The UN’s Intergovernmental Panel on Climate Change (IPCC) has just published the first part of its latest seven-yearly Assessment Report (AR6) on global warming and its consequences (see video summary). The report was prepared by 234 scientists from 66 countries and endorsed by 195 governments. Its forecasts are stark. World temperatures, already 1.1C above pre-industrial levels, will continue to rise. This will bring further rises in sea levels and more extreme weather conditions with more droughts, floods, wildfires, hurricanes and glacial melting.

The UN’s Intergovernmental Panel on Climate Change (IPCC) has just published the first part of its latest seven-yearly Assessment Report (AR6) on global warming and its consequences (see video summary). The report was prepared by 234 scientists from 66 countries and endorsed by 195 governments. Its forecasts are stark. World temperatures, already 1.1C above pre-industrial levels, will continue to rise. This will bring further rises in sea levels and more extreme weather conditions with more droughts, floods, wildfires, hurricanes and glacial melting.

The IPCC looked at a number of scenarios with different levels of greenhouse gas emissions. Even in the most optimistic scenarios, where significant steps are taken to cut emissions, global warming is set to reach 1.5C by 2040. If few or no cuts are made, global warming is predicted to reach 4.4C by 2080, the effects of which would be catastrophic.

The articles below go into considerable detail on the different scenarios and their consequences. Here we focus on the economic causes of the crisis and the policies that need to be pursued.

The articles below go into considerable detail on the different scenarios and their consequences. Here we focus on the economic causes of the crisis and the policies that need to be pursued.

Global success in reducing emissions, although partly dependent on technological developments and their impact on costs, will depend largely on the will of individuals, firms and governments to take action. These actions will be influenced by incentives, economic, social and political.

Economic causes of the climate emergency

The allocation of resources across the world is through a mixture of the market and government intervention, with the mix varying from country to country. But both market and government allocation suffer from a failure to meet social and environmental objectives – and such objectives change over time with the preferences of citizens and with the development of scientific knowledge.

The market fails to achieve a socially efficient use of the environment because large parts of the environment are a common resource (such as the air and the oceans), because production or consumption often generates environmental externalities, because of ignorance of the environmental effects of our actions, and because of a lack of concern for future generations.

The market fails to achieve a socially efficient use of the environment because large parts of the environment are a common resource (such as the air and the oceans), because production or consumption often generates environmental externalities, because of ignorance of the environmental effects of our actions, and because of a lack of concern for future generations.

Governments fail because of the dominance of short-term objectives, such as winning the next election or appeasing a population which itself has short-term objectives related to the volume of current consumption. Governments are often reluctant to ask people to make sacrifices today for the future – a future when there will be a different government. What is more, government action on the environment which involves sacrifices from their own population, often primarily benefit people in other countries and/or future generations. This makes it harder for governments to get popular backing for such policies.

Economic systems are sub-optimal when there are perverse incentives, such as advertising persuading people to consume more despite its effects on the environment, or subsidies for industries producing negative environmental externalities. But if people can see the effects of global warming affecting their lives today, though fires, floods, droughts, hurricanes, rising sea levels, etc., they are more likely to be willing to take action today or for their governments to do so, even if it involves various sacrifices. Scientists, teachers, journalists and politicians can help to drive changes in public opinion through education and appealing to people’s concern for others and for future generations, including their own descendants.

Policy implications of the IPCC report

At the COP26 meeting in Glasgow in November, countries will gather to make commitments to tackle climate change. The IPCC report is clear: although we are on course for a 1.5C rise in global temperatures by 2040, it is not too late to take action to prevent rises going much higher: to avoid the attendant damage to the planet and changes to weather systems, and the accompanying costs to lives and livelihoods. Carbon neutrality must be reached as soon as possible and this requires strong action now. It is not enough for government to set dates for achieving carbon neutrality, they must adopt policies that immediately begin reducing emissions.

At the COP26 meeting in Glasgow in November, countries will gather to make commitments to tackle climate change. The IPCC report is clear: although we are on course for a 1.5C rise in global temperatures by 2040, it is not too late to take action to prevent rises going much higher: to avoid the attendant damage to the planet and changes to weather systems, and the accompanying costs to lives and livelihoods. Carbon neutrality must be reached as soon as possible and this requires strong action now. It is not enough for government to set dates for achieving carbon neutrality, they must adopt policies that immediately begin reducing emissions.

The articles look at various policies that governments can adopt. They also look at actions that can be taken by people and businesses, actions that can be stimulated by government incentives and by social pressures. Examples include:

- A rapid phasing out of fossil fuel power stations. This may require legislation and/or the use of taxes on fossil fuel generation and subsidies for green energy.

