In December 2015, countries from around the world met in Paris at the United Nations Intergovernmental Panel on Climate Change (IPCC). The key element of the resulting Paris Agreement was to keep ‘global temperature rise this century well below 2 degrees Celsius above pre-industrial levels and to pursue efforts to limit the temperature increase even further to 1.5 degrees Celsius.’ At the same time it was agreed that the IPCC would conduct an analysis of what would need to be done to limit global warming to 1.5°C. The IPPC has just published its report.

The report, based on more than 6000 scientific studies, has been compiled by more than 80 of the world’s top climate scientists. It states that, with no additional action to mitigate climate change beyond that committed in the Paris Agreement, global temperatures are likely to rise to the 1.5°C point somewhere between 2030 and 2040 and then continue rising above that, reaching 3°C by the end of the century.

According to the report, the effects we are already seeing will accelerate. Sea levels will rise as land ice caps and glaciers melt, threatening low lying coastal areas; droughts and floods will become more severe; hurricanes and cyclones will become stronger; the habits of many animals will become degraded and species will become extinct; more coral reefs will die and fish species disappear; more land will become uninhabitable; more displacement and migration will take place, leading to political tensions and worse.

Two tragedies

The problem of greenhouse gas emissions and global warming is a classic case of the tragedy of the commons. This is where people overuse common resources, such as open grazing land, fishing grounds, or, in this case, the atmosphere as a dump for emissions. They do so because there is little, if any, direct short-term cost to themselves. Instead, the bulk of the cost is borne by others – especially in the future.

There is another related tragedy, which has been dubbed the ‘tragedy of incumbents’. This is a political problem where people in power want to retain that power and do so by appealing to short-term selfish interests. The Trump administration lauds the use of energy as helping to drive the US economy and make people better off. To paraphrase Donald Trump ‘Climate change may be happening, but, hey, let’s not beat ourselves up about it and wear hair shirts. What we do will have little or no effect compared with what’s happening in China and India. The USA is much better off with a strong automobile, oil and power sector.’

What’s to be done?

According to the IPCC report, if warming is not to exceed 1.5℃, greenhouse gas emissions must be reduced by 45% by 2030 and by 100% by around 2050. But is this achievable?

The commitments made in the Paris Agreement will not be nearly enough to achieve these reductions. There needs to be a massive movement away from fossil fuels, with between 70% and 85% of global electricity production being from renewables by 2050. There needs to be huge investment in green technology for power generation, transport and industrial production.

Both these types of policies involve governments taking action, whether through increased carbon taxes on either producers or consumer or both, or through increased subsidies for renewables and other alternatives, or through the use of cap and trade with emissions allocations (either given by government or sold at auction) and carbon trading, or through the use of regulation to prohibit or limit behaviour that leads to emissions. The issue, of course, is whether governments have the will to do anything. Some governments do, but with the election of populist leaders, such as President Trump in the USA, and probably Jair Bolsonaro in Brazil, and with sceptical governments in other countries, such as Australia, this puts even more onus on other governments.

Another avenue is a change in people’s attitudes, which may be influenced by education, governments, pressure groups, news media, etc. For example, if people could be persuaded to eat less meat, drive less (for example, by taking public transport, walking, cycling, car sharing or living nearer to their work), go on fewer holidays, heat their houses less, move to smaller homes, install better insulation, etc., these would all reduce greenhouse gas emissions.

Finally, there is the hope that the market may provide part of the solution. The cost of generating electricity from renewables is coming down and is becoming increasingly competitive with electricity generated from fossil fuels. Electric cars are coming down in price as battery technology develops; also, battery capacity is increasing and recharging is becoming quicker, helping encourage the switch from petrol and diesel cars to electric and hybrid cars. At the same time, various industrial processes are becoming more fuel efficient. But these developments, although helpful, will not be enough to achieve the 1.5°C target on their own.

Intergovernmental Panel on Climate Change (IPCC) (8/10/18)

Questions

Explain the extent to which the problem of global warming is an example of the tragedy of the commons. What other examples are there of the tragedy?

Explain the meaning of the tragedy of the incumbents and its impact on climate change? Does the length of the electoral cycle exacerbate the problem?

With the costs of low or zero carbon technology for energy and transport coming down, is there as case for doing nothing in response to the problem of global warming?

Examine the case for and against using taxes and subsidies to tackle global warming.

