UK Supermarkets: a prime example of an oligopoly. This industry is highly competitive and over the past decade, but particularly since the onset of the credit crunch, price wars have been a constant feature of this market. You could barely watch a full programme on commercial TV without seeing one of the big supermarkets advertising that their prices were lower than everyone else’s! So, despite oligopoly being towards the ‘least competitive’ end of the market structure spectrum, this is an example of just how competitive the market can actually be.

UK Supermarkets: a prime example of an oligopoly. This industry is highly competitive and over the past decade, but particularly since the onset of the credit crunch, price wars have been a constant feature of this market. You could barely watch a full programme on commercial TV without seeing one of the big supermarkets advertising that their prices were lower than everyone else’s! So, despite oligopoly being towards the ‘least competitive’ end of the market structure spectrum, this is an example of just how competitive the market can actually be.

With household incomes being squeezed, in particular by another oligopolistic industry (energy) and with the ‘middle market’ being pinched by higher-end retailers and budget retailers, the supermarket sector is facing uncertain times. Asda’s sales growth has continued to slow and in response, the giant supermarket chain will be launching a £1 billion price-cutting campaign. Tesco is the market leader, but Sainsbury’s and Asda have been battling over the second spot. One of Asda’s selling points is its low prices. Perhaps not as low as Aldi and Lidl, but this new pricing strategy will aim to bring its prices further below Tesco, Sainsbury’s and Morrisons and close the gap with the two big discount supermarkets. As Andy Clarke, Asda’s Chief Executive, said:

close the gap with the two big discount supermarkets. As Andy Clarke, Asda’s Chief Executive, said:

We regard ourselves as the UK’s leading value retailer and it is against this backdrop that I have today set out our strategic priorities which will improve, extend and expand the business over the next five years.

So, what will be the impact of lower prices? It appears as though Asda is marketing itself towards the budget end of the pricing spectrum, perhaps aiming to become fiercer competitors with Aldi and Lidl and let Tesco and Sainsbury’s do battle with the higher-end retailers, such as Waitrose and Marks and Spencer. Lower prices should cause a substitution effects towards Asda’s products, as many of them will have relatively price elastic demand. If the other supermarkets don’t respond, this should lead to sales growth. However, the key to an oligopoly is interdependence: the actions of one firm will affect all other firms in the market. The implications then, are that Tesco may react to this pricing strategy by engaging in its own price cuts, especially as the Christmas period approaches. The characteristic of interdependence was evident in the aftermath of Asda’s announcement when shares in Tesco and Morrisons both fell, showing how the markets were responding.

Of course, there are many other factors that affect a consumer’s decision as to whether to shop at Asda, Tesco or any other big supermarket. In the area where I live, we have a Tesco and a Morrisons (a few years ago, we had neither!). I don’t shop at Asda, as the nearest branch is over 30 miles away – even if prices were significantly lower, it would be more expensive to get there and back and a lot less convenient. For others, it may be loyalty and not just of the ‘I’ve shopped there all my life’ kind! For some, clubcard vouchers from Tesco may be preferred to Asda’s offerings and thus tiny price differences between the supermarkets may have little effect on a consumer’s decision as to where to shop. Many products at supermarkets are relatively cheap and thus as the proportion of our income that we spend on these goods is pretty low, any change in price doesn’t cause much of an effect on our demand.

Of course, there are many other factors that affect a consumer’s decision as to whether to shop at Asda, Tesco or any other big supermarket. In the area where I live, we have a Tesco and a Morrisons (a few years ago, we had neither!). I don’t shop at Asda, as the nearest branch is over 30 miles away – even if prices were significantly lower, it would be more expensive to get there and back and a lot less convenient. For others, it may be loyalty and not just of the ‘I’ve shopped there all my life’ kind! For some, clubcard vouchers from Tesco may be preferred to Asda’s offerings and thus tiny price differences between the supermarkets may have little effect on a consumer’s decision as to where to shop. Many products at supermarkets are relatively cheap and thus as the proportion of our income that we spend on these goods is pretty low, any change in price doesn’t cause much of an effect on our demand.

