An investigation by the International Consortium of Investigative Journalists has revealed how more than 1000 businesses from 340 major companies from around the world have used Luxembourg as a base for avoiding huge amounts of tax. Many of the companies are household names, such as Ikea, FedEx, Apple, Pepsi, Coca Cola, Dyson, Amazon, Fiat, Google, Accenture, Burberry, Procter & Gamble, Heinz, JP Morgan, Caterpillar, Deutsche Bank and Starbucks. Through complicated systems of ‘advanced tax agreements’ (ATAs), negotiated with the Luxembourg authorities via accountants PricewaterhouseCoopers (PwC), companies have used various methods of avoiding tax.

An investigation by the International Consortium of Investigative Journalists has revealed how more than 1000 businesses from 340 major companies from around the world have used Luxembourg as a base for avoiding huge amounts of tax. Many of the companies are household names, such as Ikea, FedEx, Apple, Pepsi, Coca Cola, Dyson, Amazon, Fiat, Google, Accenture, Burberry, Procter & Gamble, Heinz, JP Morgan, Caterpillar, Deutsche Bank and Starbucks. Through complicated systems of ‘advanced tax agreements’ (ATAs), negotiated with the Luxembourg authorities via accountants PricewaterhouseCoopers (PwC), companies have used various methods of avoiding tax.

Although such measures are legal, they have denied other countries vast amounts of tax revenues on sales generated in their own countries. Instead, the much reduced tax bills have been paid to Luxembourg. The result is that this tiny country, with a population of just 550,000, has, according to the IMF, the highest (nominal) GDP per head in the world (estimated to be $116,752 in 2014).

So what methods do Luxembourg and these multinational companies use to reduce the companies’ tax bills? There are three main methods. All involve having a subsidiary based in Luxembourg: often little more than a small office with one employee, a telephone and a bank account. All involve varieties of transfer pricing: setting prices that the company charges itself in transactions between a subsidiary in Luxembourg and divisions in other countrries.

So what methods do Luxembourg and these multinational companies use to reduce the companies’ tax bills? There are three main methods. All involve having a subsidiary based in Luxembourg: often little more than a small office with one employee, a telephone and a bank account. All involve varieties of transfer pricing: setting prices that the company charges itself in transactions between a subsidiary in Luxembourg and divisions in other countrries.

The first method is the use of internal loans. Companies lend money to themselves, say in the UK, from Luxembourg at high interest rates. The loan interest can be offset against profit in the UK, reducing tax liability to the UK tax authorities. But the interest earned by the Luxembourg subsidiary incurs very low taxes. Profits are thus effectively transferred from the UK to Luxembourg and a much lower tax bill is incurred.

The second involves royalty payments for the use of the company’s brands. These are owned by the Luxembourg subsidiary and the overseas divisions pay the Luxembourg subsidiary large sums for using the logos, designs and brand names. Thus, again, profits are transferred to Luxembourg, where there is a generous tax exemption.

The third involves generous allowances in Luxembourg for losses in the value of investments, even without the company having first to sell the investments. These losses can be offset against future profits, again reducing tax liability. By transferring losses made elsewhere to Luxembourg, again usually by some form of transfer pricing, these can be used to reduce the already small tax bill in Luxembourg even further.

Tax loopholes offered by tax havens, such as Luxembourg, the Cayman Islands and the Channel Islands, are denying exchequers around the world vast sums. Not surprisingly, countries, especially those with large deficits, are concerned to address the issue of tax avoidance by multinationals. This is one item on the agenda of the G20 meeting in Brisbane from the 12 to 16 November 2014.

Tax loopholes offered by tax havens, such as Luxembourg, the Cayman Islands and the Channel Islands, are denying exchequers around the world vast sums. Not surprisingly, countries, especially those with large deficits, are concerned to address the issue of tax avoidance by multinationals. This is one item on the agenda of the G20 meeting in Brisbane from the 12 to 16 November 2014.

