of the money. However, some payments were and still are made to the teams in the EFL and to organisations such as the League Managers Association and Professional Footballers Association. For example in 2011-–12 the EPL donated £189.4 million of the £1.2 billion generated from that year’s TV deal.

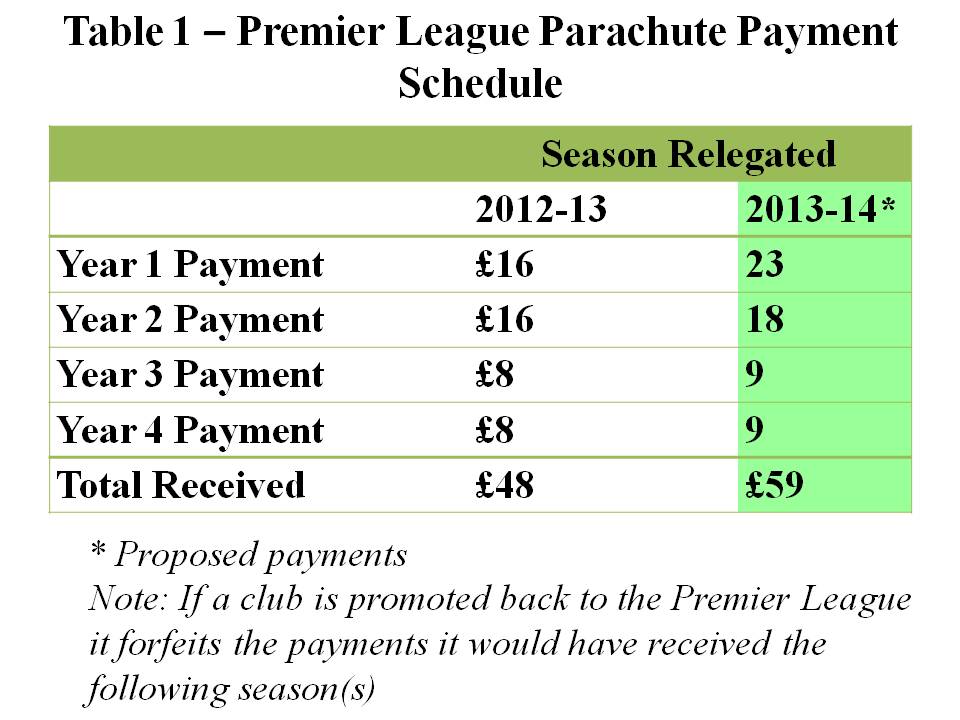

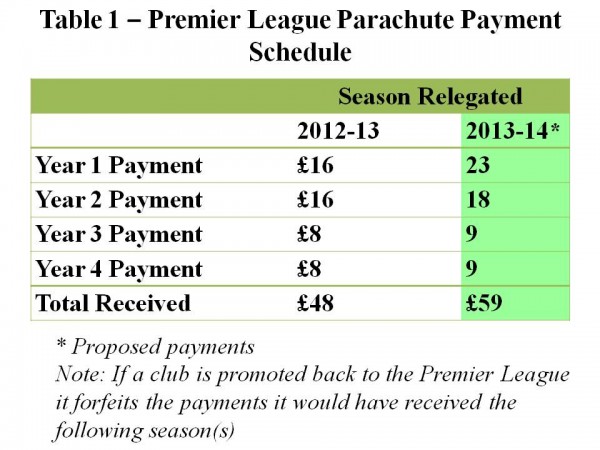

The majority of the money donated by the EPL is spent in two main ways. First, some money is redistributed to all the teams in the EFL: i.e. The Championship, League 1 and League 2. These are known as ‘solidarity payments’ and in 2011–12 the EPL spent £49.8 million on this scheme. Each club in the Championship received £2.3 million. It has been proposed that the amount paid into this scheme should be increased by 5% in the season 2013–14. Second, a relatively large amount of money is paid over a four-year period to the three teams relegated each season from the EPL into the Championship. These are known as ‘parachute payments’ and in the season 2011–12 the EPL spent £90.9 million on this scheme. The rationale for having parachute payments is to help the relegated teams adjust their wage bills to the much lower revenue streams that come from playing in the Championship. Proposed changes to the scheme are outlined in Table 1.

The chairmen of the football league clubs met on the 20th March 2013 and a number of them expressed concerns about the relatively large increase in the parachute payments compared to the solidarity payments. They were particularly concerned that the changes to the funding would damage the competitive balance of the Championship.

