An agreement in principle was reached on September 30 between the USA, Canada and Mexico over a new trade deal to replace the North American Free Trade Agreement (NAFTA). President Trump had described NAFTA as ‘the worst trade deal maybe ever signed anywhere, but certainly ever signed in this country.’ The new deal, named the United States-Mexico-Canada Agreement, or USMCA, is the result of 14 months of negotiations, which have often been fractious. A provisional bilateral agreement was made between the USA and Mexico in August. At the same time, President Trump threatened a trade war with Canada if it did not reach a trade agreement with the USA (and Mexico). The new USMCA must be ratified by lawmakers in all three countries before it can come into force. This could take a few months.

So is USMCA a radical departure from NAFTA? Does the USA stand to gain substantially, as President Trump claims? In fact, USMCA is little different from NAFTA. It could best be described as a relatively modest reworking of NAFTA. So what are the changes?

The first change affects the car industry. From 2020, 75% of the components of any vehicle crossing between the USA and Canada or Mexico must be made within one or more of the three countries to qualify for tariff-free treatment. The aim is to boost production within the region. But the main change here is merely an increase in the proportion from the current 62.5%.

A more significant change affecting the car industry concerns wages. Between 40% and 45% of a vehicle’s components must be made by workers earning at least US$16 per hour. This is some three times more than the average wage currently earned by Mexican car workers. Although it will benefit such workers, it will reduce Mexico’s competitive advantage and could hence lead to some diversion of production away from Mexico. Also, it could push up the price of cars.

The agreement has also strengthened various standards inadequately covered in NAFTA. According to The Conversation article:

The new agreement includes stronger protections for patents and trademarks in areas such as biotech, financial services and domain names – all of which have advanced considerably over the past quarter century. It also contains new provisions governing the expansion of digital trade and investment in innovative products and services.

Separately, negotiators agreed to update labor and environmental standards, which were not central to the 1994 accord and are now typical in modern trade agreements. Examples include enforcing a minimum wage for autoworkers, stricter environmental standards for Mexican trucks and lots of new rules on fishing to protect marine life.

Another area where the USMCA agreement has made changes concerns trade in dairy products. This particularly affects Canada, which has agreed to allow more US dairy products tariff-free into Canada (see the CNN article at the end of the list of articles below). New higher quotas will give US dairy farmers access to 3.6% of Canada’s dairy market. They will still pay tariffs on dairy exports to Canada that exceed the quotas, ranging from 200% to 300%.

The other significant change for consumers in Mexico and Canada is a rise in the value of duty-free imports they can bring in from the USA, including online transactions. As the first BBC article listed below states:

The new agreement raises duty-free shopping limits to $100 to enter Mexico and C$150 ($115) to enter Canada without facing import duties – well above the $50 previously allowed in Mexico and C$20 permitted by Canada. That’s good news for online shoppers in Mexico and Canada – as well as shipping firms and e-commerce companies, especially giants like Amazon.

Despite these changes, USMCA is very similar to NAFTA. It is still a preferential trade deal between the three countries, but certainly not a completely free trade deal – but nor was NAFTA.

And for the time being, US tariffs on Mexican and Canadian steel and aluminium imports remain in place. Perhaps, with the conclusion of the USMCA agreement, the Trump administration will now, as promised, consider lifting these tariffs.

What have been the chief gains and losses for the USA from USMCA?

What have been the chief gains and losses for Mexico from USMCA?

What have been the chief gains and losses for Canada from USMCA?

What are the economic gains from free trade?

Why might a group of countries prefer a preferential trade deal with various restrictions on trade rather than a completely free trade deal between them?

Distinguish between trade creation and trade diversion.

In what areas, if any, might USMCA result in trade diversion?

If the imposition of tariffs results in a net loss from a decline in trade, why might it be in the interests of a country such as the USA to impose tariffs?