Examine the case for and against using regulation to tackle global warming.

Examine the case for and against using cap-and-trade systems to tackle global warming.

Is there a prisoners’ dilemma problem in getting governments to adopt policies to tackle climate change?

What would be the motivation for individuals to ‘do their bit’ to tackle climate change? Other than altering prices or using regulation, how might the government or other agencies set about persuading people to ‘be more green’?

If you were doing a cost–benefit analysis of some project that will have beneficial environmental impacts in the future, how would you set about adjusting the values of these benefits for the fact that they occur in the future and not now?

In the last few years there have been growing concerns (see here for example) that markets in the USA are becoming increasingly dominated by a small number of firms. It is feared that the result of this will be a reduction in competition. Consistent with this, evidence suggests that the profits these firms make have increased. Last month The Economist and the Resolution Foundation published evidence (see references below) suggesting a similar picture may be emerging in Britain.

The Economist divided the British economy into 600 sub-sectors and found that in 58% of these the share of total revenue accruing to the 4 biggest firms had increased since 2008. The Resolution Foundation found a similar picture, especially in manufacturing industries where from 2004-16 the top five firms’ share of total revenue increased by over 10%.

Economic theory would suggest that as markets become more concentrated prices are likely to rise and The Economist cites research showing that mark-ups charged by firms in Britain have indeed risen. In addition to consumers facing higher prices, there is also concern that the lack of competition both in the USA and the UK is leading to lower wages being paid to workers. On the other hand, unlike in the USA, the evidence from the UK does not so far suggest there has also been an increase in corporate profits. Instead, it appears that the more successful firms’ profits have increased at the expense of their rivals.

This evidence on profits is line with a number of arguments that suggest we should perhaps be less concerned when markets are dominated by a small number of firms. Large firms may benefit from economies of scale and, being sufficiently large may be necessary for firms to innovate in new products and processes. Furthermore, high market shares may result from the competitive process as a reward for a firm developing a unique product or being more efficient than its rivals.

The Economist cites the supermarket industry as an example where concentrated is high, but competition is intense. Interestingly, this is a market where the British competition authorities have previously been concerned about the level of competition and spent considerable amounts of time investigating.

Despite these two opposing viewpoints, overall, The Economist argues strongly that we should be concerned about the situation in Britain. Not only are prices too high and wages too low, but growth in productivity is slow, even for the leading firms. Furthermore, they make clear that the situation may worsen following Brexit. It is argued that:

leaving the EU’s single market and customs union would reduce trade, easing competitive pressure from abroad.

This is consistent with evidence that joining the EC in the mid 1970s increased foreign competition in the UK and helped to end the low productivity growth that had plagued the economy since the 1930s.

Furthermore, it is suggested that:

to attract investment the government might look more favourably on proposed mergers—and loosening regulations would be easier outside the EU’s competition regime.

Therefore, it is clear that in the future there will be a vital role for the UK’s competition authority to remain independent of political objectives and aim to promote competition. In particular, they must prevent mergers that raise concentration and harm competition and intervene if they believe firms are abusing their dominant positions. Of course, following Brexit the case load of the competition authority in the UK will increase dramatically as they have to take on cases previously dealt with by the European Commission. One estimate is that it will need to look at around 40% more merger cases. It will certainly be interesting to see how competition in markets in Britain evolves over the next few years and the role competition policy plays in regulating this process.

Last week was a rough week for Britain. The “Beast from the East” and storm Emma swept through the country, bringing with them unusually heavy snowfall, which resulted in severe disruption across nearly all parts of the country. Some recent estimates put the cost of these extreme weather conditions at up to £1 billion per day. The construction industry suffering the biggest hit as work came to a halt for the best part of the week. Losses for the industry were estimated to be up to £2 billion.

Closed restaurants, empty shops and severely disrupted transport networks were all part of the effect that this extreme weather had on the overall economy. According to Howard Archer, chief economic adviser of the EY ITEM Club (a UK forecasting group):

It is possible that the severe weather [of the last few days] could lead to GDP growth being reduced by 0.1 percentage point in Q1 2018 and possibly 0.2 percentage points if the severe weather persist.

