Back in October, we examined the rise in oil prices. We said that, ‘With Brent crude currently at around $85 per barrel, some commentators are predicting the price could reach $100. At the beginning of the year, the price was $67 per barrel; in June last year it was $44. In January 2016, it reached a low of $26.’ In that blog we looked at the causes on both the demand and supply sides of the oil market. On the demand side, the world economy had been growing relatively strongly. On the supply side there had been increasing constraints, such as sanctions on Iran, the turmoil in Venezuela and the failure of shale oil output to expand as much as had been anticipated.

But what a difference a few weeks can make!

Brent crude prices have fallen from $86 per barrel in early October to just over $50 by the end of the year – a fall of 41 per cent. (Click here for a PowerPoint of the chart.) Explanations can again be found on both the demand and supply sides.

On the demand side, global growth is falling and there is concern about a possible recession (see the blog: Is the USA heading for recession?). The Bloomberg article below reports that all three main agencies concerned with the oil market – the U.S. Energy Information Administration, the Paris-based International Energy Agency and OPEC – have trimmed their oil demand growth forecasts for 2019. With lower expected demand, oil companies are beginning to run down stocks and thus require to purchase less crude oil. Fracking (Source: US Bureau of Land Management Environmental Assessment, public domain image)

On the supply side, US shale output has grown rapidly in recent weeks and US output has now reached a record level of 11.7 million barrels per day (mbpd), up from 10.0 mbpd in January 2018, 8.8 mbpd in January 2017 and 5.4 mbpd in January 2010. The USA is now the world’s biggest oil producer, with Russia producing around 11.4 mpbd and Saudi Arabia around 11.1 mpbd.

Total world supply by the end of 2018 of around 102 mbpd is some 2.5 mbpd higher than expected at the beginning of 2018 and around 0.5 mbpd greater than consumption at current prices (the remainder going into storage).

So will oil prices continue to fall? Most analysts expect them to rise somewhat in the near future. Markets may have overcorrected to the gloomy news about global growth. On the supply side, global oil production fell in December by 0.53 mbpd. In addition OPEC and Russia have signed an accord to reduce their joint production by 1.2 mbpd starting this month (January). What is more, US sanctions on Iran have continued to curb its oil exports.

But whatever happens to global growth and oil production, the future price will continue to reflect demand and supply. The difficulty for forecasters is in predicting just what the levels of demand and supply will be in these uncertain times.

Oil prices have been rising in recent weeks. With Brent crude currently at around $85 per barrel, some commentators are predicting the price could reach $100. At the beginning of the year, the price was $67 per barrel; in June last year it was $44. In January 2016, it reached a low of $26. But what has caused the price to increase?

On the demand side, the world economy has been growing relatively strongly. Over the past three years, global growth has averaged 3.5%. This has helped to offset the effects of more energy efficient technologies and the gradual shift away from oil to alternative sources of energy.

On the supply side, there have been growing constraints.

The predicted resurgence of shale oil production, after falls in both output and investment when oil prices were low in 2016, has failed to materialise as much as expected. The reason is that pipeline capacity is limited and there is very little scope for transporting more oil from the major US producing area – the Permian basin in West Texas and SE New Mexico. There are similar pipeline capacity constraints from Canadian shale fields. The problem is compounded by shortages of labour and various inputs.

But perhaps the most serious supply-side issue is the renewed sanctions on Iranian oil exports imposed by the Trump administration, due to come into force on 4 November. The USA is also putting pressure on other countries not to buy Iranian oil. Iran is the world’s third largest oil exporter.

Also, there has been continuing turmoil in the Venezuelan economy, where inflation is currently around 500 000 per cent and is expected to reach 1 million per cent by the end of the year. Consequently, the country’s oil output is down. Production has fallen by more than a third since 2016. Venezuela was the world’s third largest oil producer.

Winners and losers from high oil prices

The main gainers from high oil prices are the oil producing countries, such as Russia and Saudi Arabia. It will also encourage investment in oil exploration and new oil wells, and could help countries, such as Colombia, with potential that is considered underexploited. However, given that the main problem is a lack of supply, rather than a surge in demand, the gains will be more limited for those countries, such as the USA and Canada, suffering from supply constraints. Clearly there will be no gain for Iran.

In terms of losers, higher oil prices are likely to dampen global growth. If the oil price reaches $100 per barrel, global growth could be around 0.2 percentage points lower than had previously been forecast. In its latest World Economic Outlook, published on 8 October, the IMF has already downgraded its forecast growth for 2018 and 2019 to 3.7% from the 3.9% it forecast six months ago – and this forecast is based on the assumption that oil prices will be $69.38 a barrel in 2018 and $68.76 a barrel in 2019.

