In the last few years there have been growing concerns (see here for example) that markets in the USA are becoming increasingly dominated by a small number of firms. It is feared that the result of this will be a reduction in competition. Consistent with this, evidence suggests that the profits these firms make have increased. Last month The Economist and the Resolution Foundation published evidence (see references below) suggesting a similar picture may be emerging in Britain.

In the last few years there have been growing concerns (see here for example) that markets in the USA are becoming increasingly dominated by a small number of firms. It is feared that the result of this will be a reduction in competition. Consistent with this, evidence suggests that the profits these firms make have increased. Last month The Economist and the Resolution Foundation published evidence (see references below) suggesting a similar picture may be emerging in Britain.

The Economist divided the British economy into 600 sub-sectors and found that in 58% of these the share of total revenue accruing to the 4 biggest firms had increased since 2008. The Resolution Foundation found a similar picture, especially in manufacturing industries where from 2004-16 the top five firms’ share of total revenue increased by over 10%.

Economic theory would suggest that as markets become more concentrated prices are likely to rise and The Economist cites research showing that mark-ups charged by firms in Britain have indeed risen. In addition to consumers facing higher prices, there is also concern that the lack of competition both in the USA and the UK is leading to lower wages being paid to workers. On the other hand, unlike in the USA, the evidence from the UK does not so far suggest there has also been an increase in corporate profits. Instead, it appears that the more successful firms’ profits have increased at the expense of their rivals.

This evidence on profits is line with a number of arguments that suggest we should perhaps be less concerned when markets are dominated by a small number of firms. Large firms may benefit from economies of scale and, being sufficiently large may be necessary for firms to innovate in new products and processes. Furthermore, high market shares may result from the competitive process as a reward for a firm developing a unique product or being more efficient than its rivals.

The Economist cites the supermarket industry as an example where concentrated is high, but competition is intense. Interestingly, this is a market where the British competition authorities have previously been concerned about the level of competition and spent considerable amounts of time investigating.

Despite these two opposing viewpoints, overall, The Economist argues strongly that we should be concerned about the situation in Britain. Not only are prices too high and wages too low, but growth in productivity is slow, even for the leading firms. Furthermore, they make clear that the situation may worsen following Brexit. It is argued that:

leaving the EU’s single market and customs union would reduce trade, easing competitive pressure from abroad.

This is consistent with evidence that joining the EC in the mid 1970s increased foreign competition in the UK and helped to end the low productivity growth that had plagued the economy since the 1930s.

Furthermore, it is suggested that:

to attract investment the government might look more favourably on proposed mergers—and loosening regulations would be easier outside the EU’s competition regime.

Therefore, it is clear that in the future there will be a vital role for the UK’s competition authority to remain independent of political objectives and aim to promote competition. In particular, they must prevent mergers that raise concentration and harm competition and intervene if they believe firms are abusing their dominant positions. Of course, following Brexit the case load of the competition authority in the UK will increase dramatically as they have to take on cases previously dealt with by the European Commission. One estimate is that it will need to look at around 40% more merger cases. It will certainly be interesting to see how competition in markets in Britain evolves over the next few years and the role competition policy plays in regulating this process.

Articles

Questions

- Outline the ways in which concentration in a market is usually measured.

- Explain the different price levels that arise under the alternative models of market structure.

- Why do you think competition is currently so intense in the supermarket industry?

The term ‘Google it’ is now part of everyday language. If there is ever something you don’t know, the quickest, easiest, most cost-effective and often the best way to find the answer is to go to Google. While there are many other search engines that provide similar functions and similar results, Google was revolutionary as a search engine and as a business model.

The term ‘Google it’ is now part of everyday language. If there is ever something you don’t know, the quickest, easiest, most cost-effective and often the best way to find the answer is to go to Google. While there are many other search engines that provide similar functions and similar results, Google was revolutionary as a search engine and as a business model.

This article by Tim Harford, writing for BBC News, looks at the development of Google as a business and as a search engine. One of the reasons why Google is so effective for individuals and businesses is the speed with which information can be obtained. It is therefore used extensively to search key terms and this is one of the ways Google was able to raise advertising revenue. The business model developed to raise finance has therefore been a contributing factor to the decline in newspaper advertising revenue.

Google began the revolution in terms of search of engines and, while others do exist, Google is a classic example of a dominant firm and that raises certain problems. The article looks at many aspects of Google.

