What does it take to create a successful business? From the looks of it: mud, electric barbed wire, icy water, enormous walls to climb, big jumps to make, team work and complete exhaustion – the recipe for every successful business.

What does it take to create a successful business? From the looks of it: mud, electric barbed wire, icy water, enormous walls to climb, big jumps to make, team work and complete exhaustion – the recipe for every successful business.

Tough Mudder was founded in 2010 and runs gruelling extreme obstacle courses for anyone mad enough to think it might be fun. In the BBC News article below, you’ll see that there is a discussion as to intellectual property rights, but whatever the outcome, this company has become the main provider of such extreme sports in a remarkably short period of time. Within 2 years of being established, it had gained 500,000 participants and now records annual revenues of more than £60m. Add to this, that there has no external funding and this organic growth is beyond impressive.

A key question, then, is what creates such a successful business? Without a doubt, this depends on the product you are selling and the market a firm is in, but there are some aspects that apply across the board. Understanding what your customers want is crucial, as they represent your demand. Differentiating your product to create inelastic demand may be a good strategy to enable price rises, without losing a large number of sales, but the differentiated product is essential in establishing demand, loyalty and reputation. Marketing something in the right way and to the right audience is crucial – word-of-mouth is often the most effective form of advertising.

If you have all of these aspects, then you have the makings of a successful business. The next step is putting it into practice and climbing those high walls, taking the big jumps and hopefully avoiding the mud and ice. The following article considers Will Dean and his fast growing business.

Will Dean: ‘The Mark Zuckerberg of extreme sports’ BBC News, Will Smale (9/6/14)

Questions

- If you were starting up a business, how might you go about finding out if there is a demand for your product?

- Why is product differentiation a key aspect of a successful business? Using a diagram, explain how this might help a firm increase revenue and profits.

- What forms of marketing might be used in persuading customers to buy your product?

- In the case of Tough Mudder, which aspects have proved the most important in creating such a successful business?

- Are there any barriers to the entry of new firms in this sector? If so, what are they are how important are they in allowing Tough Mudder to retain a monopoly position?

- Which factors should be considered by a company when it is thinking of global expansion?

Life expectancy is increasing across the world and the latest set of figures from the Office for National Statistics show that in the UK it has passed 79 for boys born in 2010–12, and 82 for girls born then. In fact the prediction is that over a third of babies born in 2013 will live to more than 100. The data throws up some interesting questions. How well prepared are we for lives that last this long? And how evenly distributed is this increase in life expectancy? Pensions’ minister, Steve Webb, has called for better information on life expectancy to be shared. How would this impact on our decision making?

Life expectancy is increasing across the world and the latest set of figures from the Office for National Statistics show that in the UK it has passed 79 for boys born in 2010–12, and 82 for girls born then. In fact the prediction is that over a third of babies born in 2013 will live to more than 100. The data throws up some interesting questions. How well prepared are we for lives that last this long? And how evenly distributed is this increase in life expectancy? Pensions’ minister, Steve Webb, has called for better information on life expectancy to be shared. How would this impact on our decision making?

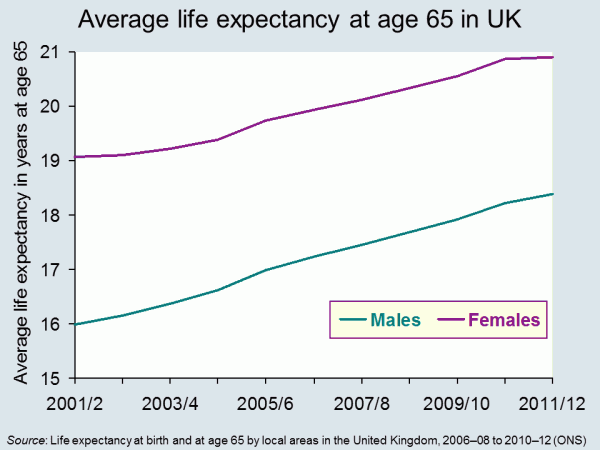

It seems reasonable to think that increasing life expectancy must be good news. And of course, for individuals it can be. In 1951 the average man retiring at 65, in England and Wales, could expect to live and draw a pension for another 12.1 years. By 2014 this had risen to 22 years.

