The market structure in which firms operate has important implications for prices, products, suppliers and profits. In competitive markets, we expect to see low prices, many firms competing with new innovations and firm behavior that is in, or at least not against the public interest. As a firm becomes dominant in a market, its behavior is likely to change and consumers and suppliers can be adversely affected. Is this the case with Amazon?

The market structure in which firms operate has important implications for prices, products, suppliers and profits. In competitive markets, we expect to see low prices, many firms competing with new innovations and firm behavior that is in, or at least not against the public interest. As a firm becomes dominant in a market, its behavior is likely to change and consumers and suppliers can be adversely affected. Is this the case with Amazon?

Much attention has been given to the dispute centering around Amazon and its actions in the market for e-books, where it holds close to two thirds of the market share. Critics of Amazon suggest that this is just one example of Amazon using its monopoly power to exploit consumers and suppliers, including the publishers and their authors. Although Amazon is not breaking any laws, there are suggestions that its behavior is ‘brutal’ and is taking advantage of consumers, suppliers and its workforce.

But rather than criticizing the actions of a monopolist like Amazon, should we instead be praising the company and its ability to compete other firms out of the market? One of the main reasons why consumers use Amazon to buy goods is that prices are cheap. So, in this respect, perhaps Amazon is not acting against consumers’ interests, as under a monopoly we typically expect low output and high prices, relative to a model of perfect competition. The question of the methods used to keep prices so low is another matter. Two conflicting views on Amazon can be seen from Annie Lowrey and Franklin Foer, who respectively said:

“Amazon relentlessly drives down prices for goods and services and delivers them fast and cheap. It ploughs its profits into price cuts and innovation rather than putting them in the hands of its investors. That benefits millions of families – full stop.”

“In effect, we’ve been thrust back 100 years to a time when the law was not up to the task of protecting the threats to democracy posed by monopoly; a time when the new nature of the corporation demanded a significant revision of government.”

So, with Amazon we have an interesting case of a monopolist, where many aspects of its behaviour fit exactly into the mould of the traditional monopolist. But, some of the outcomes we observe indicate a more competitive market. Paul Krugman has been relatively blunt in his opinion that Amazon’s dominance is bad for America. His comments are timely, given the recognition for Jean Tirole’s work in considering the problems faced when trying to regulate any firm that has significant market power. He has been awarded the Nobel Prize in Economics. I’ll leave you to decide where you place this company on the traditional spectrum of market structures, as you read the following articles.

Amazon: Monopoly or capitalist success story? BBC News, Kierran Petersen (14/10/14)

Why the Justice Department won’t go after Amazon, even though Paul Krugman thinks it’s hurting America Business Insider, Erin Fuchs (20/10/14)

Is Amazon a monopoly? The Week, Sergio Hernandez (19/11/14)

Big, bad Amazon The Economist (20/10/14)

Questions

- What are the typical characteristics of a monopoly? To what extent does Amazon fit into this market structure?

- Why does Paul Krugman suggest that Amazon is hurting America?

- How does Amazon’s behaviour with regard to (a) its suppliers and (b) its workers affect its profitability? Would it be able to behave in this way if it were a smaller company?

- Why is Amazon able to charge its customers such low prices? Why does it do this, given its market power?

- Is there an argument for more regulation of firms with such dominance in a market, as is the case with Amazon?

- The debate over e-books is ingoing. What is the argument for publishers to be able to set a minimum price? What is the argument against this?

- Should customers boycott Amazon in a protest over the alleged working conditions of Amazon factory employees?

The typical UK high street is changing. Some analysts have been arguing for some time that high streets are dying, with shops unable to face the competition from large supermarkets and out-of-town malls. But it’s not all bad news for the high street: while some types of shop are disappearing, others are growing in number.

The typical UK high street is changing. Some analysts have been arguing for some time that high streets are dying, with shops unable to face the competition from large supermarkets and out-of-town malls. But it’s not all bad news for the high street: while some types of shop are disappearing, others are growing in number.