The chairmen of the football league clubs met on the 20th March 2013 and a number of them expressed concerns about the relatively large increase in the parachute payments compared to the solidarity payments. They were particularly concerned that the changes to the funding would damage the competitive balance of the Championship.

Competitive balance refers to how the most talented players are distributed amongst the teams in a league. For example, are the majority of the most talented footballers playing for just a couple of the teams? In this case the league is competitively imbalanced and the teams with the best players will tend to win far more games than the other teams. The outcome of the league will be very predictable. If the most talented players were more evenly spread across all the teams in the league, then it would be more competitively balanced. Matches and the outcome of the league would become more unpredictable.

Does the level of competitive balance matter? Some sports economists have argued that it may have a significant impact on the success of the league. This is because fans may value the unpredictability of the results. It follows that closer and more unpredictable results will generate higher match-day attendances and increase the revenues of the clubs.

This is an interesting argument and is the opposite of what economic theory would predict for most markets. For example, the standard prediction would be that as firms outperform their rivals, they generate more revenue and profit. If they manage to drive all their rivals out of business, they would become a pure monopoly and make large abnormal profits. However in professional team sports the outcome may differ significantly. If the unpredictability of the league is highly valued by fans, then teams will generate more revenue when they have strong and evenly matched rivals.

It has been reported that further discussions about the distribution of the money will take place this month with the owners of the championship clubs arguing that there should be smaller increases in parachute payments and much larger increases in solidarity payments. Representatives of the EPL have argued that the parachute payments do not distort competition and make the championship predictable. They point out that at present only one of the top six teams in the championship (Hull) receives parachute payments, while only one of the teams promoted from the Championship in the season 2012–13 (West Ham) received these payments.

Articles

Premier League warned over rich and poor split in wake of TV deal The Guardian, Owen Gibson (19/3/13)

Championship clubs angered by Premier League parachute boost Daily Mail, Charles Sale (6/2/13)

Football league is to lessen the advantage of parachute payments The Guardian, Owen Gibson (20/3/13)

Championship clubs warn Premier League over hike in parachute payments for relegated teams The Independent, Majid Mohamed (20/3/13)

Increased parachute payments could lead to a salary cap in the Championship The Post, A. Stockhausen (21/3/13)

Scudamore:Parachute payment system fair Eurosport, Andy Eckardt (22/3/13)

Parachute payments more than a softened landing The Daisy Cutter, Richard Brook (21/3/13)

Questions

- What factors will influence the size of the attendance at a football match?

- To what extent do you think that the money generated from the sale of television rights should be equally shared between all the clubs in the English Premier League and the English Football League

- Can you think of any ways of measuring the competitive balance of a football league?

- Explain why a very competitively imbalanced league may reduce the revenue for all the clubs in that league?.

- In traditional economic theory it is assumed that firms aim to maximise their profits. What do you think is the objective of a typical football club in the English Premier League?

In 2009, the European Commission investigated Microsoft’s practice of bundling its own browser, Internet Explorer, with new copies of Windows. It found that this was an abuse of market power and created an unfair barrier to entry of other browsers, such as Firefox.

In 2009, the European Commission investigated Microsoft’s practice of bundling its own browser, Internet Explorer, with new copies of Windows. It found that this was an abuse of market power and created an unfair barrier to entry of other browsers, such as Firefox.

An agreement was reached that Microsoft would include a ‘choice screen’ in which users in the EU would be given a full list of alternative browsers and asked which they would like to install. On making their selection, a link would take them to the browser site to download the installation program. This screen would be available until 2014. Between March 2010, when the choice screen was first provided and November of the same year, 84 million browsers were downloaded through it.

In May 2011, however, the screen was no longer present on new Windows 7 purchases. The Commission took some time to realise this: indeed it was Microsoft’s rivals that pointed it out. The screen reappeared some 13 months later, after some 15m copies of Windows software had been sold.

For this lapse, the Commission has just fined Microsoft €561m. Commission Vice President in charge of competition policy, Joaquín Almunia, said:

For this lapse, the Commission has just fined Microsoft €561m. Commission Vice President in charge of competition policy, Joaquín Almunia, said:

In 2009, we closed our investigation about a suspected abuse of dominant position by Microsoft due to the tying of Internet Explorer to Windows by accepting commitments offered by the company. Legally binding commitments reached in antitrust decisions play a very important role in our enforcement policy because they allow for rapid solutions to competition problems. Of course, such decisions require strict compliance. A failure to comply is a very serious infringement that must be sanctioned accordingly.

