The growth of emerging economies, such as China, India and Brazil brings with it both good and bad news for the once dominant countries of the West. With growth rates in China reaching double digits and a much greater resilience to the credit crunch and its aftermath in these emerging nations, they became the hope of the recovery for the West. But, is it only benefits that emerge from the growth in countries like China?

The growth of emerging economies, such as China, India and Brazil brings with it both good and bad news for the once dominant countries of the West. With growth rates in China reaching double digits and a much greater resilience to the credit crunch and its aftermath in these emerging nations, they became the hope of the recovery for the West. But, is it only benefits that emerge from the growth in countries like China?

Chinese business has grown and expanded into all areas, especially technology, but countries such as the USA have been reluctant to allow mergers and takeovers of some of their businesses. Notably, the takeovers that have been resisted have been in key sectors, particularly oil, energy and technology. However, it seems as though pork is an industry that is less important or, at least, a lower risk to national security.

Smithfield Foods is a US giant, specialising in the production and selling of pork. A takeover by China’s Shuanghui International Holdings has been approved (albeit reluctantly) by the US Committee on Foreign Investment. While the takeover could still run into obstacles, this Committee’s approval is crucial, as it alleviates concerns over the impact on national security. The value of the deal is some $7.1bn, including the debt that Shuangui will have to take on. While some see this takeover as good news, others are more concerned, identifying the potential negative impact it may have on prices and standards in the USA. Zhijun Yang, Shuanghui’s Chief Executive said:

Smithfield Foods is a US giant, specialising in the production and selling of pork. A takeover by China’s Shuanghui International Holdings has been approved (albeit reluctantly) by the US Committee on Foreign Investment. While the takeover could still run into obstacles, this Committee’s approval is crucial, as it alleviates concerns over the impact on national security. The value of the deal is some $7.1bn, including the debt that Shuangui will have to take on. While some see this takeover as good news, others are more concerned, identifying the potential negative impact it may have on prices and standards in the USA. Zhijun Yang, Shuanghui’s Chief Executive said:

This transaction will create a leading global animal protein enterprise. Shuanghui International and Smithfield have a long and consistent track record of providing customers around the world with high-quality food, and we look forward to moving ahead together as one company.

The date of September 24th looks to be the decider, when a shareholder meeting is scheduled to take place. There is still resistance to the deal, but if it goes ahead it will certainly help other Chinese companies looking for the ‘OK’ from US regulators for their own business deals. The following articles consider the controversy and impact of this takeover.

US clears Smithfield’s acquisition by China’s Shuanghui Penn Energy, Reuters, Lisa Baertlein and Aditi Shrivastava (10/9/13)

Chinese takeover of US Smithfield Foods gets US security approval Telegraph (7/9/13)

US clears Smithfield acquisition by China’s Shuanghui Reuters (7/9/13)

Go-ahead for Shuanghui’s $4.7bn Smithfield deal Financial Times, Gina Chon (6/9/13)

US security panel approves Smithfield takeover Wall Street Journal, William Mauldin (6/9/13)

Questions

- What type of takeover would you classify this as? Explain your answer.

- Why have other takeovers in oil, energy and technology not met with approval?

- Some people have raised concerns about the impact of the takeover on US pork prices. Using a demand and supply diagram, illustrate the possible effects of this takeover.

- What do you think will happen to the price of pork in the US based on you answer to question 3?

- Why do Smithfield’s shareholders have to meet before the deal can go ahead?

- Is there likely to be an impact on share prices if the deal does go ahead?

On 5 and 6 April, there was a conference on conscious capitalism in San Francisco. In January, a new book, Conscious Capitalism: Liberating the Heroic Spirit of Business, by John Mackey and Rajendra Sisodia, was published. Many in the business world are enthusiastic about this seemingly new approach to business, which focuses on broader social, environmental and ethical goals, rather than simple profit maximisation.

On 5 and 6 April, there was a conference on conscious capitalism in San Francisco. In January, a new book, Conscious Capitalism: Liberating the Heroic Spirit of Business, by John Mackey and Rajendra Sisodia, was published. Many in the business world are enthusiastic about this seemingly new approach to business, which focuses on broader social, environmental and ethical goals, rather than simple profit maximisation.

As the Washington Times review linked to below states:

“Conscious Capitalism” promotes a business culture that embodies “trust, accountability, caring, transparency, integrity, loyalty and egalitarianism.” The management ideal of “Conscious Capitalism” contains four key elements of “decentralization, empowerment, innovation and collaboration.” Above all, this exemplary form of business practice relies on careful attention to four tenets: higher purpose and core values, stakeholder integration, conscious leadership and conscious culture and management.