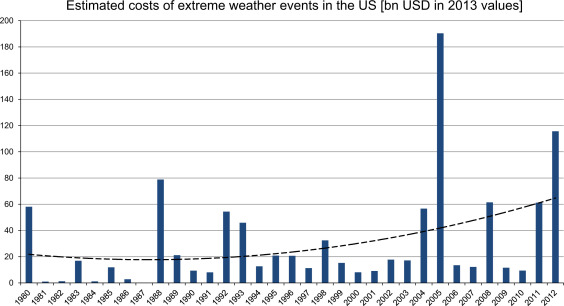

Source: Jahn (2015), Figure 2

As the occurrence of freak weather increases across the globe due to climate change, so does the economic cost of these events. The figure above shows the estimated costs of extreme weather events in the USA between 1980 and 2012 and it is reproduced from Jahn (see link below), who also fits a quadratic trend to show that these costs have been increasing over time. He goes on to characterise the impact of different types of extreme weather (including cold waves, heat waves, storms and others) on different sectors of the local economy – ranging from tourism and agriculture, to housing and the insurance sector.

Linnenluecke et al (linked below) argue that extreme weather caused by climate change could influence the decision of firms on where to locate and could lead to a reshuffle of economic activity across the world and have important policy implications. As the authors explain:

Climate change-related relocation has been given consideration in policy-oriented discussions, but not in management decisions. The effects of climate change and extreme weather events have been considered as peripheral or as a risk factor, but not as a determining factor in firm relocation processes…. This paper therefore [provides] insights for understanding how firms can enhance strategic decision-making in light of understanding and assessing their vulnerability as well as likely impacts that climate change may have on relocation decisions.

The likelihood and associated costs of extreme weather events could therefore become an increasingly important matter for discussion amongst economists and policy makers. Such weather events are likely to have profound economic implications for the world.

On 15 January 2018, Carillion went into liquidation. It was a major construction, civil engineering and facilities management company in the UK and was involved in a large number of public- and private-sector projects. Many of these were as a partner in a joint venture with other companies.

It was the second largest supplier of construction and maintenance services to Network Rail, including HS2. It was also involved in the building of hospitals, including the new Royal Liverpool University Hospital and Midland Metropolitan Hospital in Smethwick. It also provided maintenance, cleaning and catering services for many schools, universities, hospitals, prisons, government departments and local authorities. In addition it was involved in many private-sector projects.

Much of the work on the projects awarded to Carillion was then outsourced to other companies, many of which are small construction, maintenance, equipment and service companies. A large number of these may themselves be forced to close as projects cease and many bills remain unpaid.

Many of the public-sector projects in which Carillion was involved were awarded under the Public Finance Initiative (PFI). Under the scheme, the government or local authority decides the service it requires, and then seeks tenders from the private sector for designing, building, financing and running projects to provide these services. The capital costs are borne by the private sector, but then, if the provision of the service is not self-financing, the public sector pays the private firm for providing it. Thus, instead of the public sector being an owner of assets and provider or services, it is merely an enabler, buying services from the private sector. The system is known as a Public Private Partnership.

Clearly, there are immediate benefits to the public finances from using private, rather than public, funds to finance a project. Later, however, there is potentially an extra burden of having to buy the services from the private provider at a price that includes an element for profit. What is hoped is that the costs to the taxpayer of these profits will be more than offset by gains in efficiency.

Critics, however, claim that PFI projects have resulted in poorer quality of provision and that cost control has often been inadequate, resulting in a higher burden for the taxpayer in the long term. What is more, many of the projects have turned out to be highly profitable, suggesting that the terms of the original contracts were too lax.

There was some modification to the PFI process in 2012 with the launching of the government’s modified PFI scheme, dubbed PF2. Most of the changes were relatively minor, but the government would act as a minority public equity co-investor in PF2 projects, with the public sector taking stakes of up to 49 per cent in individual private finance projects and appointing a director to the boards of each project. This, it was hoped, would give the government greater oversight of projects.

With the demise of Carillion, there has been considerable debate over outsourcing by the government to the private sector and of PFI in particular. Is PFI the best model for funding public-sector investment and the running of services in the public sector?

On 18 January 2018, the National Audit Office published an assessment of PFI and PF2. The report stated that there are currently 716 PFI and PF2 projects either under construction or in operation, with a total capital value of £59.4 billion. In recent years, however, ‘the government’s use of the PFI and PF2 models has slowed significantly, reducing from, on average, 55 deals each year in the five years to 2007-08 to only one in 2016-17.’