It’s not just a pricing strategy where money is being invested by Asda. More investment will be going into their online services and more stores will be created, kin particular in London and the South East where their presence is low, but demand appears to be high. Improving ‘product quality, style and design’ will also be on the agenda, all with the aim of boosting sales growth and securing its position as the second largest retailer in the sector, perhaps with a long term aim of one day overtaking Tesco. The following articles consider the supermarket battleground.

Supermarket battle heats up as Asda announces £1bn price-cutting plan The Telegraph, Graham Ruddick (14/11/13)

Sainsbury’s profits make it second biggest supermarket BBC News (13/11/13)

Sainsbury’s profits make it second biggest supermarket BBC News (13/11/13)

Asda to launch £1bn price-cut plan AOL, Press Association (15/11/13)

Asda takes fight to rivals with £1bn investment plan The Guardian, Angela Monaghan (14/11/13)

UK’s Asda promises £1 billion investment in price cuts Reuters (14/11/13)

Asda makes bid to woo shoppers with vow of five-year £1billion price war after it was overtaken in market share by Sainsbury’s Mail Online, Sean Poulter (15/11/13)

Sainsbury’s overtakes Asda on demand for its premium lines Independent, Simon Neville (14/11/13)

Asda to put £1bn into lowering prices over five years The Grocer, Thomas Hobbs (14/11/13)

Wal-Mart posts $3.7bn quarterly income BBC News (14/11/13)

Questions

- What are the key characteristics of an oligopoly?

- What is meant by a price war? Who benefits?

- How important is the concept of price elasticity of demand when deciding whether or not to cut the price of a range of products?

- Why is the proportion of income spent on a good a key determinant of the elasticity of demand of a product?

- How can market share be calculated?

- Many suggest that the ‘middle market’ of the supermarket sector is slowly disappearing. Why is this?

- How effective will Asda’s price cutting strategy be? Which factors will determine its effectiveness?

The cost of living is a contentious issue and is likely to form a key part of the political debate for the next few years. This debate has been fuelled by the latest announcement by SSE of an average rise in consumer energy bills of 8.2%, meaning that an average dual-fuel customer would see its bill rise by £106. With this increase, the expectation is that the other big energy companies will follow suit with their own price rises.

The cost of living is a contentious issue and is likely to form a key part of the political debate for the next few years. This debate has been fuelled by the latest announcement by SSE of an average rise in consumer energy bills of 8.2%, meaning that an average dual-fuel customer would see its bill rise by £106. With this increase, the expectation is that the other big energy companies will follow suit with their own price rises.

Energy prices are made up of numerous factors, including wholesale prices, investment in infrastructure and innovation, together with government green energy taxes. SSE has put their price hike down to an increase in wholesale prices, but has also passed part of the blame onto the government by suggesting that the price hikes are required to offset the government’s energy taxes. Will Morris, from SSE said:

We’re sorry we have to do this…We’ve done as much as we could to keep prices down, but the reality is that buying wholesale energy in global markets, delivering it to customers’ homes, and government-imposed levies collected through bills – endorsed by all the major parties – all cost more than they did last year.

The price hike has been met with outrage from customers and the government and has provided Ed Miliband with further ammunition against the Coalition’s policies. However, even this announcement has yet to provide the support for Labour’s plans to freeze energy prices, as discussed in the blog Miliband’s freeze.  Customers with other energy companies are likely to see similar price rises in the coming months, as SSE’s announcement is only the first of many. A key question is how will the country provide the funding for much needed investment in the energy sector? The funds of the government are certainly not going to be available to provide investment, so the job must pass to the energy companies and in turn the consumers. It is this that is given as a key reason for the price rises.

Customers with other energy companies are likely to see similar price rises in the coming months, as SSE’s announcement is only the first of many. A key question is how will the country provide the funding for much needed investment in the energy sector? The funds of the government are certainly not going to be available to provide investment, so the job must pass to the energy companies and in turn the consumers. It is this that is given as a key reason for the price rises.

Investment in the energy infrastructure is essential for the British economy, especially given the lack of investment that we have seen over successive governments – both Labour and Conservative. Furthermore, the government’s green targets are essential and taxation is a key mechanism to meet them. Labour has been criticized for its plans to freeze energy prices, which may jeopardise these targets. The political playing field is always fraught with controversy and it seems that energy prices and thus the cost of living will remain at the centre of it for many months.