But while we can look forward to longer life, for the government, it presents some challenges The first is that we just don’t save enough for our old age. This seems to be partly because we find it hard to make decisions that will have an impact so far in the future. There are a number of measures that have been put in place to encourage us to save more, including auto-enrolment into company pension schemes. This is being rolled out across businesses over the next three years. In the 2014 Budget, the Chancellor announced that people reaching retirement age will be able to draw all their pension as a cash lump sum, rather than having to take it as a regular income.

But while we can look forward to longer life, for the government, it presents some challenges The first is that we just don’t save enough for our old age. This seems to be partly because we find it hard to make decisions that will have an impact so far in the future. There are a number of measures that have been put in place to encourage us to save more, including auto-enrolment into company pension schemes. This is being rolled out across businesses over the next three years. In the 2014 Budget, the Chancellor announced that people reaching retirement age will be able to draw all their pension as a cash lump sum, rather than having to take it as a regular income.

Another concern for government is the variations that we find in life expectancy across the UK. The 2014 ONS data identified that life expectancy for men born in Glasgow in 2012 is 72.6, in East Dorset it is 82.9. 25% of those in Glasgow are not expected to live to 65. The gap in years of good health is even greater. This presents governments with a long-term problem. How do they achieve greater equality in this instance? Do they focus resources on the areas that need it most? Do they legislate to address behaviour? Or do they rely on the provision of good advice – on diet, exercise and other factors?

Information has a role to play in both areas identified above. In April 2014, Steve Webb, suggested that in order to make good decisions at the point of retirement, people need to understand more about what lies ahead. He said:

People tend to underestimate how long they’re likely to live, so we’re talking about averages, something very broad-brush. Based on your gender, based on your age, perhaps asking one or two basic questions, like whether you’ve smoked or not, you can tell somebody that they might, on average, live for another 20 years or so.

This suggestion has led to some concerns being expressed at what appears to be an over-simplistic approach. Estimates can only be based on a mix of averages modified by individual information. Would the projections be shared with pension providers? What would you do if you exceeded your forecast life expectancy – by a long way – and had spent all your money? Could you sue someone?

Will your pension pot last as long as you will? The Telegraph, Dan Hyde and Richard Dyson (23/4/2014)

Scientists invent death test that will tell us how long we have to live Metro (11/8/13)

Games host Glasgow has worst life expectancy in the UK The Guardian, Caroline Davies (16/4/2014)

Pensioners could get life expectancy guidance BBC News Politics (17/4/14)

ONS reveals gaps in life expectancy across the UK FT Adviser Pensions, Kevin White (23/4/14)

Health care aid for developing countries boosts life expectancy Health Canal, Ruth Ann Richter (22/4/14)

A third of babies born this year will live to 100 This is Money.co.uk, Adam Uren (11/12/13)

Questions

- Thinking about the UK, what are the factors that might explain variations in life expectancy across different regions? How might the government address these differences? Why would they want to do so?

- Do the same factors explain variations between countries? Who can address these differences? Who would want to do so?

- If you could have a reasonable prediction of your life expectancy at 65, would you want it? How would your behaviour change if you were predicted a longer than average life expectancy? How would it change if you were predicted a shorter than average life expectancy?

- If you could have an accurate prediction of your life expectancy at 18, how would your answers differ? If this were possible, would it present any problems?

Britain has faced some its worst ever weather, with thousands of homes flooded once again, though the total number of flooded households has fallen compared to previous floods. However, for many households, it is just more of the same – if you’ve been flooded once, you’re likely to be flooded again and hence insurance against flooding is essential. But, if you’re an insurance company, do you really want to provide cover to a house that you can almost guarantee will flood?

Britain has faced some its worst ever weather, with thousands of homes flooded once again, though the total number of flooded households has fallen compared to previous floods. However, for many households, it is just more of the same – if you’ve been flooded once, you’re likely to be flooded again and hence insurance against flooding is essential. But, if you’re an insurance company, do you really want to provide cover to a house that you can almost guarantee will flood?

The government has pledged thousands to help households and businesses recover from the damage left by the floods and David Cameron’s latest step has been to urge insurance companies to deal with claims for flood damage as fast as possible. He has not, however, said anything regarding ‘premium holidays’ for flood victims.

The problem is that the premium you are charged depends on many factors and one key aspect is the likelihood of making a claim. The more likely the claim, the higher the premium. If a household has previous experience of flooding, the insurance company will know that there is a greater likelihood of flooding occurring again and thus the premium will be increased to reflect this greater risk. There have been concerns that some particularly vulnerable home-owners will be unable to find or afford home insurance.

