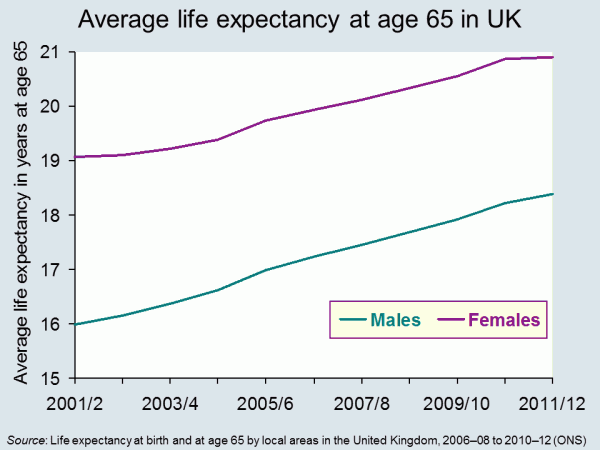

Life expectancy is increasing across the world and the latest set of figures from the Office for National Statistics show that in the UK it has passed 79 for boys born in 2010–12, and 82 for girls born then. In fact the prediction is that over a third of babies born in 2013 will live to more than 100. The data throws up some interesting questions. How well prepared are we for lives that last this long? And how evenly distributed is this increase in life expectancy? Pensions’ minister, Steve Webb, has called for better information on life expectancy to be shared. How would this impact on our decision making?

Life expectancy is increasing across the world and the latest set of figures from the Office for National Statistics show that in the UK it has passed 79 for boys born in 2010–12, and 82 for girls born then. In fact the prediction is that over a third of babies born in 2013 will live to more than 100. The data throws up some interesting questions. How well prepared are we for lives that last this long? And how evenly distributed is this increase in life expectancy? Pensions’ minister, Steve Webb, has called for better information on life expectancy to be shared. How would this impact on our decision making?

It seems reasonable to think that increasing life expectancy must be good news. And of course, for individuals it can be. In 1951 the average man retiring at 65, in England and Wales, could expect to live and draw a pension for another 12.1 years. By 2014 this had risen to 22 years.

But while we can look forward to longer life, for the government, it presents some challenges The first is that we just don’t save enough for our old age. This seems to be partly because we find it hard to make decisions that will have an impact so far in the future. There are a number of measures that have been put in place to encourage us to save more, including auto-enrolment into company pension schemes. This is being rolled out across businesses over the next three years. In the 2014 Budget, the Chancellor announced that people reaching retirement age will be able to draw all their pension as a cash lump sum, rather than having to take it as a regular income.

But while we can look forward to longer life, for the government, it presents some challenges The first is that we just don’t save enough for our old age. This seems to be partly because we find it hard to make decisions that will have an impact so far in the future. There are a number of measures that have been put in place to encourage us to save more, including auto-enrolment into company pension schemes. This is being rolled out across businesses over the next three years. In the 2014 Budget, the Chancellor announced that people reaching retirement age will be able to draw all their pension as a cash lump sum, rather than having to take it as a regular income.

Another concern for government is the variations that we find in life expectancy across the UK. The 2014 ONS data identified that life expectancy for men born in Glasgow in 2012 is 72.6, in East Dorset it is 82.9. 25% of those in Glasgow are not expected to live to 65. The gap in years of good health is even greater. This presents governments with a long-term problem. How do they achieve greater equality in this instance? Do they focus resources on the areas that need it most? Do they legislate to address behaviour? Or do they rely on the provision of good advice – on diet, exercise and other factors?

Information has a role to play in both areas identified above. In April 2014, Steve Webb, suggested that in order to make good decisions at the point of retirement, people need to understand more about what lies ahead. He said:

People tend to underestimate how long they’re likely to live, so we’re talking about averages, something very broad-brush. Based on your gender, based on your age, perhaps asking one or two basic questions, like whether you’ve smoked or not, you can tell somebody that they might, on average, live for another 20 years or so.

This suggestion has led to some concerns being expressed at what appears to be an over-simplistic approach. Estimates can only be based on a mix of averages modified by individual information. Would the projections be shared with pension providers? What would you do if you exceeded your forecast life expectancy – by a long way – and had spent all your money? Could you sue someone?

