Much of the east coast of England is subject to tidal flooding. One such area is the coastline around the Wash, the huge bay between Norfolk and Lincolnshire. Most of the vulnerable shorelines are protected by sea defences, usually in the form of concrete walls or earth embankments, traditionally paid for by the government. But part of the Norfolk shoreline is protected by shingle banks, which require annual maintenance.

Much of the east coast of England is subject to tidal flooding. One such area is the coastline around the Wash, the huge bay between Norfolk and Lincolnshire. Most of the vulnerable shorelines are protected by sea defences, usually in the form of concrete walls or earth embankments, traditionally paid for by the government. But part of the Norfolk shoreline is protected by shingle banks, which require annual maintenance.

Full government funding for maintaining these banks ended in 2013. According to new government rules, only projects that provide at least £8 of benefits for each £1 spent would qualify for such funding to continue. The area under question on the Norfolk cost of the Wash does not qualify.

Between 2013 and 2015 the work on the shingle banks is being paid for by the local council charging levies. After that, the plan is for a partnership-funding approach, where the government will make a (small) contribution as long as the bulk of the funding comes from the local community. This will involve setting up a ‘community interest company’, which will seek voluntary contributions from local residents, landowners and businesses.

Sea defences are a public good, in that it is difficult to exclude people benefiting who choose not to pay. In other words, there is a ‘free rider’ problem. However, in the case of the Wash shoreline in question, one borough councillor, Brian Long, argues that it might be possible to maintain the flood defences to protect those who do contribute while ignoring those who do not.

Not surprisingly, many residents and businesses argue that the government ought to fund the defences and, if it does have to be financed locally, then everyone should be required to pay their fair share.

Radio podcast

Holding back the sea BBC Radio 4, David Shukman (19/11/14)

Holding back the sea BBC Radio 4, David Shukman (19/11/14)

Articles

What is the price of holding back the sea? BBC News, David Shukman (19/11/14)

Firms will have to pay towards cost of sea defences between Heacham and Wolferton in West Norfolk EDP24, Chris Bishop (1/8/14)

Businesses between Snettisham and Hunstanton will have to pay for flood defences. EDP24, Chris Bishop (19/11/14)

Wash and west Norfolk sea defence repairs now under way BBC News (13/12/13)

Consultation document

Managing our coastline Borough Council of King’s Lynn and West Norfolk, Environment Agency

Questions

- What are the two main features of a public good? Are sea defences a pure public good?

- Is there a moral hazard if people choose to live in a coastal area that would be subject to flooding without sea defences?

- Who is the ‘public’ in the case of sea defences? Is it the whole country, or the local authority or just all those being protected by the defences?

- What are the problems with relying on voluntary contributions to fund, or partly fund, sea defences? How could the free-rider problem be minimised in such a funding model?

- Discuss the possible interpretations of ‘equity’ when funding sea defences.

- If ‘flood defences could be built or maintained to protect those who do contribute while ignoring those who do not’, does this mean that such defences are not a public good?

- Find out how sea defences are funded in The Netherlands. Should such a funding model be adopted in the UK?

On my commute to work on the 6th October, I happened to listen to a programme on BBC radio 4, which provided some fascinating discussion on climate change, growth, capitalism and the need for co-operation. With more countries emerging as leading economic powers, pollution and emissions continue to grow. Is it time for a green revolution?

On my commute to work on the 6th October, I happened to listen to a programme on BBC radio 4, which provided some fascinating discussion on climate change, growth, capitalism and the need for co-operation. With more countries emerging as leading economic powers, pollution and emissions continue to grow. Is it time for a green revolution?

The programme considers some ‘typical’ policies and also discusses some radical solutions. There is discussion on developing and developed nations and how these countries should be looked at in terms of compensation, entitlement and aid. Carrots and sticks are analysed as means of saving the planet and how environmental damage can be reduced, without adversely affecting the growth rate of the world economy. I won’t say any more, but it’s certainly worth listening to, for an interesting discussion on one of the biggest problems that governments across the world are facing and it is not going to go away any time soon.

Naomi Klein on climate change and growth BBC Radio 4, Start the Week (6/10/14)

Questions

- What are the market failures with the environment?