Part of the reason for this is the rise in online shopping; part is the longer-term effects of the recession. One consequence of this has been a shift in demand from large supermarkets (see the blog, Supermarket wars: a pricing race to the bottom). Many people are using local shops more, especially the deep discounters, but also the convenience stores of the big supermarket chains, such as Tesco Express and Sainsbury’s Local. Increasingly such stores are opening in shops and pubs that have closed down. As The Guardian article states:

The major supermarket chains are racing to open high street outlets as shoppers move away from the big weekly trek to out-of-town supermarkets to buying little, local and often.

Some types of shop are disappearing, such as video rental stores, photographic stores and travel agents. But other types of businesses are on the increase. In addition to convenience stores, these include cafés, coffee shops, bars, restaurants and takeaways; betting shops, gyms, hairdressers, phone shops and tattoo parlours. It seems that people are increasingly seeing their high streets as social places.

Then, reflecting the widening gap between rich and poor and the general desire of people to make their money go further, there has been a phenomenal rise in charity shops and discount stores, such as Poundland and Poundworld.

So what is the explanation? Part of it is a change in tastes and fashions, often reflecting changes in technology, such as the rise in the Internet, digital media, digital photography and smart phones. Part of it is a reflection of changes in incomes and income distribution. Part of it is a rise in highly competitive businesses, which challenge the previous incumbents.

But despite the health of some high streets, many others continue to struggle and the total number of high street stores across the UK is still declining.

What is clear is that the high street is likely to see many more changes. Some may die altogether, but others are likely to thrive if new businesses are sufficiently attracted to them or existing ones adapt to the changing market.

How the rise of tattoo parlours shows changing face of Britain’s high streets The Guardian, Zoe Wood and Sarah Butler (7/10/14)

The changing face of the British High Street: Tattoo parlours and convenience stores up, but video rental shops and travel agents down Mail Online, Dan Bloom (8/10/14)

High Street footfall struggles in August Fresh Business Thinking, Jonathan Davies (15/9/14)

Ghost town Britain: Internet shopping boom sees 16 high street stores close every day Mail Online, Sean Poulter (8/10/14)

Questions

- Which of the types of high street store are likely to have a high income elasticity of demand? How will this affect their future?

- What factors other than the types of shops and other businesses affect the viability of high streets?

- What advice would you give your local council if it was keen for high streets in its area to thrive?

- Why are many large superstores suffering a decline in sales? Are these causes likely to be temporary or long term?

- How are technological developments affecting high street sales?

- What significant changes in tastes/fashions are affecting the high street?

- Are you optimistic or pessimistic about the future of high streets? Explain.

In an earlier post, Elizabeth looked at oligopolistic competition between supermarkets. Although supermarkets have been accused of tacit price collusion on many occasions in the past, price competition has been growing. And recent developments show that it is likely to get a lot fiercer as the ‘big four’ try to take on the ‘deep discounters’, Aldi and Lidl.

In an earlier post, Elizabeth looked at oligopolistic competition between supermarkets. Although supermarkets have been accused of tacit price collusion on many occasions in the past, price competition has been growing. And recent developments show that it is likely to get a lot fiercer as the ‘big four’ try to take on the ‘deep discounters’, Aldi and Lidl.

Part of the reason for the growth in price competition has been a change in shopping behaviour. Rather than doing one big shop per week in Tesco, Sainsbury’s, Asda or Morrisons, many consumers are doing smaller shops as they seek to get more for their money. A pattern is emerging for many consumers who are getting their essentials in Aldi or Lidl, their ‘special’ items in more upmarket shops, such as Waitrose, Marks & Spencer or small high street shops (such as bakers and ethnic food shops) and getting much fewer products from the big four. Other consumers, on limited incomes, who have seen their real incomes fall as prices have risen faster than wages, are doing virtually all their shopping in the deep discounters. As the Guardian article below states:

A steely focus on price and simplicity, against a backdrop of falling living standards that has sharpened customers’ eye for a bargain, has seen the discounter grab market share from competitors and transform what we expect from our weekly shop.