The problem, however, is that, with countries seeking to attract multinational investment and to gain tax revenues from them, there is an incentive to reduce corporate tax rates. Getting any binding agreement on tax harmonisation, and creating an essentially global single market, is likely, therefore, to prove virtually impossible.

Webcasts and videos

Luxembourg Leaks: Tricks of the Trade ICIJ in partnership with the Pulitzer Center (5/11/14)

Luxembourg Leaks: Tricks of the Trade ICIJ in partnership with the Pulitzer Center (5/11/14)

Luxembourg ‘abetted’ companies in avoiding taxes France 24, Siobhán Silke (6/11/14)

Tax deals with Luxembourg save companies billions, says report Deutsche Welle, Dagmar Zindel (6/11/14)

Luxembourg: the tax haven and the $870m loan company above a stamp shop The Guardian, John Domokos, Rupert Neate and Simon Bowers (5/11/14)

Luxembourg leaks: nation under spotlight over tax avoidance claims euronews (6/11/14)

Northern and Shell used west Dublin address to cut Luxembourg tax bill on €1bn The Irish Times, Colm Keena (6/11/14)

The ATO’s global tax avoidance investigation ABC News, Phillip Lasker (9/11/14)

Pepsi, IKEA Secret Luxembourg Tax Deals Exposed TheLipTV, Elliot Hill (9/11/14)

Articles

Leaked Docs Expose More Than 340 Companies’ Tax Schemes In Luxembourg Huffington Post, Leslie Wayne, Kelly Carr, Marina Walker Guevara, Mar Cabra and Michael Hudson (5/11/14)

Luxembourg tax files: how tiny state rubber-stamped tax avoidance on an industrial scale The Guardian, Simon Bowers (5/11/14)

Fact and fiction blur in tales of tax avoidance The Guardian (9/11/14)

companies engaged in tax avoidance The Guardian, Michael Safi (6/11/14)

The Guardian view on tax avoidance: Europe must take Luxembourg to task The Guardian, Editorial (6/11/14)

G20 leaders in the mood to act on tax avoidance after Luxembourg leaks Sydney Morning Herald, Tom Allard (6/11/14)

Scale of Luxembourg tax avoidance revealed economia, Oliver Griffin (6/11/14)

EU to press Luxembourg over tax breaks amid fresh allegations BBC News (6/11/14)

Luxembourg leaks: G20 alone can’t stamp out tax avoidance The Conversation, Charles Sampford (7/11/14)

‘Lux leaks’ scandal shows why tax avoidance is a bad idea European Voice, Paige Morrow (8/11/14)

EU to Probe Luxembourg’s ‘Sweetheart Tax Deal’ with Amazon International Business Times, Jerin Mathew (7/10/14)

Investigative Project

Luxembourg Leaks: Global Companies’ Secrets Exposed The International Consortium of Investigative Journalists (5/11/14)

Questions

- Distinguish between tax avoidance and tax evasion. Which of the two is being practised by companies in their arrangements with Luxembourg?

- Explain what is meant by transfer pricing.

- Do a search of companies to find out what parts of their operations as based in Luxembourg.

- In what sense can the setting of corporate taxes be seen as a prisoner’s dilemma game between countries?

- Discuss the merits of changing corporate taxes so that they are based on revenues earned in a country rather than on profits.

- What type of agreement on tax havens is likely to be achieved by the international community?

- Is it desirable for companies to be able to offset losses against future profits?

In an earlier post, Elizabeth looked at oligopolistic competition between supermarkets. Although supermarkets have been accused of tacit price collusion on many occasions in the past, price competition has been growing. And recent developments show that it is likely to get a lot fiercer as the ‘big four’ try to take on the ‘deep discounters’, Aldi and Lidl.

