The Competition and Markets Authority (CMA) is proposing to launch a formal Market Investigation into anti-competitive practices in the UK’s £2bn veterinary industry (for pets rather than farm animals or horses). This follows a preliminary investigation which received 56 000 responses from pet owners and vet professionals. These responses reported huge rises in bills for treatment and medicines and corresponding rises in the cost of pet insurance.

The Competition and Markets Authority (CMA) is proposing to launch a formal Market Investigation into anti-competitive practices in the UK’s £2bn veterinary industry (for pets rather than farm animals or horses). This follows a preliminary investigation which received 56 000 responses from pet owners and vet professionals. These responses reported huge rises in bills for treatment and medicines and corresponding rises in the cost of pet insurance.

At the same time there has been a large increase in concentration in the industry. In 2013, independent vet practices accounted for 89% of the market; today, they account for only around 40%. Over the past 10 years, some 1500 of the UK’s 5000 vet practices had been acquired by six of the largest corporate groups. In many parts of the country, competition is weak; in others, it is non-existent, with just one of these large companies having a monopoly of veterinary services.

This market power has given rise to a number of issues. The CMA identifies the following:

- Of those practices checked, over 80% had no pricing information online, even for the most basic services. This makes is hard for pet owners to make decisions on treatment.

- Pet owners potentially overpay for medicines, many of which can be bought online or over the counter in pharmacies at much lower prices, with the pet owners merely needing to know the correct dosage. When medicines require a prescription, often it is not made clear to the owners that they can take a prescription elsewhere, and owners end up paying high prices to buy medicines directly from the vet practice.

- Even when there are several vet practices in a local area, they are often owned by the same company and hence there is no price competition. The corporate group often retains the original independent name when it acquires the practice and thus is is not clear to pet owners that ownership has changed. They may think there is local competition when there is not.

Often the corporate group provides the out-of-hours service, which tends to charge very high prices for emergency services. If there is initially an independent out-of-hours service provider, it may be driven out of business by the corporate owner of day-time services only referring pet owners to its own out-of-hours service.

Often the corporate group provides the out-of-hours service, which tends to charge very high prices for emergency services. If there is initially an independent out-of-hours service provider, it may be driven out of business by the corporate owner of day-time services only referring pet owners to its own out-of-hours service.- The corporate owners may similarly provide other services, such as specialist referral centres, diagnostic labs, animal hospitals and crematoria. By referring pets only to those services owned by itself, this crowds out independents and provides a barrier to the entry of new independents into these parts of the industry.

- Large corporate groups have the incentive to act in ways which may further reduce competition and choice and drive up their profits. They may, for example, invest in advanced equipment, allowing them to provide more sophisticated but high-cost treatment. Simpler, lower-cost treatments may not be offered to pet owners.

- The higher prices in the industry have led to large rises in the cost of pet insurance. These higher insurance costs are made worse by vets steering owners with pet insurance to choosing more expensive treatments for their pets than those without insurance. The Association of British Insurers notes that there has been a large rise in claims attributable to an increasing provision of higher-cost treatments.

- The industry suffers from acute staff shortages, which cuts down on the availability of services and allows practices to push up prices.

- Regulation by the Royal College of Veterinary Surgeons (RCVS) is weak in the area of competition and pricing.

The CMA’s formal investigation will examine the structure of the veterinary industry and the behaviour of the firms in the industry. As the CMA states:

In a well-functioning market, we would expect a range of suppliers to be able to inform consumers of their services and, in turn, consumers would act on the information they receive.

Market failures in the veterinary industry

The CMA’s concerns suggest that the market is not sufficiently competitive, with vet companies holding significant market power. This leads to higher prices for a range of vet services. However, the CMA’s analysis suggests that market failures in the industry extend beyond the simple question of market power and lack of competition.

A crucial market failure is asymmetry of information. The veterinary companies have much better information than pet owners. This is a classic principal–agent problem. The agent, in this case the vet (or vet company), has much better information than the principal, in this case the pet owner. This information can be used to the interests of the vet company, with pet owners being persuaded to purchase more extensive and expensive treatments than they might otherwise choose if they were better informed.

The principal–agent problem also arises in the context of the dependant nature of pets. They are the ones receiving the treatment and, in this context, are the principals. Their owners are the ones acquiring the treatment for them and hence are the pets’ agents. The question is whether the owners will always do the best thing for their pets. This raises philosophical questions of animal rights and whether owners should be required to protect the interests of their pets.

Another information issue is the short-term perspective of many pet owners. They may purchase a young and healthy pet and assume that it will remain so. However, as the pet gets older, it is likely to face increasing health issues, with correspondingly increasing vet bills. But many owners do not consider such future bills when they purchase the pet. They suffer from what behavioural economists call ‘irrational exuberance’. Such exuberance may also occur when the owner of a sick pet is offered expensive treatment. They may over-optimistically assume that the treatment will be totally successful and that their pet will not need further treatment.

Another information issue is the short-term perspective of many pet owners. They may purchase a young and healthy pet and assume that it will remain so. However, as the pet gets older, it is likely to face increasing health issues, with correspondingly increasing vet bills. But many owners do not consider such future bills when they purchase the pet. They suffer from what behavioural economists call ‘irrational exuberance’. Such exuberance may also occur when the owner of a sick pet is offered expensive treatment. They may over-optimistically assume that the treatment will be totally successful and that their pet will not need further treatment.