More energy price rises expected after SSE increase BBC News (10/10/13)

SSE retail boss blames government for energy price rise The Telegraph, Rebecca Clancy (10/10/13)

A better way to take the heat out of energy prices The Telegraph (11/10/13)

SSE energy price rise stokes political row Financial Times, John Aglionby and Guy Chazan (10/10/13)

Ed Miliband condemns ‘rip-off’ energy firms after SSE 8% price rise The Guardian, Terry Macalister, Angela Monaghan and Rowena Mason (28/9/12)

Coalition parties split over energy companies’ green obligations Independent, Nigel Morris (11/10/13)

Energy price rise: David Cameron defends green subsidies The Guardian, Rowena Mason (10/10/13)

‘Find better deals’ users urged as energy bills soar Daily Echo (11/10/13)

Energy Minister in row over cost of taxes Sky News (10/10/13)

SSE energy price rise ‘a bitter pill for customers’ The Guardian, Angela Monaghan (10/10/13)

Energy firm hikes prices, fuels political row Associated Press (10/10/13)

Only full-scale reform of our energy market will prevent endless price rises The Observer, Phillip Lee (27/10/13)

Questions

- In what market structure would you place the energy sector?

- Explain how green taxes push up energy bills? Use a diagram to support your answer.

- Consider the energy bill of an average household. Using your knowledge and the articles above, allocate the percentage of that bill that is derived from wholesale prices, green taxes, investment in infrastructure and any other factors. Which are the key factors that have risen, which has forced SSE (and others) to push up prices?

- Why is investment in energy infrastructure and new forms of fuel essential? How might such investment affect future prices?

- Why has Labour’s proposed 20-month price freeze been criticised?

- What has happened to energy prices over the past 20 years?

- Is there now a call for more government regulation in the energy sector to allay fears of rises in the cost of living adversely affecting the poorest households?

When people take out loans they typically do so to spend and with the UK economy in its current state, many would argue that this is a good thing. The ‘payday loan’ industry took advantage of the weak economy and the squeezed households in the UK and for the past few years, we have seen constant adverts that will appeal to many households. But, is the industry as competitive as the adverts would have us believe?

When people take out loans they typically do so to spend and with the UK economy in its current state, many would argue that this is a good thing. The ‘payday loan’ industry took advantage of the weak economy and the squeezed households in the UK and for the past few years, we have seen constant adverts that will appeal to many households. But, is the industry as competitive as the adverts would have us believe?

An inquiry into this industry has been on-going for some time, and it has now been referred to the Competition Commission, due to ‘deep-rooted problems with the way competition works’. For some, a payday loan is a short term form of finance, but for others it has become a way of living that has led to a debt spiral. Frank McKillop, policy manager at Abcul said:

There is a clear demand for instant credit and across the country we are increasingly seeing members who have debts with multiple payday lenders and a record of rolling over debts, or going to one payday lender to clear the debt to another.

One problem identified by the OFT is that customers have found it difficult to compare costs and this has led, in some cases, to customers paying back significantly more than they originally thought. Customers being unable to repay loans will ring warning bells for many people, with no-one wanting a return to the height of the credit crunch.

The OFT has criticized payday loan companies for competing not on costs, but on the speed of approval and using certain unapproved tactics as part of their advertising. The selling point of such companies is that you can have the money in a very short time period. However, the criticism is that this leads to loans being given to those who are unable to afford them. Key credit checks are not being done and with late night texts being sent to often financially vulnerable people, it is no wonder that complaints have been received. In a statement, the OFT said:

The OFT has criticized payday loan companies for competing not on costs, but on the speed of approval and using certain unapproved tactics as part of their advertising. The selling point of such companies is that you can have the money in a very short time period. However, the criticism is that this leads to loans being given to those who are unable to afford them. Key credit checks are not being done and with late night texts being sent to often financially vulnerable people, it is no wonder that complaints have been received. In a statement, the OFT said:

The competitive pressure to approve loans quickly may give firms an incentive to skimp on the affordability assessment which is designed to prevent irresponsible lending and protect consumers.