The result is that the big four are seeing their market share falling, as the chart shows.  (Click here for a PowerPoint of the chart.) In the past year, Tesco’s market share has fallen from 29.9% to 28.1%, Asda’s from 17.8% to 16.3%, Sainsbury’s from 16.9% to 16.2% and Morrisons’ from 11.7% to 11.0%. By contrast, Aldi’s has risen from 3.9% to 5.4% and Lidl’s from 3.1% to 4.0%, while Waitrose’s has also risen, from 4.7% to 4.9%. And it’s not just market share that has been falling for the big four. Profits have also fallen, as have share prices. Sales revenues in the four weeks to 13 September are down 1.6% on the same period a year ago; sales volumes are down 1.9%.

(Click here for a PowerPoint of the chart.) In the past year, Tesco’s market share has fallen from 29.9% to 28.1%, Asda’s from 17.8% to 16.3%, Sainsbury’s from 16.9% to 16.2% and Morrisons’ from 11.7% to 11.0%. By contrast, Aldi’s has risen from 3.9% to 5.4% and Lidl’s from 3.1% to 4.0%, while Waitrose’s has also risen, from 4.7% to 4.9%. And it’s not just market share that has been falling for the big four. Profits have also fallen, as have share prices. Sales revenues in the four weeks to 13 September are down 1.6% on the same period a year ago; sales volumes are down 1.9%.

But can the big four take on the discounters at their own game? Morrison’s has just announced a form of price match scheme called ‘Match & More’. If a shopper finds that a comparable grocery shop is cheaper in not only Tesco, Sainsbury’s or Asda, but also in Aldi or Lidl, then ‘Match & More users will automatically get the difference back in points on their card. Shoppers also will be able to collect extra points on hundreds of featured products and fuel’. When the difference has risen to a total £5 (5000 points), the shopper will get a £5 voucher at the till. The idea is to encourage customers to stay loyal to Morrisons.

But what if Tesco, Asda and Sainsbury’s do the same? What will be the impact on their prices and profits. Will there be a race to the bottom in prices, or will they be able to keep prices higher than the deep discounters, hoping that many customers will not cash in their vouchers?

But what if Tesco, Asda and Sainsbury’s do the same? What will be the impact on their prices and profits. Will there be a race to the bottom in prices, or will they be able to keep prices higher than the deep discounters, hoping that many customers will not cash in their vouchers?

But if effectively the big four felt forced to cut their prices to match Aldi and Lidl, could they afford to do so? This depends on their comparative average costs. At first sight, it might be thought that the big four could succeed in profitably matching the discounters, thereby clawing back market share. After all, they are much bigger and it might be thought that they would benefit from greater economies of scale and hence lower costs.

But it is not as simple as this. The discounters have lower costs than the big four. Their shops are typically in areas where rents or land prices are lower; their shops are smaller; they carry many fewer lines and thus gain economies of scale on each line; they have a much higher proportion of own-brand products; products are displayed in the boxes they come in, thus saving on the staff costs of unpacking them and placing them on shelves; they buy what is cheapest and thus do not always display the same brands.

So is Morrison’s a wise strategy? Will other supermarkets be forced to follow? Is there a prisoners’ dilemma here and, if so, is there any form of collusion in which the big four can engage which is not illegal? Can the big four differentiate themselves from the discounters and the up-market supermarkets in ways that will attract back customers?

It is worrying times for the big four.

Articles

- Heavy Discounters Up Pressure On The UK’s Big Four Supermarkets

Alliance News, Rowena Harris-Doughty (3/6/14)

- Tesco loses more market share as supermarket sector slows to record low

CITY A.M., Catherine Neilan (23/9/14)

- Record low for grocery market growth as inflation disappears

Kantar World Panel, Fraser McKevitt (23/9/14)

- How Aldi’s price plan shook up Tesco, Morrison’s, Asda and Sainsbury’s

The Guardian, Sarah Butler (29/9/14)

- Sainsbury’s shares drop 7% on falling sales report

BBC News (1/10/14)

- Sainsbury results: the reaction

Food Manufacture, Mike Stones (3/10/14)

- Morrisons Becomes First Of Big Four Grocers To Price Match Aldi, Lidl

Alliance News, Rowena Harris-Doughty (2/10/14)

- UK: Morrisons Takes On Discounters With Price Match Card

KamCity (3/10/14)

- Morrisons to match the prices of Aldi and Lidl

The Telegraph, Graham Ruddick (2/10/14)

- Three reasons why Morrisons price-matching Aldi and Lidl is not a ‘gamechanger’

The Telegraph, Graham Ruddick (2/10/14)

Questions

- Would it be possible for the big four to price match the deep discounters?