In an earlier post, Elizabeth looked at oligopolistic competition between supermarkets. Although supermarkets have been accused of tacit price collusion on many occasions in the past, price competition has been growing. And recent developments show that it is likely to get a lot fiercer as the ‘big four’ try to take on the ‘deep discounters’, Aldi and Lidl.

Part of the reason for the growth in price competition has been a change in shopping behaviour. Rather than doing one big shop per week in Tesco, Sainsbury’s, Asda or Morrisons, many consumers are doing smaller shops as they seek to get more for their money. A pattern is emerging for many consumers who are getting their essentials in Aldi or Lidl, their ‘special’ items in more upmarket shops, such as Waitrose, Marks & Spencer or small high street shops (such as bakers and ethnic food shops) and getting much fewer products from the big four. Other consumers, on limited incomes, who have seen their real incomes fall as prices have risen faster than wages, are doing virtually all their shopping in the deep discounters. As the Guardian article below states:

A steely focus on price and simplicity, against a backdrop of falling living standards that has sharpened customers’ eye for a bargain, has seen the discounter grab market share from competitors and transform what we expect from our weekly shop.

The result is that the big four are seeing their market share falling, as the chart shows.  (Click here for a PowerPoint of the chart.) In the past year, Tesco’s market share has fallen from 29.9% to 28.1%, Asda’s from 17.8% to 16.3%, Sainsbury’s from 16.9% to 16.2% and Morrisons’ from 11.7% to 11.0%. By contrast, Aldi’s has risen from 3.9% to 5.4% and Lidl’s from 3.1% to 4.0%, while Waitrose’s has also risen, from 4.7% to 4.9%. And it’s not just market share that has been falling for the big four. Profits have also fallen, as have share prices. Sales revenues in the four weeks to 13 September are down 1.6% on the same period a year ago; sales volumes are down 1.9%.

(Click here for a PowerPoint of the chart.) In the past year, Tesco’s market share has fallen from 29.9% to 28.1%, Asda’s from 17.8% to 16.3%, Sainsbury’s from 16.9% to 16.2% and Morrisons’ from 11.7% to 11.0%. By contrast, Aldi’s has risen from 3.9% to 5.4% and Lidl’s from 3.1% to 4.0%, while Waitrose’s has also risen, from 4.7% to 4.9%. And it’s not just market share that has been falling for the big four. Profits have also fallen, as have share prices. Sales revenues in the four weeks to 13 September are down 1.6% on the same period a year ago; sales volumes are down 1.9%.

But can the big four take on the discounters at their own game? Morrison’s has just announced a form of price match scheme called ‘Match & More’. If a shopper finds that a comparable grocery shop is cheaper in not only Tesco, Sainsbury’s or Asda, but also in Aldi or Lidl, then ‘Match & More users will automatically get the difference back in points on their card. Shoppers also will be able to collect extra points on hundreds of featured products and fuel’. When the difference has risen to a total £5 (5000 points), the shopper will get a £5 voucher at the till. The idea is to encourage customers to stay loyal to Morrisons.

But what if Tesco, Asda and Sainsbury’s do the same? What will be the impact on their prices and profits. Will there be a race to the bottom in prices, or will they be able to keep prices higher than the deep discounters, hoping that many customers will not cash in their vouchers?

But what if Tesco, Asda and Sainsbury’s do the same? What will be the impact on their prices and profits. Will there be a race to the bottom in prices, or will they be able to keep prices higher than the deep discounters, hoping that many customers will not cash in their vouchers?

But if effectively the big four felt forced to cut their prices to match Aldi and Lidl, could they afford to do so? This depends on their comparative average costs. At first sight, it might be thought that the big four could succeed in profitably matching the discounters, thereby clawing back market share. After all, they are much bigger and it might be thought that they would benefit from greater economies of scale and hence lower costs.

But it is not as simple as this. The discounters have lower costs than the big four. Their shops are typically in areas where rents or land prices are lower; their shops are smaller; they carry many fewer lines and thus gain economies of scale on each line; they have a much higher proportion of own-brand products; products are displayed in the boxes they come in, thus saving on the staff costs of unpacking them and placing them on shelves; they buy what is cheapest and thus do not always display the same brands.