[the business models of companies were] predicated on making loans which are unaffordable, leading to borrowers paying far more than expected through rollovers, additional interest and other charges.

While payday loans are legal and there are many companies offering them, it is what they are competing over, which seems to be in question. The industry itself has begun to change its practices, providing more information to customers, only allowing loans to be rolled over three times and the potential to freeze repayments if the customer gets into financial difficulty. If more stringent checks are completed and hence timing does not become the only grounds for competition, then the problems above may become less significant. With the ongoing OFT inquiry into the practices of the payday loan industry and the continuing demand for such financing, it is likely that we will see much more of both the good and the bad that it has to offer. The following articles consider the investigation.

Webcasts

Balls warns against payday loans ‘blank cheque’ BBC News (27/6/13)

Payday lender investigation could be delayed by bureaucracy Telegraph, Steve Hawkes (27/6/13)

Payday lenders to face ‘tougher restrictions’ on advertising BBC News, Simon Gompertz (1/7/13)

Payday lending rates BBC News, Julio Martino and Stella Creasy (2/7/13)

Articles

Regulator to investigate payday loan industry Financial Times, Elaine Moore and Robert Cookson (27/6/13)

Q&A: Payday loans BBC News (31/5/13)

Payday loans: reining in an industry that is a law unto itself Guardian (27/6/13)

Payday loans industry to face competition inquiry BBC News (27/6/13)

Payday loans firms face competition inquiry Sky News (27/6/13)

Payday loans market faces competition inquiry Guardian, Hilary Osborne (27/6/13)

OFT refers payday loans to Competition Commission Scotsman, Jane Bradley (27/6/13)

Five reasons why we all need to worry about payday lenders Telegraph, Emma Simon (27/6/13)

OFT documents

Payday lending compliance review Office of Fair Trading (27/6/13)

Questions

- Into which market structure would you place the payday loans industry? Make sure you justify your answer.

- What is the role of the (a) the OFT and (b) the Competition Commission? Do these authorities overlap?

- What part does advertising play in this industry?

- To what extent is the payday loan industry a possible cause of another credit crunch?

- Why has the OFT referred this industry to the Competition Commission?

- To what extent are payday loans an essential part of an economy?

The English Premier League (EPL) has negotiated a record TV deal which will generate £5.5 billion of revenue over the next 3 years – beginning in the season 2013–14. This represents a 70% increase on the previous deal. Controversy has arisen over some initial proposals put forward by the EPL as to how the money will be spent. The owners of the clubs in the Championship of the English Football League (EFL) are particularly concerned about the size of the proposed payments to the three teams relegated from the EPL.

The English Premier League (EPL) has negotiated a record TV deal which will generate £5.5 billion of revenue over the next 3 years – beginning in the season 2013–14. This represents a 70% increase on the previous deal. Controversy has arisen over some initial proposals put forward by the EPL as to how the money will be spent. The owners of the clubs in the Championship of the English Football League (EFL) are particularly concerned about the size of the proposed payments to the three teams relegated from the EPL.

Some 30 years ago the money generated from the sale of television rights was equally shared between all the teams in the then four divisions of the English Football League (EFL). In 1992 the top division of the English Football League broke away and formed the English Premier League (EPL). This newly formed EPL negotiated a separate television deal and kept the majority of the money. However, some payments were and still are made to the teams in the EFL and to organisations such as the League Managers Association and Professional Footballers Association. For example in 2011-–12 the EPL donated £189.4 million of the £1.2 billion generated from that year’s TV deal.