Will your pension pot last as long as you will? The Telegraph, Dan Hyde and Richard Dyson (23/4/2014)

Scientists invent death test that will tell us how long we have to live Metro (11/8/13)

Games host Glasgow has worst life expectancy in the UK The Guardian, Caroline Davies (16/4/2014)

Pensioners could get life expectancy guidance BBC News Politics (17/4/14)

ONS reveals gaps in life expectancy across the UK FT Adviser Pensions, Kevin White (23/4/14)

Health care aid for developing countries boosts life expectancy Health Canal, Ruth Ann Richter (22/4/14)

A third of babies born this year will live to 100 This is Money.co.uk, Adam Uren (11/12/13)

Questions

- Thinking about the UK, what are the factors that might explain variations in life expectancy across different regions? How might the government address these differences? Why would they want to do so?

- Do the same factors explain variations between countries? Who can address these differences? Who would want to do so?

- If you could have a reasonable prediction of your life expectancy at 65, would you want it? How would your behaviour change if you were predicted a longer than average life expectancy? How would it change if you were predicted a shorter than average life expectancy?

- If you could have an accurate prediction of your life expectancy at 18, how would your answers differ? If this were possible, would it present any problems?

Profits are maximised where marginal cost equals marginal revenue. And in a perfectly competitive market, where price equals marginal revenue, profits are maximised where marginal cost equals price. But what if marginal cost equals zero? Should the competitive profit-maximising firm give the product away? Or is there simply no opportunity for making a profit when there is a high degree of competition?

Profits are maximised where marginal cost equals marginal revenue. And in a perfectly competitive market, where price equals marginal revenue, profits are maximised where marginal cost equals price. But what if marginal cost equals zero? Should the competitive profit-maximising firm give the product away? Or is there simply no opportunity for making a profit when there is a high degree of competition?

This is the dilemma considered in the articles linked below. According to Jeremy Rifkin, what we are seeing is the development of technologies that have indeed pushed marginal cost to zero, or close to it, in a large number of sectors of the economy. For example, information can be distributed over the Internet at little or no cost, other than the time of the distributor who is often willing to do this freely in a spirit of sharing. What many people are becoming, says Rifkin, are ‘prosumers’: producing, sharing and consuming.

Over the past decade millions of consumers have become prosumers, producing and sharing music, videos, news, and knowledge at near-zero marginal cost and nearly for free, shrinking revenues in the music, newspaper and book-publishing industries.

What was once confined to a limited number of industries – music, photography, news, publishing and entertainment – is now spreading.

A new economic paradigm – the collaborative commons – has leaped onto the world stage as a powerful challenger to the capitalist market.

A growing legion of prosumers is producing and sharing information, not only knowledge, news and entertainment, but also renewable energy, 3D printed products and online college courses at near-zero marginal cost on the collaborative commons. They are even sharing cars, homes, clothes and tools, entirely bypassing the conventional capitalist market.

So is a collaborative commons a new paradigm that can replace capitalism in a large number of sectors? Are we gradually becoming sharers? And elsewhere, are we becoming swappers?

Articles

Capitalism is making way for the age of free The Guardian, Jeremy Rifkin (31/3/14)

The End of the Capitalist Era, and What Comes Next Huffington Post, Jeremy Rifkin (1/4/14)

Has the Post-Capitalist Economy Finally Arrived? Working Knowledge, James Heskett (2/4/14)

Questions

- In what aspects of your life are you a prosumer? Is this type of behaviour typical of what has always gone on in families and society?

- If marginal cost is zero, why may average cost be well above zero? Illustrate with a diagram.

- Could a monopolist make a profit if marginal cost was zero? Again, illustrate with a diagram.

- Is it desirable for there to be temporary monopoly profits for inventors of new products and services?

- What is meant by a ‘collaborative commons’? Do you participate in such a commons and, if so, how and why?

- Should tweets and Facebook posts be regarded as output?

- What is meant by an internet-of-things infrastructure?

- What are the incentives for authors to contribute to Wikipedia?

- Could marginal cost ever be zero for new physical products?

- Think about the things you buy in the supermarket. Could any of these be produced at zero marginal cost?

- How can capitalists make profits as ‘aggregators of network services and solutions’?

- Provide a critique of Rifkin’s arguments.

In his Budget on March 19, the Chancellor of the Exchequer, George Osborne, announced fundamental changes to the way people access their pensions. Previously, many people with pension savings were forced to buy an annuity. These pay a set amount of income per month from retirement for the remainder of a person’s life.

But, with annuity rates (along with other interest rates) being at historically low levels, many pensioners have struggled to make ends meet. Even those whose pension pots did not require them to buy an annuity were limited in the amount they could withdraw each year unless they had other guaranteed income of over £20,000.

Now pensioners will no longer be required to buy an annuity and they will have much greater flexibility in accessing their pensions. As the Treasury website states:

This means that people can choose how they access their defined contribution pension savings; for example they could take all their pension savings as a lump sum, draw them down over time, or buy an annuity.