Vets cite another information asymmetry. This concerns the costs they face in providing treatment. Many owners are unaware of these costs – costs that include rent, business rates, heating and lighting, staff costs, equipment costs, consumables (such as syringes, dressings, surgical gowns, antiseptic and gloves), VAT, and so on. Many of these costs have risen substantially in recent months and are reflected in the prices pet owners are charged. With people experiencing free health care for themselves from the NHS (or other national provider), this may make them feel that the price of pet health care is excessive.

Then there is the issue of inequality. Pets provide great benefits to many owners and contribute to owners’ well-being. If people on low incomes cannot afford high vet bills, they may either have to forgo having a pet, with the benefits it brings, or incur high vet bills that they ill afford or simply go without treatment for their pets.

Finally, there are the external costs that arise when people abandon their pets with various health conditions. This has been a growing problem, with many people buying pets during lockdown when they worked from home, only to abandon them later when they have had to go back to the office or other workplace. The costs of treating or putting down such pets are born by charities or local authorities.

Finally, there are the external costs that arise when people abandon their pets with various health conditions. This has been a growing problem, with many people buying pets during lockdown when they worked from home, only to abandon them later when they have had to go back to the office or other workplace. The costs of treating or putting down such pets are born by charities or local authorities.

The CMA is consulting on its proposal to begin a formal Market Investigation. This closes on 11 April. If, in the light of its consultation, the Market Investigation goes ahead, the CMA will later report on its findings and may require the veterinary industry to adopt various measures. These could require vet groups to provide better information to owners, including what lower-cost treatments are available. But given the oligopolistic nature of the industry, it is unlikely to lead to significant reductions in vets bills.

Articles

- UK competition watchdog plans probe into veterinary market

Financial Times, Suzi Ring and Oliver Ralph (12/3/24)

Vet prices: Investigation over concerns pet owners are being overcharged

Vet prices: Investigation over concerns pet owners are being overchargedSky News (12/3/24)

- UK watchdog plans formal investigation into vet pricing

The Guardian, Kalyeena Makortoff (12/3/24)

- ‘Eye-watering’ vet bills at chain-owned surgeries prompt UK watchdog review

The Guardian, Kalyeena Makortoff (7/9/23)

- Warning pet owners could be overpaying for medicine

BBC News, Lora Jones & Jim Connolly (12/3/24)

- I own a vet practice, owners complain about the spiralling costs of treatments, but I only make 5 -10% profit – here’s our expenditure breakdown

Mail Online, Alanah Khosla (14/3/24)

- Vets bills around the world: As big-name veterinary practices come under pressure for charging pet owners ‘eyewatering’ care costs, how do fees in Britain compare to other countries?

Mail Online, Rory Tingle, Dan Grennan and Katherine Lawton (13/3/24)

CMA documents

Questions

- How would you establish whether there is an abuse of market power in the veterinary industry?

- Explain what is meant by the principal–agent problem. Give some other examples both in economic and non-economic relationships.

- What market advantages do large vet companies have over independent vet practices?

- How might pet insurance lead to (a) adverse selection; (b) moral hazard? Explain. How might (i) insurance companies and (ii) vets help to tackle adverse selection and moral hazard?

- Find out what powers the CMA has to enforce its rulings.

- Search for vet prices and compare the prices charged by at least three vet practices. How would you account for the differences or similarities in prices?

You may have recently noticed construction workers from different businesses digging up the roads/pavements near where you live. You may also have noticed them laying fibre optic cables. Why has this been happening? Does it make economic sense for different companies to dig up the same stretch of pavement and lay similar cables next to one another?

You may have recently noticed construction workers from different businesses digging up the roads/pavements near where you live. You may also have noticed them laying fibre optic cables. Why has this been happening? Does it make economic sense for different companies to dig up the same stretch of pavement and lay similar cables next to one another?

For many years the UK had one national fixed communication network that was owned by British Telecom (BT) – the traditional phone landline made from copper wire. This is now operated by OpenReach – part of the BT group but a legally separate division. In addition to this national infrastructure, Virgin Media (formed in 2007 from the merged cable operators, Telewest and NTL) has gradually built up a rival fixed broadband network that now covers just over 50 per cent of the country.

Although customers have only had very limited choice over which fixed communication network to use, they have had far greater choice over which Internet service provider (ISP) to sign up for. This has been possible as the industry regulator, Ofcom, forces OpenReach to provide rival ISPs such as Sky Broadband, TalkTalk and Zen with access to its network.

Expansion of the fibre optic network

Recent government policy has tried to encourage and incentivise the replacement of the copper wire network with one that is fully fibre. This is often referred to as Fibre to the Premises (FTTP) or Fibre to the Home (FTTH). A fixed network of fully fibre broadband enables much faster download speeds and many argue that it is vital for the future competitiveness of the UK economy.

Recent government policy has tried to encourage and incentivise the replacement of the copper wire network with one that is fully fibre. This is often referred to as Fibre to the Premises (FTTP) or Fibre to the Home (FTTH). A fixed network of fully fibre broadband enables much faster download speeds and many argue that it is vital for the future competitiveness of the UK economy.

Replacing the existing fixed communication network with fibre optic cables is expensive. It can involve major civil works: i.e. the digging up of roads and pavements to install new ducts to lay the fibre optic cables inside.

Over a hundred companies, that are not part of either OpenReach or Virgin Media O2 (the parent company of Virgin Media), have recently been digging up pavements/roads and laying new fibre optic cables. Known as alternative network providers (altnets) or independent networks, these businesses vary in size, with many of them securing large loans from banks and private investors. By the middle of 2023, 2.5 million premises in the UK had access to at least two or more of these independent networks.

