The UK electricity supply market is an oligopoly. Over 95% of the market is supplied by the ‘big six’: British Gas (Centrica), EDF Energy, E.ON, npower (RWE), Scottish Power (Iberdrola) and SSE. The big six also generate much of the electricity they supply; they are vertically integrated companies. Between them they generate nearly 80% of the country’s electricity. There are a further two large generators, Drax Power Limited and GDF Suez Energy UK, making the generation industry an oligopoly of eight key players.

The UK electricity supply market is an oligopoly. Over 95% of the market is supplied by the ‘big six’: British Gas (Centrica), EDF Energy, E.ON, npower (RWE), Scottish Power (Iberdrola) and SSE. The big six also generate much of the electricity they supply; they are vertically integrated companies. Between them they generate nearly 80% of the country’s electricity. There are a further two large generators, Drax Power Limited and GDF Suez Energy UK, making the generation industry an oligopoly of eight key players.

Ofgem, the energy market regulator, has just published a report on the wholesale electricity market, arguing that it is insufficiently liquid. This, argues the report, acts as a barrier to entry to competitor suppliers. It thus proposes measures to increase liquidity and thereby increase effective competition. Liquidity, according to the report, is:

… the ability to quickly buy or sell a commodity without causing a significant change in its price and without incurring significant transaction costs. It is a key feature of a well-functioning market. A liquid market can also be thought of as a ‘deep’ market where there are a number of prices quoted at which firms are prepared to trade a product. This gives firms confidence that they can trade when needed and will not move the price substantially when they do so.

A liquid wholesale electricity market ensures that electricity products are available to trade, and that their prices are robust. These products and price signals are important for electricity generators and suppliers, who need to trade to manage their risks. Liquidity in the wholesale electricity mark et therefore supports competition in generation and supply, which has benefits for consumers in terms of downward pressure on bills, better service and greater choice.

A liquid wholesale electricity market ensures that electricity products are available to trade, and that their prices are robust. These products and price signals are important for electricity generators and suppliers, who need to trade to manage their risks. Liquidity in the wholesale electricity mark et therefore supports competition in generation and supply, which has benefits for consumers in terms of downward pressure on bills, better service and greater choice.

So how can liquidity be increased? Ofgem is proposing that the big six publish prices for two years ahead at which they are contracting to purchase electricity from generators in long-term contracts. These bilateral deals with generators are often with their own company’s generating arm. Publishing prices in this way will allow smaller suppliers to be able to seek out market opportunities. The generating companies will not be allowed to refuse to contract to supply smaller companies at the prices they are being forced to publish.

In addition, Ofgem is proposing that generators would have to sell 20% of output in the open market instead of through bilateral deals. As it is, however, some 30% of output is currently auctioned on the wholesale spot market (i.e. the market for immediate use).

But it is pricing transparency plus small suppliers being able to gain access to longer-term contracts that are the two key elements of the proposed reform.

Articles

UK utilities face having to disclose long-term deals Reuters, Karolin Schaps and Rosalba O’Brien (12/6/13)

Ofgem set to ‘break stranglehold’ in the energy market BBC News, John Moylan (12/6/13)

Ofgem plan ‘to end energy stranglehold’ BBC Today Programme, John Moylan and Ian Marlee (12/6/13)

Ofgem plan ‘to end energy stranglehold’ BBC Today Programme, John Moylan and Ian Marlee (12/6/13)

Ofgem outlines proposals to ‘break stranglehold’ of big six energy suppliers on electricity market The Telegraph (12/6/13)

Ofgem widens investigation into alleged rigging of gas and power markets The Guardian, Terry Macalister (6/6/13)

Ofgem moves to break stranglehold of ‘big six’ energy suppliers Financial Times, Guy Chazan (12/6/13)

Ofgem to crackdown on Big Six energy suppliers in bid to cut electricity prices Independent, Simon Read (12/6/13)

Reports and data

Opening up Electricity Market to Effective Competition Ofgem Press Release (12/6/13)

Wholesale power market liquidity: final proposals for a ‘Secure and Promote’ licence condition – Draft Impact Assessment Ofgem (12/6/13)

Electricity statistics Department of Energy & Climate Change

The Dirty Half Dozen Friends of the Earth (Oct 2011)

Questions

- What barriers to entry exist in (a) the wholesale and (b) the retail market for electricity?

