In an interview with Joe Rogan for his podcast, The Joe Rogan Experience, just before the US election, Donald Trump stated that, “To me, the most beautiful word – and I’ve said this for the last couple of weeks – in the dictionary today and any is the word ‘tariff’. It’s more beautiful than love; it’s more beautiful than anything. It’s the most beautiful word. This country can become rich with the use, the proper use of tariffs.”

In an interview with Joe Rogan for his podcast, The Joe Rogan Experience, just before the US election, Donald Trump stated that, “To me, the most beautiful word – and I’ve said this for the last couple of weeks – in the dictionary today and any is the word ‘tariff’. It’s more beautiful than love; it’s more beautiful than anything. It’s the most beautiful word. This country can become rich with the use, the proper use of tariffs.”

President-elect Trump has stated that he will impose tariffs on imports of 10% or 20%, with 60% and 100% tariffs on imports from China and Mexico, respectively. This protection for US industries, combined with lighter regulation, will, he claims, provide a stimulus to the economy and help create jobs. The revenues will also help to reduce America’s budget deficit.

But it is not that straightforward.

Problems with tariffs for the USA

Imposing tariffs is likely to reduce international trade. But international trade brings net benefits, which are distributed between the participants according to the terms of trade. This is the law of comparative advantage.

Imposing tariffs is likely to reduce international trade. But international trade brings net benefits, which are distributed between the participants according to the terms of trade. This is the law of comparative advantage.

In the simple two-country case, the law states that, provided the opportunity costs of producing various goods differ between the two countries, both of them can gain from mutual trade if they specialise in producing (and exporting) those goods that have relatively low opportunity costs compared with the other country. The total production and consumption of the two countries will be higher.

So if the USA has a comparative advantage in various manufactured products and a trading partner has a comparative advantage in tropical food products, such as coffee or bananas, both can gain by specialisation and trade.

If tariffs are imposed and trade is thereby reduced between the USA and its trading partners, there will be a net loss, as production will switch from lower-cost production to higher-cost production. The higher costs of less efficient production in the USA will lead to higher prices for those goods than if they were imported.

At the same time, goods that are still imported will be more expensive as the price will include the tariff. Some of this may be borne by the importer, meaning that only part of the tariff is passed on to the consumer. The incidence of the tariff between consumer and importer will depend on price elasticities of demand and supply. Nevertheless, imports will still be more expensive, allowing the domestically-produced substitutes to rise in price too, albeit probably by not so much. According to work by Kimberly Clausing and Mary E Lovely for the Peterson Institute (see link in Articles below), Trump’s proposals to raise tariffs would cost the typical American household over $2600 a year.

At the same time, goods that are still imported will be more expensive as the price will include the tariff. Some of this may be borne by the importer, meaning that only part of the tariff is passed on to the consumer. The incidence of the tariff between consumer and importer will depend on price elasticities of demand and supply. Nevertheless, imports will still be more expensive, allowing the domestically-produced substitutes to rise in price too, albeit probably by not so much. According to work by Kimberly Clausing and Mary E Lovely for the Peterson Institute (see link in Articles below), Trump’s proposals to raise tariffs would cost the typical American household over $2600 a year.

The net effect will be a rise in inflation – at least temporarily. Yet one of Donald Trump’s pledges is to reduce inflation. Higher inflation will, in turn, encourage the Fed to raise interest rates, which will dampen investment and economic growth.

Donald Trump tends to behave transactionally rather than ideologically. He is probably hoping that a rapid introduction of tariffs will then give the USA a strong bargaining position with foreign countries to trade more fairly. He is also hoping that protecting US industries by the use of tariffs, especially when coupled with deregulation, will encourage greater investment and thereby faster growth.

Much will depend on how other countries respond. If they respond by raising tariffs on US exports, any gain to industries from protection from imports will be offset by a loss to exporters.