While many have greeted the news as a liberation of the pensions market, there is also the worry that this has created a moral hazard.  When people retire, will they be tempted to blow their savings on foreign travel, a new car or other luxuries? And then, when their pension pot has dwindled and their health is failing, will they then be forced to rely on the state to fund their care?

When people retire, will they be tempted to blow their savings on foreign travel, a new car or other luxuries? And then, when their pension pot has dwindled and their health is failing, will they then be forced to rely on the state to fund their care?

But even if pensioners resist the urge to go on an immediate spending spree, there are still large risks in giving people the freedom to spend their pension savings as they choose. As the Scotsman article below states:

The risks are all too obvious. Behaviour will change. People who no longer have to buy an annuity will not do so but will then be left with a pile of cash. What to do with it? Spend it? Invest it? There are many new risky choices. But the biggest of all can be summed up in one fact: when we retire our life expectancy continues to grow. For every day we live after 65 it increases by six and a half hours. That’s right – an extra two-and-a-half years every decade.

The glory of an annuity is it pays you an income for every year you live – no matter how long. The problem with cash is that it runs out. Already the respected Institute for Fiscal Studies (IFS) has said that the reform ‘depends on highly uncertain behavioural assumptions about when people take the money’. And that ‘there is a market failure here. There will be losers from this policy’.

We do not have perfect knowledge about how long we will live or even how long we can be expected to live given our circumstances. Many people are likely to suffer from a form of myopia that makes them blind to the future: “We’re likely to be dead before the money has run out”; or “Let’s enjoy ourselves now while we still can”; or “We’ll worry about the future when it comes”.

The point is that there are various market failings in the market for pensions and savings. Will the decisions of the Chancellor have made them better or worse?

Articles

Pension shakeup in budget leaves £14bn annuities industry reeling The Guardian, Patrick Collinson (20/3/14)

Chancellor vows to scrap compulsory annuities in pensions overhaul The Guardian, Patrick Collinson and Harriet Meyer (19/3/14)

Labour backs principle of George Osborne’s pension shakeup The Guardian, Rowena Mason (23/3/14)

Osborne’s pensions overhaul may mean there is little left for future rainy days The Guardian, Phillip Inman (24/3/14)

Let’s celebrate the Chancellor’s bravery on pensions – now perhaps the Government can tackle other mighty vested interests Independent on Sunday, Mary Dejevsky (23/3/14)

A vote-buying Budget The Scotsman, John McTernan (21/3/14)

L&G warns on mis-selling risks of pension changes The Telegraph, Alistair Osborne (26/3/14)

Budget 2014: Pension firms stabilise after £5 billion sell off Interactive Investor, Ceri Jones (20/3/14)

Budget publications

Budget 2014: pensions and saving policies Institute for Fiscal Studies, Carl Emmerson (20/3/14)

Budget 2014: documents HM Treasury (March 2014)

Freedom and choice in pensions HM Treasury (March 2014)

Questions

- What market failures are there in the market for pensions?

- To what extent will the new measures help to tackle the existing market failures in the pension industry?

- Explain the concept of moral hazard. To what extent will the new pension arrangements create a moral hazard?

- Who will be the losers from the new arrangements?

- Assume that you have a choice of how much to pay into a pension scheme. What is likely to determine how much you will choose to pay?

Britain has faced some its worst ever weather, with thousands of homes flooded once again, though the total number of flooded households has fallen compared to previous floods. However, for many households, it is just more of the same – if you’ve been flooded once, you’re likely to be flooded again and hence insurance against flooding is essential. But, if you’re an insurance company, do you really want to provide cover to a house that you can almost guarantee will flood?

Britain has faced some its worst ever weather, with thousands of homes flooded once again, though the total number of flooded households has fallen compared to previous floods. However, for many households, it is just more of the same – if you’ve been flooded once, you’re likely to be flooded again and hence insurance against flooding is essential. But, if you’re an insurance company, do you really want to provide cover to a house that you can almost guarantee will flood?

The government has pledged thousands to help households and businesses recover from the damage left by the floods and David Cameron’s latest step has been to urge insurance companies to deal with claims for flood damage as fast as possible. He has not, however, said anything regarding ‘premium holidays’ for flood victims.

The problem is that the premium you are charged depends on many factors and one key aspect is the likelihood of making a claim. The more likely the claim, the higher the premium. If a household has previous experience of flooding, the insurance company will know that there is a greater likelihood of flooding occurring again and thus the premium will be increased to reflect this greater risk. There have been concerns that some particularly vulnerable home-owners will be unable to find or afford home insurance.