The key thing with insurance is that in order for it to be provided privately, certain conditions must hold. The probability of the event occurring must be less than 1 – insurance companies will not insure against certainty. The probability of the event must be known on aggregate to allow insurance companies to calculate premiums. Probabilities must be independent – if one person makes a claim, it should not increase the likelihood of others making claims.

Finally, there should be no adverse selection or moral hazard, both of which derive from asymmetric information. The former occurs where the person taking out the insurance can hide information from the company (i.e. that they are a bad risk) and the latter occurs when the person taking out insurance changes their behaviour once they are insured. Only if these conditions hold or there are easy solutions will the private market provide insurance.

On the demand-side, consumers must be willing to pay for insurance, which provides them with protection against certain contingencies: in this case against the cost of flood damage. Given the choice, rational consumers will only take out an insurance policy if they believe that the value they get from the certainty of knowing they are covered exceeds the cost of paying the insurance premium. However, if the private market fails to offer insurance, because of failures on the supply-side, there will be major gaps in coverage.

Furthermore, even if insurance policies are offered to those at most risk of flooding, the premiums charged by the insurance companies must be high enough to cover the cost of flood damage. For some homeowners, these premiums may be unaffordable, again leading to gaps in coverage.

Perhaps here there is a growing role for the government and we have seen proposals for a government-backed flood insurance scheme for high-risk properties due to start in 2015. However, a loop hole may mean that wealthy homeowners pay a levy for it, but are not able to benefit from the cheaper premiums, as they are deemed to be able to afford higher premiums. This could see many homes in the Somerset Levels being left out of this scheme, despite households being underwater for months. There is also a further role for government here and that is more investment in flood defences. If that occurs though, where will the money come from? The following articles consider flooding and the problem of insurance.

Articles

Insurers urged to process flood claims quickly BBC News (17/2/14)

Insurers urged to process flood claims quickly BBC News (17/2/14)

Flood area defences put on hold by government funding cuts The Guardian, Damian Carrington and Rajeev Syal (17/2/14)

Flooding: 200,000 houses at risk of being uninsurable The Telegraph (31/1/12)

Govt flood insurance plan ‘will not work’ Sky News (14/2/14)

Have we learned our lessons on flooding? BBC News, Roger Harrabin (14/2/14)

ABI refuses to renew statement of principles for flood insurance Insurance Age, Emmanuel Kenning (31/1/12)

Wealthy will have to pay more for flood insurance but won’t be covered because their houses are too expensive Mail Online, James Chapman (7/2/14)

Buyers need ‘flood ratings’ on all houses, Aviva Chief warns The Telegraph, James Quinn (15/2/14)

Wealthy homeowners won’t be helped by flood insurance scheme The Telegraph(11/2/14)

Costly insurance ‘will create flood-risk ghettos and £4.3tn fall in house values’ The Guardian, Patrick Wintour (12/2/14)

Leashold homes face flood insurance risk Financial Times, Alistair Gray (10/2/14)

Questions

- Consider the market for insurance against flood damage. Are risks less than one? Explain your answer.

- Explain whether or not the risk of flooding is independent.

- Are the problems of moral hazard and adverse selection relevant in the case of home insurance against flood damage?

- To what extent is the proposed government-backed flood insurance an equitable scheme? Should the government be stepping in to provide insurance itself?

- Should there be greater regulation when houses are sold to provide better information about the risk of flooding?

- Why if the concept of opportunity cost relevant here?

- How might household values be affected by recent floods, in light of the issues with insurance?

I am an avid tennis fan and have spent many nights and in the last 10 days had many early mornings (3am), where I have been glued to the television, watching in particular Rafael Nadal in the Australian Open. Tennis is one of the biggest sports worldwide and generates huge amounts of revenue through ticket sales, clothing and other accessories, sponsorship, television rights and many other avenues. When I came across the BBC article linked below, I thought it would make an excellent blog!

I am an avid tennis fan and have spent many nights and in the last 10 days had many early mornings (3am), where I have been glued to the television, watching in particular Rafael Nadal in the Australian Open. Tennis is one of the biggest sports worldwide and generates huge amounts of revenue through ticket sales, clothing and other accessories, sponsorship, television rights and many other avenues. When I came across the BBC article linked below, I thought it would make an excellent blog!