After a slow initial response to the altnets, OpenReach has recently responded by rapidly installing FTTP. The business is currently building 62 000 connections every week and plans to have 25 million premises connected by the end of 2026. In July 2022, Virgin Media O2 announced that it was establishing a new joint venture with InfraVia Capital Partners. Called Nexfibre, this business aims to connect 5 million premises to FTTP by 2026.

Is the fibre optic network a natural monopoly?

Some people argue that the fixed communication network is an example of a natural monopoly – an industry where a single firm can supply the whole market at a lower average cost than two or more firms. To what extent is this true?

An industry is a natural monopoly where the minimum efficient scale of production (MES) is larger than the market demand for the good/service. This is more likely to occur where there are significant economies of scale. Digging up roads/pavements, installing new ducts and laying fibre optic cable are clear examples of fixed costs. Once the network is built, the marginal cost of supplying customers is relatively small. Therefore, this industry has significant economies of scale and a relatively large MES. This has led many people to argue that building rival fixed communication networks is wasteful duplication and will lead to higher costs and prices.

However, when judging if a sector is a natural monopoly, it is always important to remember that a comparison needs to be made between the MES and the size of the market. An industry could have significant economies of scale, but not be an example of a natural monopoly if the market demand is significantly larger than the MES.

In the case of the fixed communication network, the size of the market will vary significantly between different regions of the country. In densely populated urban areas, such as large towns and cities, the demand for services provided via these networks is likely to be relatively large. Therefore, the MES could be smaller than the size of the market, making competition between network suppliers both possible and desirable. For example, competition may incentivise firms to innovate, become more efficient and reduce costs.

In the case of the fixed communication network, the size of the market will vary significantly between different regions of the country. In densely populated urban areas, such as large towns and cities, the demand for services provided via these networks is likely to be relatively large. Therefore, the MES could be smaller than the size of the market, making competition between network suppliers both possible and desirable. For example, competition may incentivise firms to innovate, become more efficient and reduce costs.

Research undertaken for the government by the consultancy business, Frontier Economics, found that at least a third of UK households live in areas where competition between three or more different networks is economically desirable.

By contrast, in more sparsely populated rural areas, demand for the services provided by these networks will be smaller. The fixed costs per household of installing the network over longer distances will also be larger. Therefore, the MES is more likely to be greater than the size of the market.

The same research undertaken by Frontier Economics found that around 10 per cent of households live in areas where the fixed communication network is a natural monopoly. The demand and cost conditions for another 10 per cent of households meant it is not commercially viable to have any suppliers.

Therefore, policies towards the promotion of competition, regulation, and government support for the fixed communication network might have to be adjusted depending on the specific demand and cost conditions in a particular region.

Articles

Review

Questions

- Explain the difference between fixed and wireless communication networks.

- Draw a diagram to illustrate a profit-maximising natural monopoly. Outline some of the implications for allocative efficiency.

- Discuss some of the issues with regulating natural monopolies, paying particular attention to price regulation.

- The term ‘overbuild’ is often used to describe a situation where more than one fibre broadband network is being constructed in the same place. Some people argue that incumbent network suppliers deliberately choose to use this term to imply that the outcome is harmful for society. Discuss this argument.

- An important part of government policy in this sector has been the Duct and Pole Access Strategy (DPA). Illustrate the impact of this strategy on the average cost curve and the minimum efficient scale of production for fibre broadband networks.

- Draw a diagram to illustrate a region where (a) it is economically viable to have two or more fibre optic broadband network suppliers and (b) where it is commercially unviable to have any broadband network suppliers without government support.

- Some people argue that network competition provides strong incentives for firms to innovate, to become more efficient and reduce costs. Draw a diagram to illustrate this argument.

- Explain why many ‘altnets’ are so opposed to OpenReach’s new ‘Equinox 2’ pricing scheme for its fibre network.

With the coronavirus pandemic having reached almost every country in the world, the impact on the global economy has been catastrophic. Governments have struggled balancing the spread of the virus and keeping the economy afloat. This has left businesses counting the costs of various control measures and numerous lockdowns. The crisis has particularly affected small and medium-sized enterprises (SMEs), causing massive job losses and longer-term economic scars. Among these is an increase in the market power held by dominant firms as they emerge even stronger while smaller rivals fall away.

With the coronavirus pandemic having reached almost every country in the world, the impact on the global economy has been catastrophic. Governments have struggled balancing the spread of the virus and keeping the economy afloat. This has left businesses counting the costs of various control measures and numerous lockdowns. The crisis has particularly affected small and medium-sized enterprises (SMEs), causing massive job losses and longer-term economic scars. Among these is an increase in the market power held by dominant firms as they emerge even stronger while smaller rivals fall away.

It is feared that with the full effects of the pandemic not yet realised, there may well be a wave of bankruptcies that will hit SMEs harder than larger firms, particularly in the most affected industries. Larger firms are most likely to be more profitable in general and more likely to have access to finance. Firm-level analysis using Orbis data, which includes listed and private firms, suggests that the pandemic-driven wave of bankruptcies will lead to increases in industry concentration and market power.

What is market power?

A firm holds a dominant position if its power enables it to operate within the market without taking account of the reaction of its competitors or of intermediate or final consumers. The key role of competition authorities around the world is to protect the public interest, particularly against firms abusing their dominant positions.

A firm holds a dominant position if its power enables it to operate within the market without taking account of the reaction of its competitors or of intermediate or final consumers. The key role of competition authorities around the world is to protect the public interest, particularly against firms abusing their dominant positions.