- Distinguish between spot and forward markets. Why is competition in forward markets particularly important for small suppliers of electricity?

- How will ‘liquidity’ be increased by the measures Ofgem is proposing?

- To what extent does vertical integration in the energy industry benefit consumers of electricity?

- What is a price reporting agency (PRA)? What anti-competitive activities have been taking place in the short-term energy market and why may PRAs not be ‘fit for purpose’?

- Do you think that the measures Ofgem is proposing will ensure that the big generators trade fairly with small suppliers? Explain.

- What are the dangers in the proposals for the large generators?

The Clean Energy Bill has been on the agenda for some time and not just in the UK. With climate change an ever growing global concern, investment in other cleaner energy sources has been essential. However, when it comes to investment in wind farms, developers have faced significant opposition. The balancing act for the government appears to be generating sufficient investment in wind farms, while minimising the negative externalities.

The Clean Energy Bill has been on the agenda for some time and not just in the UK. With climate change an ever growing global concern, investment in other cleaner energy sources has been essential. However, when it comes to investment in wind farms, developers have faced significant opposition. The balancing act for the government appears to be generating sufficient investment in wind farms, while minimising the negative externalities.

The phrase often thrown around with regards to wind farms, seems to be ‘not in my backyard’. That is, people recognise the need for them, but don’t want them to be built in the local areas. The reason is to do with the negative externalities. Not only are the wind farms several metres high and wide, creating a blight on the landscape, but they also create a noise, both of which impose a third party effect on the local communities. These factors, amongst others, have led to numerous protests whenever a new wind farm is suggested. The problem has been that with such challenging targets for energy, wind farms are essential and thus government regulation has been able to over-ride the protests of local communities.

However, planning guidance in the UK will now be changed to give local opposition the ability to override national energy targets. In some sense, more weight is being given to the negative externalities associated with a new wind farm. This doesn’t mean that the government is unwilling to let investment in wind farms stop. Instead, incentives are being used to try to encourage local communities to accept new wind farms. While acknowledging the existence of negative externalities, the government is perhaps trying to put a value on them. The benefits offered to local communities by developers will increase by a factor of five, thus aiming to compensate those affected accordingly. Unsurprisingly, there have been mixed opinions, summed up by Maria McCaffery, the Chief Executive of trade association RenewableUK:

Maria McCaffery, chief executive of trade association RenewableUK, said the proposals would signal the end of many planned developments and that was “disappointing”.

Developing wind farms requires a significant amount of investment to be made upfront. Adding to this cost, by following the government’s advice that we should pay substantially more into community funds for future projects, will unfortunately make some planned wind energy developments uneconomic in England.

That said, we recognise the need to ensure good practice across the industry and will continue to work with government and local authorities to benefit communities right across the country which are hosting our clean energy future.

The improved benefits package by the energy industry is expected to be in place towards the end of the year. The idea is that with greater use of wind farms, energy bills can be subsidised, thereby reducing the cost of living. Investment in wind farms (on-shore and off-shore) is essential. Current energy sources are non-renewable and as such new energy sources must be developed. However, many are focused on the short term cost and not the long term benefit that such investment will bring. The public appears to be in favour of investment in new energy sources, especially with the prospect of subsidised energy bills – but this positive outlook soon turns into protest when the developers pick ‘your back yard’ as the next site. The following articles consider this issue.

Residents to get more say over wind farms The Guardian, Fiona Harvey and Peter Walker (6/6/13)

Local communities offered more say over wind farms BBC News (6/6/13)

Locals to get veto power over wind farms The Telegraph, Robert Winnett (6/6/13)

Wind farms are a ‘complete scam’, claims the Environment Secretary who says turbines are causing ‘huge unhappiness’ Mail Online, Matt Chorley (7/6/13)

New planning guidance will make it harder to build wind farms Financial Times, Jim Pickard, Pilita Clark and Elizabeth Rigby (6/6/13)

Will more power to nimbys be the death of wind farms? Channel 4 News (6/6/13)

Locals given more ground to block wind farms Independent, Tom Bawden (6/6/13)

Questions

- What are the negative externalities associated with wind farms?