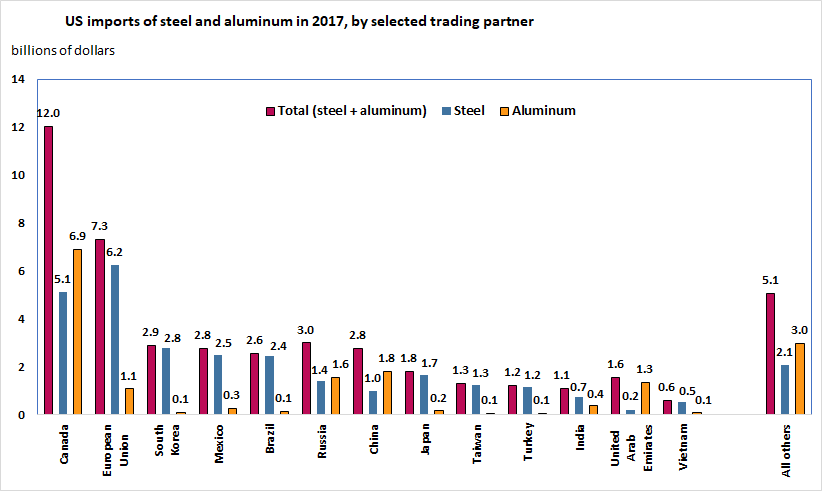

The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

Source: Bown (2018), Figure 1

A number of economists and policymakers are worried that such policies restrict trade and are likely to provoke retaliation by the affected trade partners. In recent statements, the EU has pledged to take counter-measures if the bloc is affected by these policies. In a recent press conference, the Commissioner for Trade, Cecilia Malmstrom, stated that:

We have made it clear that a move that hurts the EU and puts thousands of European jobs in jeopardy will be met with a firm and proportionate response.

She added that, ‘I truly hope that this will not happen. A trade war has no winners.’

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.

A number of studies have attempted to estimate the effect of trade restrictions and tariff wars on welfare: see for instance Anderson and Wincoop (2001), Syropoulos (2002), Fellbermayr et al. (2013). The results vary widely, depending on the case. However, there seems to be consensus that the more similar (in terms of size and industry composition) the adversaries are, the more mutually damaging a trade war is likely to be (and, therefore, less likely to happen).

As Miyagiwa et al (2016, p43) explain:

A country initiates contingent protection policy against a trading partner only if the latter has a considerably smaller domestic market than its own, while avoiding confrontation with a country having a substantially larger domestic market than its own.

As both Canada and the EU are very large advanced market economies, it remains to be seen how much risk (and potential damage to the local and global economy) US trade policymakers are willing to take.

Since running for election, Donald Trump has vowed to ‘put America first’. One of the economic policies he has advocated for achieving this objective is the imposition of tariffs on imports which, according to him, unfairly threaten American jobs. On March 8 2018, he signed orders to impose new tariffs on metal imports. These would be 25% on steel and 10% on aluminium.

His hope is that, by cutting back on imports of steel and aluminium, the tariffs could protect the domestic industries which are facing stiff competition from the EU, South Korea, Brazil, Japan and China. They are also facing competition from Canada and Mexico, but these would probably be exempt provided negotiations on the revision of NAFTA rules goes favourably for the USA.

Assuming there were no retaliation from other countries, jobs would be gained in the steel and aluminium industries. According to a report by The Trade Partnership (see link below), the tariffs would increase employment in these industries by around 33 000. However, the higher price of these metals would cause job losses in the industries using them. In fact, according to the report, more than five jobs would be lost for every one gained. The CNN Money article linked below gives example of the US industries that will be hit.

But the costs are likely to be much greater than this. Accorinding to the law of comparative advantage, trade is a positive-sum game, with a net gain to all parties engaged in trade. Unless trade restrictions are used to address a specific market distortion in the trade process itself, restricting trade will lead to a net loss in overall benefit to the parties involved.

Clearly there will be loss to steel and aluminium exporters outside the USA. There will also be a net loss to their countries unless these metals had a higher cost of production than in the USA, but were subsidised by governments so that they could be exported profitably.

But perhaps the biggest cost will arise from possible retaliation by other countries. A trade war would compound the net losses as the world moves further from trade based on comparative advantage.