A trade war, with higher tariffs, will lead to a net loss in global GDP. It is a negative sum game. In such a ‘game’, it is possible for one ‘player’ (country) to gain, but the loss to the other players (countries) will be greater than that gain.

Donald Trump is hoping that by ‘winning’ such a game, the USA could still come out better off. But the gain from higher investment, output and employment in the protected industries would have to outweigh the losses to exporting industries and from higher import prices.

Donald Trump is hoping that by ‘winning’ such a game, the USA could still come out better off. But the gain from higher investment, output and employment in the protected industries would have to outweigh the losses to exporting industries and from higher import prices.

The first Trump administration (2017–21), as part of its ‘America First’ programme, imposed large-scale tariffs on Chinese imports and on steel and aluminium from across the world. There was wide-scale retaliation by other countries with tariffs imposed on a range of US exports. There was a net loss to world income, including US GDP.

Problems with US tariffs for the rest of the world

The imposition of tariffs by the USA will have considerable effects on other countries. The higher the tariffs and the more that countries rely on exports to the USA, the bigger will the effect be. China and Mexico are likely to be the biggest losers as they face the highest tariffs and the USA is a major customer. In 2023, US imports from China were worth $427bn, while US exports to China were worth just $148bn – only 34.6% of the value of imports. The percentage is estimated to be even lower for 2024 at around 32%. In 2023, China’s exports to the USA accounted for 12.6% of its total exports; Mexico’s exports to the USA accounted for 82.7% of its total exports.

It is possible that higher tariffs could be extended beyond China to other Asian countries, such as Vietnam, South Korea, Taiwan, India and Indonesia. These countries typically run trade surpluses with the USA. Also, many of the products from these countries include Chinese components.

As far as the UK is concerned, the proposed tariffs would cause significant falls in trade. According to research by Nicolò Tamberi at the University of Sussex (see link below in Articles):

The UK’s exports to the world could fall by £22 billion (–2.6%) and imports by £1.4 (–0.16%), with significant variations across sectors. Some sectors, like fishing and petroleum, are particularly hard-hit due to their high sensitivity to tariff changes, while others, such as textiles, benefit from trade diversion as the US shifts demand away from China.

Other badly affected sectors would include mining, pharmaceuticals, finance and insurance, and business services. The overall effect, according to the research, would be to reduce UK output by just under 1%.

Countries are likely to respond to US tariffs by imposing their own tariffs on US imports. World Trade Organization rules permit the use of retaliatory tariffs equivalent to those imposed by the USA. The more aggressive the resulting trade war, the bigger would be the fall in world trade and GDP.

The EU is planning to negotiate with Trump to avoid a trade war, but officials are preparing the details of retaliatory measures should the future Trump administration impose the threatened tariffs. The EU response is likely to be strong.

Articles

The Most Beautiful Word In The Dictionary: Tariffs

The Most Beautiful Word In The Dictionary: TariffsYouTube, Joe Rogan and Donald Trump

- The exact thing that helped Trump win could become a big problem for his presidency

CNN, Matt Egan (7/11/24)

- Trump’s New Trade War With China Is Coming

Newsweek, Micah McCartney (9/11/24)

- Trump tariff threat looms large on several Asian countries – not just China – says Goldman Sachs

CNBC, Lee Ying Shan (11/11/24)

- Trump’s bigger tariff proposals would cost the typical American household over $2,600 a year

Peterson Institute for International Economics, Kimberly Clausing and Mary E Lovely (21/8/24)

- More tariffs, less red tape: what Trump will mean for key global industries

The Guardian, Jasper Jolly, Dan Milmo, Jillian Ambrose and Jack Simpson (7/11/24)

- Trump tariffs would halve UK growth and push up prices, says thinktank

The Guardian, Larry Elliott (6/11/24)

- China is trying to fix its economy – Trump could derail those plans

BBC News, João da Silva (8/11/24)

- Trump tariffs could cost UK £22bn of exports

BBC News, Faisal Islam & Tom Espiner (8/11/24)

- Trump to target EU over UK in trade war as he wants to see ‘successful Brexit’, former staffer claims

Independent, Millie Cooke (11/11/24)

- EU’s trade war nightmare gets real as Trump triumphs

Politico, Camille Gijs (6/11/24)

- Will Trump impose his tariffs? They could reduce the UK’s exports by £22 billion.