The UK’s competition authority, the Competition and Markets Authority (CMA) states:

Market power arises where an undertaking does not face effective competitive pressure. …Market power is not absolute but is a matter of degree; the degree of power will depend on the circumstances of each case. Market power can be thought of as the ability profitably to sustain prices above competitive levels or restrict output or quality below competitive levels. An undertaking with market power might also have the ability and incentive to harm the process of competition in other ways; for example, by weakening existing competition, raising entry barriers, or slowing innovation.

It can be hard to distinguish between a rapidly growing business and growing concentration of market power. In a pandemic, these distinctions can become even more difficult to discern, since there really is a deep need for a rapid deployment of capital, often in distressed situations. It is also not always evident whether the attempt to grow is driven by the need for more productive capacity, or by the desire to engage in financial engineering or to acquire market power.

It may be the case that, as consumers, we simply have no choice but to depend on various monopolies in a crisis, hoping that they operate in the public interest or that the competition authorities will ensure that they do so. With Covid-19 for example, economies will have entered the pandemic with their existing institutions, and therefore the only way to operate may be through channels controlled by concentrated power. Market dominance can occur for what seem to be good, or least necessary, reasons.

Why is market power a problem?

Why is it necessarily a problem if a successful company grows bigger than its competitors through hard work, smart strategies, and better technology adoption? It is important to recognise that increases in market power do not always mean an abuse of that market power. Just because a company may dominate the market, it does not mean there is a guaranteed negative impact on the consumer or industry. There are many advantages to a monopoly firm and, therefore, it can be argued that the existence of a market monopoly in itself should not be a cause of concern for the regulator. Unless there is evidence of past misconduct of dominance, which is abusive for the market and its stakeholders, some would argue that there is no justification for any involvement by regulators at all.

Why is it necessarily a problem if a successful company grows bigger than its competitors through hard work, smart strategies, and better technology adoption? It is important to recognise that increases in market power do not always mean an abuse of that market power. Just because a company may dominate the market, it does not mean there is a guaranteed negative impact on the consumer or industry. There are many advantages to a monopoly firm and, therefore, it can be argued that the existence of a market monopoly in itself should not be a cause of concern for the regulator. Unless there is evidence of past misconduct of dominance, which is abusive for the market and its stakeholders, some would argue that there is no justification for any involvement by regulators at all.

However, research by the International Monetary Fund concluded that excessive market power in the hands of a few firms can be a drag on medium-term growth, stifling innovation and holding back investment. Given the severity of the economic impact of the pandemic, such an outcome could undermine the recovery efforts by governments. It could also prevent new and emerging firms entering the market at a time when dynamism is desperately needed.

The ONS defines business dynamism as follows:

Business dynamism relates to measures of birth, growth and decline of businesses and its impact on employment. A steady rate of business creation and closure is necessary for an economy to grow in the long-run because it allows new ideas to flourish.

A lack of business dynamism could lead to a stagnation in productivity and wage growth. It also affects employment through changes in job creation and destruction. In this context, the UK’s most recent unemployment rate was 5%. This is the highest figure for five years and is predicted to rise to 6.5% by the end of 2021. Across multiple industries, there is now a trend of falling business dynamism with small businesses failing to break out of their local markets and start-up companies whose prices are undercut by a big rival. This creates missed opportunities in terms of growth, job creation, and rising incomes.

There has been a rise in mergers and acquisitions, especially amongst dominant firms, which is contributing to these trends. Again, it is important to recognise that mergers and acquisitions are not in themselves a problem; they can yield cost savings and produce better products. However, they can also weaken incentives for innovation and strengthen a firm’s ability to charge higher prices. Analysis shows that mergers and acquisitions by dominant firms contribute to an industry-wide decline in business dynamism.

Changes in market power due to the pandemic

The IMF identifies key indicators for market power, such as the percentage mark-up of prices over marginal cost, and the concentration of revenues among the four biggest players in a sector. New research shows that these key indicators of market power are on the rise. It is estimated that due to the pandemic, this increase in market dominance could now increase in advanced economies by at least as much as it did in the fifteen years to the end of 2015.

Global price mark-ups have risen by more than 30%, on average, across listed firms in advanced economies since 1980. And in the past 20 years, mark-up increases in the digital sector have been twice as steep as economy-wide increases. Increases in market power across multiple industries caused by the pandemic would exacerbate a trend that goes back over four decades.

Global price mark-ups have risen by more than 30%, on average, across listed firms in advanced economies since 1980. And in the past 20 years, mark-up increases in the digital sector have been twice as steep as economy-wide increases. Increases in market power across multiple industries caused by the pandemic would exacerbate a trend that goes back over four decades.

It could be argued that firms enjoying this increase in market share and strong profits is just the reward for their growth. Such success if often a result of innovation, efficiency, and improved services. However, there are growing signs in many industries that market power is becoming entrenched amid an absence of strong competitors for dominant firms. It is estimated that companies with the highest mark-ups in a given year, have an almost 85 percent chance of remaining a high mark-up firm the following year. According to experts, some of these businesses have created entry barriers – regulatory or technology driven – which are incredibly high.

Professor Jayant R. Varma, a member of the MPC of the Reserve Bank of India (RBI), observed that in several sectors characterised by an oligopolistic core and a competitive periphery, the oligopolistic core has weathered the pandemic and it is the competitive periphery that has been debilitated. Rising profits and profit margins, improving capacity utilisation and lack of new capacity additions create ripe conditions for the oligopolistic core to start exercising pricing power.

