With the growing recognition of the global climate emergency (see also), attention is being increasingly focused on policies to tackle global warming.

In the October version of its journal, Fiscal Monitor, the IMF argues that carbon taxes can play a major part in meeting the goal of achieving net zero carbon emissions by 2050 or earlier.

As the blog accompanying the journal states:

Global warming has become a clear and present threat. Actions and commitments to date have fallen short. The longer we wait, the greater the loss of life and damage to the world economy. Finance ministers must play a central role to champion and implement fiscal policies to curb climate change. To do so, they should reshape the tax system and fiscal policies to discourage carbon emissions from coal and other polluting fossil fuels.

The effect of a carbon tax on production

The argument is that carbon emissions represent a massive negative externality, where the costs are borne largely by people other than the emitters. Taxes can internalise these externalities. The effect would be to raise the price of carbon-emitting activities and reduce the quantity consumed and hence produced.

The diagram illustrates the argument. It takes the case of carbon emissions from coal-fired electricity generation in a large country. To keep the analysis simple, it is assumed that all electricity in the country is generated from coal-fired power stations and that there are many such power stations, making the market perfectly competitive.

It is assumed that all the benefits from electricity production accrue solely to the consumers of electricity (i.e. there are no external benefits from consumption). Marginal private and marginal social benefits of the production of electricity are thus the same (MPB = MSB). The curve slopes downwards because, with a downward-sloping demand for electricity, higher output results in a lower marginal benefit (diminishing marginal utility).

Competitive market forces, with producers and consumers responding only to private costs and benefits, will result in a market equilibrium at point a in the diagram: i.e. where demand equals supply. The market equilibrium price is P0 while the market equilibrium quantity is Q0. However the presence of external costs in production means that MSC > MPC. In other words, MEC = b – a.

The socially optimal output would be Q* where P = MSB = MSC, achieved at the socially optimal price of P*. This is illustrated at point d and clearly shows how external costs of production in a perfectly competitive market result in overproduction: i.e. Q0 > Q*. From society’s point of view, too much electricity is being produced and consumed.

If a carbon tax of d – c is imposed on the electricity producers, it will now be in producers’ interests to produce at Q*, where their new private marginal costs (including tax) equals their marginal private benefit.

Assessing the benefits of carbon taxes

The diagram shows the direct effect on production of electricity. With widespread carbon taxes, there would be similar direct effects on other industries that emit carbon, and also on consumers, faced with higher fuel prices. In the UK, for example, there are currently higher taxes on high-emissions vehicles than on low-emissions ones.

However, there are other effects of carbon taxes which contribute to the reduction in carbon emissions over the longer term. First, firms will have an incentive to invest in green energy production, such as wind, solar and hydro. Second, it will encourage R&D in green energy technology. Third, consumers will have an incentive to use less electricity by investing in more efficient appliances and home insulation and making an effort to turn off lights, the TV, computers and so on.

People may object to paying more for electricity, gas and motor fuel, but the tax revenues could be invested in cheaper clean public transport, home insulation and public services generally, such as health and education. This could be part of a policy of redistribution, with the tax revenues being spent on alleviating poverty. Alternatively, other taxes could be cut.

The IMF estimates that to restrict global warming to 2°C (a target seen as too modest by many environmentalists), large emitting countries ‘should introduce a carbon tax set to rise quickly to $75 a ton in 2030’.

This would mean household electric bills would go up by 43 per cent cumulatively over the next decade on average – more in countries that still rely heavily on coal in electricity generation, less elsewhere. Gasoline would cost 14 percent more on average.

It gives the example of Sweden, which has a carbon tax of $127 per ton. This has resulted in a 25% reduction in emissions since 1995, while the economy has expanded 75% since then.

Limits of carbon taxes

Although carbon taxes can make a significant contribution to combatting global warming, there are problems with their use.

First, it may be politically popular for governments not to impose them, or raise them, with politicians arguing that they are keen to help ‘struggling motorists’ or poor people ‘struggling to keep their homes warm’. In the UK, successive governments year after year have chosen not to raise road fuel taxes, despite a Fuel Price Escalator (replaced in 2011 by a Fuel Duty Stabiliser) designed to raise fuel taxes each year by more than inflation. Also, governments fear that higher energy prices would raise costs for their country’s industries, thereby damaging exports.

Second, it is difficult to measure the marginal external costs of CO2 emissions, which gives ammunition to those arguing to keep taxes low. In such cases it may be prudent, if politically possible, to set carbon taxes quite high.