- A rapid move to green transport, with investment in charging infrastructure for electric cars, subsidies for electric cars, a ban on new petrol and diesel vehicles in the near future, investment in hydrogen fuel cell technology for lorries and hydrogen production and infrastructure, cycle lanes and various incentives to cycle.

- A rapid shift away from gas for cooking and heating homes and workplaces and a move to ground source heating, solar panels and efficient electric heating combined with battery storage using electricity during the night. These again may require a mix of investment, legislation, taxes and subsidies.

- Improvements in energy efficiency, with better insulation of homes and workplaces.

- Education, public information and discussion in the media and with friends on ways in which people can reduce their carbon emissions. Things we can do include walking and cycling more, getting an electric car and reducing flying, eating less meat and dairy, reducing food waste, stopping using peat as compost, reducing heating in the home and putting on more clothes, installing better insulation and draught proofing, buying more second-hand products, repairing products where possible rather than replacing them, and so on.

- Governments requiring businesses to conduct and publish green audits and providing a range of incentives and regulations for businesses to reduce carbon emissions.

It is easy for governments to produce plans and to make long-term commitments that will fall on future governments to deliver. What is important is that radical measures are taken now. The problem is that governments are likely to face resistance from their supporters and from members of the public and various business who resist facing higher costs now. It is thus important that the pressures on governments to make radical and speedy reductions in emissions are greater than the pressures to do little or nothing and that governments are held to account for their actions and that their actions match their rhetoric.

Articles

Some climate changes now irreversible, says stark UN report

Some climate changes now irreversible, says stark UN reportChannel 4 News, Alex Thomson (9/8/21)

- Climate change: IPCC report is ‘code red for humanity’

BBC News, Matt McGrath (10/8/21)

- Climate change: Five things we have learned from the IPCC report

BBC News, Matt McGrath (10/8/21)

- Climate Scientists Reach ‘Unequivocal’ Consensus on Human-Made Warming in Landmark Report

Bloomberg Green, Eric Roston and Akshat Rathi (9/8/21)

- Climate change: Seven key takeaways from the IPCC climate change report

Sky News, Philip Whiteside (10/8/21)

- IPCC report: global emissions must peak by 2025 to keep warming at 1.5°C – we need deeds not words

The Conversation, Keith Baker (9/8/21)

- This is the most sobering report card yet on climate change and Earth’s future. Here’s what you need to know

The Conversation, Pep Canadell, Joelle Gergis, Malte Meinshausen, Mark Hemer and Michael Grose (9/8/21)

- IPCC report: how to make global emissions peak and fall – and what’s stopping us

The Conversation, Matthew Paterson (9/8/21)

- World’s 1.5C goal slipping beyond reach without urgent action, warns landmark IPCC climate report

Independent, Daisy Dunne and Louise Boyle (9/8/21)

- IPCC report: 14 ways to fight the climate crisis after publication of ‘Code Red’ warning

Independent, Harry Cockburn (10/8/21)

- Major climate changes inevitable and irreversible – IPCC’s starkest warning yet

The Guardian, Fiona Harvey (9/8/21)

- Climate scientists have done their bit. Now the pressure is on leaders for COP26.

CNN, Ivana Kottasová and Angela Dewan (10/8/21)

- 21 For 21: The Climate Change Actions Scotland Needs Now

Common Weal, Common Weal Energy Policy Group (9/8/21)

- How to build support for ambitious climate action in 4 steps

The Conversation, Sarah Sharma and Matthew Hoffmann (4/3/21)

- Scientists have finally added world politics to their climate models

Quartz, Michael J Coren (9/8/21)

Report

Questions

- Summarise the effects of different levels of global warming as predicted by the IPCC report.

- To what extent is global warming an example of the ‘tragedy of the commons’?

- How could prices be affected by government policy so as to provide an incentive to reduce carbon emissions?

- What incentives could be put in place to encourage people to cut their own individual carbon footprint?

- To what extent is game theory relevant to understanding the difficulties of achieving international action on reducing carbon emissions?

- Identify four different measures that a government could adopt to reduce carbon emissions and assess the likely effectiveness of these measures.

So here we are, summer is over (or almost over if you’re an optimist) and we are sitting in front of our screens reminiscing about hot sunny days (at least I do)! There is no doubt, however: a lot happened in the world of politics and economics in the past three months. The escalation of the US-China trade war, the run on the Turkish lira, the (successful?) conclusion of the Greek bailout – these are all examples of major economic developments that took place during the summer months, and which we will be sure to discuss in some detail in future blogs. Today, however, I will introduce a topic that I am very interested in as a researcher: the liberalisation of energy markets in developing countries and, in particular, Mexico.