Centre for Inclusive Trade Policy, University of Sussex, Nicolò Tamberi (8/11/24)

- Three possible futures for the global economy if Trump brings in new trade tariffs

The Conversation, Agelos Delis and Sami Bensassi (17/12/24)

Questions

- Explain why, according to the law of comparative advantage, all countries can gain from trade.

- In what ways may the imposition of tariffs benefit particular sections of an economy?

- Is it in countries’ interests to retaliate if the USA imposes tariffs on their exports to the USA?

- Why is a trade war a ‘negative sum game’?

- Should the UK align with the EU in resisting President-elect Trump’s trade policy or should it seek independently to make a free-trade deal with the USA? is it possible to do both?

- What should China do in response to US threats to impose tariffs of 60% or more on Chinese imports to the USA?

An agreement in principle was reached on September 30 between the USA, Canada and Mexico over a new trade deal to replace the North American Free Trade Agreement (NAFTA). President Trump had described NAFTA as ‘the worst trade deal maybe ever signed anywhere, but certainly ever signed in this country.’ The new deal, named the United States-Mexico-Canada Agreement, or USMCA, is the result of 14 months of negotiations, which have often been fractious. A provisional bilateral agreement was made between the USA and Mexico in August. At the same time, President Trump threatened a trade war with Canada if it did not reach a trade agreement with the USA (and Mexico). The new USMCA must be ratified by lawmakers in all three countries before it can come into force. This could take a few months.

An agreement in principle was reached on September 30 between the USA, Canada and Mexico over a new trade deal to replace the North American Free Trade Agreement (NAFTA). President Trump had described NAFTA as ‘the worst trade deal maybe ever signed anywhere, but certainly ever signed in this country.’ The new deal, named the United States-Mexico-Canada Agreement, or USMCA, is the result of 14 months of negotiations, which have often been fractious. A provisional bilateral agreement was made between the USA and Mexico in August. At the same time, President Trump threatened a trade war with Canada if it did not reach a trade agreement with the USA (and Mexico). The new USMCA must be ratified by lawmakers in all three countries before it can come into force. This could take a few months.

So is USMCA a radical departure from NAFTA? Does the USA stand to gain substantially, as President Trump claims? In fact, USMCA is little different from NAFTA. It could best be described as a relatively modest reworking of NAFTA. So what are the changes?

The first change affects the car industry. From 2020, 75% of the components of any vehicle crossing between the USA and Canada or Mexico must be made within one or more of the three countries to qualify for tariff-free treatment. The aim is to boost production within the region. But the main change here is merely an increase in the proportion from the current 62.5%.

The first change affects the car industry. From 2020, 75% of the components of any vehicle crossing between the USA and Canada or Mexico must be made within one or more of the three countries to qualify for tariff-free treatment. The aim is to boost production within the region. But the main change here is merely an increase in the proportion from the current 62.5%.

A more significant change affecting the car industry concerns wages. Between 40% and 45% of a vehicle’s components must be made by workers earning at least US$16 per hour. This is some three times more than the average wage currently earned by Mexican car workers. Although it will benefit such workers, it will reduce Mexico’s competitive advantage and could hence lead to some diversion of production away from Mexico. Also, it could push up the price of cars.

The agreement has also strengthened various standards inadequately covered in NAFTA. According to The Conversation article:

The new agreement includes stronger protections for patents and trademarks in areas such as biotech, financial services and domain names – all of which have advanced considerably over the past quarter century. It also contains new provisions governing the expansion of digital trade and investment in innovative products and services.