Third, they should not be seen as a sufficient policy on their own, but as just part of the solution to global warming. Legislation to prevent high emissions can be another powerful tool to prevent activities that have high carbon emissions. Examples include banning high-emission vehicles; a requirement for coal-fired power stations and carbon emitting factories to install CO2scrubbers (filters); and tougher planning regulations for factories that emit carbon. Education to encourage people to cut their own personal use of fossil fuels is another powerful means of influencing behaviour.

A cap-and-trade system, such as the European Emissions Trading Scheme would be an alternative means of cutting carbon efficiently. It involves setting quotas for emissions and allowing firms which manage to cut emissions to sell their surplus permits to less efficient firms. This puts a price pressure on firms to be more efficient. But the quotas (the ‘cap’) must be sufficiently tight if emissions are going to be cut to desired levels.

But, despite being just one possible policy, carbon taxes can make a significant contribution to combatting global warming.

IMF Fiscal Monitor, Ian Parry (team leader), Thomas Baunsgaard, William Gbohoui, Raphael Lam, Victor Mylonas, Mehdi Raissi, Alpa Shah and Baoping Shang (October 2019)

Questions

Draw a diagram to show how subsidies can lead to the optimum output of green energy.

What are the political problems in introducing or raising carbon taxes? Examine possible solutions to these problems

Choose two policies for reducing carbon emissions other than using carbon taxes? Compare their effectiveness with carbon taxes.

How is game theory relevant to getting international agreement on cutting greenhouse gas emissions? Why is there likely to be a prisoners’ dilemma problem in reaching and sticking to such agreements? How might the problem of a prisoners’ dilemma be overcome in such circumstances?

There is increasing recognition that the world is facing a climate emergency. Concerns are growing about the damaging effects of global warming on weather patterns, with increasing droughts, forest fires, floods and hurricanes. Ice sheets are melting and glaciers retreating, with consequent rising sea levels. Habitats and livelihoods are being destroyed. And many of the effects seem to be occurring more rapidly than had previously been expected.

Extinction Rebellion has staged protests in many countries; the period from 20 to 27 September saw a worldwide climate strike (see also), with millions of people marching and children leaving school to protest; a Climate Action Summit took place at the United Nations, with a rousing speech by Greta Thunberg, the 16 year-old Swedish activist; the UN’s Intergovernmental Panel on Climate Change (IPCC) has just released a report with evidence showing that the melting of ice sheets and rising sea levels is more rapid than previously thought; at its annual party conference in Brighton, the Labour Party pledged that, in government, it would bring forward the UK’s target for zero net carbon emissions from 2050 to 2030.

Increasingly attention is focusing on what can be done. At first sight, it might seem as if the answer lies solely with climate scientists, environmentalists, technologists, politicians and industry. When the matter is discussed in the media, it is often the environment correspondent, the science correspondent, the political correspondent or the business correspondent who reports on developments in policy. But economics has an absolutely central role to play in both the analysis of the problem and in examining the effectiveness of alternative solutions.

One of the key things that economists do is to examine incentives and how they impact on human behaviour. Indeed, understanding the design and effectiveness of incentives is one of the 15 Threshold Concepts we identify in the Sloman books.

One of the most influential studies of the impact of climate change and means of addressing it was the study back in 2006, The Economics of Climate Change: The Stern Review, led by the economist Sir Nicholas Stern. The Review reflected economists’ arguments that climate change represents a massive failure of markets and of governments too. Firms and individuals can emit greenhouse gases into the atmosphere at no charge to themselves, even though it imposes costs on others. These external costs are possible because the atmosphere is a public good, which is free to exploit.

Part of the solution is to ‘internalise’ these externalities by imposing charges on people and firms for their emissions, such as imposing higher taxes on cars with high exhaust emissions or on coal-fired power stations. This can be done through the tax system, with ‘green’ taxes and charges. Economists study the effectiveness of these and how much they are likely to change people’s behaviour.

Another part of the solution is to subsidise green alternatives, such as solar and wind power, that provide positive environmental externalities. But again, just how responsive will demand be? This again is something that economists study.

Of course, changing human behaviour is not just about raising the prices of activities that create negative environmental externalities and lowering the prices of those that create positive ones. Part of the solution lies in education to make people aware of the environmental impacts of their activities and what can be done about it. The problem here is that there is a lack of information – a classic market failure. Making people aware of the consequences of their actions can play a key part in the economic decisions they make. Economists study the extent that imperfect information distorts decision making and how informed decision making can improve outcomes.