- Why is global co-operation so important for tackling the problem of climate change?

- Which policies are discussed as potential solutions to the problem of climate change?

- What has been the problem with the European carbon trading scheme?

- Why may there be a trade-off between capitalism, growth and the problem of carbon emissions?

- To what extent do you think that countries such as Bangladesh should be ‘compensated’?

The Office for National Statistics (ONS) reported that the quantity of retail sales in the UK was 3.9% higher in August than it had been in July. However strong price competition meant that the value of these sales increased by only 0.4%. What were the key factors driving the big increase in the quantity of sales? Was it simply the response of consumers to falling prices?

The Office for National Statistics (ONS) reported that the quantity of retail sales in the UK was 3.9% higher in August than it had been in July. However strong price competition meant that the value of these sales increased by only 0.4%. What were the key factors driving the big increase in the quantity of sales? Was it simply the response of consumers to falling prices?

The data indicated that there was strong demand for goods associated with the housing market such as carpets, fridges and cookers. Spending on furniture increased very rapidly with sales rising by 24% over a 12 month period. Flat packed furniture proved to be particularly popular with consumers.

There was also strong demand for electrical goods and more specifically vacuum cleaners. The ONS estimated that a boom in the sale of vacuum cleaners in August was responsible for 25% of the increase in retail sales.

Why did the sales of vacuum cleaners increase so rapidly in August? Did UK households suddenly decide to keep their houses cleaner? The sales data shows that certain types of vacuum cleaners sold in much larger numbers than others.

For example, Tesco reported a 44% increase in the sales of 2,000 watt vacuum cleaners in the last two weeks in August while the Co-op reported an increase of 38%. Referring to the last weekend in August, the head of small domestic appliances at the on-line retailer ao.com stated that

We saw a huge surge in sales of corded vacuums over 1,600 watts over the weekend, with sales quadrupling.

There were also reports that a significant number of customers were buying more than one vacuum cleaner with these larger motors.

The key reason for the sudden surge in demand was the implementation of new regulations by the European Union as part of its energy efficiency directive. The ultimate objective of this directive is to reduce climate change. The specific policy that appears to have had such a big impact on consumers in the UK was the ban imposed on firms in the EU from making or importing vacuum cleaners that have motors above 1600 watts. This ban came into effect on the 1st September 2014.

A spokesperson for the consumer group Which? stated in August that

If you’re in the market for a powerful vacuum, you should act quickly, before all the models currently sell out. A Best Buy 2,200-watt vacuum costs around £27 a year to run in electricity – only around £8 more than the best scoring 1,600-watt we’ve tested.

The EU plans to reduce the maximum permitted wattage in vacuum cleaners to 900 watts in 2017. Restrictions have already been imposed on bigger electrical appliances such as televisions, washing machines and refrigerators. The EUs Ecodesign directive may also be extended to a range of smaller electrical appliances such as toasters and hair dressers in the future. It’ll be interesting to see if consumers respond in the same way to regulations imposed by the EU in the future.

Ten days left to vacuum up a powerful cleaner BBC (21/08/14)

Housing boom, food discounting and vacuum ban boost UK spending The Guardian, Larry Elliott, Phillip Inman, Lisa Bachelor (18/9/14)

UK retail sales boosted by vacuum cleaner sales BBC (18/9/14)

Retailers sell out of vacuum cleaners ahead of EU ban The Telegraph, Elliot Pinkham (30/8/14)

Power surge! Fourfold rise in sales of super vacuums: Some customers buying two or more models to beat new EU regulations Daily Mail, Andrew Levy (1/9/14)

Energy Efficiency Directive European Commission (accessed on 24/9/14)

Vacuum cleaner splurge pushes up UK retail sales The Guardian, Phillip Inman (18/9/14)

Questions

- Using a demand and supply diagram, illustrate what has happened in the market for high wattage vacuum cleaners in August. Pay particular attention in your answer to the role of expectations.

- What did your previous diagram predict would happen to the price of high wattage vacuum cleaners in August? Did this in fact happen?