Separately, negotiators agreed to update labor and environmental standards, which were not central to the 1994 accord and are now typical in modern trade agreements. Examples include enforcing a minimum wage for autoworkers, stricter environmental standards for Mexican trucks and lots of new rules on fishing to protect marine life.

Another area where the USMCA agreement has made changes concerns trade in dairy products. This particularly affects Canada, which has agreed to allow more US dairy products tariff-free into Canada (see the CNN article at the end of the list of articles below). New higher quotas will give US dairy farmers access to 3.6% of Canada’s dairy market. They will still pay tariffs on dairy exports to Canada that exceed the quotas, ranging from 200% to 300%.

Another area where the USMCA agreement has made changes concerns trade in dairy products. This particularly affects Canada, which has agreed to allow more US dairy products tariff-free into Canada (see the CNN article at the end of the list of articles below). New higher quotas will give US dairy farmers access to 3.6% of Canada’s dairy market. They will still pay tariffs on dairy exports to Canada that exceed the quotas, ranging from 200% to 300%.

The other significant change for consumers in Mexico and Canada is a rise in the value of duty-free imports they can bring in from the USA, including online transactions. As the first BBC article listed below states:

The new agreement raises duty-free shopping limits to $100 to enter Mexico and C$150 ($115) to enter Canada without facing import duties – well above the $50 previously allowed in Mexico and C$20 permitted by Canada. That’s good news for online shoppers in Mexico and Canada – as well as shipping firms and e-commerce companies, especially giants like Amazon.

Despite these changes, USMCA is very similar to NAFTA. It is still a preferential trade deal between the three countries, but certainly not a completely free trade deal – but nor was NAFTA.

And for the time being, US tariffs on Mexican and Canadian steel and aluminium imports remain in place. Perhaps, with the conclusion of the USMCA agreement, the Trump administration will now, as promised, consider lifting these tariffs.

Video

Articles

- USMCA, the new trade deal between the US, Canada, and Mexico, explained

Vox, Jen Kirby (2/10/18)

- USMCA: What Donald Trump’s Nafta replacement trade deal means and how it will work

Independent, Mythili Sampathkumar (2/10/18)

- USMCA trade deal: Who gets what from ‘new Nafta’?

BBC News, Jessica Murphy & Natalie Sherman (1/10/18)

- Can Trump really cut the US trade deficit?

BBC News, Andrew Walker (2/10/18)

- How is ‘new NAFTA’ different? A trade expert explains

The Conversation, Amanda M. Countryman (2/10/18)

- Was NAFTA ‘worst trade deal ever’? Few agree

PolitiFact, Jon Greenberg (29/9/18)

- NAFTA out, USMCA in: What’s in the Canada, Mexico, US trade deal?

Aljazeera, Heather Gies (2/10/18)

- Mexico boosted by US-Canada agreement on revamped Nafta deal

Financial Times, Jude Webber (3/10/18)

- Nafta Is Dead. Long Live Nafta.

Bloomberg (2/10/18)

- Trump Clears Deck for China Trade War With New Nafta Deal

Bloomberg, Rich Miller, Andrew Mayeda and Jenny Leonard (2/10/18)

- Fact check: Is Trump right that the new trade deal is “biggest” ever?

CBS News (2/10/18)

- Commentary: What Trump’s new trade pact signals about China

Reuters, Andres Martinez (4/10/18)

- Canada opened its dairy market. But by how much?

CNN, Katie Lobosco (2/10/18)

Questions

- What have been the chief gains and losses for the USA from USMCA?

- What have been the chief gains and losses for Mexico from USMCA?

- What have been the chief gains and losses for Canada from USMCA?

- What are the economic gains from free trade?

- Why might a group of countries prefer a preferential trade deal with various restrictions on trade rather than a completely free trade deal between them?

- Distinguish between trade creation and trade diversion.