Just google it: The student project that changed the world BBC News, Tim Harford (27/03/17)

Questions

- Is Google a natural monopoly? What are the characteristics of a natural monopoly and how does this differ from a monopoly?

- Are there barriers to entry in the market in which Google operates?

- What are the key determinants of demand for Google from businesses and individuals?

- Why do companies want to advertise via Google? How might the reasons differ from advertising in newspapers?

- Why has there been a decline in advertising in newspapers? How do you think this has affected newspapers’ revenue and profits?

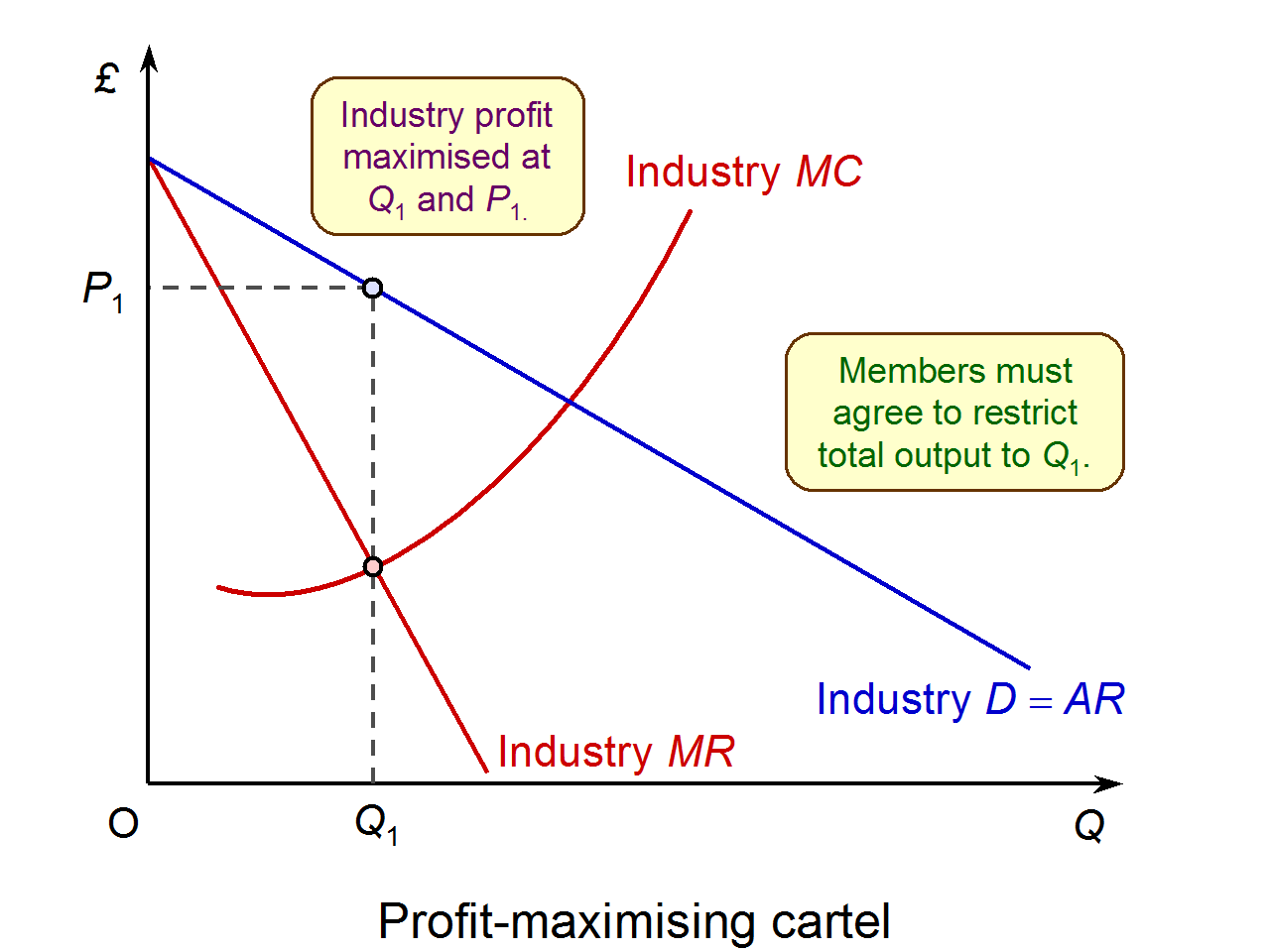

Price fixing agreements between firms are one of the most serious breaches of competition law. Therefore, if detected, the firms involved face substantial fines (see here for an example), plus there is also the potential for jail sentences and director disqualification for participants. However, due to their secretive nature and the need for hard evidence of communication between firms, it is difficult for competition authorities to detect cartel activity.

