Donald Trump has threatened to pull out of the World Trade Organization. ‘If they don’t shape up, I would withdraw from the WTO,’ he said. He argues that the USA is being treated very badly by the WTO and that the organisation needs to ‘change its ways’.

Historically, the USA has done relatively well compared with other countries in trade disputes brought to the WTO. However, President Trump does not like being bound by an international organisation which prohibits the unilateral imposition of tariffs that are not in direct retaliation against a trade violation by other countries. Such tariffs have been imposed by the Trump administration on steel and aluminium imports. This has led to retaliatory tariffs on US imports by the EU, China and Canada – something that is permitted under WTO rules.

Whether or not the USA does withdraw from the WTO, Trump’s threats bring into question the power of the WTO and other countries’ compliance with WTO rules. With the rise in protectionist sentiments around the world, the power of the WTO would seem to be on the wane.

Even if the USA does not withdraw from the WTO, it is succeeding in weakening the organisation. Appeals cases have to be heard by an ‘appellate body’, consisting of at least three judges drawn from a list of seven, each elected for four years. But the USA has the power to block new appointees – and has done so. As Larry Elliott states in the first article below:

The list of judges is already down to four and will be down to the minimum of three when the Mauritian member, Shree Baboo Chekitan Servansing, retires at the end of September. Two more members will go by the end of next year, at which point the appeals process will come to a halt.

This raises the question of the implication of a ‘no-deal’ Brexit – something that seems more likely as the UK struggles to reach a trade agreement with the EU. Leaving without a deal would mean ‘reverting to WTO rules’. But if these rules are being ignored by powerful countries such as the USA and possibly China, and if the appeals procedure has ground to a halt, this could leave the UK without the safety net of international trade rules. Outside the EU – the world’s most powerful trade bloc – the UK could find itself having to accept poor trade terms with the USA and other large countries.

The Economist is probably not the kind of newspaper that you will read more than once per issue – certainly not two years after its publication date. That is because, by definition, financial news articles are ephemeral: they have greater value, the more recent they are – especially in the modern financial world, where change can be strikingly fast. To my surprise, however, I found myself reading again an article on inequality that I had first read two years ago – and it is (of course) still relevant today.

The title of the article was ‘You may be higher in the global wealth pyramid than you think’ and it discusses exactly that: how much wealth does it take for someone to be considered ‘rich’? The answer to this question is of course, ‘it depends’. And it does depend on which group you compare yourself against. Although this may feel obvious, some of the statistics that are presented in this article may surprise you.

According to the article

If you had $2200 to your name (adding together your bank deposits, financial investments and property holdings, and subtracting your debts) you might not think yourself terribly fortunate. But you would be wealthier than half the world’s population, according to this year’s Global Wealth Report by the Crédit Suisse Research Institute. If you had $71 560 or more, you would be in the top tenth. If you were lucky enough to own over $744 400 you could count yourself a member of the global 1% that voters everywhere are rebelling against.

For many (including yours truly) these numbers may come as a surprise when you first see them. $2200 in today’s exchange rate is about £1640. And this is wealth, not income – including all earthly possessions (net of debt). £1640 of wealth is enough to put you ahead of half of the planet’s population. Have a $774 400 (£556 174 – about the average price of a two-bedroom flat in London) and – congratulations! You are part of the global richest 1% everyone is complaining about…

Such comparisons are certainly thought provoking. They show how unevenly wealth is distributed across countries. They also show that countries which are more open to trade are more likely to have benefited the most from it. Take a closer look at the statistics and you will realise that you are more likely to be rich (compared to the global average) if you live in one of these countries.

Of course, wealth inequality does not happen only across countries – it happens also within countries. You can own a two-bedroom flat in London (and be, therefore, part of the 1% global elite), but having to live on a very modest budget because your income (which is a flow variable, as opposed to wealth, which is a stock variable) has not grown fast enough in relation to other parts of the national population.

Would you be better off if there were less trade? Certainly not – you would probably be even poorer, as trade theories (and most of the empirical evidence I am aware of) assert. Why do we then talk so much about trade wars and trade restrictions recently? Why do we elect politicians who advocate such restrictions? It is probably easier to answer these questions using political than economic theory (although game theory may have some interesting insights to offer – have you heard of the ‘Chicken game‘?). But as I am neither political scientists nor a game theorist, I will just continue to wonder about it.