There are many aspects of tennis (and of every other sport) that can be analysed from a Business and Economics stance. With the cost of living having increased faster than wages, real disposable income for many households is at an all-time low. Furthermore, we have so many choices today in terms of what we do – the entertainment industry has never been so diverse. This means that every form of entertainment, be it sport, music, cinema, books or computer games, is in competition. And then within each of these categories, there’s further competition: do you go to the football or the tennis? Do you save up for one big event and go to nothing else, or watch the big event on TV and instead go to several other smaller events? Tennis is therefore competing in a highly competitive sporting market and a wider entertainment market. The ATP Executive Chairman and President said:

We’ve all got to understand the demands on people’s discretionary income are huge, they are being pulled in loads of different avenues – entertainment options of film, music, sport – so we just need to make sure that our market share remains and hopefully grows as well.

As we know from economic analysis, product differentiation and advertising are key and tennis is currently in a particularly great era when it comes to drawing in the fans, with four global superstars.

However, tennis and all sports are about more than just bringing in the fans to the live events. Sponsorship deals are highly lucrative for players and, in this case, for the ATP and WTA tennis tours. It is lucrative sponsorship deals which create prize money worth fighting for, which help to draw in the best players and this, in turn, helps to draw in the fans and the TV companies.

With technological development, all sports are accessible by wider audiences and tennis is making the most of the fast growth in digital media. Looking at the packaging of tour events and how best to generate revenues through TV rights is a key part of strategic development for the ATP. It goes a long way to showing how even one of the world’s most successful sporting tours is always looking at ways to innovate and adapt to changing economic and social times. Tennis is certainly a sport that has exploited all the opportunities it has had and, through successful advertising, well-organised events and fantastic players, it has created a formidable product, which can compete with any other entertainment product out there. As evidence, the following fact was observed in the Telegraph article:

With technological development, all sports are accessible by wider audiences and tennis is making the most of the fast growth in digital media. Looking at the packaging of tour events and how best to generate revenues through TV rights is a key part of strategic development for the ATP. It goes a long way to showing how even one of the world’s most successful sporting tours is always looking at ways to innovate and adapt to changing economic and social times. Tennis is certainly a sport that has exploited all the opportunities it has had and, through successful advertising, well-organised events and fantastic players, it has created a formidable product, which can compete with any other entertainment product out there. As evidence, the following fact was observed in the Telegraph article:

A 1400 megawatt spike – equivalent to 550,000 kettles being boiled – was recorded at around 9.20pm on that day [6/7/08] as Nadal lifted the trophy. The surge is seen as an indicator of millions viewing the final and then rushing to the kitchen after it is over. The national grid felt a bigger surge after the Nadal victory even than at half time during the same year’s Champions League final between Manchester United and Chelsea.

Tennis top guns driving ATP revenues BBC News, Bill Wilson (20/1/14)

The top 20 sporting moments of the noughties: The 2008 Wimbledon Final The Telegraph, Mark Hodgkinson (14/12/09)

The global tennis industry in numbers BBC News (22/1/14)

Questions

- How does tennis generate its revenue?

- In which market structure would you place the sport of tennis?

- What are the key features of the ATP tour which have allowed it to become so successful? Can other sports benefit from exploiting similar things?

- How has technological development created more opportunities for tennis to generate increased revenues?

- Can game theory be applied to tennis and, if so, in what ways?

- Why does sponsorship of the ATP tour play such an important role in the business of tennis?

- How important is (a) product differentiation and (b) advertising in sport?

In December 2013, Uruguay passed a law permitting the growing, distribution and consumption of marijuana. The legislation comes into effect in April 2014. The state will regulate the industry to ensure good quality strains of the crop are grown and sold. It will also tax the industry.

In December 2013, Uruguay passed a law permitting the growing, distribution and consumption of marijuana. The legislation comes into effect in April 2014. The state will regulate the industry to ensure good quality strains of the crop are grown and sold. It will also tax the industry.

Uruguay is the first country to legalise cannabis, but in July 2012, Colorado and Washington states in the USA passed laws permitting the sale and possession of small amounts of the drug for recreational use. (It was already legal to possess the drug for medical use.) The laws took effect a few months later. It is heavily taxed, however, especially in Washington, where it is taxed at a rate of 25% three times over: when it is sold to the processor; when the processor sells it to the retailer; and when the retailer sells it to the consumer. In Massachusetts, Nevada and Oregon, medical cannabis shops will be permitted to open this year. In the Netherlands, although the sale of cannabis is still illegal, ‘coffee shops’ are permitted to sell people up to 5 grams per day.