- A fully informed rational consumer may purchase a higher wattage vacuum cleaner if they consider that the improvement in cleaning performance is greater than the extra cost of purchasing and using the cleaner. Can you provide an economic rationale for banning the sale of these machines in these circumstances?

- Using a demand and supply diagram illustrate the impact of banning the sale of a product in a competitive market.

Every year thousands of entrepreneurs will have another great idea that is sure to take off and bring in millions of customers. However, most of these great ideas will turn into another business failure. But, in the case of Dropbox, it is multiple business failures that eventually created a huge success, giving hope to millions of budding entrepreneurs.

Every year thousands of entrepreneurs will have another great idea that is sure to take off and bring in millions of customers. However, most of these great ideas will turn into another business failure. But, in the case of Dropbox, it is multiple business failures that eventually created a huge success, giving hope to millions of budding entrepreneurs.

With 300 million users, the file sharing ‘Dropbox’ is certainly a success, estimated at a value of $10bn. But it didn’t happen immediately and was preceded by a few failures. So, what is the secret to success in this case? The co-founder of Dropbox, Drew Houston, said that it is all about providing something that customers want. In the case of Dropbox, customers are crucial: the more people use it, the easier it becomes for others to use it too, as it allows file sharing on a much larger scale. Perhaps here we have a case of network externalities.

With Dropbox people would tell their friends about it and collaborate. So when you go into work and work on a project with colleagues you recruit them in essence to become Dropbox users because you’re all working on a project together.

No doubt there are many other examples of businesses that have proved a success after several failed attempts. Providing customers with what they want, at the time when they need it is clearly a key ingredient, but so, it appears, is business failure. The following article from BBC News considers the rise of Dropbox.

Dropbox and the failures behind it BBC News, Richard Taylor (1/7/14)

Questions

- Customers are clearly crucial for any business to succeed. How can a new entrepreneur find out if there is a demand?

- Why was timing so important in the case of Dropbox?

- Given that customers can actually use Dropbox for free, how does this company make so much money?

- What are network externalities? Explain them in the context of Dropbox.

- Drew Houston says that ‘distribution’ is another key ingredient to success. What do you think is meant by this and how will it help create success?

Life expectancy is increasing across the world and the latest set of figures from the Office for National Statistics show that in the UK it has passed 79 for boys born in 2010–12, and 82 for girls born then. In fact the prediction is that over a third of babies born in 2013 will live to more than 100. The data throws up some interesting questions. How well prepared are we for lives that last this long? And how evenly distributed is this increase in life expectancy? Pensions’ minister, Steve Webb, has called for better information on life expectancy to be shared. How would this impact on our decision making?

Life expectancy is increasing across the world and the latest set of figures from the Office for National Statistics show that in the UK it has passed 79 for boys born in 2010–12, and 82 for girls born then. In fact the prediction is that over a third of babies born in 2013 will live to more than 100. The data throws up some interesting questions. How well prepared are we for lives that last this long? And how evenly distributed is this increase in life expectancy? Pensions’ minister, Steve Webb, has called for better information on life expectancy to be shared. How would this impact on our decision making?

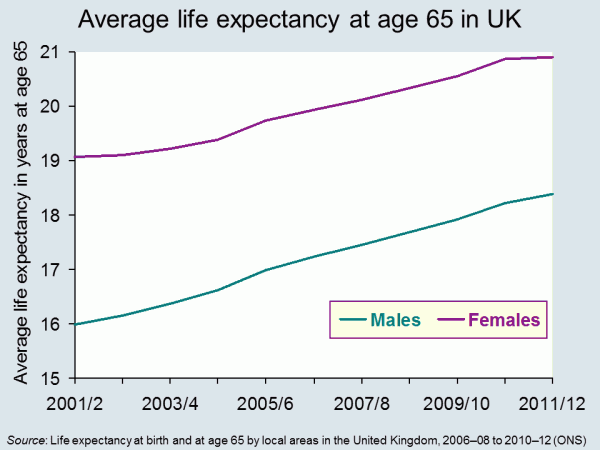

It seems reasonable to think that increasing life expectancy must be good news. And of course, for individuals it can be. In 1951 the average man retiring at 65, in England and Wales, could expect to live and draw a pension for another 12.1 years. By 2014 this had risen to 22 years.