- Conduct a cost-benefit analysis as to whether a wind farm should be constructed in your local area. Which factors have you given greatest weight to?

- In question 2 above, were you concerned about the Pareto criterion or the Hicks-Kaldor criterion?

- If local communities can be compensated sufficiently, should wind farms go ahead?

- If the added cost to the development of wind farms means that some will no longer go ahead, is this efficient?

- Why is there a need to invest in new energy sources?

- To what extent is climate change a global problem requiring international (and not national) solution?

The Competition Commission (CC) recently completed their provisional investigation into the cement and concrete market in Great Britain (press release). They concluded that coordination between the main cement producers is resulting in high prices.

The Competition Commission (CC) recently completed their provisional investigation into the cement and concrete market in Great Britain (press release). They concluded that coordination between the main cement producers is resulting in high prices.

In contrast, to illegal cartels (see for example the recent post on this site), the firms in this market are not accused of doing anything illegal. Instead, the CC’s concern is with tacit collusion. Here, no illegal communication between firms takes place, firms simply do not compete intensely due to a mutual understanding that high prices are collectively beneficial.

Economic theory suggests that one key factor that facilitates tacit coordination is a low number of firms in the market. The UK cement market certainly meets this criteria as it is an oligopoly with just three main players plus a new entrant. The CC concluded that:

In a highly concentrated market where the product doesn’t vary, the established producers know too much about each other’s businesses and have concentrated on retaining their respective market shares rather than competing to the full.

They estimate that this cost consumers over £180m in a 3 year period.

Whilst tacit collusion is not illegal, competition authorities can try to prevent it from arising by intervening in mergers that they believe will make it more likely. In fact, the new entrant to the cement market came about due to sales required by the CC before they would allow a joint-venture between two of the main players to go ahead. Clearly the CC’s recent findings suggest that this intervention was not sufficient to ensure intense competition in the market. However, an additional tool available to the authorities in the UK is to be able to remedy harm to competition undercovered as a result of an investigation into the market. In some cases this may even involve breaking-up firms in the market (see for example the decision to force BAA to sell several airports).

When deciding on how to remedy the problem in the cement market, the CC will be keen to avoid the past mistakes of their Danish counterparts. In a famous case, in 1993 the Danish authorities attempted to increase competition in the concrete market by publishing individual sellers’ prices. The idea was that this would stimulate competition by encouraging buyers to shop around. However, evidence published here suggests that this in fact increased prices by around 15%! Why? The paper examines possible explanations and concludes that the information published by the competition authorities helped firms to monitor each others behaviour and therefore facilitated tacit coordination in the market. This is entirely consistent with economic theory which shows that another key factor which facilitates tacit coordination is market transparency.

When deciding on how to remedy the problem in the cement market, the CC will be keen to avoid the past mistakes of their Danish counterparts. In a famous case, in 1993 the Danish authorities attempted to increase competition in the concrete market by publishing individual sellers’ prices. The idea was that this would stimulate competition by encouraging buyers to shop around. However, evidence published here suggests that this in fact increased prices by around 15%! Why? The paper examines possible explanations and concludes that the information published by the competition authorities helped firms to monitor each others behaviour and therefore facilitated tacit coordination in the market. This is entirely consistent with economic theory which shows that another key factor which facilitates tacit coordination is market transparency.

The CC suggest that such monitoring is also possible in the GB market:

Established information channels such as price announcement letters can signal their plans, and tit-for-tat behaviour and cross-sales can be used to prevent or retaliate against any moves to disturb the overall balance between the different players in this market.

According to the above press release, the remedies the CC are considering include: the sale of capacity or plants by the leading players in the market, creation of buying groups, prohibition on price announcements and restrictions on the publication of industry level data. This suggests that the CC are well aware that reducing market transparency can play a key role in preventing coordination. It will be fascinating to, first, see what the CC opt for, then, what impact this has on competition in the industry.