Price fixing agreements between firms are one of the most serious breaches of competition law. Therefore, if detected, the firms involved face substantial fines (see here for an example), plus there is also the potential for jail sentences and director disqualification for participants. However, due to their secretive nature and the need for hard evidence of communication between firms, it is difficult for competition authorities to detect cartel activity.

In order to assist detection, competition authorities offer leniency programmes that guarantee full immunity from fines to the first participant to come forward and blow the whistle on the cartel. This has become a key way in which competition authorities detect cartels. Recently, competition authorities have introduced a number of new tools to try to enhance cartel detection.

First, the European Commission launched an online tool to make it easier for cartels to be reported to them. This tool allows anonymous two-way communication in the form of text messages between a whistle blower and the Commission. The Commissioner in charge of competition policy, Margrethe Vestager, stated that:

First, the European Commission launched an online tool to make it easier for cartels to be reported to them. This tool allows anonymous two-way communication in the form of text messages between a whistle blower and the Commission. The Commissioner in charge of competition policy, Margrethe Vestager, stated that:

If people are concerned by business practices that they think are wrong, they can help put things right. Inside knowledge can be a powerful tool to help the Commission uncover cartels and other anti-competitive practices. With our new tool it is possible to provide information, while maintaining anonymity. Information can contribute to the success of our investigations quickly and more efficiently to the benefit of consumers and the EU’s economy as a whole.

Second, the UK Competition and Markets Authority (CMA) has launched an online and social media campaign to raise awareness of what is illegal under competition law and to encourage illegal activity to be reported to them. The CMA stated that:

Second, the UK Competition and Markets Authority (CMA) has launched an online and social media campaign to raise awareness of what is illegal under competition law and to encourage illegal activity to be reported to them. The CMA stated that:

Cartels are both harmful and illegal, and the consequences of breaking the law are extremely serious. That is why we are launching this campaign – to help people understand what cartel activity looks like and how to report it so we can take action.

This campaign is on the back of the CMA’s own research which found that less that 25% of the businesses they surveyed believed that they knew competition law well. Furthermore, the CMA is now offering a reward of up to £100,000 and guaranteed anonymity to individuals who provide them with information.

It will be fascinating to see the extent to which these new tools are used and whether they aid the competition authorities in detecting and prosecuting cartel behaviour.

Articles

CMA launches crackdown on cartels as illegal activity rises The Telegraph, Bradley Gerrard (20/03/17)

European Commission launches new anonymous whistleblower tool, but who would use it? Competition Policy Blog, Andreas Stephan (21/03/17)

CMA launches campaign to crackdown on cartels Insider Media Limited, Karishma Patel (21/03/17)

Questions

- Why do you think leniency programmes are a key way in which competition authorities detect cartels?

- Who do you think is most likely to blow the whistle on a cartel (see the article above by A.Stephan)?

- Why is it worrying that so few businesses appear to know competition law well?

- Which of the two tools do you think is most likely to enhance cartel detection? Explain why.

As an avid sport’s fan, Sky Sports and Eurosport are must haves for me! In the days leading up to the end of January, it was a rather tense time in my house with the prospect of Eurosport being removed from anyone who was a Sky TV subscriber. Thankfully the threat has now gone and tranquility returns, but what was going on behind the scenes?

As an avid sport’s fan, Sky Sports and Eurosport are must haves for me! In the days leading up to the end of January, it was a rather tense time in my house with the prospect of Eurosport being removed from anyone who was a Sky TV subscriber. Thankfully the threat has now gone and tranquility returns, but what was going on behind the scenes?

Whether you have Sky TV, BT, Virgin or any other, we generally take it for granted that we can pick and choose the channels we want, pay our subscription to our provider and happily watch our favourite shows. However, behind the scenes there is a web of deals. While Sky own many channels, such as Sky Sports; BT own others and there are a range of other companies that own the rest. Some companies pay Sky for their channels to be shown, while Sky pays other companies for access to their channels.

