On April 2nd, Donald Trump announced sweeping new ‘reciprocal’ tariffs. These would be in addition to 25% tariffs on imports of cars, steel and aluminium already announced and any other tariffs in place on individual countries, such as China. The new tariffs would apply to US imports from every country, except for Canada and Mexico where tariffs had already been imposed.

On April 2nd, Donald Trump announced sweeping new ‘reciprocal’ tariffs. These would be in addition to 25% tariffs on imports of cars, steel and aluminium already announced and any other tariffs in place on individual countries, such as China. The new tariffs would apply to US imports from every country, except for Canada and Mexico where tariffs had already been imposed.

The new tariffs would depend on the size of the country’s trade in goods surplus with the USA (i.e. the USA’s trade in goods deficit with that country). The bigger the percentage surplus, the bigger the tariff. But, no matter how small a country’s surplus or even if it runs a deficit (i.e. imports more goods from the USA than it sells), it would still face a minimum 10% ‘baseline’ tariff.

President Trump stated that these tariffs are to counter what he claims as unfair trade practices inflicted on the USA. People had been expecting that these tariffs would reflect the tariffs applied by other countries on US goods and possibly also non-tariff barriers, such as the ban on chlorine-washed chicken or hormone-injected beef in the EU and UK. But, by basing them on the size of a country’s trade surplus, this meant imposing them on many countries with which the USA has a free-trade deal with no tariffs at all.

The table gives some examples of the new tariff rates. The largest rates would apply to China and south-east Asian countries, which supply low-priced products, such as clothing, footwear and electronics to the US market. In China’s case, it would a reciprocal tariff rate of 34% plus the previously imposed tariff rate of 20%, giving a massive 54%.

The table gives some examples of the new tariff rates. The largest rates would apply to China and south-east Asian countries, which supply low-priced products, such as clothing, footwear and electronics to the US market. In China’s case, it would a reciprocal tariff rate of 34% plus the previously imposed tariff rate of 20%, giving a massive 54%.

What is more, the ‘de minimis’ exemption will be scrapped for packages sent by private couriers. This had exempted goods of $800 or less sent direct to consumers from China and other countries from companies such as Temu and Alibaba. It is also intended to cut back on packages of synthetic opioids sent from these countries.

Since ‘liberation day’, President Trump has made several changes to these tariff rates. On 9 April he ‘paused’ the implementation of the tariffs above the 10% rate pending trade discussions with individual countries. However, in the case of China, there have been tit-for-tat tariff increases, so that by the end of April, the US tariff rate on Chinese imports was a massive 145% and the Chinese rate on US imports was 125%. The two countries seemed locked in a high-stakes game of chicken.

The US formula for reciprocal tariffs

As we have seen, the proposed (and then paused) reciprocal tariffs do not reflect countries’ tariff rates on the USA. Instead, rates for countries running a trade in goods surplus with the USA (a US trade deficit with these countries) are designed to reflect the size of that surplus as a percentage of their total imports from the USA. The White House has published the following formula.

where:

When the two elasticities are multiplied together this gives 1 and so can be ignored. As there was no previous ‘reciprocal’ tariff, the rise in the reciprocal tariff rate is the actual reciprocal tariff rate. The formula for the reciprocal tariff rate thus becomes the percentage trade surplus of that country with the USA: (exports – imports) / imports, expressed as a percentage. This is then rounded up to the nearest whole number.

President Trump also stated that countries would be given a discount to show US goodwill. This involves halving the rate from the above formula and then rounding up to the nearest whole number.

Take the case of China. China’s exports of goods to the USA in 2024 were $439bn, while its imports of goods from the USA were $144bn, giving China a trade surplus with the USA of $295bn. Expressing this as a percentage of exports gives ($295/$439 × 100)/2 = 33.6%, rounded up to 34%. For the EU, the formula gives ($227bn/$584bn × 100)/2 = 19.4%, rounded up to 20%.

Questioning the value of φ. Even if you accept the formula itself as the basis for imposing tariffs, the value of the second term in the denominator, φ, is likely to be seriously undervalued. The term represents the elasticity of import prices with respect to tariff changes. It shows the proportion of a tariff rise that is passed on to consumers, which is assumed to be just one quarter, with producers bearing the remaining three quarters. In reality, it is highly likely that most of the tariff will get passed on, as it was with the tariffs applied in Donald Trump’s first presidency.

If the value for φ were 1 (i.e. all the tariff passed on to the consumer), the formula would give a ‘reciprocal tariff’ of just one quarter of that with a value of φ of 0.25. The figures in the table above would look very different. If the rates were then still halved, all countries with a tariff below 40% (such as the EU, Japan or India) would instead face just the baseline tariff of 10%. What is more, China’s rate would be reduced from 54% to 30% (the original 20% plus the baseline of 10%). Cambodia’s would be reduced to 13%. Even if the halving discount were no longer applied, the rates would still be only half of those shown in the table (and 37% for China).