Another part of the solution may be direct government investment in green technologies or the use of legislation to prevent or restrict activities that contribute to global warming. But in each case, economists are well placed to examine the efficacy and the costs and benefits of alternative policies. Economists have the tools to make cost–benefit appraisals.

Economists also study the motivations of people and how they affect their decisions, including decisions about whether or not to take part in activities with high emissions, such air travel, and decisions on ‘green’ activities, such as eating less meat and more vegetables.

If you are starting out on an economics degree, you will soon see that economists are at the centre of the analysis of some of the biggest issues of the day, such as climate change and the environment generally, inequality and poverty, working conditions, the work–life balance, the price of accommodation, the effects of populism and the retreat from global responsibility and, in the UK especially, the effects of Brexit, of whatever form.

Intergovernmental Panel on Climate Change (IPCC) (25/9/19)

Questions

Explain what is meant by environmental externalities.

Compare the relative merits of carbon taxes and legislation as means of reducing carbon emissions.

If there is a climate emergency, why are most governments unwilling to take the necessary measures to make their countries net carbon neutral within the next few years?

In what ways would you suggest incentivising (a) individuals and (b) firms to reduce carbon emissions? Explain your reasoning.

For what reasons are the burdens of climate changed shared unequally between people across the globe?

In 2015, at the COP21 climate change conference in Paris, an agreement was reached between the 195 countries present. The Paris agreement committed countries to limiting global warming to ‘well below’ 2°C and preferably to no more than 1.5°C. above pre-industrial levels. To do this, a ‘cap-and-trade’ system would be adopted, with countries agreeing to limits to their emissions and then being able to buy emissions credits to exceed these limits from countries which had managed to emit below their limits. However, to implement the agreement, countries would need to adopt a ‘rulebook’ about how the permitted limits would be applied, how governments would measure and report emissions cuts, how the figures would be verified and just how a cap-and-trade system would work.

At the COP24 meeting from 2 to 15 December 2018 in Katowice, Poland, nearly 14 000 delegates from 196 countries discussed the details of a rulebook. Despite some 2800 points of contention and some difficult and heated negotiations, agreement was finally reached. Rules for targeting, measuring and verifying emissions have been accepted. If countries exceed their limits, they must explain why and also how they will meet them in future. Rich countries agreed to provide help to poor countries in curbing their emissions and adapting to rising sea levels, droughts, floods and other climate-induced problems.

But no details have been agreed on the system of carbon trading, thanks to objections from the Brazilian delegates, who felt that insufficient account would be made of their country’s existing promises on not chopping down parts of the Amazon rainforest.

Most seriously, the measures already agreed which would be covered by the rulebook will be insufficient to meet the 2°C, let alone the 1.5°C, target. The majority of the measures are voluntary ‘nationally determined contributions’, which countries are required to submit under the Paris agreement. These, so far, would probably be sufficient to limit global warming to only around 3°C, at which level there would be massive environmental, economic and social consequences.

There was, however, a belief among delegates that further strong international action was required. Indeed, under the Paris agreement, emissions limits to keep global warming to the ‘well below 2°C’ level must be agreed by 2020.

Climate change is a case of severe market failure. A large proportion of the external costs of pollution are borne outside the countries where the emitters are based. This creates a disincentive for countries acting alone to internalise all these externalities through the tax system or charges, or to regulate them toughly. Only by countries taking an international perspective and by acting collectively can the externalities be seen as a fully internal problem.

Even though most governments recognise the nature and scale of the problem, one of the biggest problems they face is in persuading people that it is in their interests to cut carbon emissions – something that may become increasingly difficult with the rise in populism and the realisation that higher fuel and other prices will make people poorer in the short term.

The Conversation, David Farrell and Hamid Homatash (10/12/18)

Questions

To what extent can the atmosphere been seen as a ‘global commons’?

What incentives might be given for business to make ‘green investments’?

To what extent might changes in technology help businesses and consumers to ‘go green’?

Why might international negotiations over tackling climate change result in a prisoner’s dilemma problem? What steps could be taken to tackle the problem?

How would an emissions cap-and-trade system work?

Investigate the Brazilian objections to the proposals for emissions credits. Were the delegates justified in their objections?

What types of initiative could businesses take to tackle ‘supply chain emissions’?

How could countries, such as the USA, be persuaded to reduce their reliance on coal – an industry lauded by President Trump?