The drivers and macroeconomic implications of such rises in market power are likely to differ across economies and individual industries. Even in those industries that benefited from the crisis, such as the digital sector, dominant players are among the biggest winners. The technology industry has been under the microscope in recent years, and increasingly the big tech firms are under scrutiny from regulators around the world. The market disruptors that displaced incumbents two decades ago have become increasingly dominant players that do not face the same competitive pressures from today’s would-be disruptors. The pandemic is adding to powerful underlying forces such as network effects and economies of scale and scope.

A new regulator that aims to curb this increasing dominance of the tech giants has been established in the UK. The Digital Markets Unit (DMU) will be based inside the Competition and Markets Authority. The DMU will first look to create new codes of conduct for companies such as Facebook and Google and their relationship with content providers and advertisers. Business Secretary Kwasi Kwarteng said the regime will be ‘unashamedly pro-competition’.

A new regulator that aims to curb this increasing dominance of the tech giants has been established in the UK. The Digital Markets Unit (DMU) will be based inside the Competition and Markets Authority. The DMU will first look to create new codes of conduct for companies such as Facebook and Google and their relationship with content providers and advertisers. Business Secretary Kwasi Kwarteng said the regime will be ‘unashamedly pro-competition’.

Policy Responses

The additions in regulation in the UK fall in line with the guidance from the IMF. It recommends that adjustments to competition-policy frameworks need to be made in order to minimise the adverse effects of market dominance. Such adjustments must, however, be tailored to national circumstances, both in general and to address the specific challenges raised by the surge of the digital economy.

It recommends the following five actions:

- Competition authorities should be increasingly vigilant when enforcing merger control. The criteria for competition authorities to review a deal should cover all relevant cases – including acquisitions of small players that may grow to compete with dominant firms.

- Second, competition authorities should more actively enforce prohibitions on the abuse of dominant positions and make greater use of market investigations to uncover harmful behaviour without any reported breach of the law.

- Greater efforts are needed to ensure competition in input markets, including labour markets.

- Competition authorities should be empowered to keep pace with the digital economy, where the rise of big data and artificial intelligence is multiplying incumbent firms’ advantage. Facilitating data portability and interoperability of systems can make it easier for new firms to compete with established players.

- Investments may be needed to further boost sector-specific expertise amid rapid technological change.

Conclusion

The crisis has had a significant impact on all businesses, with many shutting their doors for good. However, there has been a greater negative impact on SMEs. Even in industries that have flourished from the pandemic, it is the dominant firms that have emerged the biggest winners. There is concern that the increasing market power will remain embedded in many economies, stifling future competition and economic growth. While the negative effects of increased market power have been moderate so far, the findings suggest that competition authorities should be increasingly vigilant to ensure that these effects do not become more harmful in the future.

Reviews of competition policy frameworks have already begun in some major economies. Young, high-growth firms that innovate and create high-quality jobs deserve a level playing field and a fair chance to succeed. Support directed to SMEs is important, as many small firms have been unable to benefit from government programmes designed to help firms access financing during the pandemic. Policymakers should act now to prevent a further, sharp rise in market power that could hold back the post-pandemic recovery.

Articles

Podcast

Official documents

Questions

- What are the arguments for and against the assistance of a monopoly?

- What barriers to entry may exist that prevent small firms from entering an industry?

- What policies can be implemented to limit market power?

- Define and explain market dynamism.

In recent years, US tech companies have faced increased scrutiny in Washington over their size and power. Despite the big tech firms in America being economically robust, seemingly more so than any other sector, they are also more politically vulnerable. This potential vulnerability is present regardless of the recent election result.

In recent years, US tech companies have faced increased scrutiny in Washington over their size and power. Despite the big tech firms in America being economically robust, seemingly more so than any other sector, they are also more politically vulnerable. This potential vulnerability is present regardless of the recent election result.

Both the Democrat and Republican parties are thinking critically about monopoly power and antitrust issues, where ‘antitrust’ refers to the outlawing or control of oligopolistic collusion. Despite the varied reasons across different parts of the political spectrum, the increased scrutiny over big tech companies is bipartisan.

Rising monopoly power

Monopoly power occurs when a firm has a dominant position in the market. A pure monopoly is when one firm has a 100% share of the market. A firm might be considered to have monopoly power with more than a 25% market share.

If there is a rise in market concentration, it tends to hurt blue-collar workers, such as those employed in factories, more than everyone else. Research, from the University of Chicago, studied what happens to particular classes of workers when companies increasingly dominate a market and have more power to raise prices. The study found that those workers that make things tend to be left worse off, while the workers who sell, market or design things gain. When companies have more pricing power, they make fewer products and sell each one for a higher profit margin. In that case, it’s far more valuable to a company to be an employee working in so-called expansionary positions, such as marketing, than in production jobs, such as working on a factory line — because there’s less production to be done and more salesmanship.

Monopoly power under Trump Vs Biden

In February, President Trump and his economic team saw no need to rewrite the federal government’s antitrust rules, drawing a battle line with the Democrats on an issue that has increasingly drawn the attention of economists, legal scholars and other academics. In their annual Economic Report of the President, Mr. Trump and his advisers effectively dismissed research that found large American companies increasingly dominate industries like telecommunications and tech, stifling competition and hurting consumers. At the time the Trump administration contended that studies demonstrating a rise in market concentration were flawed and that the rise of large companies may not be a bad thing for consumers.