Are the tariffs justified?

Even if a correct value of φ were used, a percentage trade surplus is a poor way of measuring the protection used by a country. Many countries running a trade surplus with the USA are low-income countries with low labour costs. They have a comparative advantage in labour-intensive goods. That allows such goods to be purchased at low cost by Americans. Their trade surplus may not be a reflection of protection at all.

Even if a correct value of φ were used, a percentage trade surplus is a poor way of measuring the protection used by a country. Many countries running a trade surplus with the USA are low-income countries with low labour costs. They have a comparative advantage in labour-intensive goods. That allows such goods to be purchased at low cost by Americans. Their trade surplus may not be a reflection of protection at all.

Also, if protection is to be used to reflect the trade imbalance with each country, then why impose a 10% baseline on countries, like the UK, with which the USA has a trade surplus? By the Trump administration’s logic, it ought to be subsidising UK imports or accepting of UK tariffs on imports of US goods.

But President Trump also wants to address the USA’s overall trade deficit. The US balance of trade in goods deficit was $1063bn in 2023 (the latest year for a full set of figures). But the overall balance of payments must balance. There were thus surpluses elsewhere on the balance of payments account (and some other deficits). There was a surplus on the services account of $278bn and on the financial account of $924bn. In other words, inward investment to the USA (both direct and portfolio) and the acquisition of dollars by other countries as a reserve asset were very large and helped to drive up the exchange rate. This made US goods less competitive and imports relatively cheaper.

The USA has a large national debt of some $36 trillion of which some $9 trillion is owed to foreign investors (people, institutions or countries). Servicing the debt pushes up US interest rates. This helps to maintain a high exchange rate, thereby making imports cheaper and worsening the trade deficit. The fiscal burden of servicing the debt also crowds out US government expenditure on items such as defence, education, law and order and infrastructure. President Trump hopes that tariffs will bring in additional revenue to help finance the deficit.

Effects on the USA

If the tariffs reduce spending on imports and if other countries do not retaliate, then the US balance of trade should improve. However, a tariff is effectively a tax on imported goods. It is charged to the importing company not to the manufacturer abroad. As we saw in the context of the false value for φ, most of the tariff will be passed on to American consumers. Theoretically the incidence of the tariff is shared between the supplier and the purchaser, but in practice, most of the higher cost to the importer will be passed on to the consumer. As with other taxes, the effect is to transfer money from the consumer to the government, making people poorer but giving the government extra revenue. This revenue will be dollars, not foreign currency.

As some of the biggest price rises will be for cheap manufactured products, such as imports from China, and various staple foodstuffs, the effects could be felt disproportionately by the poor. Higher import prices will allow domestic producers competing with these imports to raise their prices too. The tariffs are thus likely to be inflationary. But because the inflation would be the result of higher costs, not higher demand, this could lead to recession as real incomes fell.

American resources will be diverted by the tariffs from sectors in which the USA has a comparative advantage, such as advanced manufactured goods and services, to more basic products. Tariffs on cheap imports will make domestic versions of these products more profitable: even though they are more costly to produce, they will be sold at a higher price.

The tariffs will also directly affect goods produced by US companies. The reason is that many use complex supply chains involving parts produced abroad. Take the case of Apple. Even though it is an American company which designs its products in California, the company sources parts from several Asian countries and has factories in Vietnam, China, India, and Thailand. These components will face tariffs and thus directly affect the price of iPhones, iPads, MacBooks, etc. Similarly affected are other US tech hardware manufacturers, US car manufactures, clothing and footwear producers, such as The Gap and Nike, and home goods producers.

Monetary policy response. How the Fed would respond is not clear. Higher inflation and lower growth, or even a recession, produces what is known as ‘stagflation’: inflation combined with stagnation. Many countries experienced stagflation following the Russian invasion of Ukraine, when higher commodity prices led to soaring inflation and economic slowdown. There was a cost-of-living crisis.

Monetary policy response. How the Fed would respond is not clear. Higher inflation and lower growth, or even a recession, produces what is known as ‘stagflation’: inflation combined with stagnation. Many countries experienced stagflation following the Russian invasion of Ukraine, when higher commodity prices led to soaring inflation and economic slowdown. There was a cost-of-living crisis.

If a central bank has a simple mandate of keeping inflation to a target, higher inflation would be likely to lead to higher interest rates, making recession even more likely. It is the inflation of the two elements of stagflation (inflation and stagnation) that is addressed. The recession is thus likely to be deepened by monetary policy. But as the Fed has a dual mandate of controlling inflation but also of maximising employment, it may choose not to raise interest rates, or even to lower them, to get the optimum balance between these two targets.