- In what areas, if any, might USMCA result in trade diversion?

- If the imposition of tariffs results in a net loss from a decline in trade, why might it be in the interests of a country such as the USA to impose tariffs?

So here we are, summer is over (or almost over if you’re an optimist) and we are sitting in front of our screens reminiscing about hot sunny days (at least I do)! There is no doubt, however: a lot happened in the world of politics and economics in the past three months. The escalation of the US-China trade war, the run on the Turkish lira, the (successful?) conclusion of the Greek bailout – these are all examples of major economic developments that took place during the summer months, and which we will be sure to discuss in some detail in future blogs. Today, however, I will introduce a topic that I am very interested in as a researcher: the liberalisation of energy markets in developing countries and, in particular, Mexico.

So here we are, summer is over (or almost over if you’re an optimist) and we are sitting in front of our screens reminiscing about hot sunny days (at least I do)! There is no doubt, however: a lot happened in the world of politics and economics in the past three months. The escalation of the US-China trade war, the run on the Turkish lira, the (successful?) conclusion of the Greek bailout – these are all examples of major economic developments that took place during the summer months, and which we will be sure to discuss in some detail in future blogs. Today, however, I will introduce a topic that I am very interested in as a researcher: the liberalisation of energy markets in developing countries and, in particular, Mexico.

Why Mexico? Well, because it is a great example of a large developing economy that has been attempting to liberalise its energy market and reverse price setting and monopolistic practices that go back several decades. Until very recently, the price of petrol in Mexico was set and controlled by Pemex, a state monopolist. This put Pemex under pressure since, as a sole operator, it was responsible for balancing growing demand and costs, even to the detriment of its own finances.

The petrol (or ‘gasoline’) price liberalisation started in May 2017 and took place in stages – starting in the North part of Mexico and ending in November of the same year in the central and southern regions of the country. The main objective was to address the notable decrease in domestic oil production that put at risk the ability of the country to meet demand; as well as Mexico’s increasing dependency on foreign markets affected by the surge of the international oil price. The government has spent the past five years trying to create a stronger regulatory framework, while easing the financial burden on the state and halting the decline in oil reserves and production. Unsurprisingly, opening up a monopolistic market turns out to be a complex and bumpy process.