In February, President Trump and his economic team saw no need to rewrite the federal government’s antitrust rules, drawing a battle line with the Democrats on an issue that has increasingly drawn the attention of economists, legal scholars and other academics. In their annual Economic Report of the President, Mr. Trump and his advisers effectively dismissed research that found large American companies increasingly dominate industries like telecommunications and tech, stifling competition and hurting consumers. At the time the Trump administration contended that studies demonstrating a rise in market concentration were flawed and that the rise of large companies may not be a bad thing for consumers.

On page 201, the report reads:

Concentration may be driven by economies of scale and scope that can lower costs for consumers. Also, successful firms tend to grow, and it is important that antitrust enforcement and competition policy not be used to punish firms for their competitive success.

The Trump administration approved some high-profile corporate mergers, such as the merger of Sprint and T-Mobile, while also trying to block others, such as AT&T’s purchase of Time Warner. Mr. Trump’s advisers stated that agencies already had the tools they needed to evaluate mergers and antitrust cases. It lamented that some Americans have come to hold the mistaken, simplistic view that ‘Big Is Bad.’

However, it is likely that such big firms, including the tech giants, would take a hit under the new presidency. President-Elect Joe Biden has pledged to undo the tax cuts introduced by Trump and has vowed to increase corporation tax from 21% to 28%. As part of these tax changes, he has suggested the introduction of a minimum 15% tax for all companies with a revenue of over $100 million. This has now been given the nickname of the ‘Amazon Tax’ and it is clear how it would impact on the big the firms such as Amazon.

This is the opposite of what was probable if Trump were to have been re-elected. It was expected that the US would continue along the path of deregulation and lower taxes for corporates and high-income households, which would have been welcomed by the stock market. However, analysts suggest that the tax changes under Biden would negatively affect the US tech sector, with some analysts maintaining that the banking sector would also be hit.

Antitrust enforcement is often associated with the political left, but the current situation is not so clear-cut. In the past, Silicon Valley has largely avoided any clashes with Washington, even when European regulators have levied fines against the tech giants. European regulators have fined Google a total of $9bn for anticompetitive practices. In 2018 Donald Trump attacked the EU decisions. “I told you so! The European Union just slapped a Five Billion Dollar fine on one of our great companies, Google,” Trump tweeted. “They truly have taken advantage of the US, but not for long!”

Antitrust enforcement is often associated with the political left, but the current situation is not so clear-cut. In the past, Silicon Valley has largely avoided any clashes with Washington, even when European regulators have levied fines against the tech giants. European regulators have fined Google a total of $9bn for anticompetitive practices. In 2018 Donald Trump attacked the EU decisions. “I told you so! The European Union just slapped a Five Billion Dollar fine on one of our great companies, Google,” Trump tweeted. “They truly have taken advantage of the US, but not for long!”

However, since then the mood has changed, with Trump and other conservatives joining liberals, including senators Elizabeth Warren and Bernie Sanders, in attacking the dominance of tech firms, including Amazon, Google, Facebook and others. While Democrats have largely stuck to criticising the scale of big tech’s dominance, Republicans, including Trump, have accused the major tech companies of censoring conservative speech.

An antitrust subcommittee of the Democrat-controlled House Judiciary Committee released a 449-page report excoriating the Big Four tech companies, Amazon, Facebook, Apple and Google-owner, Alphabet, for what it calls systematic and continuing abuses of their monopoly power. Recommendations from the report include ways to limit their power, force them out of certain areas of business and even a break-up of some of them.

Democratic lawmakers working on the probe claim that these firms have too much power, and that power must be reined in. But not all Republicans involved agreed with the recommendations. One Republican congressman, Jim Jordan, dismissed the report as “partisan” and said it advanced “radical proposals that would refashion antitrust law in the vision of the far left.” However, others have said they support many of the report’s conclusions about the firms’ anti-competitive tactics, but that remedies proposed by Democrats go too far.

The US tech giants

Amazon is a leading example of the economic strength held by the tech giants. Amazon has produced 12-month revenues of $321bn to October 2020, which in an increase from 2019 and 2018 revenues of $280bn and $233bn respectively. However, Amazon, along with the other big players Apple, Facebook, Google parent Alphabet, and Microsoft, are facing increased government scrutiny.

The US Department of Justice has filed a lawsuit against Google for entrenching itself as the dominant search engine through anti-competitive practices. Google’s complex algorithms, software, and custom-built servers helped make it into one of the world’s richest and most-powerful corporations. It currently dominates the online search market in the USA, accounting for around 80% of search queries. The lawsuit accuses the tech company of abusing its position to maintain an illegal monopoly over search and search advertising. Facebook also faces an antitrust lawsuit from the Federal Trade Commission. It is arguable that the US tech giants are so powerful that they may accomplish the seemingly impossible and unite the two parties, at least on one policy – breaking them up.

If it is correct that the tech giants’ behaviour ultimately damages innovation and exacerbates inequality, it is arguable that such problems have only grown worse with the coronavirus pandemic. Many smaller businesses have succumbed to the economic damage: many have been closed during lockdowns or suffered a decline in sales; many have gone out of business.

The changing patterns in teleworking and retail have accelerated in ways that have made Americans more reliant on technologies produced by a few firms. Shares in the Big Four, along with Microsoft, Netflix, and Tesla, added $291 billion in market value in just one day last week. It could therefore be claimed that the dangers of Big Tech domination are more profound now than they were even a few months ago.

Google’s lawsuit

On 20 October, the Department of Justice — along with eleven state Attorneys General — filed a civil antitrust lawsuit in the U.S. District Court for the District of Columbia to stop Google from unlawfully maintaining monopolies through anticompetitive and exclusionary practices in the search and search advertising markets and to remedy the competitive harms.