The key thing with insurance is that in order for it to be provided privately, certain conditions must hold. The probability of the event occurring must be less than 1 – insurance companies will not insure against certainty. The probability of the event must be known on aggregate to allow insurance companies to calculate premiums. Probabilities must be independent – if one person makes a claim, it should not increase the likelihood of others making claims.

Finally, there should be no adverse selection or moral hazard, both of which derive from asymmetric information. The former occurs where the person taking out the insurance can hide information from the company (i.e. that they are a bad risk) and the latter occurs when the person taking out insurance changes their behaviour once they are insured. Only if these conditions hold or there are easy solutions will the private market provide insurance.

On the demand-side, consumers must be willing to pay for insurance, which provides them with protection against certain contingencies: in this case against the cost of flood damage. Given the choice, rational consumers will only take out an insurance policy if they believe that the value they get from the certainty of knowing they are covered exceeds the cost of paying the insurance premium. However, if the private market fails to offer insurance, because of failures on the supply-side, there will be major gaps in coverage.

Furthermore, even if insurance policies are offered to those at most risk of flooding, the premiums charged by the insurance companies must be high enough to cover the cost of flood damage. For some homeowners, these premiums may be unaffordable, again leading to gaps in coverage.

Perhaps here there is a growing role for the government and we have seen proposals for a government-backed flood insurance scheme for high-risk properties due to start in 2015. However, a loop hole may mean that wealthy homeowners pay a levy for it, but are not able to benefit from the cheaper premiums, as they are deemed to be able to afford higher premiums. This could see many homes in the Somerset Levels being left out of this scheme, despite households being underwater for months. There is also a further role for government here and that is more investment in flood defences. If that occurs though, where will the money come from? The following articles consider flooding and the problem of insurance.

Articles

Insurers urged to process flood claims quickly BBC News (17/2/14)

Insurers urged to process flood claims quickly BBC News (17/2/14)

Flood area defences put on hold by government funding cuts The Guardian, Damian Carrington and Rajeev Syal (17/2/14)

Flooding: 200,000 houses at risk of being uninsurable The Telegraph (31/1/12)

Govt flood insurance plan ‘will not work’ Sky News (14/2/14)

Have we learned our lessons on flooding? BBC News, Roger Harrabin (14/2/14)

ABI refuses to renew statement of principles for flood insurance Insurance Age, Emmanuel Kenning (31/1/12)

Wealthy will have to pay more for flood insurance but won’t be covered because their houses are too expensive Mail Online, James Chapman (7/2/14)

Buyers need ‘flood ratings’ on all houses, Aviva Chief warns The Telegraph, James Quinn (15/2/14)

Wealthy homeowners won’t be helped by flood insurance scheme The Telegraph(11/2/14)

Costly insurance ‘will create flood-risk ghettos and £4.3tn fall in house values’ The Guardian, Patrick Wintour (12/2/14)

Leashold homes face flood insurance risk Financial Times, Alistair Gray (10/2/14)

Questions

- Consider the market for insurance against flood damage. Are risks less than one? Explain your answer.

- Explain whether or not the risk of flooding is independent.

- Are the problems of moral hazard and adverse selection relevant in the case of home insurance against flood damage?

- To what extent is the proposed government-backed flood insurance an equitable scheme? Should the government be stepping in to provide insurance itself?

- Should there be greater regulation when houses are sold to provide better information about the risk of flooding?

- Why if the concept of opportunity cost relevant here?

- How might household values be affected by recent floods, in light of the issues with insurance?

A few weeks ago, Elizabeth wrote a blog on the payday loan industry and its referral by the OFT to the Competition Commission (see A payday inquiry). Now the Archbishop of Canterbury, Justin Welby, has joined the debate. He suggests that the problem of sky-high interest rates charged by payday loan companies would be tackled better by increased competition from elsewhere in the industry than by regulation.

A few weeks ago, Elizabeth wrote a blog on the payday loan industry and its referral by the OFT to the Competition Commission (see A payday inquiry). Now the Archbishop of Canterbury, Justin Welby, has joined the debate. He suggests that the problem of sky-high interest rates charged by payday loan companies would be tackled better by increased competition from elsewhere in the industry than by regulation.

In particular, he proposes an expansion of credit unions. These could provide a much cheaper alternative for people in financial difficulties who are seeking short-term loans. He would like church members with relevant skills to volunteer at credit unions and proposes setting up local credit unions operated from church buildings.