So how realistic is this vision of caring capitalism? There may be a few inspiring businesspeople, truly committed to improving the interests of the various stakeholders of their business and society more generally, but could it become a model for business in general? And if so, does this require education, monitoring and regulation? Or can a libertarian approach to business generate an environment where conscious and caring capitalists flourish and succeed better than those with a more narrow focus on profit?

So how realistic is this vision of caring capitalism? There may be a few inspiring businesspeople, truly committed to improving the interests of the various stakeholders of their business and society more generally, but could it become a model for business in general? And if so, does this require education, monitoring and regulation? Or can a libertarian approach to business generate an environment where conscious and caring capitalists flourish and succeed better than those with a more narrow focus on profit?

The following videos and articles discuss conscious capitalism and the arguments of those, such as John Mackey, founder and co-CEO of Whole Food Market, who advocate it.

Webcasts

Conscious capitalism The Economist, John Mackey (15/3/13)

Conscious capitalism The Economist, John Mackey (15/3/13)

Conscious Capitalism: Heroes of the Business World Conscious capitalism, April in San Francisco (5/4/13)

It’s Not Corporate Social Responsibility Conscious capitalism, John Mackey (Jan 13)

Articles, reviews and information

Conscious Capitalism: Creating a New Paradigm for Business Whole Planet Foundation, John Mackey

Companies that Practice “Conscious Capitalism” Perform 10x Better Harvard Business Review, Tony Schwartz (4/4/13)

4 Ways to Become a (More) Conscious Capitalist Inc., Francesca Louise Fenzi (8/4/13)

The New Management Paradigm & John Mackey’s Whole Foods Forbes, Steve Denning (5/1/13)

Book Review: ‘Conscious Capitalism’ Washington Times, Anthony j. Sadar (20/3/13)

Book Review: Whole Foods Co-CEO John Mackey’s Conscious Capitalism Huffington Post, Christine Bader (28/1/13)

Chicken Soup for a Davos Soul Wall Street Journal, Alan Murray (16/1/13)

Conscious business Wikipedia

Questions

- What are the features of conscious capitalism?

- Do firms “get the shareholders they deserve”?

- How might firms that are not pursuing conscious capitalism be persuaded to become more conscious and more caring?

- How does conscious capitalism differ from corporate social responsibility?

- What would you understand by “conscious consumers”? How might their behaviour differ from other consumers?

- Why might firms engaging in conscious capitalism become more profitable than firms that have a simple aim of profit maximisation?

- What reforms, both internal within a firm and in the legal environment, does John Mackey advocate? Do you agree with his suggestions? What else do you suggest?

When you hear about China, it’s often regarding their huge population, their strong growth or their dominance in exports. But, when it comes to baby milk, China is certainly an importer – and a big one at that. For many new parents, getting the ‘real thing’ when it comes to baby formula is absolutely essential.

When you hear about China, it’s often regarding their huge population, their strong growth or their dominance in exports. But, when it comes to baby milk, China is certainly an importer – and a big one at that. For many new parents, getting the ‘real thing’ when it comes to baby formula is absolutely essential.

Chinese baby formula is feared by many new parents, due to the potential for it to contain hormones and dangerous chemicals. This has led them to go to great lengths to ensure they have sufficient supplies of imported baby formula, often only trusting it if it has been hand carried from overseas. However, such is the demand for this safe version of baby milk that the global response has been to place restrictions on it. Essentially, we are seeing a system of rationing emerging.

Hong Kong was the first government to limit the amount bought to two cans of formula per day, with the potential for a fine of over $64,000 and up to two years in prison for those who do not abide by the rules. The UK has now also responded with restrictions on the quantity that can be purchased and other countries may follow suit if the excess demand continues.

According to Sainsburys:

As a short-term measure, retailers including Sainsbury’s are limiting the amount of baby milk powder that people can buy. In this way we aim to ensure a constant supply for our customers and we therefore hope they won’t be inconvenienced.

The Chinese government has reacted to this and is aiming to restore confidence in the food industry, but as yet there has been little positive effect and until there are 100% guarantees of food safety the surge in demand for baby formula from abroad is likely to continue.

This policy of rationing is clearly not only going to affect Chinese parents looking to import baby formula, but is already having an impact on domestic residents. Parents living in the UK are feeling the rationing effects and are also being restricted in terms of how many cans of formula they can buy per day. For many families this isn’t a problem, but for those with multiple children and for whom a trip to the supermarket is not a simple task, the restrictions on baby milk purchases is likely to become a problem. The following articles consider this topic.