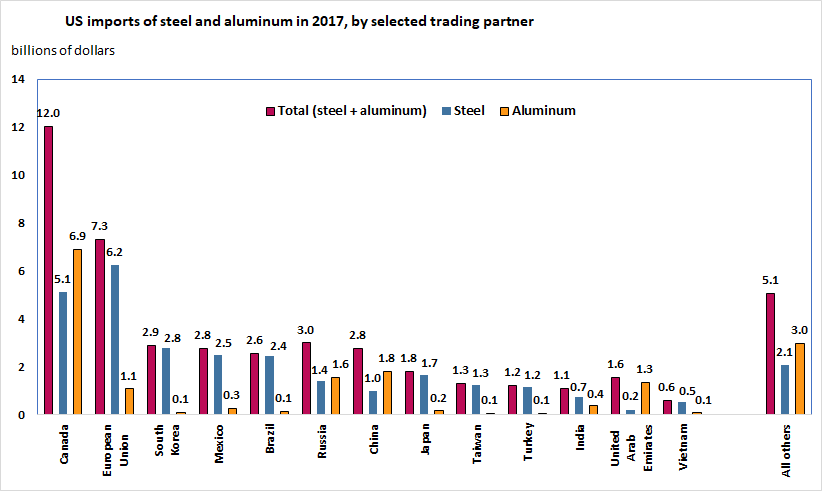

The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

Source: Bown (2018), Figure 1

A number of economists and policymakers are worried that such policies restrict trade and are likely to provoke retaliation by the affected trade partners. In recent statements, the EU has pledged to take counter-measures if the bloc is affected by these policies. In a recent press conference, the Commissioner for Trade, Cecilia Malmstrom, stated that:

We have made it clear that a move that hurts the EU and puts thousands of European jobs in jeopardy will be met with a firm and proportionate response.

She added that, ‘I truly hope that this will not happen. A trade war has no winners.’

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.

A number of studies have attempted to estimate the effect of trade restrictions and tariff wars on welfare: see for instance Anderson and Wincoop (2001), Syropoulos (2002), Fellbermayr et al. (2013). The results vary widely, depending on the case. However, there seems to be consensus that the more similar (in terms of size and industry composition) the adversaries are, the more mutually damaging a trade war is likely to be (and, therefore, less likely to happen).

As Miyagiwa et al (2016, p43) explain:

A country initiates contingent protection policy against a trading partner only if the latter has a considerably smaller domestic market than its own, while avoiding confrontation with a country having a substantially larger domestic market than its own.

As both Canada and the EU are very large advanced market economies, it remains to be seen how much risk (and potential damage to the local and global economy) US trade policymakers are willing to take.

With the Conservatives having lost their majority in Parliament in the recent UK election, there is renewed discussion of the form that Brexit might take. EU states are members of the single market and the customs union. A ‘hard Brexit’ involves leaving both and this was the government’s stance prior to the election. But there is now talk of a softer Brexit, which might mean retaining membership of the single market and/or customs union.

The single market

Belonging to the single market means accepting the free movement of goods, services, capital and labour. It also involves tariff-free trade within the single market and adopting a common set of rules and regulations over trade, product standards, safety, packaging, etc., with disputes settled by the European Court of Justice. Membership of the single market involves paying budgetary contributions. Norway and Iceland are members of the single market.

The single market brings huge benefits from free trade with no administrative barriers from customs checks and paperwork. But it would probably prove impossible to negotiate remaining in the single market with an opt out on free movement of labour. Controlling immigration from EU countries was a key part of the Leave campaign.

The customs union

This involves all EU countries adopting the same tariffs (customs duties) on imports from outside the EU. These tariffs are negotiated by the European Commission with non-EU countries on a country-by-country basis. Goods imported from outside the EU are charged tariffs in the country of import and can then be sold freely around the EU with no further tariffs.

Remaining a member of the customs union would allow the UK to continue trading freely in the EU, subject to meeting various non-tariff regulations. It would also allow free ‘borderless’ trade between Northern Ireland and the Republic of Ireland. However, being a member of the customs union would prevent the UK from negotiating separate trade deals with non-EU countries. The ability to negotiate such deals has been argued to be one of the main benefits of leaving the EU.

Free(r) trade area

The UK could negotiate a trade deal with the EU. But it is highly unlikely that such a deal could be in place by March 2019, the date when the UK is scheduled to leave the EU. At that point, trade barriers would be imposed, including between the two parts of the island of Ireland. Such deals are very complex, especially in the area of services, which are the largest category of UK exports. Negotiating tariff-free or reduced-tariff trade is only a small part of the problem; the biggest part involves negotiating product standards, regulations and other non-tariff barriers.

All the above options thus involve serious problems and the government will be pushed from various sides, not least within the Conservative Party, for different degrees of ‘softness’ or ‘hardness’ of Brexit. What is more, the pressure from business for free trade with the EU is likely to grow. Brexit may mean Brexit, but just what form it will take is very unclear.

Explain the trading agreement between Norway and the EU.

How does the Norwegian arrangement with the EU differ from the Turkish one?

What are meant by the terms ‘hard Brexit’ and ‘soft Brexit’?

How does a customs union differ from a free trade area?

Is it possible to have (a) a customs union without a single market; (b) a single market without a customs union?

To what extent is it in the EU’s interests to negotiate a deal with the UK which lets it maintain access to the customs union without having free movement of labour?

The EU insists that talks about future trading arrangements between the UK and the EU can take place only after sufficient progress has been made on the terms of the ‘divorce’. What elements are included in the divorce terms?