So is Morrison’s a wise strategy? Will other supermarkets be forced to follow? Is there a prisoners’ dilemma here and, if so, is there any form of collusion in which the big four can engage which is not illegal? Can the big four differentiate themselves from the discounters and the up-market supermarkets in ways that will attract back customers?

It is worrying times for the big four.

Articles

- Heavy Discounters Up Pressure On The UK’s Big Four Supermarkets

Alliance News, Rowena Harris-Doughty (3/6/14)

- Tesco loses more market share as supermarket sector slows to record low

CITY A.M., Catherine Neilan (23/9/14)

- Record low for grocery market growth as inflation disappears

Kantar World Panel, Fraser McKevitt (23/9/14)

- How Aldi’s price plan shook up Tesco, Morrison’s, Asda and Sainsbury’s

The Guardian, Sarah Butler (29/9/14)

- Sainsbury’s shares drop 7% on falling sales report

BBC News (1/10/14)

- Sainsbury results: the reaction

Food Manufacture, Mike Stones (3/10/14)

- Morrisons Becomes First Of Big Four Grocers To Price Match Aldi, Lidl

Alliance News, Rowena Harris-Doughty (2/10/14)

- UK: Morrisons Takes On Discounters With Price Match Card

KamCity (3/10/14)

- Morrisons to match the prices of Aldi and Lidl

The Telegraph, Graham Ruddick (2/10/14)

- Three reasons why Morrisons price-matching Aldi and Lidl is not a ‘gamechanger’

The Telegraph, Graham Ruddick (2/10/14)

Questions

- Would it be possible for the big four to price match the deep discounters?

- What is meant by the prisoners’ dilemma? In what ways are the big four in a prisoners’ dilemma situation?

- Assume that you had to advise Tesco on it strategy? What advise would you give it and why?

- Assume that two firms, M and A, are playing the following ‘game’: firm M pledges to match firm A’s prices; and firm A pledges to sell at 2% below M’s price. What will be the outcome of this game?

- Is Morrisons wise to adopt its ‘Match & More’ strategy?

- Why is it difficult for Morrisons to make a like-for-like comparison with Aldi and Lidl in its ‘Match & More’ strategy?

- Why may Aldi and Lidl benefit from Morrisons’ strategy?

Merlin Entertainments PLC is one of the largest operator of visitor attractions in the world and owns over a third of the most popular theme parks in Europe. It runs the four most visited parks in England – Alton Towers, Legoland Windsor, Thorpe Park and Chessington World of Adventures as well as the most popular theme park in Italy – Gardaland. Alton Towers alone had 2.5 million visitors in 2013. Anybody thinking of going to one of these attractions is faced with a wide range of different entry fees .

Merlin Entertainments PLC is one of the largest operator of visitor attractions in the world and owns over a third of the most popular theme parks in Europe. It runs the four most visited parks in England – Alton Towers, Legoland Windsor, Thorpe Park and Chessington World of Adventures as well as the most popular theme park in Italy – Gardaland. Alton Towers alone had 2.5 million visitors in 2013. Anybody thinking of going to one of these attractions is faced with a wide range of different entry fees .

Theme parks and tourist attractions have market power so their owners have to make some interesting pricing decisions. They have to tackle the same dilemma that confronts any seller that faces a downward sloping demand curve for its goods/services.

One option for the firm would be to increase the entry fee. This would produce higher profits per visitor as some of the surplus from the transaction previously enjoyed by the consumer will be extracted by the seller and converted into producer surplus. Unfortunately for the business the higher price, all other things equal, will also result in fewer visitors. Some people will be deterred from visiting because of the higher price and the seller will lose out on potential revenue.