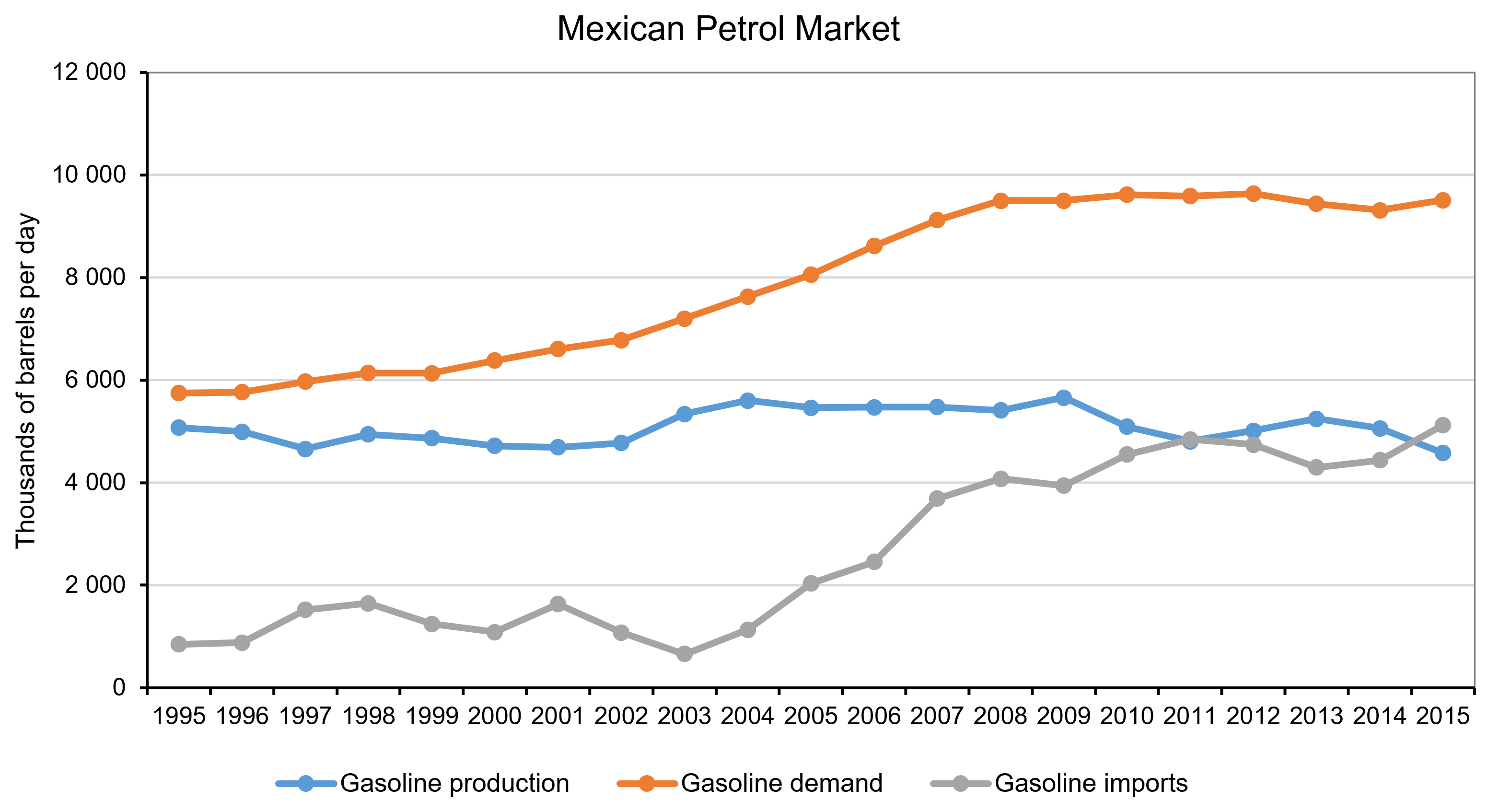

Source: Author’s calculations using data from the Energy Information Bank, Ministry of Energy, Mexico

Source: Author’s calculations using data from the Energy Information Bank, Ministry of Energy, Mexico

Despite all the reforms, retail petrol prices have kept rising. Although part of this price rise is demand-driven, an increasing number of researchers highlight the significance of the distribution of oil-related infrastructure in determining price outcomes at the federal and regional (state) level. Saturation and scarcity of both distribution and storage infrastructure are probably the two most significant impediments to opening the sector up to competition (Mexico Institute, 2018). You see, the original design of these networks and the deployment of the infrastructure was not aimed at maximising efficiency of distribution – the price was set by the monopolist and, in a way that was compliant with government policy (Mexico Institute, 2018). Economic efficiency was not always part of this equation. As a result, consumers located in better-deployed areas were subsidising the inherent logistics costs of less ‘well endowed’ regions by facing an artificially higher price than they would have in a competitive market.

But what about now? Do such differences in the allocation of infrastructure between regions lead to location-related differences in the price of petrol? If so, by how much? And, what policies should the government pursue to address such imbalances? These are all questions that I explore in one of my recent working papers titled ‘Widening the Gap: Lessons from the aftermath of the energy market reform in Mexico’ (with Hugo Vallarta) and I will be sharing some of the answers with you in a future blog.

Articles

Data

Questions

- Are state-owned monopolies effective in delivering successful market outcomes? Why yes, why no?

- In the case of Mexico, are you surprised about the complexities that were involved with opening up markets to competition? Explain why.

- Use Google to identify countries in which energy markets are controlled by state-owned monopolies.