Clearly, the negative effect will be greater, the larger a country’s imports are as a percentage of its GDP. Countries that are particularly vulnerable to higher oil prices are the eurozone, Japan, China, India and most other Asian economies. Lower growth in these countries could have significant knock-on effects on other countries.

Consumers in advanced oil-importing countries would face higher fuel costs, accounting for an additional 0.3 per cent of household spending. Inflation could rise by as much as 1 percentage point.

The size of the effects depends on just how much oil prices rise and for how long. This depends on various demand- and supply-side factors, not least of which in the short term is speculation. Crucially, global political events, and especially US policies, will be the major driving factor in what happens.

Draw a supply and demand diagram to illustrate what has been happening to oil prices in the past few weeks and what is likely to happen in the coming weeks.

What is the significance of the price elasticity of demand and supply in determining the size of oil price increase?

What determines (a) the price elasticity of demand for oil; (b) the income elasticity of demand for oil; (c) the price elasticity of supply of oil?

Why might oil prices overshoot the equilibrium price that reflects changed demand and supply conditions?

Use demand and supply diagrams to illustrate (a) the destabilising effects that speculation could have on oil prices; (b) a stabilising effect.

What industries might gain from higher oil prices and why?

What would OPEC’s best policy be in the current circumstances? Explain.

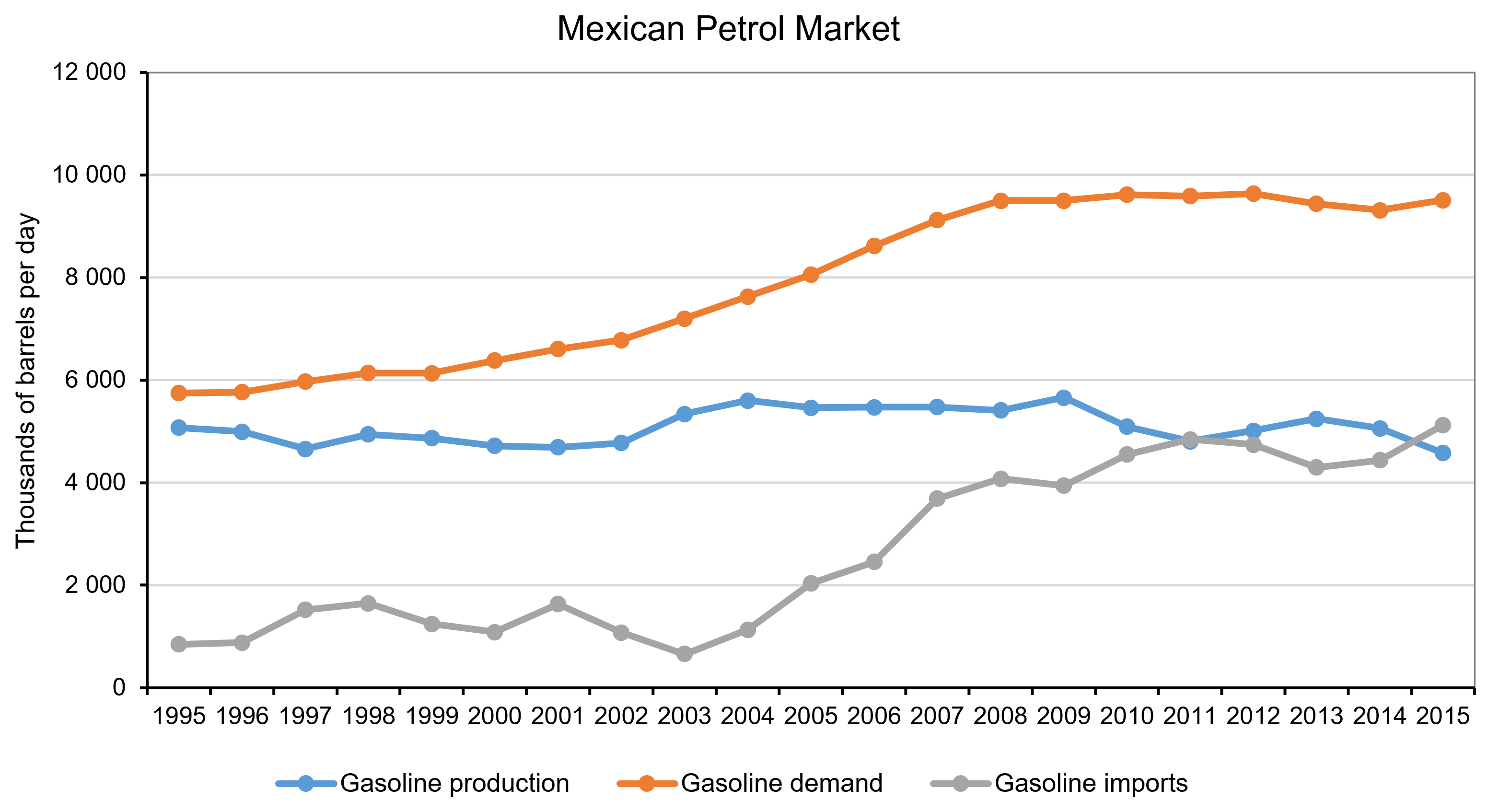

So here we are, summer is over (or almost over if you’re an optimist) and we are sitting in front of our screens reminiscing about hot sunny days (at least I do)! There is no doubt, however: a lot happened in the world of politics and economics in the past three months. The escalation of the US-China trade war, the run on the Turkish lira, the (successful?) conclusion of the Greek bailout – these are all examples of major economic developments that took place during the summer months, and which we will be sure to discuss in some detail in future blogs. Today, however, I will introduce a topic that I am very interested in as a researcher: the liberalisation of energy markets in developing countries and, in particular, Mexico.

Why Mexico? Well, because it is a great example of a large developing economy that has been attempting to liberalise its energy market and reverse price setting and monopolistic practices that go back several decades. Until very recently, the price of petrol in Mexico was set and controlled by Pemex, a state monopolist. This put Pemex under pressure since, as a sole operator, it was responsible for balancing growing demand and costs, even to the detriment of its own finances.

The petrol (or ‘gasoline’) price liberalisation started in May 2017 and took place in stages – starting in the North part of Mexico and ending in November of the same year in the central and southern regions of the country. The main objective was to address the notable decrease in domestic oil production that put at risk the ability of the country to meet demand; as well as Mexico’s increasing dependency on foreign markets affected by the surge of the international oil price. The government has spent the past five years trying to create a stronger regulatory framework, while easing the financial burden on the state and halting the decline in oil reserves and production. Unsurprisingly, opening up a monopolistic market turns out to be a complex and bumpy process.