* * * * * * * * * *

In this news item we hand over to ‘Kostas Economides’, an imaginary lecturer in Economics at the imaginary ‘University of the South of England’. Kostas’s blog is written by Guy Judge. Guy recently retired from the University of Portsmouth, where he was Deputy Head of Department, and is now a Visiting Fellow.

In his blog, Kostas frequently reflects on various economic issues, as well as on life at USE. Here he recounts a conversation with his colleagues about Justin Welby’s proposals. They consider various implications of the proposals from an economist’s point of view.

In his blog, Kostas frequently reflects on various economic issues, as well as on life at USE. Here he recounts a conversation with his colleagues about Justin Welby’s proposals. They consider various implications of the proposals from an economist’s point of view.

Kostas’s blog

Pay day loans Guy’s Other Stuff, Guy Judge (30/7/13)

To provide some background to Kostas’s blog, you’ll see below the normal set of links to newspaper articles.

We may well return to Kostas in the near future, as he is planning to look at a number of topical economic issues.

Articles

Why I support Justin Welby’s battle with Wonga The Telegraph, Jacob Rees-Mogg (30/7/13)

Church plans to compete with payday lender Wonga BBC News, Robert Piggott (25/7/13)

Archbishop of Canterbury wants to ‘compete’ Wonga out of existence The Guardian, Miles Brignall (25/7/13)

Let the payday lenders prosper, but not extort Financial Times (30/7/13)

Coalition will support Archbishop of Canterbury Justin Welby’s plan for credit unions, says Vince Cable Independent, Andrew Grice (28/7/13)

Former Archbishop Rowan Williams backs action against payday loan firms Cambridge News, Jennie Baker (30/7/13)

Why Justin Welby’s vision of kumbayah capitalism is wrong The Telegraph, James Quinn (25/7/13)

Wonga V The Church: Comparing Interest Rates Of Payday Loans And Credit Unions The Huffington Post, Tom Moseley (25/7/13)

Wonga Warned Church Of England Could ‘Compete’ It Out Of Existence The Huffington Post, Tom Moseley (25/7/13)

Credit unions thriving even before Archbishop Welby’s attack on Wonga The Guardian, Rupert Jones (29/7/13)

Questions

- Find out the monthly interest rates being charged by various payday loan companies. Take one loan company as an example and calculate what would happen to your debt over the course of a year if you borrowed £100 and paid nothing back each month. What would be the annualised rate of interest?

- What are the arguments for and against banning payday loan companies?

- What are the arguments for and against imposing an interest rate cap on such companies?

- What are the differences between credit unions and banks?

- Should the interest rates charged by credit unions be uncapped?

- Explain what is meant by ‘moral hazard’ and give some examples. What moral hazard would there be in placing a limit on the number of months over which a debt could go on accumulating?

- How would you decide what a ‘normal’ rate of interest should be? Should this vary with the risk of default and, if so, by how much?

Life expectancy is increasing across the world and the latest set of figures from the Office for National Statistics show that in the UK it has passed 79 for boys born in 2010–12, and 82 for girls born then. In fact the prediction is that over a third of babies born in 2013 will live to more than 100. The data throws up some interesting questions. How well prepared are we for lives that last this long? And how evenly distributed is this increase in life expectancy? Pensions’ minister, Steve Webb, has called for better information on life expectancy to be shared. How would this impact on our decision making?

Life expectancy is increasing across the world and the latest set of figures from the Office for National Statistics show that in the UK it has passed 79 for boys born in 2010–12, and 82 for girls born then. In fact the prediction is that over a third of babies born in 2013 will live to more than 100. The data throws up some interesting questions. How well prepared are we for lives that last this long? And how evenly distributed is this increase in life expectancy? Pensions’ minister, Steve Webb, has called for better information on life expectancy to be shared. How would this impact on our decision making? But while we can look forward to longer life, for the government, it presents some challenges The first is that we just don’t save enough for our old age. This seems to be partly because we find it hard to make decisions that will have an impact so far in the future. There are a number of measures that have been put in place to encourage us to save more, including auto-enrolment into company pension schemes. This is being rolled out across businesses over the next three years. In the 2014 Budget, the Chancellor announced that people reaching retirement age will be able to draw all their pension as a cash lump sum, rather than having to take it as a regular income.

But while we can look forward to longer life, for the government, it presents some challenges The first is that we just don’t save enough for our old age. This seems to be partly because we find it hard to make decisions that will have an impact so far in the future. There are a number of measures that have been put in place to encourage us to save more, including auto-enrolment into company pension schemes. This is being rolled out across businesses over the next three years. In the 2014 Budget, the Chancellor announced that people reaching retirement age will be able to draw all their pension as a cash lump sum, rather than having to take it as a regular income.