- What is meant by the prisoners’ dilemma? In what ways are the big four in a prisoners’ dilemma situation?

- Assume that you had to advise Tesco on it strategy? What advise would you give it and why?

- Assume that two firms, M and A, are playing the following ‘game’: firm M pledges to match firm A’s prices; and firm A pledges to sell at 2% below M’s price. What will be the outcome of this game?

- Is Morrisons wise to adopt its ‘Match & More’ strategy?

- Why is it difficult for Morrisons to make a like-for-like comparison with Aldi and Lidl in its ‘Match & More’ strategy?

- Why may Aldi and Lidl benefit from Morrisons’ strategy?

Merlin Entertainments PLC is one of the largest operator of visitor attractions in the world and owns over a third of the most popular theme parks in Europe. It runs the four most visited parks in England – Alton Towers, Legoland Windsor, Thorpe Park and Chessington World of Adventures as well as the most popular theme park in Italy – Gardaland. Alton Towers alone had 2.5 million visitors in 2013. Anybody thinking of going to one of these attractions is faced with a wide range of different entry fees .

Merlin Entertainments PLC is one of the largest operator of visitor attractions in the world and owns over a third of the most popular theme parks in Europe. It runs the four most visited parks in England – Alton Towers, Legoland Windsor, Thorpe Park and Chessington World of Adventures as well as the most popular theme park in Italy – Gardaland. Alton Towers alone had 2.5 million visitors in 2013. Anybody thinking of going to one of these attractions is faced with a wide range of different entry fees .

Theme parks and tourist attractions have market power so their owners have to make some interesting pricing decisions. They have to tackle the same dilemma that confronts any seller that faces a downward sloping demand curve for its goods/services.

One option for the firm would be to increase the entry fee. This would produce higher profits per visitor as some of the surplus from the transaction previously enjoyed by the consumer will be extracted by the seller and converted into producer surplus. Unfortunately for the business the higher price, all other things equal, will also result in fewer visitors. Some people will be deterred from visiting because of the higher price and the seller will lose out on potential revenue.

An alternative strategy would be for the theme park to reduce its entry fee. All other things equal, this will increase the number of visitors. However, it would also mean that the profit per customer would fall. The frustrating issue for the seller is that some of its customers, who would still have visited the attraction at the higher price, are now able to get a better deal.

This dilemma exists if the seller has to charge all of its different customers the same entry fee. If it could charge a higher entry fee to those customers who would be willing to pay more and a lower entry fee to those who would be willing to pay less then it could make more money. Extra revenue could be obtained from those additional sales that take place at the lower price while more consumer surplus could be extracted from those still paying the higher price.