Source: Author’s calculations using data from the Energy Information Bank, Ministry of Energy, Mexico

Despite all the reforms, retail petrol prices have kept rising. Although part of this price rise is demand-driven, an increasing number of researchers highlight the significance of the distribution of oil-related infrastructure in determining price outcomes at the federal and regional (state) level. Saturation and scarcity of both distribution and storage infrastructure are probably the two most significant impediments to opening the sector up to competition (Mexico Institute, 2018). You see, the original design of these networks and the deployment of the infrastructure was not aimed at maximising efficiency of distribution – the price was set by the monopolist and, in a way that was compliant with government policy (Mexico Institute, 2018). Economic efficiency was not always part of this equation. As a result, consumers located in better-deployed areas were subsidising the inherent logistics costs of less ‘well endowed’ regions by facing an artificially higher price than they would have in a competitive market.

But what about now? Do such differences in the allocation of infrastructure between regions lead to location-related differences in the price of petrol? If so, by how much? And, what policies should the government pursue to address such imbalances? These are all questions that I explore in one of my recent working papers titled ‘Widening the Gap: Lessons from the aftermath of the energy market reform in Mexico’ (with Hugo Vallarta) and I will be sharing some of the answers with you in a future blog.

Oil prices are determined by demand and supply. Changes in oil prices are the result of shifts in demand and/or supply, with the size of the price change depending on the size of the shift and the price elasticity of demand and supply.

Some of the shifts are long term, with the price of oil varying from year to year or even moving in a particular direction for longer periods of time. Thus the opening up of new supplies, such as from fracking wells, can lead to a long-term fall in oil prices, while agreements by, say, OPEC to curb output can lead to a long-term rise in prices (see the blogs The oil see-saw, OPEC deal pushes up oil prices and An oil glut).

Medium and long-term price movements can also reflect medium and long-term changes in demand, such as a recession – oil prices fell dramatically as the world economy slid into recession in 2008/9 and then recovered as the global economy recovered.

Another long-term factor is the development of substitutes, such as renewable energy, which can reduce the demand for oil; another is developments that economise on power, such as more fuel-efficient vehicles and machines.

But oil prices do not just reflect these long-term movements in demand and supply. They also reflect daily and weekly movements as demand and supply respond to global and national events.