This may seem unduly harsh, given that Internet Explorer’s share of the browser market has fallen dramatically. In 2009, it had around 50% of the European market, with its main rival at the time, Mozilla’s Firefox, having just under 40%. By 2013, Internet Explorer’s share has fallen to around 24% and Firefox’s to around 29%. Google’s Chrome, which was just starting up in 2009, has seen its share of the European market rise to around 35% and is now the market leader. Partly this is due to the rise in tablets and smartphones, a large proportion of which use Google’s Android operating system and the Chrome browser.

This may seem unduly harsh, given that Internet Explorer’s share of the browser market has fallen dramatically. In 2009, it had around 50% of the European market, with its main rival at the time, Mozilla’s Firefox, having just under 40%. By 2013, Internet Explorer’s share has fallen to around 24% and Firefox’s to around 29%. Google’s Chrome, which was just starting up in 2009, has seen its share of the European market rise to around 35% and is now the market leader. Partly this is due to the rise in tablets and smartphones, a large proportion of which use Google’s Android operating system and the Chrome browser.

Not surprisingly, the European Commission is investigating Google to see whether it is abusing a dominant position. Is Google’s case, it’s not just about its share of the browser market, it’s more about its share of the search market, which in the EU is around 90% (compared with around 65% in the USA). As The Economist article below states:

The Commissioner believes that Google may be favouring its own specialised services (eg, for flights or hotels) at rivals’ expense; that its deals with publishers may unfairly exclude competitors; and that it prevents advertisers from taking their data elsewhere.

Joaquín Almunia asked Google to respond to these concerns by January 31. Google delivered its suggestions on the deadline, but we await to hear precisely what it said and how the Commission will respond. It is understood that Google’s proposal is for clearly labelling its own products on its search engine.

Articles

Microsoft Fined $732 Million By EU Over Browser eWeek, Michelle Maisto (6/3/13)

Microsoft faces hefty EU fine The Guardian (6/3/13)

Sin of omission The Economist (9/3/13)

Microsoft fined by European Commission over web browser BBC News (6/3/13)

EU commissioner Joaquin Almunia announces Microsoft fine BBC News (6/3/13)

Microsoft’s European Fine Comes in an Era of Browser Diversity Forbes, J.P. Gownder (6/3/13)

Life after Firefox: Can Mozilla regain its mojo? BBC News, Dave Lee (11/4/12)

Google responds to European commission’s antitrust chief The Guardian, Charles Arthur (31/1/13)

Google May Clinch EU Settlement After ‘Summer,’ Almunia Says Bloomberg Businessweek, Stephanie Bodoni and Aoife White (22/2/13)

European Commission Press Release

Antitrust: Commission fines Microsoft for non-compliance with browser choice commitments Europa (6/3/13)

Questions

- Why did Microsoft’s share of the browser market continue to decline between May 2011 and June 2012?

- Why would it matter if Microsoft had market power in the browser market, given that it’s free for anyone to download a browser?

- In what ways might Google be abusing a dominant position in the market?

- Can Mozilla regain its mojo?

- According to the second Guardian article, the Microsoft-backed lobby group Icomp said “To be seen as a success, any settlement must … include specific measures to restore competition and allow other parties to compete effectively on a level playing field with Google in the key markets of search and search advertising.” Give examples of such measures and assess how successful they might be.

- Would “clearly labelling its own products on its search engine” be enough to ensure adequate competition?

The Big Four are well known: Deloitte, Ernst and Young, KPMG and PWC. They act as auditors for 90% of the UK’s stock-market listed companies. They have a very close relationship with the companies that they audit and because of this have faced criticism of not warning of the financial crisis. A further accusation is that the relationship between auditors and managers has become blurred.

The Big Four are well known: Deloitte, Ernst and Young, KPMG and PWC. They act as auditors for 90% of the UK’s stock-market listed companies. They have a very close relationship with the companies that they audit and because of this have faced criticism of not warning of the financial crisis. A further accusation is that the relationship between auditors and managers has become blurred.