Articles

Same product, same price? Competition in the UK Global Cement (22/05/13)

Competition Commission uncovers `serious problems’ in cement market Graham Huband, The Courier (22/05/13)

Competition Commission call for cement sell-off Mark Leftley, London Evening Standard (21/05/13)

Competition Commission documents

CC looks to break open cement market Competition Commission Press Release (21/5/13)

Aggregates, cement and ready-mix concrete market investigation Competition Commission core documents (various dates)

Questions

- Explain tacit collusion using a Prisoner’s dilemma game.

- Is cement the type of product where we might expect coordination to be most likely?

- Why is cement an important market in the UK economy?

- The first article above suggests that most of the management team at the new entrant came from the other main players in the market. Do you think this may significantly affect the likelihood of tacit collusion?

- Evaluate the pros and cons of the alternative remedies the CC are considering.

The UK economy faces a growing problem of energy supplies as energy demand continues to rise and as old power stations come to the end of their lives. In fact some 10% of the UK’s electricity generation capacity will be shut down this month.

The UK economy faces a growing problem of energy supplies as energy demand continues to rise and as old power stations come to the end of their lives. In fact some 10% of the UK’s electricity generation capacity will be shut down this month.

Energy prices have risen substantially over the past few years and are set to rise further. Partly this is the result of rising global gas prices.

In 2012, the response to soaring gas prices was to cut gas’s share of generation from 39.9% per cent to 27.5%. Coal’s share of generation increased from 29.5% to 39.3%, its highest share since 1996 (see The Department of Energy and Climate Change’s Energy trends section 5: electricity). But with old coal-fired power stations closing down and with the need to produce a greater proportion of energy from renewables, this trend cannot continue.

But new renewable sources, such as wind and solar, take a time to construct. New nuclear takes much longer (see the News Item, Going nuclear). And electricity from these low-carbon sources, after taking construction costs into account, is much more expensive to produce than electricity from coal-fired power stations.

But new renewable sources, such as wind and solar, take a time to construct. New nuclear takes much longer (see the News Item, Going nuclear). And electricity from these low-carbon sources, after taking construction costs into account, is much more expensive to produce than electricity from coal-fired power stations.

So how will the change in balance between demand and supply affect prices and the security of supply in the coming years. Will we all have to get used to paying much more for electricity? Do we increasingly run the risk of the lights going out? The following video explores these issues.

Webcast

UK may face power shortages as 10% of energy supply is shut down BBC News, Joe Lynam (4/4/13)

Data

Electricity Statistics Department of Energy & Climate Change

Quarterly energy prices Department of Energy & Climate Change

Questions

- What factors have led to a rise in electricity prices over the past few years? Distinguish between demand-side and supply-side factors and illustrate your arguments with a diagram.

- Are there likely to be power cuts in the coming years as a result of demand exceeding supply?

- What determines the price elasticity of demand for electricity?

- What measures can governments adopt to influence the demand for electricity? Will these affect the position and/or slope of the demand curve?

- Why have electricity prices fallen in the USA? Could the UK experience falling electricity prices for similar reasons in a few years’ time?

- In what ways could the government take into account the externalities from power generation and consumption in its policies towards the energy sector?

The English Premier League (EPL) has negotiated a record TV deal which will generate £5.5 billion of revenue over the next 3 years – beginning in the season 2013–14. This represents a 70% increase on the previous deal. Controversy has arisen over some initial proposals put forward by the EPL as to how the money will be spent. The owners of the clubs in the Championship of the English Football League (EFL) are particularly concerned about the size of the proposed payments to the three teams relegated from the EPL.

The English Premier League (EPL) has negotiated a record TV deal which will generate £5.5 billion of revenue over the next 3 years – beginning in the season 2013–14. This represents a 70% increase on the previous deal. Controversy has arisen over some initial proposals put forward by the EPL as to how the money will be spent. The owners of the clubs in the Championship of the English Football League (EFL) are particularly concerned about the size of the proposed payments to the three teams relegated from the EPL.

Some 30 years ago the money generated from the sale of television rights was equally shared between all the teams in the then four divisions of the English Football League (EFL). In 1992 the top division of the English Football League broke away and formed the English Premier League (EPL). This newly formed EPL negotiated a separate television deal and kept the majority of the money. However, some payments were and still are made to the teams in the EFL and to organisations such as the League Managers Association and Professional Footballers Association. For example in 2011-–12 the EPL donated £189.4 million of the £1.2 billion generated from that year’s TV deal.