In December 2015, countries from around the world met in Paris at the United Nations Intergovernmental Panel on Climate Change (IPCC). The key element of the resulting Paris Agreement was to keep ‘global temperature rise this century well below 2 degrees Celsius above pre-industrial levels and to pursue efforts to limit the temperature increase even further to 1.5 degrees Celsius.’ At the same time it was agreed that the IPCC would conduct an analysis of what would need to be done to limit global warming to 1.5°C. The IPPC has just published its report.

The report, based on more than 6000 scientific studies, has been compiled by more than 80 of the world’s top climate scientists. It states that, with no additional action to mitigate climate change beyond that committed in the Paris Agreement, global temperatures are likely to rise to the 1.5°C point somewhere between 2030 and 2040 and then continue rising above that, reaching 3°C by the end of the century.

According to the report, the effects we are already seeing will accelerate. Sea levels will rise as land ice caps and glaciers melt, threatening low lying coastal areas; droughts and floods will become more severe; hurricanes and cyclones will become stronger; the habits of many animals will become degraded and species will become extinct; more coral reefs will die and fish species disappear; more land will become uninhabitable; more displacement and migration will take place, leading to political tensions and worse.

Two tragedies

The problem of greenhouse gas emissions and global warming is a classic case of the tragedy of the commons. This is where people overuse common resources, such as open grazing land, fishing grounds, or, in this case, the atmosphere as a dump for emissions. They do so because there is little, if any, direct short-term cost to themselves. Instead, the bulk of the cost is borne by others – especially in the future.

There is another related tragedy, which has been dubbed the ‘tragedy of incumbents’. This is a political problem where people in power want to retain that power and do so by appealing to short-term selfish interests. The Trump administration lauds the use of energy as helping to drive the US economy and make people better off. To paraphrase Donald Trump ‘Climate change may be happening, but, hey, let’s not beat ourselves up about it and wear hair shirts. What we do will have little or no effect compared with what’s happening in China and India. The USA is much better off with a strong automobile, oil and power sector.’

What’s to be done?

According to the IPCC report, if warming is not to exceed 1.5℃, greenhouse gas emissions must be reduced by 45% by 2030 and by 100% by around 2050. But is this achievable?

The commitments made in the Paris Agreement will not be nearly enough to achieve these reductions. There needs to be a massive movement away from fossil fuels, with between 70% and 85% of global electricity production being from renewables by 2050. There needs to be huge investment in green technology for power generation, transport and industrial production.

Both these types of policies involve governments taking action, whether through increased carbon taxes on either producers or consumer or both, or through increased subsidies for renewables and other alternatives, or through the use of cap and trade with emissions allocations (either given by government or sold at auction) and carbon trading, or through the use of regulation to prohibit or limit behaviour that leads to emissions. The issue, of course, is whether governments have the will to do anything. Some governments do, but with the election of populist leaders, such as President Trump in the USA, and probably Jair Bolsonaro in Brazil, and with sceptical governments in other countries, such as Australia, this puts even more onus on other governments.

Another avenue is a change in people’s attitudes, which may be influenced by education, governments, pressure groups, news media, etc. For example, if people could be persuaded to eat less meat, drive less (for example, by taking public transport, walking, cycling, car sharing or living nearer to their work), go on fewer holidays, heat their houses less, move to smaller homes, install better insulation, etc., these would all reduce greenhouse gas emissions.

Finally, there is the hope that the market may provide part of the solution. The cost of generating electricity from renewables is coming down and is becoming increasingly competitive with electricity generated from fossil fuels. Electric cars are coming down in price as battery technology develops; also, battery capacity is increasing and recharging is becoming quicker, helping encourage the switch from petrol and diesel cars to electric and hybrid cars. At the same time, various industrial processes are becoming more fuel efficient. But these developments, although helpful, will not be enough to achieve the 1.5°C target on their own.

Intergovernmental Panel on Climate Change (IPCC) (8/10/18)

Questions

Explain the extent to which the problem of global warming is an example of the tragedy of the commons. What other examples are there of the tragedy?

Explain the meaning of the tragedy of the incumbents and its impact on climate change? Does the length of the electoral cycle exacerbate the problem?

With the costs of low or zero carbon technology for energy and transport coming down, is there as case for doing nothing in response to the problem of global warming?

Examine the case for and against using taxes and subsidies to tackle global warming.

Examine the case for and against using regulation to tackle global warming.

Examine the case for and against using cap-and-trade systems to tackle global warming.

Is there a prisoners’ dilemma problem in getting governments to adopt policies to tackle climate change?