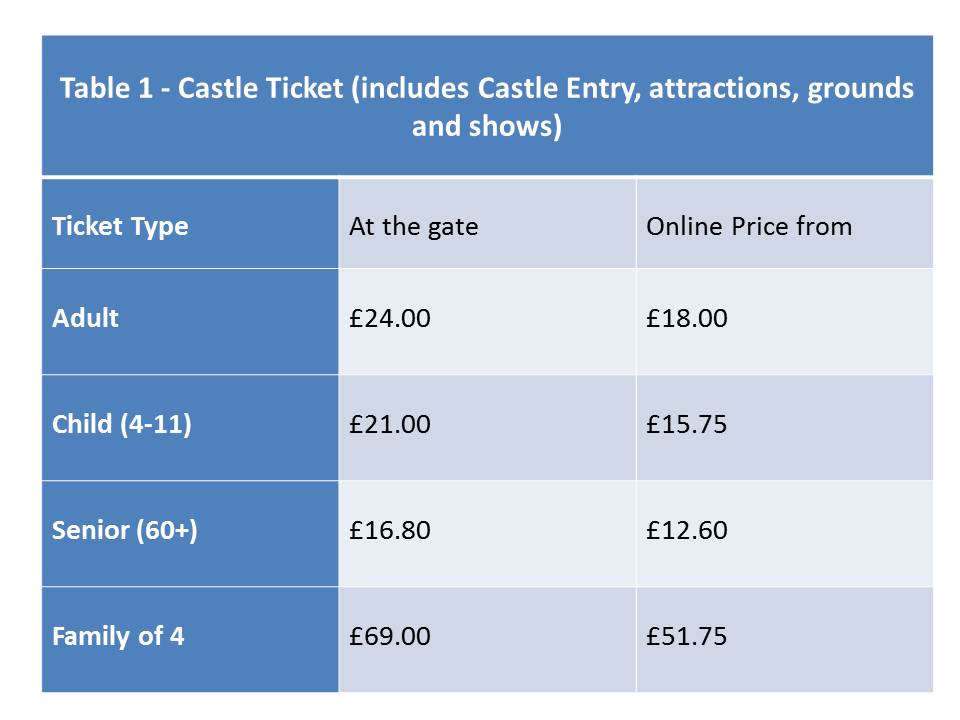

Is it possible for a firm to charge different prices to different customers for the same or a similar good or service? Table 1 below shows the entry fees for Warwick Castle, another tourist attraction owned by Merlin Entertainments PLC.

It can immediately be seen from this table that some groups of customers pay a different entry fee from others. For example adults have to pay £24 to enter on the day while people aged 60 and over pay a lower price £16.80. The entry fee for children aged between 4 and 11 is £21.00 while those aged 3 and under go for free. Students aged 16-18 can gain entry for a price of £13.50 if they can provide valid ID and purchase the tickets from the visitbritainshop website.

In this example, the company has allocated people into different categories by age (i.e. senior, adult, student, older children and younger children) and has set the entry fee that customers in each group have to pay.

The table also shows that if customers purchase on- line then they can get the tickets more cheaply. The entry fee for each category is 25% lower if the ticket is booked seven days in advance i.e. the prices shown in the last column in the table. If the booking is made between 2-6 days in advance then the discount is only 10% i.e. an adult ticket would cost £21.60. The on-line discounts are open to everyone. People are given the choice to either book on-line in advance or pay on the day. This is different from a situation where you are placed into a category by the firm. For example the customer cannot choose whether they are over 60!

If people are prepared to spend more time searching on the internet then other cheaper prices can also be obtained. Once again these offers are open to anyone willing to spend the time and effort in order to find them.

All the ticket prices above give people access to exactly the same attractions on the day. They do not give the visitor access to two of the attractions at the castle – the Dragon Tower and Castle Dungeon. Entry to the Dragon Tower would cost an adult on the day an extra £1.80 while entry to the Castle Dungeon would cost an extra £5.40.

Warwick Castle Ticket Prices Warwick Castle (accessed on 04/09/14)

Alton Towers Alton Towers (accessed on 08/09/14)

Warwick Castle Tickets visitbritainshop (accessed on 02/09/14)

Global Attractions Attendance Report teaconnect (accessed on 05/09/14)

Merlin Entertainments Merlin Entertainments (accessed on 08/09/14)

Questions

- What pricing decisions do firms have to make if they operate in a perfectly competitive market?

- Explain why an individual tourist attraction will have a downward sloping demand curve

- Paying an entry fee and an extra payment per attraction is known as what type of pricing? What advantages does this type of price strategy have for the seller?

- How would you calculate the profit per customer? What factors other than the entrance fee would determine the profit made per customer in a theme park or tourist attractions?

- Paying a different price depending on which category you have been assigned to by the seller is known as what type of pricing strategy? Can this type of pricing strategy ever be in the interests of society?

- In the example used in the case, customers are assigned to different categories by age. Can you think of any other ways that firms could categorise their customers?

- Given the category customers have been assigned to they can pay different prices depending on whether they buy the tickets on line. What is the price strategy called when customers can choose from a variety of pricing options for the same or similar product? Can you think of any different methods that could be used by the seller to carry out this type of pricing strategy?

Over the past few decades, numerous areas within the British economy have been partly or fully privatized and one such case is British Rail. Why is this relevant now? We’re once again looking at the potential increase in rail fares across the country and the impact this will have on commuters and households. So, have the promises of privatisation – namely lower fares – actually materialised?