One such company is Discovery, which owns a range of channels including TLC, Eurosport, DMAX and Animal planet. Discovery then sells these channels to providers, such as Sky and Virgin, who pay a price for access. The problem was that Sky and Discovery had failed to reach an agreement for these channels and as the deadline of 31st January 2017 loomed, it became increasingly possible that Discovery would simply remove its channels from Sky. This would mean that Sky customers would no longer have access to these channels, while customers with other providers would continue to watch them, as companies such as Virgin still had an agreement in place.

The issue was money. Hours before the deadline, a deal was finally reached such that Discovery will now keep its programmes on Sky for ‘years to come’. Discovery has indicated the final deal was better than had originally been proposed, while Sky indicate that the deal accepted by Discovery was the same as had previously been offered! Although no details of the financial agreement have been released, it seems likely that either Sky increased the price they were willing to pay or Discovery lowered the price it was asking for. Both companies stood to lose if the dispute was not settled, but it’s interesting to consider which company was at more risk. Following the announcement that a deal had been struck, Discovery shares rose by 2.5 per cent, while Sky’s share remained unchanged.

The issue was money. Hours before the deadline, a deal was finally reached such that Discovery will now keep its programmes on Sky for ‘years to come’. Discovery has indicated the final deal was better than had originally been proposed, while Sky indicate that the deal accepted by Discovery was the same as had previously been offered! Although no details of the financial agreement have been released, it seems likely that either Sky increased the price they were willing to pay or Discovery lowered the price it was asking for. Both companies stood to lose if the dispute was not settled, but it’s interesting to consider which company was at more risk. Following the announcement that a deal had been struck, Discovery shares rose by 2.5 per cent, while Sky’s share remained unchanged.

While Sky said that viewing figures on Discovery’s channels had been falling and that it had been over-paying for years, it seems likely that if a deal had not been reached, millions of Sky customers may have considered switching to other providers, who were still able to show Discovery channels. Although Sky has been looking to cut its costs and one way is to cut the price it pays for channels, failure to reach an agreement may have cost it a significant sum in lost revenue, as channels such as Eurosport are hugely popular.

Discovery claimed that the price Sky was paying them was not fair and that it was paying them less for its channels that it did 10 years ago. Susanna Dinnage, Discovery’s Managing Director in the UK said:

“We believe Sky is using what we consider to be its dominant market position to further its own commercial interest over those of viewers and independent broadcasters. The vitality of independent broadcasters like Discovery and plurality in TV is under threat.”

Sky claimed that Discovery was demanding close to £1bn for its programmes and that given that these channels were losing viewers, this price was unrealistic. A spokesman said:

Sky claimed that Discovery was demanding close to £1bn for its programmes and that given that these channels were losing viewers, this price was unrealistic. A spokesman said:

“Despite our best efforts to reach a sensible agreement, we, like many other platforms and broadcasters across Europe, have found the price expectations for the Discovery portfolio to be completely unrealistic. Discovery’s portfolio of channels includes many which are linear-only where viewing is falling …

Sky has a strong track record of understanding the value of the content we acquire on behalf of our customers, and as a result we’ve taken the decision not to renew this contract on the terms offered …

We have been overpaying Discovery for years and are not going to anymore. We will now move to redeploy the same amount of money into content we know our customers value.”

Here we have a classic case of two firms in negotiation; each with a lot to lose, but both wanting the best outcome. There are hundreds of channels with millions of programmes and hence it is a competitive market. So why was it that Discovery could pose such a threat to the huge broadcaster? The following articles consider the dispute and the eleventh hour agreement.

Discovery strikes deal to keep channels on Sky BBC News (1/2/17)

Discovery channel strikes last-minute deal with Sky to stay on TV, saving Animal Planet and Eurosport Independent, Aatif Sulleyman (1/2/17)

Eurosport stays o Sky after late deal is struck with hours to spare between broadcasting giant and Discovery Mail Online, Kieran Gill (1/2/17)

Discovery averts UK blackout with Sky in last-minute deal Bloomberg, Rebecca Penty, Joe Mayes and Gerry Smith (1/2/17)

Is Sky losing Discovery? Eurosport, Animal Planet and other fan favourite set to stay International Business Times, Owen Hughes (1/2/17)

Discovery goes to war with Sky over channel fees with blackout threat The Telegraph, Christopher Williams (25/1/17)

Questions

- Can you use game theory to outline the ‘game’ that Sky and Discovery were playing?

- Is the ‘threat’ of stopping access to channels credible?