So here we are, summer is over (or almost over if you’re an optimist) and we are sitting in front of our screens reminiscing about hot sunny days (at least I do)! There is no doubt, however: a lot happened in the world of politics and economics in the past three months. The escalation of the US-China trade war, the run on the Turkish lira, the (successful?) conclusion of the Greek bailout – these are all examples of major economic developments that took place during the summer months, and which we will be sure to discuss in some detail in future blogs. Today, however, I will introduce a topic that I am very interested in as a researcher: the liberalisation of energy markets in developing countries and, in particular, Mexico.

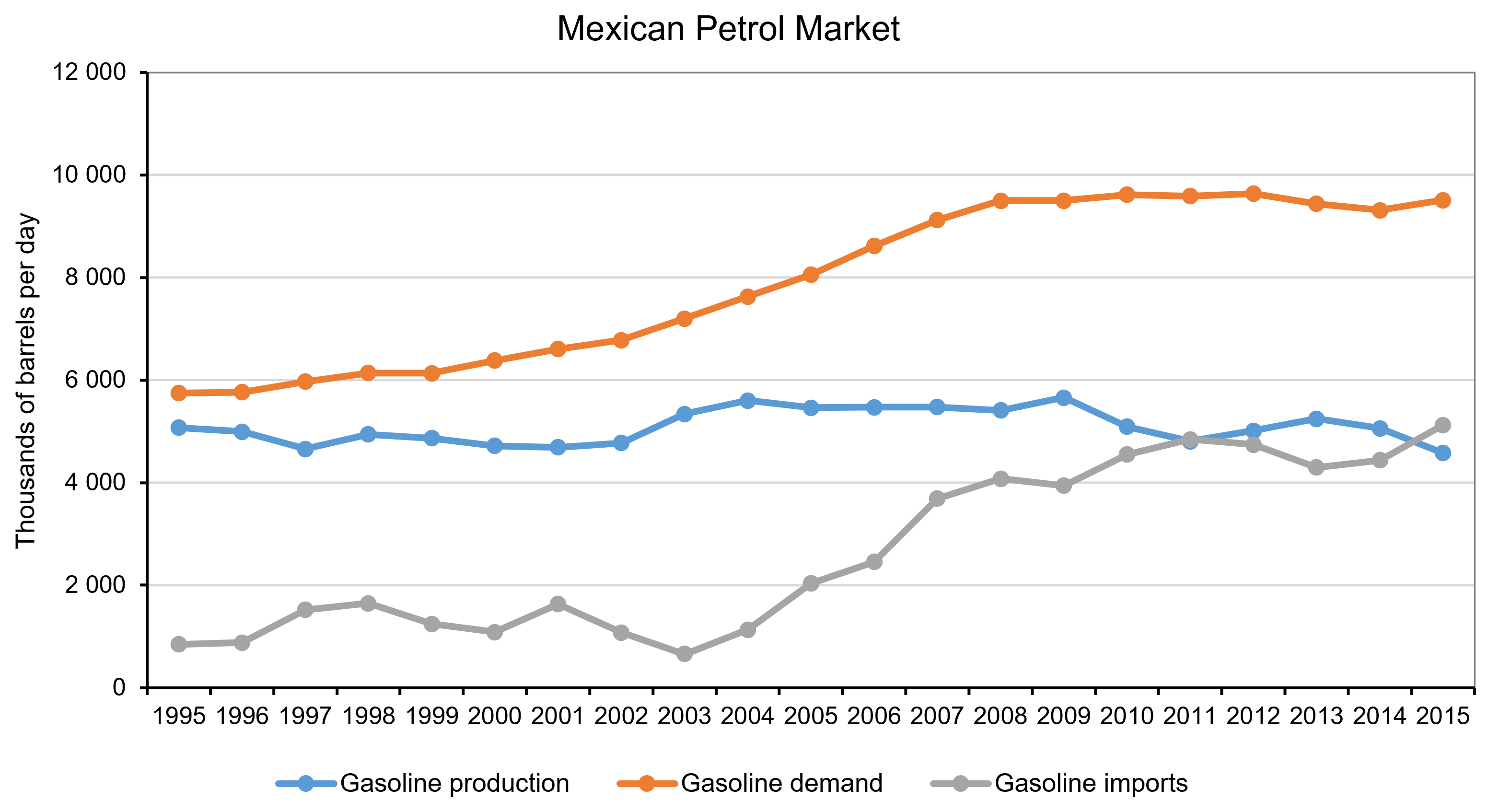

Why Mexico? Well, because it is a great example of a large developing economy that has been attempting to liberalise its energy market and reverse price setting and monopolistic practices that go back several decades. Until very recently, the price of petrol in Mexico was set and controlled by Pemex, a state monopolist. This put Pemex under pressure since, as a sole operator, it was responsible for balancing growing demand and costs, even to the detriment of its own finances.