Baby milk rationing: Chinese fears spark global restrictions BBC News, Celia Hatton (10/4/13)

Stop rationing information about baby formula milk The Telegraph, Rosie Murray-West (9/4/13)

Baby milk rationed in UK over China export fear BBC News (8/4/13)

Baby Formula rationed in UK over China demand Sky News (9/4/13)

Supermarkets limit sales of baby milk to stop bulk buying to feed China market Independent, Emma Bamford (8/4/13)

Cahinese thirst for formula spurs rationing Financial Times, Amie Tsang and Louise Lucas (7/4/13)

Entrepreneurs milk Chinese thirst for formula Financial Times, Amie Tsang and Louise Lucas (7/4/13)

Baby milk powder rationing introduced by supermarkets The Guardian, Rebecca Smithers (8/4/13)

Questions

- Using a diagram of demand and supply, illustrate how a shortage for a product can emerge. How does the price mechanism usually work to eliminate a shortage?

- What actions can be taken to deal with a shortage?

- How will more stringent regulations by the Chinese government help to restore confidence in Chinese baby milk formula?

- What impact will the imports of baby milk formula into China have on China’s exchange rate and its balance of payments?

- How could this situation be taken advantage of by entrepreneurs? Could it be used as a viable business opportunity?

The UK economy faces a growing problem of energy supplies as energy demand continues to rise and as old power stations come to the end of their lives. In fact some 10% of the UK’s electricity generation capacity will be shut down this month.

The UK economy faces a growing problem of energy supplies as energy demand continues to rise and as old power stations come to the end of their lives. In fact some 10% of the UK’s electricity generation capacity will be shut down this month.

Energy prices have risen substantially over the past few years and are set to rise further. Partly this is the result of rising global gas prices.

In 2012, the response to soaring gas prices was to cut gas’s share of generation from 39.9% per cent to 27.5%. Coal’s share of generation increased from 29.5% to 39.3%, its highest share since 1996 (see The Department of Energy and Climate Change’s Energy trends section 5: electricity). But with old coal-fired power stations closing down and with the need to produce a greater proportion of energy from renewables, this trend cannot continue.

But new renewable sources, such as wind and solar, take a time to construct. New nuclear takes much longer (see the News Item, Going nuclear). And electricity from these low-carbon sources, after taking construction costs into account, is much more expensive to produce than electricity from coal-fired power stations.

But new renewable sources, such as wind and solar, take a time to construct. New nuclear takes much longer (see the News Item, Going nuclear). And electricity from these low-carbon sources, after taking construction costs into account, is much more expensive to produce than electricity from coal-fired power stations.

So how will the change in balance between demand and supply affect prices and the security of supply in the coming years. Will we all have to get used to paying much more for electricity? Do we increasingly run the risk of the lights going out? The following video explores these issues.

Webcast

UK may face power shortages as 10% of energy supply is shut down BBC News, Joe Lynam (4/4/13)

Data

Electricity Statistics Department of Energy & Climate Change

Quarterly energy prices Department of Energy & Climate Change

Questions

- What factors have led to a rise in electricity prices over the past few years? Distinguish between demand-side and supply-side factors and illustrate your arguments with a diagram.

- Are there likely to be power cuts in the coming years as a result of demand exceeding supply?

- What determines the price elasticity of demand for electricity?

- What measures can governments adopt to influence the demand for electricity? Will these affect the position and/or slope of the demand curve?

- Why have electricity prices fallen in the USA? Could the UK experience falling electricity prices for similar reasons in a few years’ time?

- In what ways could the government take into account the externalities from power generation and consumption in its policies towards the energy sector?

The English Premier League (EPL) has negotiated a record TV deal which will generate £5.5 billion of revenue over the next 3 years – beginning in the season 2013–14. This represents a 70% increase on the previous deal. Controversy has arisen over some initial proposals put forward by the EPL as to how the money will be spent. The owners of the clubs in the Championship of the English Football League (EFL) are particularly concerned about the size of the proposed payments to the three teams relegated from the EPL.

The English Premier League (EPL) has negotiated a record TV deal which will generate £5.5 billion of revenue over the next 3 years – beginning in the season 2013–14. This represents a 70% increase on the previous deal. Controversy has arisen over some initial proposals put forward by the EPL as to how the money will be spent. The owners of the clubs in the Championship of the English Football League (EFL) are particularly concerned about the size of the proposed payments to the three teams relegated from the EPL.