If other countries retaliate by themselves raising tariffs on US exports and/or if consumers boycott American goods and services, this will further reduce incomes in the USA. Just two days after ‘liberation day’, China retaliated against America’s 34% additional tariff on Chinese imports by imposing its own 34% tariff on US imports to China.

A trade war will make the world poorer, especially the USA. Investors know this. In the two days following ‘liberation day’, stock markets around the world fell sharply and especially in the USA. The Dow Jones was down 9.3% and the tech-heavy Nasdaq Composite was down 11.4%.

Effects on the rest of the world

The effects of the tariffs on other countries will obviously depend on the tariff rate. The countries facing the largest tariffs are some of the poorest countries which supply the USA with simple labour-intensive products, such as garments, footwear, food and minerals. This could have a severe effect on their economies and cause rapidly increasing poverty and hardship.

If countries retaliate, then this will raise prices of their imports from the USA and hurt their own domestic consumers. This will fuel inflation and push the more seriously affected countries into recession.

If countries retaliate, then this will raise prices of their imports from the USA and hurt their own domestic consumers. This will fuel inflation and push the more seriously affected countries into recession.

If the USA retaliates to this retaliation, thereby further escalating the trade war, the effects could be very serious. The world could be pushed into a deep recession. The benefits of trade, where all countries can gain by specialising in producing goods with low opportunity costs and importing those with high domestic opportunity costs, would be seriously eroded.

What President Trump hopes is that the tariffs will put him in a strong negotiating position. He could offer to reduce or scrap the tariffs on a particular country in exchange for something he wants. An example would be the offer to scrap or reduce the baseline 10% tariff on UK exports and/or the 25% tariff on UK exports of cars, steel and aluminium. This could be in exchange for the UK allowing the importation of US chlorinated chicken or abolishing the digital services tax. This was introduced in 2020 and is a 2% levy on tech firms, including big US firms such as Amazon, Alphabet (Google), Meta and X.

It will be fascinating but worrying to see how the politics of the trade war play out.

Videos

Trump’s tariffs on China, EU and more, at a glance

Trump’s tariffs on China, EU and more, at a glance- Why Trump’s tariffs aren’t really reciprocal

- Trump Tariff calculations are “unreliable”

- Here’s a look at Trump’s math for ‘reciprocal’ tariffs

- The U.S. is the loser in Trump’s tariff war

- “American Empire Is in Decline”: Trump’s Trade War & Tariffs

- ‘Our unity is our strength’ – EU responds to Trump’s tariffs

BBC News, Michelle Fleury and Kayla Epstein (2/4/25)

BBC News, Ben Chu (3/4/25)

New Statesman on YouTube, Andrew Marr & Duncan Weldon (3/4/25)

Reuters on YouTube, Daniel Burns (3/4/25)

MSNBC on YouTube, Steve Rattner (4/4/25)

Democracy Now on YouTube, Richard Wolff (3/4/25)

BBC News, Ursula von der Leyen, President of the European Commission (3/4/25)

Articles

- How were Donald Trump’s tariffs calculated?

- How to read the White House’s tariff formula

- Trump’s ‘idiotic’ and flawed tariff calculations stun economists

- Perilous and chaotic, Trump’s ‘liberation day’ endangers the world’s broken economy – and him

- ‘In economic terms, Trump’s tariffs make no sense at all’

- Trump’s chaos-inducing global tariffs, explained in charts

- Trump’s trade war will hurt everyone – from Cambodian factories to US online shoppers

- Consumers are boycotting US goods around the world. Should Trump be worried?

- How the UK and Europe could respond to Trump’s ‘liberation day’ tariffs

- Trump just massively escalated his trade war. Here’s what he announced

- EU plans countermeasures to new US tariffs, says EU chief

- Wall Street analysts anguish over ‘Liberation Day’

- Reciprocal tariffs: you won’t believe how they came up with the numbers

- Donald Trump baffles economists with tariff formula

- Five key takeaways from Trump’s ‘Liberation Day’ reciprocal tariffs

- These American companies are in big trouble from Trump tariffs

BBC News, Ben Chu and Tom Edgington (3/4/25)

Axios, Felix Salmon and Neil Irwin (3/4/25)

The Guardian, Richard Partington (3/4/25)

The Guardian, Martin Kettle (2/4/25)

The Guardian, Heather Stewart and Richard Partington (4/3/25)

The Guardian, Lauren Aratani, Lucy Swan, Ana Lucía González Paz and Aliya Uteuova (3/4/25)