An alternative strategy would be for the theme park to reduce its entry fee. All other things equal, this will increase the number of visitors. However, it would also mean that the profit per customer would fall. The frustrating issue for the seller is that some of its customers, who would still have visited the attraction at the higher price, are now able to get a better deal.

This dilemma exists if the seller has to charge all of its different customers the same entry fee. If it could charge a higher entry fee to those customers who would be willing to pay more and a lower entry fee to those who would be willing to pay less then it could make more money. Extra revenue could be obtained from those additional sales that take place at the lower price while more consumer surplus could be extracted from those still paying the higher price.

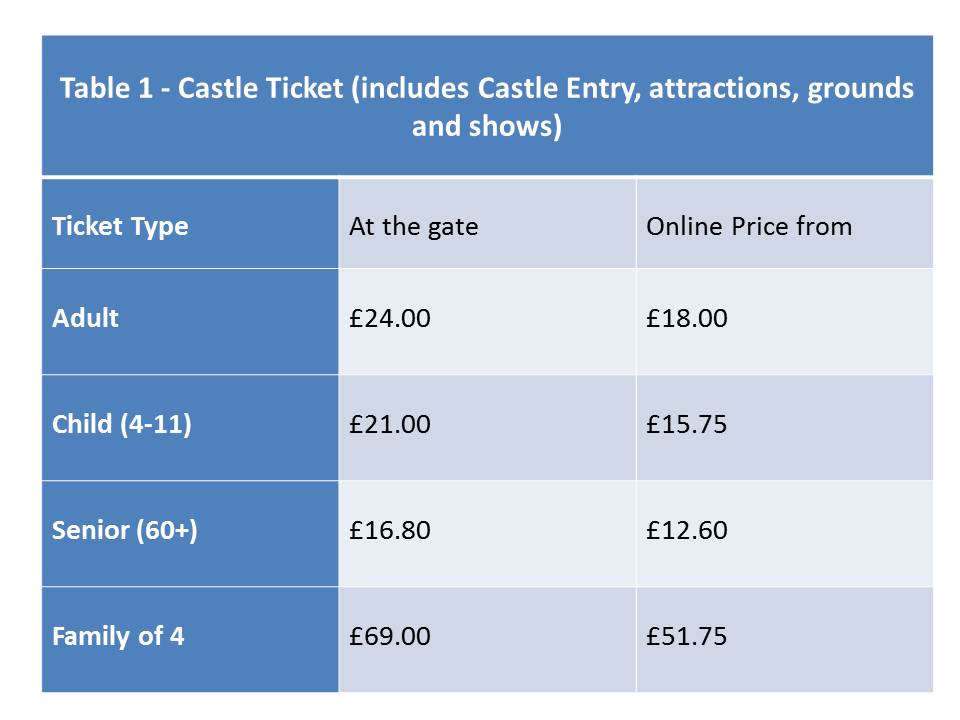

Is it possible for a firm to charge different prices to different customers for the same or a similar good or service? Table 1 below shows the entry fees for Warwick Castle, another tourist attraction owned by Merlin Entertainments PLC.

It can immediately be seen from this table that some groups of customers pay a different entry fee from others. For example adults have to pay £24 to enter on the day while people aged 60 and over pay a lower price £16.80. The entry fee for children aged between 4 and 11 is £21.00 while those aged 3 and under go for free. Students aged 16-18 can gain entry for a price of £13.50 if they can provide valid ID and purchase the tickets from the visitbritainshop website.

In this example, the company has allocated people into different categories by age (i.e. senior, adult, student, older children and younger children) and has set the entry fee that customers in each group have to pay.

The table also shows that if customers purchase on- line then they can get the tickets more cheaply. The entry fee for each category is 25% lower if the ticket is booked seven days in advance i.e. the prices shown in the last column in the table. If the booking is made between 2-6 days in advance then the discount is only 10% i.e. an adult ticket would cost £21.60. The on-line discounts are open to everyone. People are given the choice to either book on-line in advance or pay on the day. This is different from a situation where you are placed into a category by the firm. For example the customer cannot choose whether they are over 60!