This is the most significant legal challenge to a major tech company in decades and comes as US authorities are increasingly critical of the business practices of the major tech companies. The suit alleges that Google is no longer a start-up company with an innovative way to search the emerging internet. Instead Google is being described as a “monopoly gatekeeper for the internet” that has used “pernicious” anticompetitive tactics to maintain and extend its monopolies.

This is the most significant legal challenge to a major tech company in decades and comes as US authorities are increasingly critical of the business practices of the major tech companies. The suit alleges that Google is no longer a start-up company with an innovative way to search the emerging internet. Instead Google is being described as a “monopoly gatekeeper for the internet” that has used “pernicious” anticompetitive tactics to maintain and extend its monopolies.

The allegation that Google is unfairly acting as a gatekeeper to the internet is based on the argument that through a series of business agreements, Google has effectively locked out any competition. One of the specific arrangements being challenged is the issue of Google being preloaded on mobile devices. On mobile phones running its Android operating system, Google is preinstalled and cannot be deleted. The company pays billions each year to “secure default status for its general search engine and, in many cases, to specifically prohibit Google’s counterparties from dealing with Google’s competitors,” the suit states. It is argued that this alone forecloses competition for internet search as it denies its rivals to compete effectively and prevent potential innovation.

However, Google has defended its position, calling the lawsuit “deeply flawed”. It has argued that consumers themselves choose to use Google; they do not use it because they are forced to or because they can’t find an alternative search platform. Google also argues that this lawsuit will not be beneficial for consumers. It claims that this will artificially prop up lower-quality search alternatives, increase phone prices, and make it harder for people to get the search services they want to use.

Conclusion

Despite wanting to stop Google from “unlawfully maintaining monopolies in the markets for” search services, advertising, and general search text, the lack of consensus and divergence among the Democrats and Republicans on the antitrust issues remains a major issue to move things forward.

The Democrats want to see the power held by these companies reined in, while the Republicans would rather see targeted antitrust enforcement over onerous and burdensome regulation that kills industry innovation. It is clear that the US government will have to balance its reforms and ideas while making sure not to put the largest companies in the USA at a competitive disadvantage versus their competitors globally.

Articles

- US tech giants accused of ‘monopoly power’

BBC News (6/10/20)

- Tech, healthcare & the ‘fear index’: An investor’s guide to US election night 2020

Investment Trust Insider, Alex Steger, Alex Rosenberg, John Coumarianos, Nicole Piper, Jake Martin and Ian Wenik (2/11/20)

- Justice Department Sues Monopolist Google For Violating Antitrust Laws

The United States Department of Justice (20/10/20)

- Trump Administration Sees No Threat to Economy From Monopolies

The New York Times, Jim Tankersley (20/2/20)

- Trump vs Biden: Winners and losers under America’s next leader

Shares, Yoosof Farah (29/10/20)

- America’s Monopoly Problem Goes Way Beyond the Tech Giants

The Atlantic, David Dayen (28/7/20)

- US justice department sues Google over accusation of illegal monopoly

The Guardian, Dominic Rushe and Kari Paul (20/10/20)

Questions

- With the aid of a diagram, explain how pricing decisions are made in a monopoly.

- What factors influence the degree of monopoly power a company has within an industry?

- What are the advantages of a monopoly?

- Why would a government want to prevent a monopoly? Discuss the policies a government could implement to do this.