Should the government have closer oversight of private providers? The government has been criticised for not heeding profit warnings by Carillion and continuing to award it contracts.

Should the whole system of outsourcing and PFI be rethought? Should more construction and services be brought ‘in-house’ and directly provided by the public-sector organisation, or at least managed directly by it with a direct relationship with private-sector providers? The articles below consider these issues.

Why did Carillion go into liquidation? Could this have been foreseen?

Identify the projects in which Carillion has been involved.

What has the government proposed to deal with the problems created by Carillion’s liquidation?

What are the advantages and disadvantages of the Private Finance Initiative?

Why have the number and value of new PFI projects declined significantly in recent years?

How might PFI projects be tightened up so as to retain the benefits and minimise the disadvantages of the system?

Why have PFI cost reductions proved difficult to achieve? (See paragraphs 2.7 to 2.17 in the National Audit Office report.)

How would you assess whether PFI deals represent value for money?

What are the arguments for and against public-sector organisations providing services, such as cleaning and catering, directly themselves rather than outsourcing them to private-sector companies?

Does outsourcing reduce risks for the public-sector organisation involved?

The linked articles below look at the state of the railways in Britain and whether renationalisation would be the best way of securing more investment, better services and lower fares.

Rail travel and rail freight involve significant positive externalities, as people and goods transported by rail reduce road congestion, accidents and traffic pollution. In a purely private rail system with no government support, these externalities would not be taken into account and there would be a socially sub-optimal use of the railways. If all government support for the railways were withdrawn, this would almost certainly result in rail closures, as was the case in the 1960s, following the publication of the Beeching Report in 1963.

Also the returns on rail investment are generally long term. Such investment may not, therefore, be attractive to private rail operators seeking shorter-term returns.

These are strong arguments for government intervention to support the railways. But there is considerable disagreement over the best means of doing so.

One option is full nationalisation. This would include both the infrastructure (track, signalling, stations, bridges, tunnels and marshalling yards) and the trains (the trains themselves – both passenger and freight – and their operation).

At present, the infrastructure (except for most stations) is owned, operated, developed and maintained by Network Rail, which is a non-departmental public company (NDPB) or ‘Quango’ (Quasi-autonomous non-governmental organisation, such as NHS trusts, the Forestry Commission or the Office for Students. It has no shareholders and reinvests its profits in the rail infrastructure. Like other NDPBs, it has an arm’s-length relationship with the government. Network Rail is answerable to the government via the Department for Transport. This part of the system, therefore, is nationalised – if the term ‘nationalised organisations’ includes NDPBs and not just full public corporations such as the BBC, the Bank of England and Post Office Ltd.

Train operating companies, however, except in Northern Ireland, are privately owned under a franchise system, with each franchise covering specific routes. Each of the 17 passenger franchises is awarded under a competitive tendering system for a specific period of time, typically seven years, but with some for longer. Some companies operate more than one franchise.

Companies awarded a profitable franchise are required to pay the government for operating it. Companies awarded a loss-making franchise are given subsidies by the government to operate it. In awarding franchises, the government looks at the level of payments the bidders are offering or the subsidies they are requiring.

But this system has come in for increasing criticism, with rising real fares, overcrowding on many trains and poor service quality. The Labour Party is committed to taking franchises into public ownership as they come up for renewal. Indeed, there is considerable public support for nationalising the train operating companies.

The main issue is which system would best address the issues of externalities, efficiency, quality of service, fares and investment. Ultimately it depends on the will of the government. Under either system the government plays a major part in determining the level of financial support, operating criteria and the level of investment. For this reason, many argue that the system of ownership is less important than the level and type of support given by the government and how it requires the railways to be run.

What categories of market failure would exist in a purely private rail system with no government intervention?

What types of savings could be made by nationalising train operating companies?

The franchise system is one of contestable monopolies. In what ways are they contestable and what benefits does the system bring? Are there any costs from the contestable nature of the system?

Is it feasible to have franchises that allow more than one train operator to run on most routes, thereby providing some degree of continuing competition?

How are rail fares determined in Britain?

Would nationalising the train operating companies be costly to the taxpayer? Explain.

What determines the optimal length of a franchise under the current system?

What role does leasing play in investment in rolling stock?

What are the arguments for and against the government’s decision in November 2017 to allow the Virgin/Stagecoach partnership to pull out of the East Coast franchise three years early because it found the agreed payments to the government too onerous?