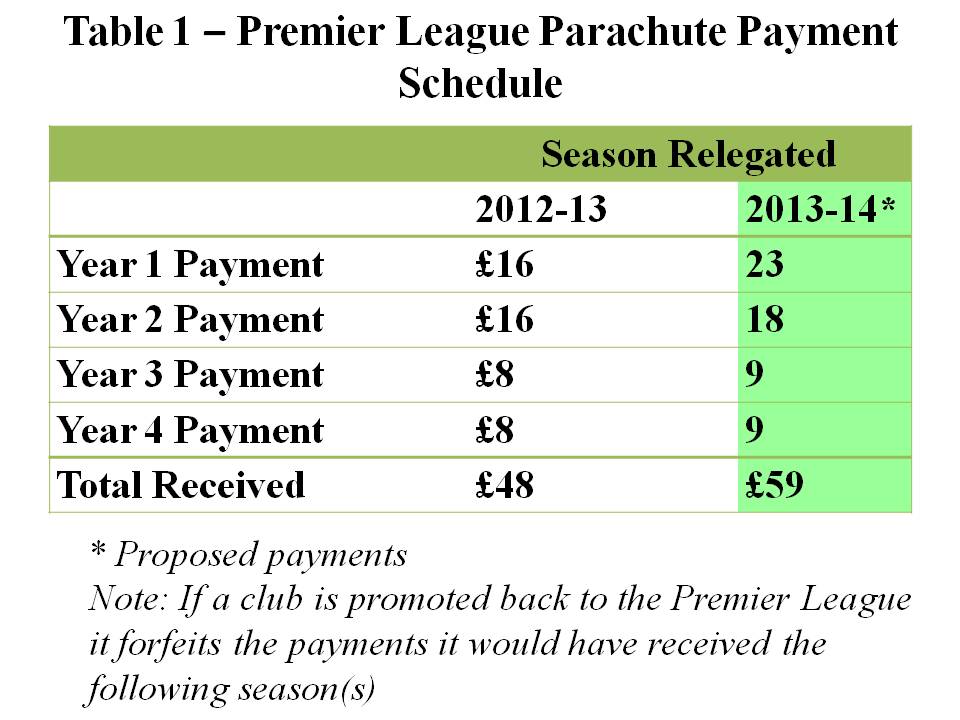

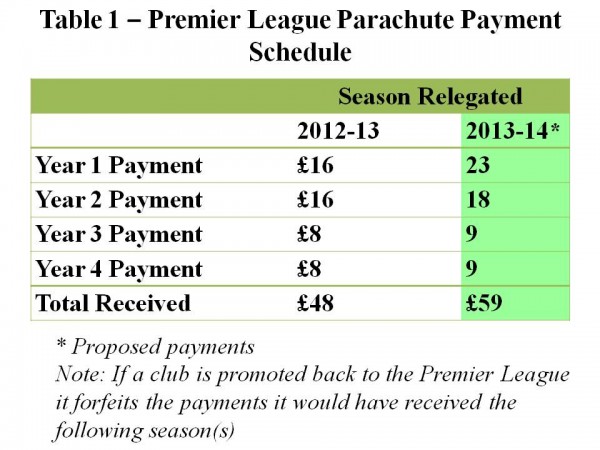

The majority of the money donated by the EPL is spent in two main ways. First, some money is redistributed to all the teams in the EFL: i.e. The Championship, League 1 and League 2. These are known as ‘solidarity payments’ and in 2011–12 the EPL spent £49.8 million on this scheme. Each club in the Championship received £2.3 million. It has been proposed that the amount paid into this scheme should be increased by 5% in the season 2013–14. Second, a relatively large amount of money is paid over a four-year period to the three teams relegated each season from the EPL into the Championship. These are known as ‘parachute payments’ and in the season 2011–12 the EPL spent £90.9 million on this scheme. The rationale for having parachute payments is to help the relegated teams adjust their wage bills to the much lower revenue streams that come from playing in the Championship. Proposed changes to the scheme are outlined in Table 1.

The chairmen of the football league clubs met on the 20th March 2013 and a number of them expressed concerns about the relatively large increase in the parachute payments compared to the solidarity payments. They were particularly concerned that the changes to the funding would damage the competitive balance of the Championship.

The chairmen of the football league clubs met on the 20th March 2013 and a number of them expressed concerns about the relatively large increase in the parachute payments compared to the solidarity payments. They were particularly concerned that the changes to the funding would damage the competitive balance of the Championship.

Competitive balance refers to how the most talented players are distributed amongst the teams in a league. For example, are the majority of the most talented footballers playing for just a couple of the teams? In this case the league is competitively imbalanced and the teams with the best players will tend to win far more games than the other teams. The outcome of the league will be very predictable. If the most talented players were more evenly spread across all the teams in the league, then it would be more competitively balanced. Matches and the outcome of the league would become more unpredictable.