In some sense, there is a problem of divorce of ownership from control. The companies that are audited by the Big Four have shareholders who are interested in profits and their dividends. But they employ managers who are responsible for the day-to-day running of the business. However, there are concerns that the auditors have become more concerned with meeting the interests of the managers and not of the shareholders. It has been suggested that the company’s management tend to ‘present their accounts in the most favourable light, whereas shareholder interests can be quite different.’ Laura Carstensen, the chair of the Audit Investigation Group said:

It is clear that there is significant dissatisfaction amongst some institutional investors with the relevance and extent of reporting in audited financial reports … management may have incentives to present their accounts in the most favourable light, whereas shareholder interests can be quite different.

The Big Four have been criticised for limiting competition in the industry. The Competition Commission has said that companies typically stay with the same auditing firm and this acts to limit competition. One suggestion to encourage competition is to enforce rotation of Auditors. However, the Big Four have said that the market remains competitive, ‘healthy and robust’ and that any enforcement as noted above would not be in the public interest. Other, smaller auditing companies have praised the preliminary report of the Competition Commission. One firm said:

The Big Four have been criticised for limiting competition in the industry. The Competition Commission has said that companies typically stay with the same auditing firm and this acts to limit competition. One suggestion to encourage competition is to enforce rotation of Auditors. However, the Big Four have said that the market remains competitive, ‘healthy and robust’ and that any enforcement as noted above would not be in the public interest. Other, smaller auditing companies have praised the preliminary report of the Competition Commission. One firm said:

No one solution will achieve market correction, but rather a combination of tendering requirements, encouragement of transparency and dialogue between auditors, companies and investors, and reform of outdated exclusionary practices should provide a backdrop for a healthier FTSE 350 audit market.

The report is not yet final, but the future of the Big Four is somewhat uncertain, especially with the European Commission’s desire to break them up. The following articles look at this industry.

Big Four accountants reject claims over high prices and poor competition The Guardian, Josephine Moulds and David Feeney (22/2/13)

Competition Commission raps Big Four accountants BBC News (22/2/13)

Big Four’s rivals welcome audit shake-up Financial Times, Adam Jones (22/2/13)

UK’s “Big Four” accountants under fire from watchdog Reuters, Huw Jones (22/2/13)

Big Four chastised by Competition Commission The Telegraph, Helia Ebrahimi (22/2/13)

The uncompetitive culture of auditing’s big four remains undented The Guardian, Prem Sikka (23/2/13)

Big Four accountants ‘in closed club on audits’ Independent, Mark Leftly (23/2/13)

Questions

- What is the role of the Competition Commission?

- Explain with other examples the problem of the divorce of ownership from control. How might the interest of shareholders and managers differ? Can they ever be aligned?

- Is market share a good measure of the competitiveness of an industry?

- What are the benefits of competition?

- Why has the regulator suggested that the Big Four are limiting competition?

- What solutions have been proposed by the Competition Commission? Explain how they are likely to stimulate competition in this market.

The Competition Commission (CC) recently completed their provisional investigation into the cement and concrete market in Great Britain (press release). They concluded that coordination between the main cement producers is resulting in high prices.

The Competition Commission (CC) recently completed their provisional investigation into the cement and concrete market in Great Britain (press release). They concluded that coordination between the main cement producers is resulting in high prices. When deciding on how to remedy the problem in the cement market, the CC will be keen to avoid the past mistakes of their Danish counterparts. In a famous case, in 1993 the Danish authorities attempted to increase competition in the concrete market by publishing individual sellers’ prices. The idea was that this would stimulate competition by encouraging buyers to shop around. However, evidence published here suggests that this in fact increased prices by around 15%! Why? The paper examines possible explanations and concludes that the information published by the competition authorities helped firms to monitor each others behaviour and therefore facilitated tacit coordination in the market. This is entirely consistent with economic theory which shows that another key factor which facilitates tacit coordination is market transparency.

When deciding on how to remedy the problem in the cement market, the CC will be keen to avoid the past mistakes of their Danish counterparts. In a famous case, in 1993 the Danish authorities attempted to increase competition in the concrete market by publishing individual sellers’ prices. The idea was that this would stimulate competition by encouraging buyers to shop around. However, evidence published here suggests that this in fact increased prices by around 15%! Why? The paper examines possible explanations and concludes that the information published by the competition authorities helped firms to monitor each others behaviour and therefore facilitated tacit coordination in the market. This is entirely consistent with economic theory which shows that another key factor which facilitates tacit coordination is market transparency.