What would be the motivation for individuals to ‘do their bit’ to tackle climate change? Other than altering prices or using regulation, how might the government or other agencies set about persuading people to ‘be more green’?

If you were doing a cost–benefit analysis of some project that will have beneficial environmental impacts in the future, how would you set about adjusting the values of these benefits for the fact that they occur in the future and not now?

Last week was a rough week for Britain. The “Beast from the East” and storm Emma swept through the country, bringing with them unusually heavy snowfall, which resulted in severe disruption across nearly all parts of the country. Some recent estimates put the cost of these extreme weather conditions at up to £1 billion per day. The construction industry suffering the biggest hit as work came to a halt for the best part of the week. Losses for the industry were estimated to be up to £2 billion.

Closed restaurants, empty shops and severely disrupted transport networks were all part of the effect that this extreme weather had on the overall economy. According to Howard Archer, chief economic adviser of the EY ITEM Club (a UK forecasting group):

It is possible that the severe weather [of the last few days] could lead to GDP growth being reduced by 0.1 percentage point in Q1 2018 and possibly 0.2 percentage points if the severe weather persist.

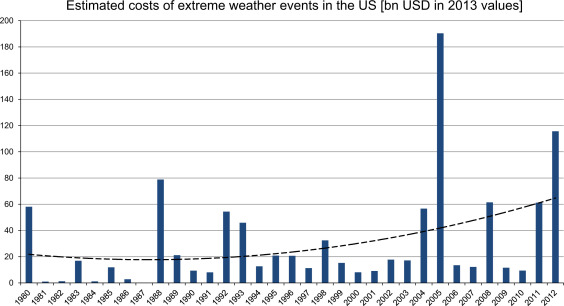

Source: Jahn (2015), Figure 2

As the occurrence of freak weather increases across the globe due to climate change, so does the economic cost of these events. The figure above shows the estimated costs of extreme weather events in the USA between 1980 and 2012 and it is reproduced from Jahn (see link below), who also fits a quadratic trend to show that these costs have been increasing over time. He goes on to characterise the impact of different types of extreme weather (including cold waves, heat waves, storms and others) on different sectors of the local economy – ranging from tourism and agriculture, to housing and the insurance sector.

Linnenluecke et al (linked below) argue that extreme weather caused by climate change could influence the decision of firms on where to locate and could lead to a reshuffle of economic activity across the world and have important policy implications. As the authors explain:

Climate change-related relocation has been given consideration in policy-oriented discussions, but not in management decisions. The effects of climate change and extreme weather events have been considered as peripheral or as a risk factor, but not as a determining factor in firm relocation processes…. This paper therefore [provides] insights for understanding how firms can enhance strategic decision-making in light of understanding and assessing their vulnerability as well as likely impacts that climate change may have on relocation decisions.

The likelihood and associated costs of extreme weather events could therefore become an increasingly important matter for discussion amongst economists and policy makers. Such weather events are likely to have profound economic implications for the world.

With the growing recognition of the global climate emergency (see also), attention is being increasingly focused on policies to tackle global warming.

With the growing recognition of the global climate emergency (see also), attention is being increasingly focused on policies to tackle global warming.  It is assumed that all the benefits from electricity production accrue solely to the consumers of electricity (i.e. there are no external benefits from consumption). Marginal private and marginal social benefits of the production of electricity are thus the same (MPB = MSB). The curve slopes downwards because, with a downward-sloping demand for electricity, higher output results in a lower marginal benefit (diminishing marginal utility).

It is assumed that all the benefits from electricity production accrue solely to the consumers of electricity (i.e. there are no external benefits from consumption). Marginal private and marginal social benefits of the production of electricity are thus the same (MPB = MSB). The curve slopes downwards because, with a downward-sloping demand for electricity, higher output results in a lower marginal benefit (diminishing marginal utility). However, there are other effects of carbon taxes which contribute to the reduction in carbon emissions over the longer term. First, firms will have an incentive to invest in green energy production, such as wind, solar and hydro. Second, it will encourage R&D in green energy technology. Third, consumers will have an incentive to use less electricity by investing in more efficient appliances and home insulation and making an effort to turn off lights, the TV, computers and so on.