Over the past few decades, numerous areas within the British economy have been partly or fully privatized and one such case is British Rail. Why is this relevant now? We’re once again looking at the potential increase in rail fares across the country and the impact this will have on commuters and households. So, have the promises of privatisation – namely lower fares – actually materialised?

Comparing the increase in rail fares with that of the RPI makes for interesting reading. Data obtained back in January 2013 shows that since 1995, when the last set of British Rail fares were published, the RPI has been 66%, according to data from Barry Doe and this compares unfavourably with the increase in a single ticket from London to Manchester which had increased by over 200%. However, it compares favourably with a season ticket, which had only increased by 65%. In the last couple of years, increased in rail fares have been capped by the government to increase by no more than the rate of inflation. As such, customers are likely to be somewhat insulated from the increases that were expected, which could have ranged between 3 and 5%.

This announcement has been met with mixed reviews, with many in support of such caps and the benefit this will bring to working households, including Passenger Focus, the rail customer watchdog. Its Passenger Director, David Sidebottom said:

The capping of rail fare rises by inflation will be welcome news to passengers in England, especially those who rely on the train for work, as will the ban on train companies increasing some fares by more than the average. It is something we have been pushing for, for several years now and we are pleased that the Government has recognised the need to act to relieve the burden on passengers.

However, others have criticised the increases in rail fares, given the cost of living crisis and the potential 9% pay rise for MPs. The acting General Secretary of the RMT transport union commented:

However, others have criticised the increases in rail fares, given the cost of living crisis and the potential 9% pay rise for MPs. The acting General Secretary of the RMT transport union commented:

The announcement from George Osborne does not stack up to a freeze for millions of people whose incomes are stagnant due to years of austerity. To try and dress this up as benefiting working people is pure fraud on the part of the Government … Tomorrow, RMT will be out at stations across the north where some off-peak fares will double overnight.

Commuters in different parts of the country do face different prices and with some changes in peak travel times in the Northern part of the country, it is expected that some customers will see significant hikes in prices. Peak travel prices being higher is no surprise and there are justifiable reasons for this, but would such changes in peak times in the North have occurred had we still been under British Rail? Privatisation should bring more competition, lower prices and government revenue at the point of sale. Perhaps you might want to look in more detail at the actual to see whether or not you think the benefits of privatisation have actually emerged. The following articles consider the latest announcement regarding rail fares.

Rail fares to increase by 2.5% in January after Osborne caps price rises at no more than inflation Mail Online, Tom McTague (7/9/14)

Have train fares gone up or down since British Rail? BBC News, Tom Castella (22/1/13)

Rail fares to match inflation rate for another 12 months The Guardian (7/9/14)

Britain caps rail fares at inflation Reuters (7/9/14)

Regulated rail fares to increase by 3.5% in 2015 BBC News (19/8/14)

Northern commuters face big rise in fares for evening travel The Guardian, Gwyn Topham (7/9/14)

Commuter rail fares frozen again, says George Osborne BBC News (7/8/14)

Rail fares, the third payroll tax Financial Times, Jonathan Eley (22/8/14)

Questions

- What are the general advantages and disadvantages of privatisation, whether it is of British Rail or British Gas?

- Why is it that season tickets have increased by less than the RPI, but single tickets have increased by more?

- What are the conditions needed to allow train companies to charge a higher price at peak travel times?

- Are higher prices at peak times an example of price discrimination? Explain why or why not.

- In the Financial Times article, it is suggested that rail fares are like a payroll tax. What is a payroll tax and why are rail fares related to this? Does it suggest that the current method of setting rail fares is equitable?

- Based on the arguments contained in the articles, do you think the cap on rail fares is sufficient?

The market structure in which firms operate has important implications for prices, products, suppliers and profits. In competitive markets, we expect to see low prices, many firms competing with new innovations and firm behavior that is in, or at least not against the public interest. As a firm becomes dominant in a market, its behavior is likely to change and consumers and suppliers can be adversely affected. Is this the case with Amazon?

The market structure in which firms operate has important implications for prices, products, suppliers and profits. In competitive markets, we expect to see low prices, many firms competing with new innovations and firm behavior that is in, or at least not against the public interest. As a firm becomes dominant in a market, its behavior is likely to change and consumers and suppliers can be adversely affected. Is this the case with Amazon?