The petrol (or ‘gasoline’) price liberalisation started in May 2017 and took place in stages – starting in the North part of Mexico and ending in November of the same year in the central and southern regions of the country. The main objective was to address the notable decrease in domestic oil production that put at risk the ability of the country to meet demand; as well as Mexico’s increasing dependency on foreign markets affected by the surge of the international oil price. The government has spent the past five years trying to create a stronger regulatory framework, while easing the financial burden on the state and halting the decline in oil reserves and production. Unsurprisingly, opening up a monopolistic market turns out to be a complex and bumpy process.

Source: Author’s calculations using data from the Energy Information Bank, Ministry of Energy, Mexico

Source: Author’s calculations using data from the Energy Information Bank, Ministry of Energy, Mexico

Despite all the reforms, retail petrol prices have kept rising. Although part of this price rise is demand-driven, an increasing number of researchers highlight the significance of the distribution of oil-related infrastructure in determining price outcomes at the federal and regional (state) level. Saturation and scarcity of both distribution and storage infrastructure are probably the two most significant impediments to opening the sector up to competition (Mexico Institute, 2018). You see, the original design of these networks and the deployment of the infrastructure was not aimed at maximising efficiency of distribution – the price was set by the monopolist and, in a way that was compliant with government policy (Mexico Institute, 2018). Economic efficiency was not always part of this equation. As a result, consumers located in better-deployed areas were subsidising the inherent logistics costs of less ‘well endowed’ regions by facing an artificially higher price than they would have in a competitive market.

But what about now? Do such differences in the allocation of infrastructure between regions lead to location-related differences in the price of petrol? If so, by how much? And, what policies should the government pursue to address such imbalances? These are all questions that I explore in one of my recent working papers titled ‘Widening the Gap: Lessons from the aftermath of the energy market reform in Mexico’ (with Hugo Vallarta) and I will be sharing some of the answers with you in a future blog.

Articles

Data

Questions

- Are state-owned monopolies effective in delivering successful market outcomes? Why yes, why no?

- In the case of Mexico, are you surprised about the complexities that were involved with opening up markets to competition? Explain why.

- Use Google to identify countries in which energy markets are controlled by state-owned monopolies.

On 15 January 2018, Carillion went into liquidation. It was a major construction, civil engineering and facilities management company in the UK and was involved in a large number of public- and private-sector projects. Many of these were as a partner in a joint venture with other companies.

On 15 January 2018, Carillion went into liquidation. It was a major construction, civil engineering and facilities management company in the UK and was involved in a large number of public- and private-sector projects. Many of these were as a partner in a joint venture with other companies.

It was the second largest supplier of construction and maintenance services to Network Rail, including HS2. It was also involved in the building of hospitals, including the new Royal Liverpool University Hospital and Midland Metropolitan Hospital in Smethwick. It also provided maintenance, cleaning and catering services for many schools, universities, hospitals, prisons, government departments and local authorities. In addition it was involved in many private-sector projects.

Much of the work on the projects awarded to Carillion was then outsourced to other companies, many of which are small construction, maintenance, equipment and service companies. A large number of these may themselves be forced to close as projects cease and many bills remain unpaid.

Many of the public-sector projects in which Carillion was involved were awarded under the Public Finance Initiative (PFI). Under the scheme, the government or local authority decides the service it requires, and then seeks tenders from the private sector for designing, building, financing and running projects to provide these services. The capital costs are borne by the private sector, but then, if the provision of the service is not self-financing, the public sector pays the private firm for providing it. Thus, instead of the public sector being an owner of assets and provider or services, it is merely an enabler, buying services from the private sector. The system is known as a Public Private Partnership.

Clearly, there are immediate benefits to the public finances from using private, rather than public, funds to finance a project. Later, however, there is potentially an extra burden of having to buy the services from the private provider at a price that includes an element for profit. What is hoped is that the costs to the taxpayer of these profits will be more than offset by gains in efficiency.