If people are prepared to spend more time searching on the internet then other cheaper prices can also be obtained. Once again these offers are open to anyone willing to spend the time and effort in order to find them.

All the ticket prices above give people access to exactly the same attractions on the day. They do not give the visitor access to two of the attractions at the castle – the Dragon Tower and Castle Dungeon. Entry to the Dragon Tower would cost an adult on the day an extra £1.80 while entry to the Castle Dungeon would cost an extra £5.40.

Warwick Castle Ticket Prices Warwick Castle (accessed on 04/09/14)

Alton Towers Alton Towers (accessed on 08/09/14)

Warwick Castle Tickets visitbritainshop (accessed on 02/09/14)

Global Attractions Attendance Report teaconnect (accessed on 05/09/14)

Merlin Entertainments Merlin Entertainments (accessed on 08/09/14)

Questions

- What pricing decisions do firms have to make if they operate in a perfectly competitive market?

- Explain why an individual tourist attraction will have a downward sloping demand curve

- Paying an entry fee and an extra payment per attraction is known as what type of pricing? What advantages does this type of price strategy have for the seller?

- How would you calculate the profit per customer? What factors other than the entrance fee would determine the profit made per customer in a theme park or tourist attractions?

- Paying a different price depending on which category you have been assigned to by the seller is known as what type of pricing strategy? Can this type of pricing strategy ever be in the interests of society?

- In the example used in the case, customers are assigned to different categories by age. Can you think of any other ways that firms could categorise their customers?

- Given the category customers have been assigned to they can pay different prices depending on whether they buy the tickets on line. What is the price strategy called when customers can choose from a variety of pricing options for the same or similar product? Can you think of any different methods that could be used by the seller to carry out this type of pricing strategy?

Over the past few decades, numerous areas within the British economy have been partly or fully privatized and one such case is British Rail. Why is this relevant now? We’re once again looking at the potential increase in rail fares across the country and the impact this will have on commuters and households. So, have the promises of privatisation – namely lower fares – actually materialised?

Over the past few decades, numerous areas within the British economy have been partly or fully privatized and one such case is British Rail. Why is this relevant now? We’re once again looking at the potential increase in rail fares across the country and the impact this will have on commuters and households. So, have the promises of privatisation – namely lower fares – actually materialised?

Comparing the increase in rail fares with that of the RPI makes for interesting reading. Data obtained back in January 2013 shows that since 1995, when the last set of British Rail fares were published, the RPI has been 66%, according to data from Barry Doe and this compares unfavourably with the increase in a single ticket from London to Manchester which had increased by over 200%. However, it compares favourably with a season ticket, which had only increased by 65%. In the last couple of years, increased in rail fares have been capped by the government to increase by no more than the rate of inflation. As such, customers are likely to be somewhat insulated from the increases that were expected, which could have ranged between 3 and 5%.

This announcement has been met with mixed reviews, with many in support of such caps and the benefit this will bring to working households, including Passenger Focus, the rail customer watchdog. Its Passenger Director, David Sidebottom said:

The capping of rail fare rises by inflation will be welcome news to passengers in England, especially those who rely on the train for work, as will the ban on train companies increasing some fares by more than the average. It is something we have been pushing for, for several years now and we are pleased that the Government has recognised the need to act to relieve the burden on passengers.

However, others have criticised the increases in rail fares, given the cost of living crisis and the potential 9% pay rise for MPs. The acting General Secretary of the RMT transport union commented:

However, others have criticised the increases in rail fares, given the cost of living crisis and the potential 9% pay rise for MPs. The acting General Secretary of the RMT transport union commented:

The announcement from George Osborne does not stack up to a freeze for millions of people whose incomes are stagnant due to years of austerity. To try and dress this up as benefiting working people is pure fraud on the part of the Government … Tomorrow, RMT will be out at stations across the north where some off-peak fares will double overnight.