Already, many countries are talking about retaliation. For example, the EU is considering a ‘reciprocal’ tariff of 25% on cranberries, bourbon and Harley-Davidsons, all produced in politically sensitive US states (see the first The Economist article below). ‘As Jean-Claude Juncker, president of the European Commission, puts it, “We can also do stupid”.’ In fact, this is quite a politically astute move to put pressure on Mr Trump.

But cannot countries appeal to the WTO? Possibly, but this route might take some time. What is more, the USA has attempted to get around WTO rules by justifying the tariffs on ‘national security’ grounds – something allowed under Article XXI of WTO rules, provided it can be justified. This could possibly deter countries from retaliating, but it is probably unlikely. In the current climate, there seems to be a growing mood for flouting, or at least loosely interpreting, WTO rules.

One of President Trump’s main policy slogans has been ‘America first’. As Trump sees it, a manifestation of a country’s economic strength is its current account balance. He would love the USA to have a current account surplus. As it is, it has the largest current account deficit in the world (in absolute terms) of $481 billion in 2016 or 2.6% of GDP. This compares with the UK’s $115bn or 4.4% of GDP. Germany, by contrast, had a surplus in 2016 of $294bn or 8.5% of GDP.

However, he looks at other countries’ current account surpluses suspiciously – they may be a sign, he suspects, of ‘unfair play’. Germany’s surplus of over $50bn with the USA is particularly in his sights. Back in January, as President-elect, he threatened to put a 35% tariff on imports of German cars.

In practice, Germany is governed by eurozone rules, which prevent it from subsidising exports. And it does not have its own currency to manipulate. What is more, it is relatively open to imports from the USA. The EU imposes an average tariff of just 3% on US imports and importers also have to add VAT (19% in the case of Germany) to make them comparably priced with goods produced within the EU.

So why does Germany have such a large current account surplus? The article below explores the question and dismisses the claim that it’s the result of currency manipulation or discrimination against imports. The article states that the reason for the German surplus is that:

… it saves more than it invests. The correspondence of savings minus investment with exports minus imports is not an economic theory; it’s an accounting identity. Germans collectively spend less than they produce, and the difference necessarily shows up as net exports.

But why do the Germans save so much? The answer given is that, with an aging population, Germans are sensibly saving now to support themselves in old age. If Germany were to reduce its current account surplus, this would entail either the government reducing its budget surplus, or people reducing the amount they save, or some combination of the two. This is because a current account surplus, which consists of exports and other incomes from abroad (X) minus imports and any other income flowing abroad (M), must equal the surplus of saving (S) plus taxation (T) over investment (I) plus government expenditure (G). In terms of withdrawals and injections, given that:

I + G + X = S + T + M

then, rearranging the terms,

X – M = (S + T) – (I + G).

If German people are reluctant to reduce the amount they save, then an alternative is for the German government to reduce taxation or increase government expenditure. In the run-up to the forthcoming election on 24 September, Chancellor Merkel’s centre-right CDU party advocates cutting taxes, while the main opposition party, the SPD, advocates increasing government expenditure, especially on infrastructure. The article considers the arguments for these two approaches.

Why does Germany have such a large current account surplus?

What are the costs and benefits to Germany of having a large current account surplus?

What is meant by ‘mercantilism’? Why is its justification fallacious?

If Germany had its own currency, would it be a good idea for it to let that currency appreciate?

What are meant by ‘resource crowding out’ and ‘financial crowding out’? Why might the policies of tax cuts advocated by the CDU result in crowding out? What form would it take and why?

Compare the relative benefits of the policies advocated by the CDU and SPD to reduce Germany’s budget surplus.

Would other countries, such as the USA, benefit from a reduction in Germany’s current account surplus?

Is what ways would the USA gain and lose from restricting imports from Germany? Would it be a net gain or loss? Explain.

Economists were generally in favour of the UK remaining in the EU and highly critical of the policy proposals of Donald Trump. And yet the UK voted to leave the EU and Donald Trump was elected.

People rejected the advice of most economists. Many blamed the failure of most economists to predict the 2007/8 financial crisis and to find solutions to the growing gulf between rich and poor, with the majority stuck on low incomes.