Two such events occurred at the end of August/beginning of September this year. The first was Hurricane Harvey. Even though it was downgraded to a tropical storm as it made landfall across the coast of the Gulf of Mexico, it dumped massive amounts of rain on southern Texas and Louisiana. This disrupted oil drilling and refining, shutting down a quarter of the entire US refining capacity. The initial effect was a surge in US oil prices in late August as oil production in much of Texas shut down and a rise in petrol prices as supplies from refineries fell.

Then prices fell back again in early September as production and refining resumed and as it became apparent that there had been less damage to oil infrastructure than initially feared. Also the USA tapped into some of its strategic oil reserves to make up for the shortfall in supply.

Then in early September, the North Koreans tested a hydrogen bomb – much larger than the previous atom bombs it had tested. This prompted fears of US retaliation and heightened tensions in the region. As the Reuters article states:

That put downward pressure on crude as traders moved money out of oil – seen as high-risk markets – into gold futures, traditionally viewed as a safe haven for investors. Spot gold prices rose for a third day, gaining 0.9 per cent on Monday

Quite large daily movements in oil prices are not uncommon as traders respond to such events. A major determinant of short-term demand is expectations, and nervousness about events can put substantial downward pressure on oil prices if it is felt that there could be a downward effect on the global economy – or substantial upward pressure if it is felt that supplies might be disrupted. Often markets over-correct, with prices moving back again as the situation becomes clearer and as nervousness subsides.

What are the determinants of the price elasticity of demand for oil?

Search news articles to find some other examples of short-term movements in oil prices as markets responded to some political or natural event.

Why do markets often over-correct?

Explain the long-term oil price movements over the past 10 years.

Why is gold seen as a ‘safe haven’?

If refineries buy oil from oil producers, what would determine the net effect on oil prices of a decline in oil production and a decline in demand for oil by the refineries?

What role does speculation play in determining oil prices? Explain how such speculation could (a) reduce price volatility; (b) increase price volatility. Under what circumstances is (b) more likely than (a)?

The recent low price of oil has been partly the result of faltering global demand but mainly the result of increased supply from shale oil deposits. The increased supply of shale oil has not been offset by a reduction in OPEC production. Quite the opposite: OPEC has declared that it will not cut back production even if the price of oil were to fall to $30 per barrel.

We looked at the implications for the global economy in the post, A crude indicator of the economy (Part 2). We also looked at the likely effect on oil prices over the longer term and considered what the long-run supply curve might look like. Here we examine the long-run effect on prices in more detail. In particular, we look at the arguments of two well-known commentators, Jim O’Neill and Anatole Kaletsky, both of whom have articles on the Project Syndicate site. They disagree about what will happen to oil prices and to energy markets more generally in 2015 and beyond.

Jim O’Neill argues that with shale oil production becoming unprofitable at the low prices of late 2014/early 2015, the oil price will rise. He argues that a good indicator of the long-term equilibrium price of oil is the five-year forward price, which is much less subject to speculation and is more reflective of the fundamentals of demand and supply. The five-year forward price is around $80 per barrel – a level to which O’Neill thinks oil prices are heading.

Anatole Kaletsky disagrees. He sees $50 per barrel as a more likely long-term equilibrium price. He argues that new sources of oil have made the oil market much more competitive. The OPEC cartel no longer has the market power it had from the mid 1970s to the mid 1980s and from the mid 2000s, when surging Chinese demand temporarily created a global oil shortage and strengthened OPEC’s control of prices. Instead, the current situation is more like the period from 1986 to 2004 when North Sea and Alaskan oil development undermined OPEC’s power and made the oil market much more competitive.

Kaletsky argues that in a competitive market, price will equal the marginal cost of the highest cost producer necessary to balance demand and supply. The highest cost producers in this case are the shale oil producers in the USA. As he says:

Under this competitive logic, the marginal cost of US shale oil would become a ceiling for global oil prices, whereas the costs of relatively remote and marginal conventional oilfields in OPEC and Russia would set a floor. As it happens, estimates of shale-oil production costs are mostly around $50, while marginal conventional oilfields generally break even at around $20. Thus, the trading range in the brave new world of competitive oil should be roughly $20 to $50.

So who is right? Well, we will know in twelve months or more! But, in the meantime, try to use economic analysis to judge the arguments by answering the questions below.

For what reasons might the five-year forward price of oil be (a) a good indicator and (b) a poor indicator of the long-term price of oil?

Under O’Neill’s analysis, what would the long-term supply curve of oil look like?

Are shale oil producers price takers? Explain.