So should cannabis be legalised? People have very strong views on the subject and this can make a calm assessment of the issue more difficult. The economist’s approach to legalising cannabis involves seeking to identify and measure the costs and benefits of doing so. If the benefits exceed the costs, then it should be legalised; if not, it should remain illegal (or made illegal). The problem is that the size of the costs and benefits are not easy calculate as they involve estimates of things such as consumption levels, tax revenues, crime reduction, the effects on the consumption of other drugs, including legal drugs such as alcohol and tobacco.

Nevertheless, various estimates of these costs and benefits have been made and provide a basis for discussion.

Possible benefits of cannabis legalisation include: increased tax revenues for the government; reduction in crime, and hence reduction in law enforcement and prison costs; encouraging people with addiction problems to seek help, as they would not fear arrest; reduction in the price, benefiting users; regulating quality of the drug; reducing the consumption of alcohol and more dangerous drugs if these are substitutes for cannabis; moral arguments concerning freedom of individuals to choose their lifestyle.

Possible costs include: increased consumption of cannabis, with attendant health and social side effects; increased consumption of other drugs if they are complements, or if cannabis is an ‘entry level’ drug to harder drugs; moral objections to drug taking.

Clearly some of these costs and benefits are easier to measure than others. Moral arguments are almost impossible to assess quantitatively, even when various underlying moral standpoints are agreed.

The following articles look at recent events and at the arguments, both economic and non-economic.

Articles

As Uruguay moves to legalise cannabis, is the ‘war on drugs’ finished? Metro (20/1/14)

Regulating the sale of marijuana: Global perspective Journalist’s Resource, John Wihbey (17/1/14)

Next Step in Uruguay: Competitive, Quality Marijuana Independent European Daily Express (IEDE) (12/1/14)

U.S. support for legalization of marijuana at an all-time HIGH Mail Online, Anna Edwards (7/1/14)

14 Ways Marijuana Legalization Could Boost The Economy Huffington Post, Harry Bradford (7/11/12)

Colorado pot legalization: 30 questions (and answers) The Denver Post, John Ingold (13/12/12)

Economists Predict Marijuana Legalization Will Produce ‘Public-Health Benefits’ Forbes, Jacob Sullum (1/11/13)

Papers

Economics of Cannabis Legalization Hemp Today, Dale Gieringer (10/10/93)

Pros & Cons of Legalizing Marijuana About.com: US Liberal Politics, Deborah White

Would Marijuana Legalization Increase the Demand for Marijuana? About.com: Economics, Mike Moffatt

Time to Legalize Marijuana? – 500+ Economists Endorse Marijuana Legalization About.com: Economics, Mike Moffatt

A cost benefit analysis of cannabis legalisation Institute for Social and Economic Research, University of Essex

Licensing and regulation of the cannabis market in England and Wales: Towards a cost–benefit analysis Institute for Social and Economic Research, University of Essex, Mark Bryan, Emilia Del Bono and Stephen Pudney (9/13)

What Can We Learn from the Dutch Cannabis Coffeeshop Experience? Rand Drug Policy Research Center, Robert J. MacCoun (7/10)

Podcast

Licensing and regulating the cannabis market in England and Wales Institute for Social and Economic Research, University of Essex, Stephen Pudney (15/9/13)

Questions

- If a country legalises cannabis, what is likely to happen to the price of cannabis? Use a demand and supply diagram to illustrate your argument, considering the effects on both demand and supply. How are the price elasticities of demand and supply relevant to your answer?

- What externalities are there from drug use?

- What externalities are there from making cannabis illegal?

- Distinguish between complementary and substitute goods for cannabis? How is the demand for these likely to be affected by legalising cannabis?

- Go through each of the benefits and costs of legalising cannabis and identify difficulties that might be experienced in quantifying these costs and benefits?

- If cannabis were legalised, how would you set about determining the optimum rate of tax on cannabis production, processing, distribution and sale?

- Consider the arguments for and against legalising cannabis from the perspective of (a) a free-market liberal and (b) a social democrat who sees government intervention as an important means of achieving various social goals.

What does it take to create a successful business? From the looks of it: mud, electric barbed wire, icy water, enormous walls to climb, big jumps to make, team work and complete exhaustion – the recipe for every successful business.

What does it take to create a successful business? From the looks of it: mud, electric barbed wire, icy water, enormous walls to climb, big jumps to make, team work and complete exhaustion – the recipe for every successful business.