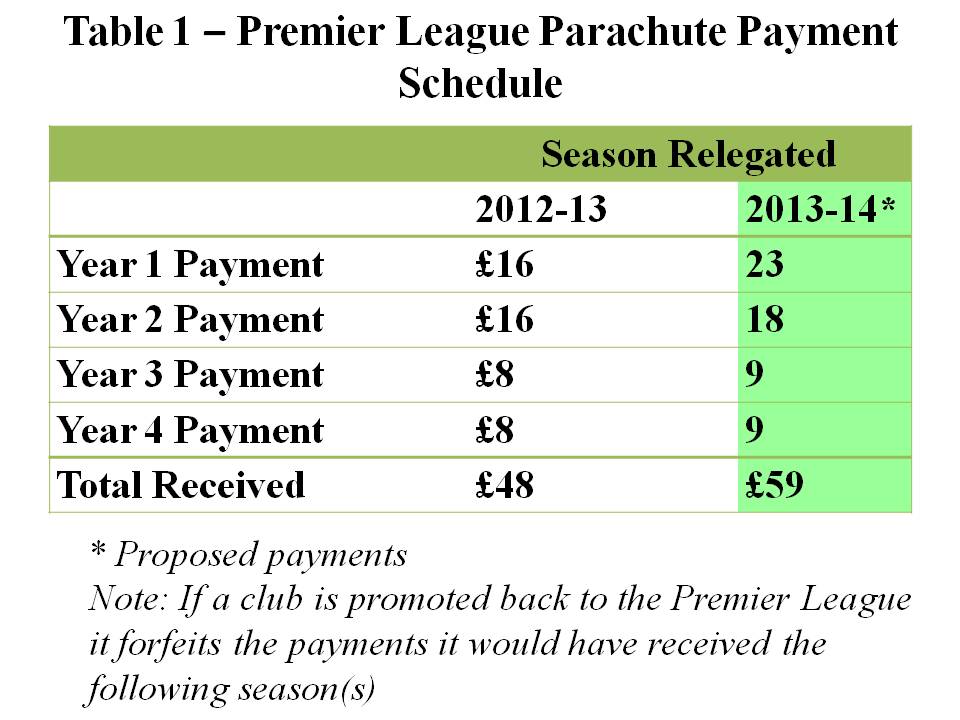

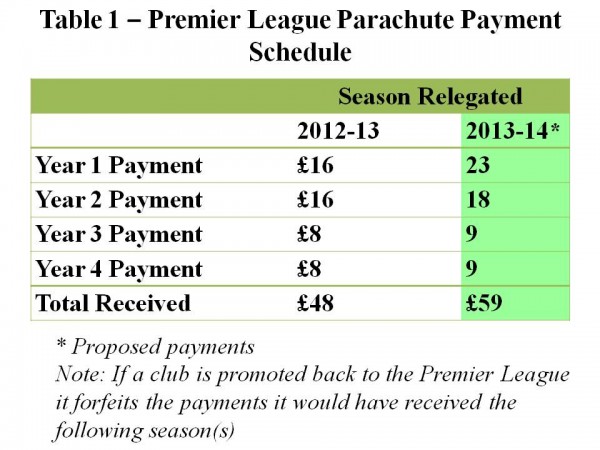

The majority of the money donated by the EPL is spent in two main ways. First, some money is redistributed to all the teams in the EFL: i.e. The Championship, League 1 and League 2. These are known as ‘solidarity payments’ and in 2011–12 the EPL spent £49.8 million on this scheme. Each club in the Championship received £2.3 million. It has been proposed that the amount paid into this scheme should be increased by 5% in the season 2013–14. Second, a relatively large amount of money is paid over a four-year period to the three teams relegated each season from the EPL into the Championship. These are known as ‘parachute payments’ and in the season 2011–12 the EPL spent £90.9 million on this scheme. The rationale for having parachute payments is to help the relegated teams adjust their wage bills to the much lower revenue streams that come from playing in the Championship. Proposed changes to the scheme are outlined in Table 1.