Draw a diagram showing the marginal and average cost curves of a swing shale oil producer. Put values on the vertical axis to demonstrate Kaletsky’s arguments. Also put average and marginal revenue on the diagram and show the amount of profit at the maximum-profit point.

Why are shale oil producers likely to have much higher long-run average costs than short-run variable costs? How does this affect Kaletsky’s arguments?

Under Kaletsky’s analysis, what would the long-term supply curve of oil look like?

Criticise Kaletsky’s arguments from O’Neill’s point of view.

Criticise O’Neill’s arguments from Kaletsky’s point of view.

Will OPEC’s policy of not cutting back production help to restore its position of market power?

Why might the fall in the oil price below $50 in early 2015 represent ‘overshooting’? Why does overshooting often occur in volatile markets?

Back in October, we examined the rise in oil prices. We said that, ‘With Brent crude currently at around $85 per barrel, some commentators are predicting the price could reach $100. At the beginning of the year, the price was $67 per barrel; in June last year it was $44. In January 2016, it reached a low of $26.’ In that blog we looked at the causes on both the demand and supply sides of the oil market. On the demand side, the world economy had been growing relatively strongly. On the supply side there had been increasing constraints, such as sanctions on Iran, the turmoil in Venezuela and the failure of shale oil output to expand as much as had been anticipated.

Back in October, we examined the rise in oil prices. We said that, ‘With Brent crude currently at around $85 per barrel, some commentators are predicting the price could reach $100. At the beginning of the year, the price was $67 per barrel; in June last year it was $44. In January 2016, it reached a low of $26.’ In that blog we looked at the causes on both the demand and supply sides of the oil market. On the demand side, the world economy had been growing relatively strongly. On the supply side there had been increasing constraints, such as sanctions on Iran, the turmoil in Venezuela and the failure of shale oil output to expand as much as had been anticipated. Brent crude prices have fallen from $86 per barrel in early October to just over $50 by the end of the year – a fall of 41 per cent. (Click here for a PowerPoint of the chart.) Explanations can again be found on both the demand and supply sides.

Brent crude prices have fallen from $86 per barrel in early October to just over $50 by the end of the year – a fall of 41 per cent. (Click here for a PowerPoint of the chart.) Explanations can again be found on both the demand and supply sides. Oil prices decline on swelling oversupply, volatile markets

Oil prices decline on swelling oversupply, volatile markets Oil prices have been rising in recent weeks. With Brent crude currently at around $85 per barrel, some commentators are predicting the price could reach $100. At the beginning of the year, the price was $67 per barrel; in June last year it was $44. In January 2016, it reached a low of $26. But what has caused the price to increase?

Oil prices have been rising in recent weeks. With Brent crude currently at around $85 per barrel, some commentators are predicting the price could reach $100. At the beginning of the year, the price was $67 per barrel; in June last year it was $44. In January 2016, it reached a low of $26. But what has caused the price to increase? scope for transporting more oil from the major US producing area – the

scope for transporting more oil from the major US producing area – the  In terms of losers, higher oil prices are likely to dampen global growth. If the oil price reaches $100 per barrel, global growth could be around 0.2 percentage points lower than had previously been forecast. In its

In terms of losers, higher oil prices are likely to dampen global growth. If the oil price reaches $100 per barrel, global growth could be around 0.2 percentage points lower than had previously been forecast. In its  So here we are, summer is over (or almost over if you’re an optimist) and we are sitting in front of our screens reminiscing about hot sunny days (at least I do)! There is no doubt, however: a lot happened in the world of politics and economics in the past three months. The escalation of the US-China trade war, the run on the Turkish lira, the (successful?) conclusion of the Greek bailout – these are all examples of major economic developments that took place during the summer months, and which we will be sure to discuss in some detail in future blogs. Today, however, I will introduce a topic that I am very interested in as a researcher: the liberalisation of energy markets in developing countries and, in particular, Mexico.

So here we are, summer is over (or almost over if you’re an optimist) and we are sitting in front of our screens reminiscing about hot sunny days (at least I do)! There is no doubt, however: a lot happened in the world of politics and economics in the past three months. The escalation of the US-China trade war, the run on the Turkish lira, the (successful?) conclusion of the Greek bailout – these are all examples of major economic developments that took place during the summer months, and which we will be sure to discuss in some detail in future blogs. Today, however, I will introduce a topic that I am very interested in as a researcher: the liberalisation of energy markets in developing countries and, in particular, Mexico. Source: Author’s calculations using data from the Energy Information Bank, Ministry of Energy, Mexico

Source: Author’s calculations using data from the Energy Information Bank, Ministry of Energy, Mexico