Commuters in different parts of the country do face different prices and with some changes in peak travel times in the Northern part of the country, it is expected that some customers will see significant hikes in prices. Peak travel prices being higher is no surprise and there are justifiable reasons for this, but would such changes in peak times in the North have occurred had we still been under British Rail? Privatisation should bring more competition, lower prices and government revenue at the point of sale. Perhaps you might want to look in more detail at the actual to see whether or not you think the benefits of privatisation have actually emerged. The following articles consider the latest announcement regarding rail fares.

Rail fares to increase by 2.5% in January after Osborne caps price rises at no more than inflation Mail Online, Tom McTague (7/9/14)

Have train fares gone up or down since British Rail? BBC News, Tom Castella (22/1/13)

Rail fares to match inflation rate for another 12 months The Guardian (7/9/14)

Britain caps rail fares at inflation Reuters (7/9/14)

Regulated rail fares to increase by 3.5% in 2015 BBC News (19/8/14)

Northern commuters face big rise in fares for evening travel The Guardian, Gwyn Topham (7/9/14)

Commuter rail fares frozen again, says George Osborne BBC News (7/8/14)

Rail fares, the third payroll tax Financial Times, Jonathan Eley (22/8/14)

Questions

- What are the general advantages and disadvantages of privatisation, whether it is of British Rail or British Gas?

- Why is it that season tickets have increased by less than the RPI, but single tickets have increased by more?

- What are the conditions needed to allow train companies to charge a higher price at peak travel times?

- Are higher prices at peak times an example of price discrimination? Explain why or why not.

- In the Financial Times article, it is suggested that rail fares are like a payroll tax. What is a payroll tax and why are rail fares related to this? Does it suggest that the current method of setting rail fares is equitable?

- Based on the arguments contained in the articles, do you think the cap on rail fares is sufficient?

With the new Premier League football season only a week away, TV companies are heavily advertising the matches they will be showing. Until recently, BSkyB, having seen off competition from Setanta and ESPN, appeared to have an untouchable position in this market. However, competition now appears to be intensifying.

With the new Premier League football season only a week away, TV companies are heavily advertising the matches they will be showing. Until recently, BSkyB, having seen off competition from Setanta and ESPN, appeared to have an untouchable position in this market. However, competition now appears to be intensifying.

BT entered the market in 2012 by paying £738m for the rights to screen 38 Premier League matches a season for 3 seasons, with Sky showing another 116 matches. BT is clearly heavily backing its sports coverage with an initial outlay of £1.5b and them continuing to sign up high profile presenters and ambassadors including former players and a current manager.

Furthermore, BT dealt Sky (and ITV) a hefty blow last year when it outbid them to win the rights to exclusively show European club competition matches from 2015. Sky responded by saying that:

We bid with a clear view of what the rights are worth to us. It seems BT chose to pay far in excess of our valuation

If true, this would illustrate the winner’s curse which can arise in auctions. However, John Petter, chief executive of BT Retail, said that the deal demonstrated that BT Sport was committed to establishing itself in this market and countered Sky’s suggestion that they had overpaid by saying:

They would say that, wouldn’t they? Secretly, I’d expect them to be kicking themselves and full of regrets this morning

Clearly important to BT’s strategy is bundling its sports coverage in for free with their broadband packages. This is not without controversy since, at the same time as spending vast amounts of money to setup its sports coverage, BT is receiving large government subsidies to improve rural broadband provision.

An important forthcoming ruling from the Competition Appeal Tribunal will have a significant effect on how competition between BT and Sky develops. In this case Sky is accused of abusing its dominant position by refusing to supply BT’s YouView service with its sports channels at a reasonable wholesale price and could now be forced to do so.