If agreement is not reached by 29 March 2019, what happens and what would be the consequences?

Will a hung parliament, or at least a government supported by the DUP on a confidence and supply basis, make it more or less likely that there will be a hard Brexit?

For what reasons may the EU favour (a) a hard Brexit; (b) a soft Brexit?

In the light of the Brexit vote and the government’s position that the UK will leave the single market and customs union, there has been much discussion of the need for the UK to achieve trade deals. Indeed, a UK-US trade deal was one of the key issues on Theresa May’s agenda when she met Donald Trump just a week after his inauguration.

But what forms can a trade deal take? What does achieving one entail? What are likely to be the various effects on different industries – who will be the winners and losers? And what role does comparative advantage play? The articles below examine these questions.

Given that up until Brexit, the UK already has free trade with the rest of the EU, there is a lot to lose if barriers are erected when the UK leaves. In the meantime, it is vital to start negotiating new trade deals, a process that can be extremely difficult and time-consuming.

A far as new trade arrangements with the EU are concerned, these cannot be agreed until after the UK leaves the EU, in approximately two years’ time, although the government is keen that preliminary discussions take place as soon as Article 50 is triggered, which the government plans to do by the end of March.

What elements would be included in a UK-US trade deal?

Explain the gains from trade that can result from exploiting comparative advantage.

Explain the statement in the article that allowing trade to be determined by comparative advantage is ‘often politically unacceptable, as governments generally look to protect jobs and tax revenues, as well as to protect activities that fund innovation’.

Why is it difficult to work out in advance the likely effects on trade of a trade deal?

What would be the benefits and costs to the UK of allowing all countries’ imports into the UK tariff free?

What are meant by ‘trade creation’ and ‘trade diversion’? What determines the extent to which a trade deal will result in trade creation or trade diversion?

Donald Trump has threatened to pull out of the World Trade Organization. ‘If they don’t shape up, I would withdraw from the WTO,’ he said. He argues that the USA is being treated very badly by the WTO and that the organisation needs to ‘change its ways’.

Donald Trump has threatened to pull out of the World Trade Organization. ‘If they don’t shape up, I would withdraw from the WTO,’ he said. He argues that the USA is being treated very badly by the WTO and that the organisation needs to ‘change its ways’. Whether or not the USA does withdraw from the WTO, Trump’s threats bring into question the power of the WTO and other countries’ compliance with WTO rules. With the rise in protectionist sentiments around the world, the power of the WTO would seem to be on the wane.

Whether or not the USA does withdraw from the WTO, Trump’s threats bring into question the power of the WTO and other countries’ compliance with WTO rules. With the rise in protectionist sentiments around the world, the power of the WTO would seem to be on the wane. This raises the question of the implication of a ‘no-deal’ Brexit – something that seems more likely as the UK struggles to reach a trade agreement with the EU. Leaving without a deal would mean ‘reverting to WTO rules’. But if these rules are being ignored by powerful countries such as the USA and possibly China, and if the appeals procedure has ground to a halt, this could leave the UK without the safety net of international trade rules. Outside the EU – the world’s most powerful trade bloc – the UK could find itself having to accept poor trade terms with the USA and other large countries.

This raises the question of the implication of a ‘no-deal’ Brexit – something that seems more likely as the UK struggles to reach a trade agreement with the EU. Leaving without a deal would mean ‘reverting to WTO rules’. But if these rules are being ignored by powerful countries such as the USA and possibly China, and if the appeals procedure has ground to a halt, this could leave the UK without the safety net of international trade rules. Outside the EU – the world’s most powerful trade bloc – the UK could find itself having to accept poor trade terms with the USA and other large countries. The Economist is probably not the kind of newspaper that you will read more than once per issue – certainly not two years after its publication date. That is because, by definition, financial news articles are ephemeral: they have greater value, the more recent they are – especially in the modern financial world, where change can be strikingly fast. To my surprise, however, I found myself reading again an article on inequality that I had first read two years ago – and it is (of course) still relevant today.

The Economist is probably not the kind of newspaper that you will read more than once per issue – certainly not two years after its publication date. That is because, by definition, financial news articles are ephemeral: they have greater value, the more recent they are – especially in the modern financial world, where change can be strikingly fast. To my surprise, however, I found myself reading again an article on inequality that I had first read two years ago – and it is (of course) still relevant today.

Of course, wealth inequality does not happen only across countries – it happens also within countries. You can own a two-bedroom flat in London (and be, therefore, part of the 1% global elite), but having to live on a very modest budget because your income (which is a flow variable, as opposed to wealth, which is a stock variable) has not grown fast enough in relation to other parts of the national population.

Of course, wealth inequality does not happen only across countries – it happens also within countries. You can own a two-bedroom flat in London (and be, therefore, part of the 1% global elite), but having to live on a very modest budget because your income (which is a flow variable, as opposed to wealth, which is a stock variable) has not grown fast enough in relation to other parts of the national population. The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.