The chairmen of the football league clubs met on the 20th March 2013 and a number of them expressed concerns about the relatively large increase in the parachute payments compared to the solidarity payments. They were particularly concerned that the changes to the funding would damage the competitive balance of the Championship.

The chairmen of the football league clubs met on the 20th March 2013 and a number of them expressed concerns about the relatively large increase in the parachute payments compared to the solidarity payments. They were particularly concerned that the changes to the funding would damage the competitive balance of the Championship.

Competitive balance refers to how the most talented players are distributed amongst the teams in a league. For example, are the majority of the most talented footballers playing for just a couple of the teams? In this case the league is competitively imbalanced and the teams with the best players will tend to win far more games than the other teams. The outcome of the league will be very predictable. If the most talented players were more evenly spread across all the teams in the league, then it would be more competitively balanced. Matches and the outcome of the league would become more unpredictable.

Does the level of competitive balance matter? Some sports economists have argued that it may have a significant impact on the success of the league. This is because fans may value the unpredictability of the results. It follows that closer and more unpredictable results will generate higher match-day attendances and increase the revenues of the clubs.

This is an interesting argument and is the opposite of what economic theory would predict for most markets. For example, the standard prediction would be that as firms outperform their rivals, they generate more revenue and profit. If they manage to drive all their rivals out of business, they would become a pure monopoly and make large abnormal profits. However in professional team sports the outcome may differ significantly. If the unpredictability of the league is highly valued by fans, then teams will generate more revenue when they have strong and evenly matched rivals.

It has been reported that further discussions about the distribution of the money will take place this month with the owners of the championship clubs arguing that there should be smaller increases in parachute payments and much larger increases in solidarity payments. Representatives of the EPL have argued that the parachute payments do not distort competition and make the championship predictable. They point out that at present only one of the top six teams in the championship (Hull) receives parachute payments, while only one of the teams promoted from the Championship in the season 2012–13 (West Ham) received these payments.

Articles

Premier League warned over rich and poor split in wake of TV deal The Guardian, Owen Gibson (19/3/13)

Championship clubs angered by Premier League parachute boost Daily Mail, Charles Sale (6/2/13)

Football league is to lessen the advantage of parachute payments The Guardian, Owen Gibson (20/3/13)

Championship clubs warn Premier League over hike in parachute payments for relegated teams The Independent, Majid Mohamed (20/3/13)

Increased parachute payments could lead to a salary cap in the Championship The Post, A. Stockhausen (21/3/13)

Scudamore:Parachute payment system fair Eurosport, Andy Eckardt (22/3/13)

Parachute payments more than a softened landing The Daisy Cutter, Richard Brook (21/3/13)

Questions

- What factors will influence the size of the attendance at a football match?

- To what extent do you think that the money generated from the sale of television rights should be equally shared between all the clubs in the English Premier League and the English Football League

- Can you think of any ways of measuring the competitive balance of a football league?

- Explain why a very competitively imbalanced league may reduce the revenue for all the clubs in that league?.

- In traditional economic theory it is assumed that firms aim to maximise their profits. What do you think is the objective of a typical football club in the English Premier League?

The UK electricity supply market is an oligopoly. Over 95% of the market is supplied by the ‘big six’: British Gas (Centrica), EDF Energy, E.ON, npower (RWE), Scottish Power (Iberdrola) and SSE. The big six also generate much of the electricity they supply; they are vertically integrated companies. Between them they generate nearly 80% of the country’s electricity. There are a further two large generators, Drax Power Limited and GDF Suez Energy UK, making the generation industry an oligopoly of eight key players.

The UK electricity supply market is an oligopoly. Over 95% of the market is supplied by the ‘big six’: British Gas (Centrica), EDF Energy, E.ON, npower (RWE), Scottish Power (Iberdrola) and SSE. The big six also generate much of the electricity they supply; they are vertically integrated companies. Between them they generate nearly 80% of the country’s electricity. There are a further two large generators, Drax Power Limited and GDF Suez Energy UK, making the generation industry an oligopoly of eight key players.