Does the level of competitive balance matter? Some sports economists have argued that it may have a significant impact on the success of the league. This is because fans may value the unpredictability of the results. It follows that closer and more unpredictable results will generate higher match-day attendances and increase the revenues of the clubs.

This is an interesting argument and is the opposite of what economic theory would predict for most markets. For example, the standard prediction would be that as firms outperform their rivals, they generate more revenue and profit. If they manage to drive all their rivals out of business, they would become a pure monopoly and make large abnormal profits. However in professional team sports the outcome may differ significantly. If the unpredictability of the league is highly valued by fans, then teams will generate more revenue when they have strong and evenly matched rivals.

It has been reported that further discussions about the distribution of the money will take place this month with the owners of the championship clubs arguing that there should be smaller increases in parachute payments and much larger increases in solidarity payments. Representatives of the EPL have argued that the parachute payments do not distort competition and make the championship predictable. They point out that at present only one of the top six teams in the championship (Hull) receives parachute payments, while only one of the teams promoted from the Championship in the season 2012–13 (West Ham) received these payments.

Articles

Premier League warned over rich and poor split in wake of TV deal The Guardian, Owen Gibson (19/3/13)

Championship clubs angered by Premier League parachute boost Daily Mail, Charles Sale (6/2/13)

Football league is to lessen the advantage of parachute payments The Guardian, Owen Gibson (20/3/13)

Championship clubs warn Premier League over hike in parachute payments for relegated teams The Independent, Majid Mohamed (20/3/13)

Increased parachute payments could lead to a salary cap in the Championship The Post, A. Stockhausen (21/3/13)

Scudamore:Parachute payment system fair Eurosport, Andy Eckardt (22/3/13)

Parachute payments more than a softened landing The Daisy Cutter, Richard Brook (21/3/13)

Questions

- What factors will influence the size of the attendance at a football match?

- To what extent do you think that the money generated from the sale of television rights should be equally shared between all the clubs in the English Premier League and the English Football League

- Can you think of any ways of measuring the competitive balance of a football league?

- Explain why a very competitively imbalanced league may reduce the revenue for all the clubs in that league?.

- In traditional economic theory it is assumed that firms aim to maximise their profits. What do you think is the objective of a typical football club in the English Premier League?

The Big Four are well known: Deloitte, Ernst and Young, KPMG and PWC. They act as auditors for 90% of the UK’s stock-market listed companies. They have a very close relationship with the companies that they audit and because of this have faced criticism of not warning of the financial crisis. A further accusation is that the relationship between auditors and managers has become blurred.

The Big Four are well known: Deloitte, Ernst and Young, KPMG and PWC. They act as auditors for 90% of the UK’s stock-market listed companies. They have a very close relationship with the companies that they audit and because of this have faced criticism of not warning of the financial crisis. A further accusation is that the relationship between auditors and managers has become blurred.

In some sense, there is a problem of divorce of ownership from control. The companies that are audited by the Big Four have shareholders who are interested in profits and their dividends. But they employ managers who are responsible for the day-to-day running of the business. However, there are concerns that the auditors have become more concerned with meeting the interests of the managers and not of the shareholders. It has been suggested that the company’s management tend to ‘present their accounts in the most favourable light, whereas shareholder interests can be quite different.’ Laura Carstensen, the chair of the Audit Investigation Group said:

It is clear that there is significant dissatisfaction amongst some institutional investors with the relevance and extent of reporting in audited financial reports … management may have incentives to present their accounts in the most favourable light, whereas shareholder interests can be quite different.

The Big Four have been criticised for limiting competition in the industry. The Competition Commission has said that companies typically stay with the same auditing firm and this acts to limit competition. One suggestion to encourage competition is to enforce rotation of Auditors. However, the Big Four have said that the market remains competitive, ‘healthy and robust’ and that any enforcement as noted above would not be in the public interest. Other, smaller auditing companies have praised the preliminary report of the Competition Commission. One firm said:

The Big Four have been criticised for limiting competition in the industry. The Competition Commission has said that companies typically stay with the same auditing firm and this acts to limit competition. One suggestion to encourage competition is to enforce rotation of Auditors. However, the Big Four have said that the market remains competitive, ‘healthy and robust’ and that any enforcement as noted above would not be in the public interest. Other, smaller auditing companies have praised the preliminary report of the Competition Commission. One firm said:

No one solution will achieve market correction, but rather a combination of tendering requirements, encouragement of transparency and dialogue between auditors, companies and investors, and reform of outdated exclusionary practices should provide a backdrop for a healthier FTSE 350 audit market.