So to what extent are economists to blame for the rise in populism – a wave that could lead to electoral upsets in various European countries? The podcast below brings together economists and politicians from across the political spectrum. It is over an hour long and provides an in-depth discussion of many of the issues and the extent to which economists can provide answers.

Podcast

Should economists share the blame for populism?Guardian Politics Weekly podcast, Heather Stewart, joined by Andrew Lilico, Ann Pettifor, Jonathan Portes, Rachel Reeves and Vince Cable (23/2/17)

Questions

Why has globalisation become a dirty word?

Assess the arguments for and against an open policy towards immigration?

In what positive ways may economists contribute to populism?

Do economists concentrate too much on growth in GDP rather than on its distribution?

Give some examples of ways in which various popular interpretations of economic phenomena may confuse correlation with causality.

Why did the proportions of people who voted for and against Brexit differ considerably from one part of the country to another, from one age group to another and from one social group to another?

In what ways have economists and the subject of economics contributed towards a growth in human welfare?

What are the advantages and disadvantages of the trend for undergraduate economics curricula to become more mathematical (at least until relatively recently)?

An agreement in principle was reached on September 30 between the USA, Canada and Mexico over a new trade deal to replace the North American Free Trade Agreement (NAFTA). President Trump had described NAFTA as ‘the worst trade deal maybe ever signed anywhere, but certainly ever signed in this country.’ The new deal, named the United States-Mexico-Canada Agreement, or USMCA, is the result of 14 months of negotiations, which have often been fractious. A provisional bilateral agreement was made between the USA and Mexico in August. At the same time, President Trump threatened a trade war with Canada if it did not reach a trade agreement with the USA (and Mexico). The new USMCA must be ratified by lawmakers in all three countries before it can come into force. This could take a few months.

An agreement in principle was reached on September 30 between the USA, Canada and Mexico over a new trade deal to replace the North American Free Trade Agreement (NAFTA). President Trump had described NAFTA as ‘the worst trade deal maybe ever signed anywhere, but certainly ever signed in this country.’ The new deal, named the United States-Mexico-Canada Agreement, or USMCA, is the result of 14 months of negotiations, which have often been fractious. A provisional bilateral agreement was made between the USA and Mexico in August. At the same time, President Trump threatened a trade war with Canada if it did not reach a trade agreement with the USA (and Mexico). The new USMCA must be ratified by lawmakers in all three countries before it can come into force. This could take a few months. Another area where the USMCA agreement has made changes concerns trade in dairy products. This particularly affects Canada, which has agreed to allow more US dairy products tariff-free into Canada (see the CNN article at the end of the list of articles below). New higher quotas will give US dairy farmers access to 3.6% of Canada’s dairy market. They will still pay tariffs on dairy exports to Canada that exceed the quotas, ranging from 200% to 300%.

Another area where the USMCA agreement has made changes concerns trade in dairy products. This particularly affects Canada, which has agreed to allow more US dairy products tariff-free into Canada (see the CNN article at the end of the list of articles below). New higher quotas will give US dairy farmers access to 3.6% of Canada’s dairy market. They will still pay tariffs on dairy exports to Canada that exceed the quotas, ranging from 200% to 300%. New NAFTA deal

New NAFTA deal The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.

Assuming there were no retaliation from other countries, jobs would be gained in the steel and aluminium industries. According to a report by The Trade Partnership (see link below), the tariffs would increase employment in these industries by around 33 000. However, the higher price of these metals would cause job losses in the industries using them. In fact, according to the report, more than five jobs would be lost for every one gained. The CNN Money article linked below gives example of the US industries that will be hit.

Assuming there were no retaliation from other countries, jobs would be gained in the steel and aluminium industries. According to a report by The Trade Partnership (see link below), the tariffs would increase employment in these industries by around 33 000. However, the higher price of these metals would cause job losses in the industries using them. In fact, according to the report, more than five jobs would be lost for every one gained. The CNN Money article linked below gives example of the US industries that will be hit. But perhaps the biggest cost will arise from possible retaliation by other countries. A trade war would compound the net losses as the world moves further from trade based on comparative advantage.

But perhaps the biggest cost will arise from possible retaliation by other countries. A trade war would compound the net losses as the world moves further from trade based on comparative advantage.