- Although we don’t know the final financial settlement, why would Sky have had a reason to increase the price it paid to Discovery?

- Why would it be in Discovery’s interests to accept the deal that Sky offered?

- Susanna Dinnage suggested that Sky was using its dominant market position. What does this mean and how does this suggest that Sky might be able to behave?

- What type of market structure is the pay-TV industry? Think about it in terms of broadcasters, channels and programmes as you might get very different answers!

Earlier this week FIFA, the world governing body of football, announced plans to expand the World Cup from 32 to 48 teams starting in 2026. It is fair to say that this has been met with mixed reactions, in part due to the politics and money involved. However, for an economist one particularly interesting question is how the change will affect the incentives of the teams taking part in the competition.

Earlier this week FIFA, the world governing body of football, announced plans to expand the World Cup from 32 to 48 teams starting in 2026. It is fair to say that this has been met with mixed reactions, in part due to the politics and money involved. However, for an economist one particularly interesting question is how the change will affect the incentives of the teams taking part in the competition.

As a result of the change in the first stage of the competition, teams will be play the two other teams in their group. The best two teams in the group will then progress to the next round with the worst team going home. This is in contrast to the current format where the best two teams from a group of four go through to the next round.

Currently, in the final round of group matches all four of the teams in the group play simultaneously. However, an immediate implication of the new format is that this will no longer be the case. Instead, one of the teams will have finished their group matches before the other two teams play each other. This could have important implications for the incentives of the teams involved. To see this we can recall a very famous match played under similar circumstances between West Germany and Austria at the 1982 World Cup.

The results of the earlier group games meant that if West Germany beat Austria by one or two goals to nil both teams would progress to the next round. Any other result would mean that Algeria progressed at the expense of one of these two teams. The way in which the match played out was that West Germany scored early on and much of the rest of the game descended into farce. Both teams refused to attack or tackle their opponents, as they had no incentive to so (see here for some clips of the action, or lack of!).

The results of the earlier group games meant that if West Germany beat Austria by one or two goals to nil both teams would progress to the next round. Any other result would mean that Algeria progressed at the expense of one of these two teams. The way in which the match played out was that West Germany scored early on and much of the rest of the game descended into farce. Both teams refused to attack or tackle their opponents, as they had no incentive to so (see here for some clips of the action, or lack of!).

There is no evidence to suggest that West Germany and Austria had come to a formal agreement to do this. Instead, the two teams appear to have simply had a mutual understanding that refraining from competing would be beneficial for both of them.

This is exactly what economists refer to as tacit collusion – a mutual understanding that refraining from competition and keeping prices high benefits all firms in the market. Much like the fans who had to sit through the farce of a game (you can hear the frustration of the crowd in the video clip linked to above), the end result is harm to consumers who have to pay the higher prices or go without the product.

For this reason governments use competition policy to try to stop situations arising in markets that make the possibility of tacit collusion more likely. One way in which this is done is by preventing mergers in markets where tacit collusion appears possible and would be facilitated by the reduction in the number of firms as a result of the merger. The equivalent for the World Cup would be preventing a change in the format of the competition.

An alternative approach is to tinker with the rules of the game in order to make collusion harder. FIFA seems to have some awareness of the possibility of doing this as it is suggesting that it may require all tied games to extra-time and then a penalty shoot-out in order to determine a winner. Clearly, this would go at least some way to alleviating concerns about tacit collusion in the final group matches because coordinating on a draw would no longer be possible. In a similar fashion, competition authorities can also intervene in markets to change the rules of the game (see for example the recent intervention in the UK cement industry).

Therefore, more generally, the World Cup example highlights the fact that variations in the structure of markets and the rules of the game can have significant effects on firms’ incentives and this can have important consequences for market outcomes. It will certainly be fascinating to see what rules are imposed for the 2026 World Cup and how the teams taking part respond.

Articles

World Cup: Fifa to expand competition to 48 teams after vote BBC News (10/1/17)

How will a 48-team World Cup work? Fifa’s plan for 2026 explained The Guardian, Paul MacInnes (10/1/17)

The Disgrace of Gijón and the 48-team FIFA World Cup Mike or the Don (12/1/17)

Questions

- What is the difference between tacit collusion and a cartel?

- Why does a reduction in the number of firms in a market make collusion easier?

- What other factors make collusion more likely?

- How does competition policy try to prevent the different forms of collusion?