It will also be fascinating to see how BT Sport’s strategy develops over time. BT is unlikely to continue  to provide all its coverage for free once it includes the European matches that it has won the rights to show at great expense. It will also be fascinating to see the extent to which it continues to have success in winning broadcasting rights in the future.

to provide all its coverage for free once it includes the European matches that it has won the rights to show at great expense. It will also be fascinating to see the extent to which it continues to have success in winning broadcasting rights in the future.

Competition will inevitably push up the amount that the Premier League raises in the next rights auction. Current predictions are that these will be sold for over £4bn, up from £3bn in the previous auction. This will increase the amount the Premier League clubs receive and is also likely to further push up player wages. It remains to be seen the extent to which this will benefit viewers, not to mention pubs wishing to show the games some of whom have in the past looked for alternative solutions because of the high prices they have to pay.

BT wins court battle forcing review of Sky wholesale pricing decision The Guardian, Mark Sweney (17/02/14)

BT Sport does little to lift BT TV homes informitv – connected vision (01/08/14)

BT Sport continues to invest in football line-up MediaWeek, Arif Durrani (29/07/14)

Questions

- What are the key characteristics of the market for sports broadcasting rights?

- What are the pros and cons for consumers of BT Sport’s emergence?

- How do you think Sky might respond to competition from BT Sport?

- How do you think BT Sport’s strategy might develop over time?

An investigation by the International Consortium of Investigative Journalists has revealed how more than 1000 businesses from 340 major companies from around the world have used Luxembourg as a base for avoiding huge amounts of tax. Many of the companies are household names, such as Ikea, FedEx, Apple, Pepsi, Coca Cola, Dyson, Amazon, Fiat, Google, Accenture, Burberry, Procter & Gamble, Heinz, JP Morgan, Caterpillar, Deutsche Bank and Starbucks. Through complicated systems of ‘advanced tax agreements’ (ATAs), negotiated with the Luxembourg authorities via accountants PricewaterhouseCoopers (PwC), companies have used various methods of avoiding tax.

An investigation by the International Consortium of Investigative Journalists has revealed how more than 1000 businesses from 340 major companies from around the world have used Luxembourg as a base for avoiding huge amounts of tax. Many of the companies are household names, such as Ikea, FedEx, Apple, Pepsi, Coca Cola, Dyson, Amazon, Fiat, Google, Accenture, Burberry, Procter & Gamble, Heinz, JP Morgan, Caterpillar, Deutsche Bank and Starbucks. Through complicated systems of ‘advanced tax agreements’ (ATAs), negotiated with the Luxembourg authorities via accountants PricewaterhouseCoopers (PwC), companies have used various methods of avoiding tax. So what methods do Luxembourg and these multinational companies use to reduce the companies’ tax bills? There are three main methods. All involve having a subsidiary based in Luxembourg: often little more than a small office with one employee, a telephone and a bank account. All involve varieties of transfer pricing: setting prices that the company charges itself in transactions between a subsidiary in Luxembourg and divisions in other countrries.

So what methods do Luxembourg and these multinational companies use to reduce the companies’ tax bills? There are three main methods. All involve having a subsidiary based in Luxembourg: often little more than a small office with one employee, a telephone and a bank account. All involve varieties of transfer pricing: setting prices that the company charges itself in transactions between a subsidiary in Luxembourg and divisions in other countrries. Tax loopholes offered by tax havens, such as Luxembourg, the Cayman Islands and the Channel Islands, are denying exchequers around the world vast sums. Not surprisingly, countries, especially those with large deficits, are concerned to address the issue of tax avoidance by multinationals. This is one item on the agenda of the G20 meeting in Brisbane from the 12 to 16 November 2014.

Tax loopholes offered by tax havens, such as Luxembourg, the Cayman Islands and the Channel Islands, are denying exchequers around the world vast sums. Not surprisingly, countries, especially those with large deficits, are concerned to address the issue of tax avoidance by multinationals. This is one item on the agenda of the G20 meeting in Brisbane from the 12 to 16 November 2014.