Could the current system be amended in any way to meet the criticisms that it does not adequately take into account the positive externalities of rail transport and the need for substantial investment, while also encouraging excessive risk taking by bidding companies at the tendering stage?

In December 2015, countries from around the world met in Paris at the United Nations Intergovernmental Panel on Climate Change (IPCC). The key element of the resulting Paris Agreement was to keep ‘global temperature rise this century well below 2 degrees Celsius above pre-industrial levels and to pursue efforts to limit the temperature increase even further to 1.5 degrees Celsius.’ At the same time it was agreed that the IPCC would conduct an analysis of what would need to be done to limit global warming to 1.5°C. The IPPC has just published its report.

In December 2015, countries from around the world met in Paris at the United Nations Intergovernmental Panel on Climate Change (IPCC). The key element of the resulting Paris Agreement was to keep ‘global temperature rise this century well below 2 degrees Celsius above pre-industrial levels and to pursue efforts to limit the temperature increase even further to 1.5 degrees Celsius.’ At the same time it was agreed that the IPCC would conduct an analysis of what would need to be done to limit global warming to 1.5°C. The IPPC has just published its report. According to the report, the effects we are already seeing will accelerate. Sea levels will rise as land ice caps and glaciers melt, threatening low lying coastal areas; droughts and floods will become more severe; hurricanes and cyclones will become stronger; the habits of many animals will become degraded and species will become extinct; more coral reefs will die and fish species disappear; more land will become uninhabitable; more displacement and migration will take place, leading to political tensions and worse.

According to the report, the effects we are already seeing will accelerate. Sea levels will rise as land ice caps and glaciers melt, threatening low lying coastal areas; droughts and floods will become more severe; hurricanes and cyclones will become stronger; the habits of many animals will become degraded and species will become extinct; more coral reefs will die and fish species disappear; more land will become uninhabitable; more displacement and migration will take place, leading to political tensions and worse.

want to retain that power and do so by appealing to short-term selfish interests. The Trump administration lauds the use of energy as helping to drive the US economy and make people better off. To paraphrase Donald Trump ‘Climate change may be happening, but, hey, let’s not beat ourselves up about it and wear hair shirts. What we do will have little or no effect compared with what’s happening in China and India. The USA is much better off with a strong automobile, oil and power sector.’

want to retain that power and do so by appealing to short-term selfish interests. The Trump administration lauds the use of energy as helping to drive the US economy and make people better off. To paraphrase Donald Trump ‘Climate change may be happening, but, hey, let’s not beat ourselves up about it and wear hair shirts. What we do will have little or no effect compared with what’s happening in China and India. The USA is much better off with a strong automobile, oil and power sector.’ The commitments made in the Paris Agreement will not be nearly enough to achieve these reductions. There needs to be a massive movement away from fossil fuels, with between 70% and 85% of global electricity production being from renewables by 2050. There needs to be huge investment in green technology for power generation, transport and industrial production.

The commitments made in the Paris Agreement will not be nearly enough to achieve these reductions. There needs to be a massive movement away from fossil fuels, with between 70% and 85% of global electricity production being from renewables by 2050. There needs to be huge investment in green technology for power generation, transport and industrial production. Finally, there is the hope that the market may provide part of the solution. The cost of generating electricity from renewables is coming down and is becoming increasingly competitive with electricity generated from fossil fuels. Electric cars are coming down in price as battery technology develops; also, battery capacity is increasing and recharging is becoming quicker, helping encourage the switch from petrol and diesel cars to electric and hybrid cars. At the same time, various industrial processes are becoming more fuel efficient. But these developments, although helpful, will not be enough to achieve the 1.5°C target on their own.

Finally, there is the hope that the market may provide part of the solution. The cost of generating electricity from renewables is coming down and is becoming increasingly competitive with electricity generated from fossil fuels. Electric cars are coming down in price as battery technology develops; also, battery capacity is increasing and recharging is becoming quicker, helping encourage the switch from petrol and diesel cars to electric and hybrid cars. At the same time, various industrial processes are becoming more fuel efficient. But these developments, although helpful, will not be enough to achieve the 1.5°C target on their own. IPCC climate change report

IPCC climate change report In the last few years there have been growing concerns (see

In the last few years there have been growing concerns (see