The report is not yet final, but the future of the Big Four is somewhat uncertain, especially with the European Commission’s desire to break them up. The following articles look at this industry.

Big Four accountants reject claims over high prices and poor competition The Guardian, Josephine Moulds and David Feeney (22/2/13)

Competition Commission raps Big Four accountants BBC News (22/2/13)

Big Four’s rivals welcome audit shake-up Financial Times, Adam Jones (22/2/13)

UK’s “Big Four” accountants under fire from watchdog Reuters, Huw Jones (22/2/13)

Big Four chastised by Competition Commission The Telegraph, Helia Ebrahimi (22/2/13)

The uncompetitive culture of auditing’s big four remains undented The Guardian, Prem Sikka (23/2/13)

Big Four accountants ‘in closed club on audits’ Independent, Mark Leftly (23/2/13)

Questions

- What is the role of the Competition Commission?

- Explain with other examples the problem of the divorce of ownership from control. How might the interest of shareholders and managers differ? Can they ever be aligned?

- Is market share a good measure of the competitiveness of an industry?

- What are the benefits of competition?

- Why has the regulator suggested that the Big Four are limiting competition?

- What solutions have been proposed by the Competition Commission? Explain how they are likely to stimulate competition in this market.

UK Supermarkets: a prime example of an oligopoly. This industry is highly competitive and over the past decade, but particularly since the onset of the credit crunch, price wars have been a constant feature of this market. You could barely watch a full programme on commercial TV without seeing one of the big supermarkets advertising that their prices were lower than everyone else’s! So, despite oligopoly being towards the ‘least competitive’ end of the market structure spectrum, this is an example of just how competitive the market can actually be.

UK Supermarkets: a prime example of an oligopoly. This industry is highly competitive and over the past decade, but particularly since the onset of the credit crunch, price wars have been a constant feature of this market. You could barely watch a full programme on commercial TV without seeing one of the big supermarkets advertising that their prices were lower than everyone else’s! So, despite oligopoly being towards the ‘least competitive’ end of the market structure spectrum, this is an example of just how competitive the market can actually be. close the gap with the two big discount supermarkets. As Andy Clarke, Asda’s Chief Executive, said:

close the gap with the two big discount supermarkets. As Andy Clarke, Asda’s Chief Executive, said: Of course, there are many other factors that affect a consumer’s decision as to whether to shop at Asda, Tesco or any other big supermarket. In the area where I live, we have a Tesco and a Morrisons (a few years ago, we had neither!). I don’t shop at Asda, as the nearest branch is over 30 miles away – even if prices were significantly lower, it would be more expensive to get there and back and a lot less convenient. For others, it may be loyalty and not just of the ‘I’ve shopped there all my life’ kind! For some, clubcard vouchers from Tesco may be preferred to Asda’s offerings and thus tiny price differences between the supermarkets may have little effect on a consumer’s decision as to where to shop. Many products at supermarkets are relatively cheap and thus as the proportion of our income that we spend on these goods is pretty low, any change in price doesn’t cause much of an effect on our demand.

Of course, there are many other factors that affect a consumer’s decision as to whether to shop at Asda, Tesco or any other big supermarket. In the area where I live, we have a Tesco and a Morrisons (a few years ago, we had neither!). I don’t shop at Asda, as the nearest branch is over 30 miles away – even if prices were significantly lower, it would be more expensive to get there and back and a lot less convenient. For others, it may be loyalty and not just of the ‘I’ve shopped there all my life’ kind! For some, clubcard vouchers from Tesco may be preferred to Asda’s offerings and thus tiny price differences between the supermarkets may have little effect on a consumer’s decision as to where to shop. Many products at supermarkets are relatively cheap and thus as the proportion of our income that we spend on these goods is pretty low, any change in price doesn’t cause much of an effect on our demand.