Some 30 years ago the money generated from the sale of television rights was equally shared between all the teams in the then four divisions of the English Football League (EFL). In 1992 the top division of the English Football League broke away and formed the English Premier League (EPL). This newly formed EPL negotiated a separate television deal and kept the majority of the money. However, some payments were and still are made to the teams in the EFL and to organisations such as the League Managers Association and Professional Footballers Association. For example in 2011-–12 the EPL donated £189.4 million of the £1.2 billion generated from that year’s TV deal.

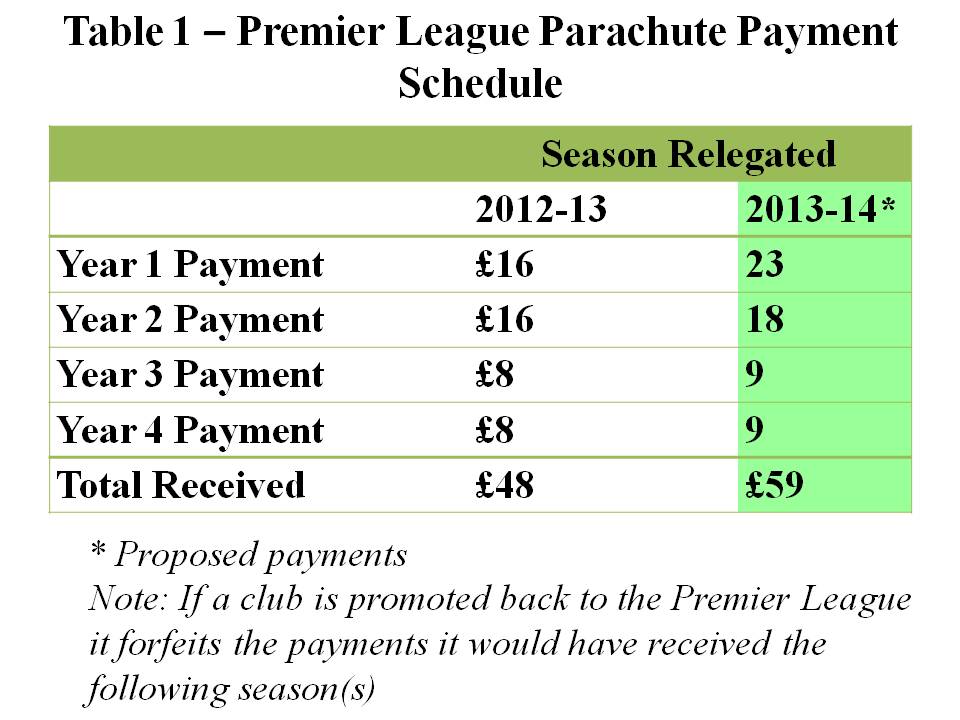

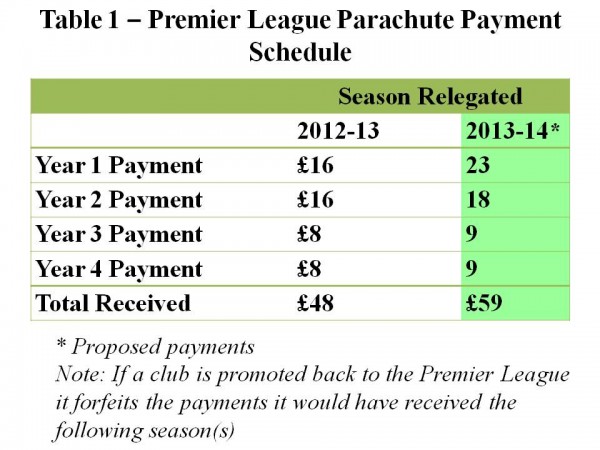

The majority of the money donated by the EPL is spent in two main ways. First, some money is redistributed to all the teams in the EFL: i.e. The Championship, League 1 and League 2. These are known as ‘solidarity payments’ and in 2011–12 the EPL spent £49.8 million on this scheme. Each club in the Championship received £2.3 million. It has been proposed that the amount paid into this scheme should be increased by 5% in the season 2013–14. Second, a relatively large amount of money is paid over a four-year period to the three teams relegated each season from the EPL into the Championship. These are known as ‘parachute payments’ and in the season 2011–12 the EPL spent £90.9 million on this scheme. The rationale for having parachute payments is to help the relegated teams adjust their wage bills to the much lower revenue streams that come from playing in the Championship. Proposed changes to the scheme are outlined in Table 1.

The chairmen of the football league clubs met on the 20th March 2013 and a number of them expressed concerns about the relatively large increase in the parachute payments compared to the solidarity payments. They were particularly concerned that the changes to the funding would damage the competitive balance of the Championship.