The Conversation, Lisa Toohey (3/4/25)

The Conversation, Alan Bradshaw and Dannie Kjeldgaard (4/4/25)

The Conversation, Renaud Foucart (3/4/25)

CNN, Elisabeth Buchwald (2/4/25)

Reuters, Philip Blenkinsop and Benoit Van Overstraeten (3/4/25)

FT Alphaville, Robin Wigglesworth (3/4/25)

Financial Times, Alexandra Scaggs (3/4/25)

Financial Times, Peter Foster and Sam Fleming (3/4/25)

Aljazeera (3/4/25)

Axios, Nathan Bomey (3/4/25)

White House publications

- Fact Sheet: President Donald J. Trump Declares National Emergency to Increase our Competitive Edge, Protect our Sovereignty, and Strengthen our National and Economic Security

- Reciprocal Tariff Calculations

The White House (2/3/25)

Executive of the President of the United States (3/4/25)

Questions

- What is the law of comparative advantage? Does this imply that free trade is always the best alternative for countries?

- From a US perspective, what are the arguments for and against the tariffs announced by President Trump on 2 April 2025?

- What response to the tariffs is in the UK’s best interests and why?

- Should the UK align with the EU in responding to the tariffs?

- What is meant by a negative sum game? Explain whether a trade war is a negative sum game. Can a specific ‘player’ gain in a negative sum game?

- What happened to stock markets directly following President Trump’s announcement and what has happened since? Explain you findings.

Donald Trump has threatened to pull out of the World Trade Organization. ‘If they don’t shape up, I would withdraw from the WTO,’ he said. He argues that the USA is being treated very badly by the WTO and that the organisation needs to ‘change its ways’.

Donald Trump has threatened to pull out of the World Trade Organization. ‘If they don’t shape up, I would withdraw from the WTO,’ he said. He argues that the USA is being treated very badly by the WTO and that the organisation needs to ‘change its ways’. Whether or not the USA does withdraw from the WTO, Trump’s threats bring into question the power of the WTO and other countries’ compliance with WTO rules. With the rise in protectionist sentiments around the world, the power of the WTO would seem to be on the wane.

Whether or not the USA does withdraw from the WTO, Trump’s threats bring into question the power of the WTO and other countries’ compliance with WTO rules. With the rise in protectionist sentiments around the world, the power of the WTO would seem to be on the wane. This raises the question of the implication of a ‘no-deal’ Brexit – something that seems more likely as the UK struggles to reach a trade agreement with the EU. Leaving without a deal would mean ‘reverting to WTO rules’. But if these rules are being ignored by powerful countries such as the USA and possibly China, and if the appeals procedure has ground to a halt, this could leave the UK without the safety net of international trade rules. Outside the EU – the world’s most powerful trade bloc – the UK could find itself having to accept poor trade terms with the USA and other large countries.

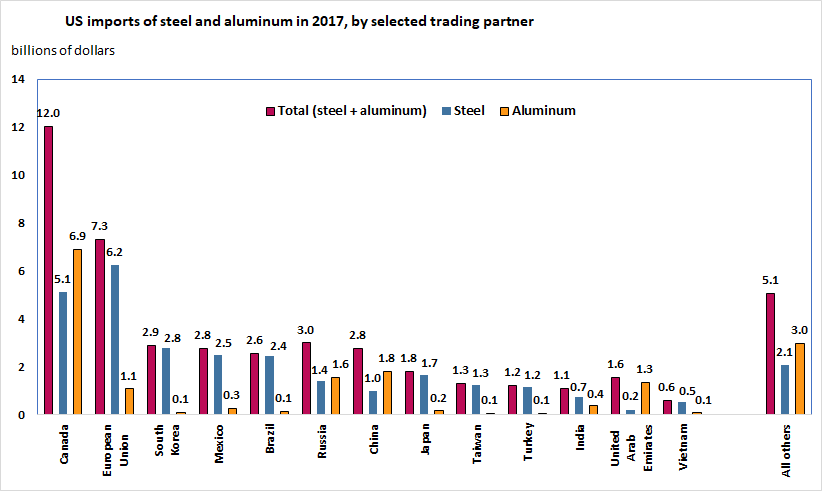

This raises the question of the implication of a ‘no-deal’ Brexit – something that seems more likely as the UK struggles to reach a trade agreement with the EU. Leaving without a deal would mean ‘reverting to WTO rules’. But if these rules are being ignored by powerful countries such as the USA and possibly China, and if the appeals procedure has ground to a halt, this could leave the UK without the safety net of international trade rules. Outside the EU – the world’s most powerful trade bloc – the UK could find itself having to accept poor trade terms with the USA and other large countries. The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.