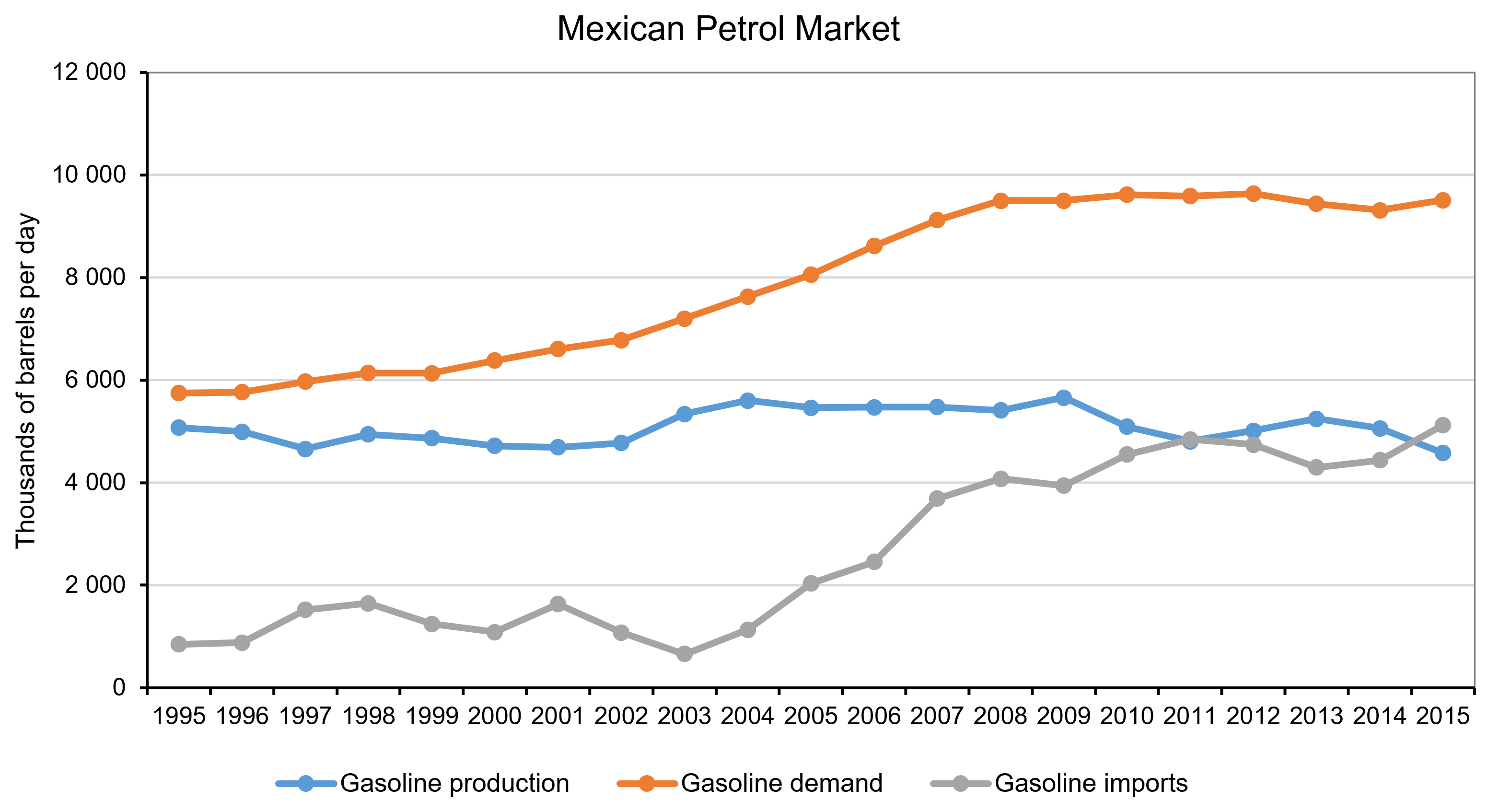

So here we are, summer is over (or almost over if you’re an optimist) and we are sitting in front of our screens reminiscing about hot sunny days (at least I do)! There is no doubt, however: a lot happened in the world of politics and economics in the past three months. The escalation of the US-China trade war, the run on the Turkish lira, the (successful?) conclusion of the Greek bailout – these are all examples of major economic developments that took place during the summer months, and which we will be sure to discuss in some detail in future blogs. Today, however, I will introduce a topic that I am very interested in as a researcher: the liberalisation of energy markets in developing countries and, in particular, Mexico.

So here we are, summer is over (or almost over if you’re an optimist) and we are sitting in front of our screens reminiscing about hot sunny days (at least I do)! There is no doubt, however: a lot happened in the world of politics and economics in the past three months. The escalation of the US-China trade war, the run on the Turkish lira, the (successful?) conclusion of the Greek bailout – these are all examples of major economic developments that took place during the summer months, and which we will be sure to discuss in some detail in future blogs. Today, however, I will introduce a topic that I am very interested in as a researcher: the liberalisation of energy markets in developing countries and, in particular, Mexico.

Why Mexico? Well, because it is a great example of a large developing economy that has been attempting to liberalise its energy market and reverse price setting and monopolistic practices that go back several decades. Until very recently, the price of petrol in Mexico was set and controlled by Pemex, a state monopolist. This put Pemex under pressure since, as a sole operator, it was responsible for balancing growing demand and costs, even to the detriment of its own finances.

The petrol (or ‘gasoline’) price liberalisation started in May 2017 and took place in stages – starting in the North part of Mexico and ending in November of the same year in the central and southern regions of the country. The main objective was to address the notable decrease in domestic oil production that put at risk the ability of the country to meet demand; as well as Mexico’s increasing dependency on foreign markets affected by the surge of the international oil price. The government has spent the past five years trying to create a stronger regulatory framework, while easing the financial burden on the state and halting the decline in oil reserves and production. Unsurprisingly, opening up a monopolistic market turns out to be a complex and bumpy process.

Source: Author’s calculations using data from the Energy Information Bank, Ministry of Energy, Mexico

Source: Author’s calculations using data from the Energy Information Bank, Ministry of Energy, Mexico

Despite all the reforms, retail petrol prices have kept rising. Although part of this price rise is demand-driven, an increasing number of researchers highlight the significance of the distribution of oil-related infrastructure in determining price outcomes at the federal and regional (state) level. Saturation and scarcity of both distribution and storage infrastructure are probably the two most significant impediments to opening the sector up to competition (Mexico Institute, 2018). You see, the original design of these networks and the deployment of the infrastructure was not aimed at maximising efficiency of distribution – the price was set by the monopolist and, in a way that was compliant with government policy (Mexico Institute, 2018). Economic efficiency was not always part of this equation. As a result, consumers located in better-deployed areas were subsidising the inherent logistics costs of less ‘well endowed’ regions by facing an artificially higher price than they would have in a competitive market.

But what about now? Do such differences in the allocation of infrastructure between regions lead to location-related differences in the price of petrol? If so, by how much? And, what policies should the government pursue to address such imbalances? These are all questions that I explore in one of my recent working papers titled ‘Widening the Gap: Lessons from the aftermath of the energy market reform in Mexico’ (with Hugo Vallarta) and I will be sharing some of the answers with you in a future blog.

Articles

Data

Questions

- Are state-owned monopolies effective in delivering successful market outcomes? Why yes, why no?

- In the case of Mexico, are you surprised about the complexities that were involved with opening up markets to competition? Explain why.

- Use Google to identify countries in which energy markets are controlled by state-owned monopolies.