The chairmen of the football league clubs met on the 20th March 2013 and a number of them expressed concerns about the relatively large increase in the parachute payments compared to the solidarity payments. They were particularly concerned that the changes to the funding would damage the competitive balance of the Championship.

Competitive balance refers to how the most talented players are distributed amongst the teams in a league. For example, are the majority of the most talented footballers playing for just a couple of the teams? In this case the league is competitively imbalanced and the teams with the best players will tend to win far more games than the other teams. The outcome of the league will be very predictable. If the most talented players were more evenly spread across all the teams in the league, then it would be more competitively balanced. Matches and the outcome of the league would become more unpredictable.

Does the level of competitive balance matter? Some sports economists have argued that it may have a significant impact on the success of the league. This is because fans may value the unpredictability of the results. It follows that closer and more unpredictable results will generate higher match-day attendances and increase the revenues of the clubs.

This is an interesting argument and is the opposite of what economic theory would predict for most markets. For example, the standard prediction would be that as firms outperform their rivals, they generate more revenue and profit. If they manage to drive all their rivals out of business, they would become a pure monopoly and make large abnormal profits. However in professional team sports the outcome may differ significantly. If the unpredictability of the league is highly valued by fans, then teams will generate more revenue when they have strong and evenly matched rivals.

It has been reported that further discussions about the distribution of the money will take place this month with the owners of the championship clubs arguing that there should be smaller increases in parachute payments and much larger increases in solidarity payments. Representatives of the EPL have argued that the parachute payments do not distort competition and make the championship predictable. They point out that at present only one of the top six teams in the championship (Hull) receives parachute payments, while only one of the teams promoted from the Championship in the season 2012–13 (West Ham) received these payments.

Articles

Premier League warned over rich and poor split in wake of TV deal The Guardian, Owen Gibson (19/3/13)

Championship clubs angered by Premier League parachute boost Daily Mail, Charles Sale (6/2/13)

Football league is to lessen the advantage of parachute payments The Guardian, Owen Gibson (20/3/13)

Championship clubs warn Premier League over hike in parachute payments for relegated teams The Independent, Majid Mohamed (20/3/13)

Increased parachute payments could lead to a salary cap in the Championship The Post, A. Stockhausen (21/3/13)

Scudamore:Parachute payment system fair Eurosport, Andy Eckardt (22/3/13)

Parachute payments more than a softened landing The Daisy Cutter, Richard Brook (21/3/13)

Questions

- What factors will influence the size of the attendance at a football match?

- To what extent do you think that the money generated from the sale of television rights should be equally shared between all the clubs in the English Premier League and the English Football League

- Can you think of any ways of measuring the competitive balance of a football league?

- Explain why a very competitively imbalanced league may reduce the revenue for all the clubs in that league?.

- In traditional economic theory it is assumed that firms aim to maximise their profits. What do you think is the objective of a typical football club in the English Premier League?

The growth of emerging economies, such as China, India and Brazil brings with it both good and bad news for the once dominant countries of the West. With growth rates in China reaching double digits and a much greater resilience to the credit crunch and its aftermath in these emerging nations, they became the hope of the recovery for the West. But, is it only benefits that emerge from the growth in countries like China?

The growth of emerging economies, such as China, India and Brazil brings with it both good and bad news for the once dominant countries of the West. With growth rates in China reaching double digits and a much greater resilience to the credit crunch and its aftermath in these emerging nations, they became the hope of the recovery for the West. But, is it only benefits that emerge from the growth in countries like China? Smithfield Foods is a US giant, specialising in the production and selling of pork. A takeover by China’s Shuanghui International Holdings has been approved (albeit reluctantly) by the US Committee on Foreign Investment. While the takeover could still run into obstacles, this Committee’s approval is crucial, as it alleviates concerns over the impact on national security. The value of the deal is some $7.1bn, including the debt that Shuangui will have to take on. While some see this takeover as good news, others are more concerned, identifying the potential negative impact it may have on prices and standards in the USA. Zhijun Yang, Shuanghui’s Chief Executive said:

Smithfield Foods is a US giant, specialising in the production and selling of pork. A takeover by China’s Shuanghui International Holdings has been approved (albeit reluctantly) by the US Committee on Foreign Investment. While the takeover could still run into obstacles, this Committee’s approval is crucial, as it alleviates concerns over the impact on national security. The value of the deal is some $7.1bn, including the debt that Shuangui will have to take on. While some see this takeover as good news, others are more concerned, identifying the potential negative impact it may have on prices and standards in the USA. Zhijun Yang, Shuanghui’s Chief Executive said: