On 5 and 6 April, there was a conference on conscious capitalism in San Francisco. In January, a new book, Conscious Capitalism: Liberating the Heroic Spirit of Business, by John Mackey and Rajendra Sisodia, was published. Many in the business world are enthusiastic about this seemingly new approach to business, which focuses on broader social, environmental and ethical goals, rather than simple profit maximisation.

On 5 and 6 April, there was a conference on conscious capitalism in San Francisco. In January, a new book, Conscious Capitalism: Liberating the Heroic Spirit of Business, by John Mackey and Rajendra Sisodia, was published. Many in the business world are enthusiastic about this seemingly new approach to business, which focuses on broader social, environmental and ethical goals, rather than simple profit maximisation.

As the Washington Times review linked to below states:

“Conscious Capitalism” promotes a business culture that embodies “trust, accountability, caring, transparency, integrity, loyalty and egalitarianism.” The management ideal of “Conscious Capitalism” contains four key elements of “decentralization, empowerment, innovation and collaboration.” Above all, this exemplary form of business practice relies on careful attention to four tenets: higher purpose and core values, stakeholder integration, conscious leadership and conscious culture and management.

So how realistic is this vision of caring capitalism? There may be a few inspiring businesspeople, truly committed to improving the interests of the various stakeholders of their business and society more generally, but could it become a model for business in general? And if so, does this require education, monitoring and regulation? Or can a libertarian approach to business generate an environment where conscious and caring capitalists flourish and succeed better than those with a more narrow focus on profit?

So how realistic is this vision of caring capitalism? There may be a few inspiring businesspeople, truly committed to improving the interests of the various stakeholders of their business and society more generally, but could it become a model for business in general? And if so, does this require education, monitoring and regulation? Or can a libertarian approach to business generate an environment where conscious and caring capitalists flourish and succeed better than those with a more narrow focus on profit?

The following videos and articles discuss conscious capitalism and the arguments of those, such as John Mackey, founder and co-CEO of Whole Food Market, who advocate it.

Webcasts

Conscious capitalism The Economist, John Mackey (15/3/13)

Conscious capitalism The Economist, John Mackey (15/3/13)

Conscious Capitalism: Heroes of the Business World Conscious capitalism, April in San Francisco (5/4/13)

It’s Not Corporate Social Responsibility Conscious capitalism, John Mackey (Jan 13)

Articles, reviews and information

Conscious Capitalism: Creating a New Paradigm for Business Whole Planet Foundation, John Mackey

Companies that Practice “Conscious Capitalism” Perform 10x Better Harvard Business Review, Tony Schwartz (4/4/13)

4 Ways to Become a (More) Conscious Capitalist Inc., Francesca Louise Fenzi (8/4/13)

The New Management Paradigm & John Mackey’s Whole Foods Forbes, Steve Denning (5/1/13)

Book Review: ‘Conscious Capitalism’ Washington Times, Anthony j. Sadar (20/3/13)

Book Review: Whole Foods Co-CEO John Mackey’s Conscious Capitalism Huffington Post, Christine Bader (28/1/13)

Chicken Soup for a Davos Soul Wall Street Journal, Alan Murray (16/1/13)

Conscious business Wikipedia

Questions

- What are the features of conscious capitalism?

- Do firms “get the shareholders they deserve”?

- How might firms that are not pursuing conscious capitalism be persuaded to become more conscious and more caring?

- How does conscious capitalism differ from corporate social responsibility?

- What would you understand by “conscious consumers”? How might their behaviour differ from other consumers?

- Why might firms engaging in conscious capitalism become more profitable than firms that have a simple aim of profit maximisation?

- What reforms, both internal within a firm and in the legal environment, does John Mackey advocate? Do you agree with his suggestions? What else do you suggest?

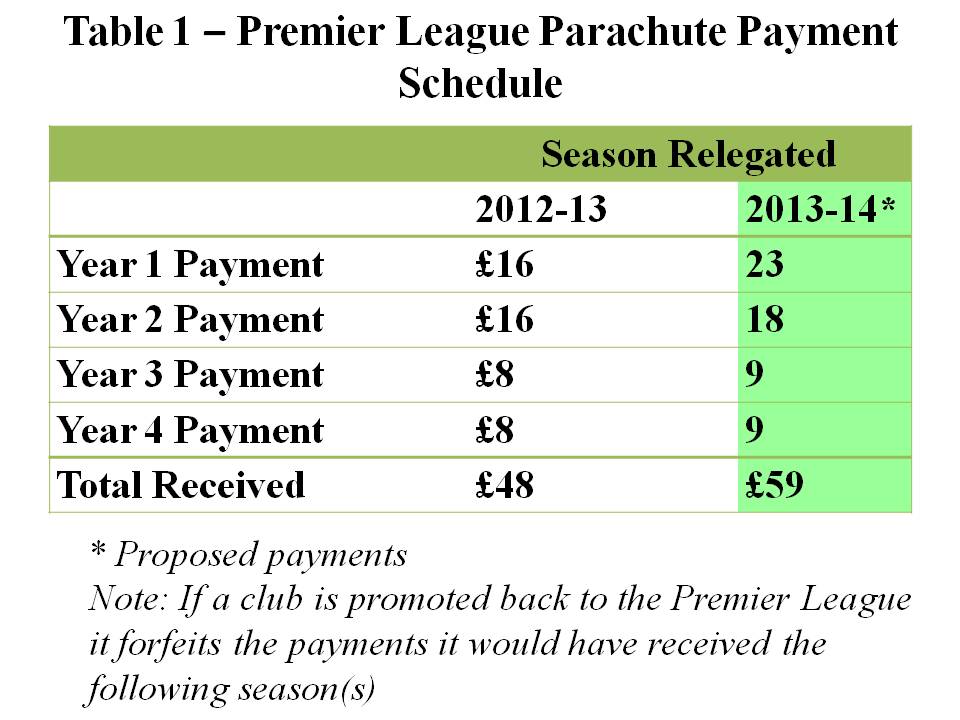

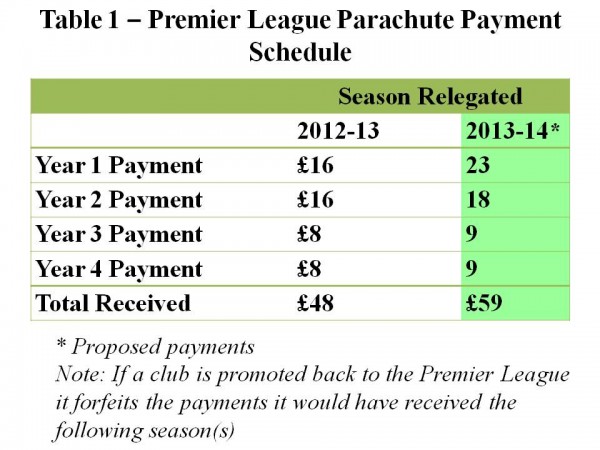

The English Premier League (EPL) has negotiated a record TV deal which will generate £5.5 billion of revenue over the next 3 years – beginning in the season 2013–14. This represents a 70% increase on the previous deal. Controversy has arisen over some initial proposals put forward by the EPL as to how the money will be spent. The owners of the clubs in the Championship of the English Football League (EFL) are particularly concerned about the size of the proposed payments to the three teams relegated from the EPL.

The English Premier League (EPL) has negotiated a record TV deal which will generate £5.5 billion of revenue over the next 3 years – beginning in the season 2013–14. This represents a 70% increase on the previous deal. Controversy has arisen over some initial proposals put forward by the EPL as to how the money will be spent. The owners of the clubs in the Championship of the English Football League (EFL) are particularly concerned about the size of the proposed payments to the three teams relegated from the EPL.

Some 30 years ago the money generated from the sale of television rights was equally shared between all the teams in the then four divisions of the English Football League (EFL). In 1992 the top division of the English Football League broke away and formed the English Premier League (EPL). This newly formed EPL negotiated a separate television deal and kept the majority of the money. However, some payments were and still are made to the teams in the EFL and to organisations such as the League Managers Association and Professional Footballers Association. For example in 2011-–12 the EPL donated £189.4 million of the £1.2 billion generated from that year’s TV deal.

The majority of the money donated by the EPL is spent in two main ways. First, some money is redistributed to all the teams in the EFL: i.e. The Championship, League 1 and League 2. These are known as ‘solidarity payments’ and in 2011–12 the EPL spent £49.8 million on this scheme. Each club in the Championship received £2.3 million. It has been proposed that the amount paid into this scheme should be increased by 5% in the season 2013–14. Second, a relatively large amount of money is paid over a four-year period to the three teams relegated each season from the EPL into the Championship. These are known as ‘parachute payments’ and in the season 2011–12 the EPL spent £90.9 million on this scheme. The rationale for having parachute payments is to help the relegated teams adjust their wage bills to the much lower revenue streams that come from playing in the Championship. Proposed changes to the scheme are outlined in Table 1.

The chairmen of the football league clubs met on the 20th March 2013 and a number of them expressed concerns about the relatively large increase in the parachute payments compared to the solidarity payments. They were particularly concerned that the changes to the funding would damage the competitive balance of the Championship.

The chairmen of the football league clubs met on the 20th March 2013 and a number of them expressed concerns about the relatively large increase in the parachute payments compared to the solidarity payments. They were particularly concerned that the changes to the funding would damage the competitive balance of the Championship.

Competitive balance refers to how the most talented players are distributed amongst the teams in a league. For example, are the majority of the most talented footballers playing for just a couple of the teams? In this case the league is competitively imbalanced and the teams with the best players will tend to win far more games than the other teams. The outcome of the league will be very predictable. If the most talented players were more evenly spread across all the teams in the league, then it would be more competitively balanced. Matches and the outcome of the league would become more unpredictable.

Does the level of competitive balance matter? Some sports economists have argued that it may have a significant impact on the success of the league. This is because fans may value the unpredictability of the results. It follows that closer and more unpredictable results will generate higher match-day attendances and increase the revenues of the clubs.

This is an interesting argument and is the opposite of what economic theory would predict for most markets. For example, the standard prediction would be that as firms outperform their rivals, they generate more revenue and profit. If they manage to drive all their rivals out of business, they would become a pure monopoly and make large abnormal profits. However in professional team sports the outcome may differ significantly. If the unpredictability of the league is highly valued by fans, then teams will generate more revenue when they have strong and evenly matched rivals.

It has been reported that further discussions about the distribution of the money will take place this month with the owners of the championship clubs arguing that there should be smaller increases in parachute payments and much larger increases in solidarity payments. Representatives of the EPL have argued that the parachute payments do not distort competition and make the championship predictable. They point out that at present only one of the top six teams in the championship (Hull) receives parachute payments, while only one of the teams promoted from the Championship in the season 2012–13 (West Ham) received these payments.

Articles

Premier League warned over rich and poor split in wake of TV deal The Guardian, Owen Gibson (19/3/13)

Championship clubs angered by Premier League parachute boost Daily Mail, Charles Sale (6/2/13)

Football league is to lessen the advantage of parachute payments The Guardian, Owen Gibson (20/3/13)

Championship clubs warn Premier League over hike in parachute payments for relegated teams The Independent, Majid Mohamed (20/3/13)

Increased parachute payments could lead to a salary cap in the Championship The Post, A. Stockhausen (21/3/13)

Scudamore:Parachute payment system fair Eurosport, Andy Eckardt (22/3/13)

Parachute payments more than a softened landing The Daisy Cutter, Richard Brook (21/3/13)

Questions

- What factors will influence the size of the attendance at a football match?

- To what extent do you think that the money generated from the sale of television rights should be equally shared between all the clubs in the English Premier League and the English Football League

- Can you think of any ways of measuring the competitive balance of a football league?

- Explain why a very competitively imbalanced league may reduce the revenue for all the clubs in that league?.

- In traditional economic theory it is assumed that firms aim to maximise their profits. What do you think is the objective of a typical football club in the English Premier League?

In 2009, the European Commission investigated Microsoft’s practice of bundling its own browser, Internet Explorer, with new copies of Windows. It found that this was an abuse of market power and created an unfair barrier to entry of other browsers, such as Firefox.

In 2009, the European Commission investigated Microsoft’s practice of bundling its own browser, Internet Explorer, with new copies of Windows. It found that this was an abuse of market power and created an unfair barrier to entry of other browsers, such as Firefox.

An agreement was reached that Microsoft would include a ‘choice screen’ in which users in the EU would be given a full list of alternative browsers and asked which they would like to install. On making their selection, a link would take them to the browser site to download the installation program. This screen would be available until 2014. Between March 2010, when the choice screen was first provided and November of the same year, 84 million browsers were downloaded through it.

In May 2011, however, the screen was no longer present on new Windows 7 purchases. The Commission took some time to realise this: indeed it was Microsoft’s rivals that pointed it out. The screen reappeared some 13 months later, after some 15m copies of Windows software had been sold.

For this lapse, the Commission has just fined Microsoft €561m. Commission Vice President in charge of competition policy, Joaquín Almunia, said:

For this lapse, the Commission has just fined Microsoft €561m. Commission Vice President in charge of competition policy, Joaquín Almunia, said:

In 2009, we closed our investigation about a suspected abuse of dominant position by Microsoft due to the tying of Internet Explorer to Windows by accepting commitments offered by the company. Legally binding commitments reached in antitrust decisions play a very important role in our enforcement policy because they allow for rapid solutions to competition problems. Of course, such decisions require strict compliance. A failure to comply is a very serious infringement that must be sanctioned accordingly.

This may seem unduly harsh, given that Internet Explorer’s share of the browser market has fallen dramatically. In 2009, it had around 50% of the European market, with its main rival at the time, Mozilla’s Firefox, having just under 40%. By 2013, Internet Explorer’s share has fallen to around 24% and Firefox’s to around 29%. Google’s Chrome, which was just starting up in 2009, has seen its share of the European market rise to around 35% and is now the market leader. Partly this is due to the rise in tablets and smartphones, a large proportion of which use Google’s Android operating system and the Chrome browser.

This may seem unduly harsh, given that Internet Explorer’s share of the browser market has fallen dramatically. In 2009, it had around 50% of the European market, with its main rival at the time, Mozilla’s Firefox, having just under 40%. By 2013, Internet Explorer’s share has fallen to around 24% and Firefox’s to around 29%. Google’s Chrome, which was just starting up in 2009, has seen its share of the European market rise to around 35% and is now the market leader. Partly this is due to the rise in tablets and smartphones, a large proportion of which use Google’s Android operating system and the Chrome browser.

Not surprisingly, the European Commission is investigating Google to see whether it is abusing a dominant position. Is Google’s case, it’s not just about its share of the browser market, it’s more about its share of the search market, which in the EU is around 90% (compared with around 65% in the USA). As The Economist article below states:

The Commissioner believes that Google may be favouring its own specialised services (eg, for flights or hotels) at rivals’ expense; that its deals with publishers may unfairly exclude competitors; and that it prevents advertisers from taking their data elsewhere.

Joaquín Almunia asked Google to respond to these concerns by January 31. Google delivered its suggestions on the deadline, but we await to hear precisely what it said and how the Commission will respond. It is understood that Google’s proposal is for clearly labelling its own products on its search engine.

Articles

Microsoft Fined $732 Million By EU Over Browser eWeek, Michelle Maisto (6/3/13)

Microsoft faces hefty EU fine The Guardian (6/3/13)

Sin of omission The Economist (9/3/13)

Microsoft fined by European Commission over web browser BBC News (6/3/13)

EU commissioner Joaquin Almunia announces Microsoft fine BBC News (6/3/13)

Microsoft’s European Fine Comes in an Era of Browser Diversity Forbes, J.P. Gownder (6/3/13)

Life after Firefox: Can Mozilla regain its mojo? BBC News, Dave Lee (11/4/12)

Google responds to European commission’s antitrust chief The Guardian, Charles Arthur (31/1/13)

Google May Clinch EU Settlement After ‘Summer,’ Almunia Says Bloomberg Businessweek, Stephanie Bodoni and Aoife White (22/2/13)

European Commission Press Release

Antitrust: Commission fines Microsoft for non-compliance with browser choice commitments Europa (6/3/13)

Questions

- Why did Microsoft’s share of the browser market continue to decline between May 2011 and June 2012?

- Why would it matter if Microsoft had market power in the browser market, given that it’s free for anyone to download a browser?

- In what ways might Google be abusing a dominant position in the market?

- Can Mozilla regain its mojo?

- According to the second Guardian article, the Microsoft-backed lobby group Icomp said “To be seen as a success, any settlement must … include specific measures to restore competition and allow other parties to compete effectively on a level playing field with Google in the key markets of search and search advertising.” Give examples of such measures and assess how successful they might be.

- Would “clearly labelling its own products on its search engine” be enough to ensure adequate competition?

Few people have £18bn worth of funds to spend. But someone that does is Warren Buffett and a Brazilian firm, who look set to purchase Heinz for this sum. Heinz, known for things like baked beans and ketchup already has an exceptionally strong brand and is cash rich – these are two ingredients which Warren Buffett likes and have undoubtedly played their part in securing what looks to be a tasty deal.

Few people have £18bn worth of funds to spend. But someone that does is Warren Buffett and a Brazilian firm, who look set to purchase Heinz for this sum. Heinz, known for things like baked beans and ketchup already has an exceptionally strong brand and is cash rich – these are two ingredients which Warren Buffett likes and have undoubtedly played their part in securing what looks to be a tasty deal.

The company’s Board has already approved the deal, but shareholders still need to have their say and have been offered $72.50 per share. 650 million bottles of Heinz ketchup are sold every year and its baked beans, at the least in the UK, are second to none. Products like this have given Heinz its global brand name and have provided the opportunity to shareholders to make significant gains. Its Chairman said:

The Heinz brand is one of the most respected brands in the global food industry and this historic transaction provides tremendous value to Heinz shareolders.

This statement was certainly reciprocated by Warren Buffett when he spoke to CNBC, saying:

It is our kind of company … I’ve sampled it many times … Anytime we see a deal is attractive and it’s our kind of business and we’ve got the money, I’m ready to do.

The deal therefore looks to be profitable to both sides, but is there more to it? An investigation has already been launched by the Securities and Exchange Commission as to whether information about this purchase was leaked early and was used to make money. Insider trading occurs when someone is given information early about a merger such as the one described above. They then use this information, before it is made public, to buy up a company’s stock. It is incredibly difficult to prosecute and huge amounts of money can be made by hedge funds, amongst others. This is certainly one aspect of the deal to keep your eye on.

The deal therefore looks to be profitable to both sides, but is there more to it? An investigation has already been launched by the Securities and Exchange Commission as to whether information about this purchase was leaked early and was used to make money. Insider trading occurs when someone is given information early about a merger such as the one described above. They then use this information, before it is made public, to buy up a company’s stock. It is incredibly difficult to prosecute and huge amounts of money can be made by hedge funds, amongst others. This is certainly one aspect of the deal to keep your eye on.

So, what does the future hold for Warren Buffett and Heinz? Buffett likes to extract extra value from companies he purchases and has in the past split up his businesses to create separate trading companies. However, given his taste for ketchup and his appreciation for strong global brands, it’s unlikely that we’ll see a change to the recipe of any of the well-known products. The following articles consider the takeover and the case of insider trading.

Will Buffet ‘squeeze value’ from Heinz BBC News (15/2/13)

Heinz-Buffett deal: will anyone spill the beans on insider trading? The Guardian, Heidi Moore (15/2/13)

Heinz bought by Warren Buffett’s Berkshire Hathaway for $28bn BBC News (14/2/13)

Traders sued over Heinz share bets Independent, Nikhil Kumar (16/2/13)

Heinz deal brings it back to its roots Financial Times, Alan Rappeport, Dan McCrum and Anoushka Sakoui (14/2/13)

Beanz means Buffet: Heinz purchased in $28bn takeover The Guardian, Dominic Rush (14/2/13)

US SEC sues over Heinz option trading before buyout Reuters (15/2/13)

Warren Buffet and Brazil’s ‘Sage’ Jorge Leman strike £18bn Heinz deal The Telegraph, Richard Blackden (15/2/13)

Questions

- What type of take-over would you class this as?

- Consider the Boston matrix – in which category would you place Heinz when you think about its market share and market growth?

- Why is a company that has a global brand and that is cash rich so tempting?

- Given your answer to question 3, why have other investors not taken an interest in purchasing Heinz?

- If you were a shareholder in Heinz, what factors would you consider when deciding whether or not to vote for the takeover?

- What growth strategy has Heinz used to establish its current position in the global market place?

- What is insider trading? Explain how early information can be used to make money in the case of Heinz.

- Explain how the share price of $72.50 is set. How does the market have a role?

The technology sector is highly complex and is led by Apple. However, as the tablet market is continuing to grow, it is becoming increasingly competitive with other firms such as Samsung gaining market share. Although both firms sell many products, it is the growing tablet market which is one of the keys to their continued growth.

The technology sector is highly complex and is led by Apple. However, as the tablet market is continuing to grow, it is becoming increasingly competitive with other firms such as Samsung gaining market share. Although both firms sell many products, it is the growing tablet market which is one of the keys to their continued growth.

Tablet PCs have seen a growth in the final quarter of 2012 to a high of 52.5 million units, according to IDC. Although Apple, leading the market, has seen a growth in its sales, its market share has declined to 43.6%. Over the same period, Samsung has increased its market share from 7.3% to 15.1%. While it is still a huge margin behind Apple in the tablet PC market, Samsung’s increase in sales from 2.2 million to 7.9 million is impressive and if such a trend were to continue, it would certainly cause Apple to take note.

It’s not just these two firms trying to take advantage of this growing industry. Microsoft has recently launched a new tablet PC and although its reception was less than spectacular, it is expected that Microsoft will become a key competitor in the long run. There are many factors driving the growth in this market and the war over market share is surely only just beginning. The chart shows the 75.3% growth in sales in just one year. (Click here for a PowerPoint of the chart.)

It’s not just these two firms trying to take advantage of this growing industry. Microsoft has recently launched a new tablet PC and although its reception was less than spectacular, it is expected that Microsoft will become a key competitor in the long run. There are many factors driving the growth in this market and the war over market share is surely only just beginning. The chart shows the 75.3% growth in sales in just one year. (Click here for a PowerPoint of the chart.)

A Research Director at IDC said:

We expected a very strong fourth quarter, and the market didn’t disappoint…New product launches from the category’s top vendors, as well as new entrant Microsoft, led to a surge in consumer interest and very robust shipments totals during the holiday season’

Apple has been so dominant in this sector that other companies until recently have had little success in gaining market share. However, with companies such as Samsung and ASUS now making in-roads, competition is likely to become fierce. There are already concerns that Apple’s best days are behind it and its share price reflects this. People are now less willing to pay a premium price for an Apple product, as the innovations of its competitors have now caught up with those of the leading brand name. The following articles consider this growing market.

Samsung gain tablet market share as Apple lead narrows BBC News (1/2/13)

Apple snatches US lead from Samsung Financial Times, Tim Bradshaw (1/2/13)

Apple revenues miss expectations despite high sales figures BBC News (24/1/13)

Samsung eats into Apple sales in the tablet market Mirror, Ruki Sayid (1/2/13)

MacWorld’s Apple celebration opens amid fears of tech giant’s decline Guardian, Rory Carroll (31/1/13)

Samsung’s tablet sales soar as Apple’s grip on market loosens Daily News and Analysis, Richard Blagden (2/2/13)

Samsung takes a nibble out of Apple’s tablet lead InfoWorld, Ted Samson(31/1/13)

Tablet Sales up 75% as Samsung and Asus Gain on Apple Interational Business Times, Edward Smith (31/1/13)

Questions

- Which factors are behind this exceptional growth in the tablet PC market?

- Using the Boston matrix, where do you think tablet PCs fit in terms of market size and market growth?

- Where would you place this market in terms of the product life cycle?

- What does the product life cycle say about the degree of competition, the impact on pricing on profits etc. in the phase that you placed the tablet PC market in your answer to question 3?

- Why have Apple’s shares fallen recently? Do you think this will be the new trend?

- Microsoft’s new tablet didn’t attract huge sales. What explanation was given for this? Use a diagram to help answer this question.

- Tablet PCs are relatively expensive, yet sales of them have increased significantly over the past few years. What explanation is there for this, given that we have been (and still are) in tough financial times?

On 5 and 6 April, there was a conference on conscious capitalism in San Francisco. In January, a new book, Conscious Capitalism: Liberating the Heroic Spirit of Business, by John Mackey and Rajendra Sisodia, was published. Many in the business world are enthusiastic about this seemingly new approach to business, which focuses on broader social, environmental and ethical goals, rather than simple profit maximisation.

On 5 and 6 April, there was a conference on conscious capitalism in San Francisco. In January, a new book, Conscious Capitalism: Liberating the Heroic Spirit of Business, by John Mackey and Rajendra Sisodia, was published. Many in the business world are enthusiastic about this seemingly new approach to business, which focuses on broader social, environmental and ethical goals, rather than simple profit maximisation. So how realistic is this vision of caring capitalism? There may be a few inspiring businesspeople, truly committed to improving the interests of the various stakeholders of their business and society more generally, but could it become a model for business in general? And if so, does this require education, monitoring and regulation? Or can a libertarian approach to business generate an environment where conscious and caring capitalists flourish and succeed better than those with a more narrow focus on profit?

So how realistic is this vision of caring capitalism? There may be a few inspiring businesspeople, truly committed to improving the interests of the various stakeholders of their business and society more generally, but could it become a model for business in general? And if so, does this require education, monitoring and regulation? Or can a libertarian approach to business generate an environment where conscious and caring capitalists flourish and succeed better than those with a more narrow focus on profit?