However, there are other effects of carbon taxes which contribute to the reduction in carbon emissions over the longer term. First, firms will have an incentive to invest in green energy production, such as wind, solar and hydro. Second, it will encourage R&D in green energy technology. Third, consumers will have an incentive to use less electricity by investing in more efficient appliances and home insulation and making an effort to turn off lights, the TV, computers and so on. Third, they should not be seen as a sufficient policy on their own, but as just part of the solution to global warming. Legislation to prevent high emissions can be another powerful tool to prevent activities that have high carbon emissions. Examples include banning high-emission vehicles; a requirement for coal-fired power stations and carbon emitting factories to install CO2 scrubbers (filters); and tougher planning regulations for factories that emit carbon. Education to encourage people to cut their own personal use of fossil fuels is another powerful means of influencing behaviour.

Third, they should not be seen as a sufficient policy on their own, but as just part of the solution to global warming. Legislation to prevent high emissions can be another powerful tool to prevent activities that have high carbon emissions. Examples include banning high-emission vehicles; a requirement for coal-fired power stations and carbon emitting factories to install CO2 scrubbers (filters); and tougher planning regulations for factories that emit carbon. Education to encourage people to cut their own personal use of fossil fuels is another powerful means of influencing behaviour.  Fiscal Policies to Curb Climate Change

Fiscal Policies to Curb Climate Change There is increasing recognition that the world is facing a climate emergency. Concerns are growing about the damaging effects of global warming on weather patterns, with increasing droughts, forest fires, floods and hurricanes. Ice sheets are melting and glaciers retreating, with consequent rising sea levels. Habitats and livelihoods are being destroyed. And many of the effects seem to be occurring more rapidly than had previously been expected.

There is increasing recognition that the world is facing a climate emergency. Concerns are growing about the damaging effects of global warming on weather patterns, with increasing droughts, forest fires, floods and hurricanes. Ice sheets are melting and glaciers retreating, with consequent rising sea levels. Habitats and livelihoods are being destroyed. And many of the effects seem to be occurring more rapidly than had previously been expected. Part of the solution is to ‘internalise’ these externalities by imposing charges on people and firms for their emissions, such as imposing higher taxes on cars with high exhaust emissions or on coal-fired power stations. This can be done through the tax system, with ‘green’ taxes and charges. Economists study the effectiveness of these and how much they are likely to change people’s behaviour.

Part of the solution is to ‘internalise’ these externalities by imposing charges on people and firms for their emissions, such as imposing higher taxes on cars with high exhaust emissions or on coal-fired power stations. This can be done through the tax system, with ‘green’ taxes and charges. Economists study the effectiveness of these and how much they are likely to change people’s behaviour.  In 2015, at the

In 2015, at the  According to the report, the effects we are already seeing will accelerate. Sea levels will rise as land ice caps and glaciers melt, threatening low lying coastal areas; droughts and floods will become more severe; hurricanes and cyclones will become stronger; the habits of many animals will become degraded and species will become extinct; more coral reefs will die and fish species disappear; more land will become uninhabitable; more displacement and migration will take place, leading to political tensions and worse.

According to the report, the effects we are already seeing will accelerate. Sea levels will rise as land ice caps and glaciers melt, threatening low lying coastal areas; droughts and floods will become more severe; hurricanes and cyclones will become stronger; the habits of many animals will become degraded and species will become extinct; more coral reefs will die and fish species disappear; more land will become uninhabitable; more displacement and migration will take place, leading to political tensions and worse.

want to retain that power and do so by appealing to short-term selfish interests. The Trump administration lauds the use of energy as helping to drive the US economy and make people better off. To

want to retain that power and do so by appealing to short-term selfish interests. The Trump administration lauds the use of energy as helping to drive the US economy and make people better off. To  The commitments made in the

The commitments made in the  Finally, there is the hope that the market may provide part of the solution. The cost of generating electricity from renewables is coming down and is becoming increasingly competitive with electricity generated from fossil fuels. Electric cars are coming down in price as battery technology develops; also, battery capacity is increasing and recharging is becoming quicker, helping encourage the switch from petrol and diesel cars to electric and hybrid cars. At the same time, various industrial processes are becoming more fuel efficient. But these developments, although helpful, will not be enough to achieve the 1.5°C target on their own.

Finally, there is the hope that the market may provide part of the solution. The cost of generating electricity from renewables is coming down and is becoming increasingly competitive with electricity generated from fossil fuels. Electric cars are coming down in price as battery technology develops; also, battery capacity is increasing and recharging is becoming quicker, helping encourage the switch from petrol and diesel cars to electric and hybrid cars. At the same time, various industrial processes are becoming more fuel efficient. But these developments, although helpful, will not be enough to achieve the 1.5°C target on their own.