But while we can look forward to longer life, for the government, it presents some challenges The first is that we just don’t save enough for our old age. This seems to be partly because we find it hard to make decisions that will have an impact so far in the future. There are a number of measures that have been put in place to encourage us to save more, including auto-enrolment into company pension schemes. This is being rolled out across businesses over the next three years. In the 2014 Budget, the Chancellor announced that people reaching retirement age will be able to draw all their pension as a cash lump sum, rather than having to take it as a regular income.

But while we can look forward to longer life, for the government, it presents some challenges The first is that we just don’t save enough for our old age. This seems to be partly because we find it hard to make decisions that will have an impact so far in the future. There are a number of measures that have been put in place to encourage us to save more, including auto-enrolment into company pension schemes. This is being rolled out across businesses over the next three years. In the 2014 Budget, the Chancellor announced that people reaching retirement age will be able to draw all their pension as a cash lump sum, rather than having to take it as a regular income.

Another concern for government is the variations that we find in life expectancy across the UK. The 2014 ONS data identified that life expectancy for men born in Glasgow in 2012 is 72.6, in East Dorset it is 82.9. 25% of those in Glasgow are not expected to live to 65. The gap in years of good health is even greater. This presents governments with a long-term problem. How do they achieve greater equality in this instance? Do they focus resources on the areas that need it most? Do they legislate to address behaviour? Or do they rely on the provision of good advice – on diet, exercise and other factors?

Information has a role to play in both areas identified above. In April 2014, Steve Webb, suggested that in order to make good decisions at the point of retirement, people need to understand more about what lies ahead. He said:

People tend to underestimate how long they’re likely to live, so we’re talking about averages, something very broad-brush. Based on your gender, based on your age, perhaps asking one or two basic questions, like whether you’ve smoked or not, you can tell somebody that they might, on average, live for another 20 years or so.

This suggestion has led to some concerns being expressed at what appears to be an over-simplistic approach. Estimates can only be based on a mix of averages modified by individual information. Would the projections be shared with pension providers? What would you do if you exceeded your forecast life expectancy – by a long way – and had spent all your money? Could you sue someone?

Will your pension pot last as long as you will? The Telegraph, Dan Hyde and Richard Dyson (23/4/2014)

Scientists invent death test that will tell us how long we have to live Metro (11/8/13)

Games host Glasgow has worst life expectancy in the UK The Guardian, Caroline Davies (16/4/2014)

Pensioners could get life expectancy guidance BBC News Politics (17/4/14)

ONS reveals gaps in life expectancy across the UK FT Adviser Pensions, Kevin White (23/4/14)

Health care aid for developing countries boosts life expectancy Health Canal, Ruth Ann Richter (22/4/14)

A third of babies born this year will live to 100 This is Money.co.uk, Adam Uren (11/12/13)

Questions

- Thinking about the UK, what are the factors that might explain variations in life expectancy across different regions? How might the government address these differences? Why would they want to do so?

- Do the same factors explain variations between countries? Who can address these differences? Who would want to do so?

- If you could have a reasonable prediction of your life expectancy at 65, would you want it? How would your behaviour change if you were predicted a longer than average life expectancy? How would it change if you were predicted a shorter than average life expectancy?

- If you could have an accurate prediction of your life expectancy at 18, how would your answers differ? If this were possible, would it present any problems?

Much of the east coast of England is subject to tidal flooding. One such area is the coastline around the Wash, the huge bay between Norfolk and Lincolnshire. Most of the vulnerable shorelines are protected by sea defences, usually in the form of concrete walls or earth embankments, traditionally paid for by the government. But part of the Norfolk shoreline is protected by shingle banks, which require annual maintenance.

Much of the east coast of England is subject to tidal flooding. One such area is the coastline around the Wash, the huge bay between Norfolk and Lincolnshire. Most of the vulnerable shorelines are protected by sea defences, usually in the form of concrete walls or earth embankments, traditionally paid for by the government. But part of the Norfolk shoreline is protected by shingle banks, which require annual maintenance.