Critics, however, claim that PFI projects have resulted in poorer quality of provision and that cost control has often been inadequate, resulting in a higher burden for the taxpayer in the long term. What is more, many of the projects have turned out to be highly profitable, suggesting that the terms of the original contracts were too lax.

There was some modification to the PFI process in 2012 with the launching of the government’s modified PFI scheme, dubbed PF2. Most of the changes were relatively minor, but the government would act as a minority public equity co-investor in PF2 projects, with the public sector taking stakes of up to 49 per cent in individual private finance projects and appointing a director to the boards of each project. This, it was hoped, would give the government greater oversight of projects.

With the demise of Carillion, there has been considerable debate over outsourcing by the government to the private sector and of PFI in particular. Is PFI the best model for funding public-sector investment and the running of services in the public sector?

On 18 January 2018, the National Audit Office published an assessment of PFI and PF2. The report stated that there are currently 716 PFI and PF2 projects either under construction or in operation, with a total capital value of £59.4 billion. In recent years, however, ‘the government’s use of the PFI and PF2 models has slowed significantly, reducing from, on average, 55 deals each year in the five years to 2007-08 to only one in 2016-17.’

Should the government have closer oversight of private providers? The government has been criticised for not heeding profit warnings by Carillion and continuing to award it contracts.

Should the whole system of outsourcing and PFI be rethought? Should more construction and services be brought ‘in-house’ and directly provided by the public-sector organisation, or at least managed directly by it with a direct relationship with private-sector providers? The articles below consider these issues.

Articles

Carillion collapse: How can one of the Government’s biggest contractors go bust? Independent, Ben Chu (15/1/18)

The main unanswered questions raised by Carillion’s collapse The Telegraph, Jon Yeomans (15/1/18)

Carillion taskforce to help small firms hit by outsourcer’s collapse The Telegraph, Rhiannon Curry (18/1/18)

Carillion Q&A: The consequences of collapse and what the government should do next The Conversation, John Colley (17/1/18)

UK finance watchdog exposes lost PFI billions Financial Times, Henry Mance and George Parker (17/1/18)

PFI not ‘fit for purpose’, says UK provider Financial Times, Gill Plimmer and Jonathan Ford (6/11/17)

Revealed: The £200bn Cost Of ‘Wasteful’ PFI Contracts Huffington Post, George Bowden (18/1/18)

U.K. Spends $14 Billion Per Year on Carillion-Style Projects Bloomberg, Alex Morales (18/1/18)

Carillion may have gone bust, but outsourcing is a powerful public good The Guardian, John McTernan (17/1/18)

PFI deals ‘costing taxpayers billions’ BBC News (18/1/18)

Taxpayers will need to pay £200bn PFI bill, says Watchdog ITV News (18/1/18)

The PFI bosses fleeced us all. Now watch them walk away The Guardian, George Monbiot (16/1/18)

Carillion’s collapse shows that we need an urgent review of outsourcing The Guardian, David Walker (16/1/18)

Carillion collapse: What next for public services? LocalGov, Jos Creese (16/1/18)

Taxpayers to foot £200bn bill for PFI contracts – audit office The Guardian, Rajeev Syal (18/1/18)

Official publications

A new approach to public private partnerships HM Treasury (December 2012)

Private Finance Initiative and Private Finance 2 projects: 2016 summary data GOV.UK

PFI and PF2 National Audit Office (18/1/18)

Questions

- Why did Carillion go into liquidation? Could this have been foreseen?

- Identify the projects in which Carillion has been involved.

- What has the government proposed to deal with the problems created by Carillion’s liquidation?

- What are the advantages and disadvantages of the Private Finance Initiative?

- Why have the number and value of new PFI projects declined significantly in recent years?

- How might PFI projects be tightened up so as to retain the benefits and minimise the disadvantages of the system?

- Why have PFI cost reductions proved difficult to achieve? (See paragraphs 2.7 to 2.17 in the National Audit Office report.)

- How would you assess whether PFI deals represent value for money?

- What are the arguments for and against public-sector organisations providing services, such as cleaning and catering, directly themselves rather than outsourcing them to private-sector companies?

- Does outsourcing reduce risks for the public-sector organisation involved?

The linked articles below look at the state of the railways in Britain and whether renationalisation would be the best way of securing more investment, better services and lower fares.

The linked articles below look at the state of the railways in Britain and whether renationalisation would be the best way of securing more investment, better services and lower fares.

Rail travel and rail freight involve significant positive externalities, as people and goods transported by rail reduce road congestion, accidents and traffic pollution. In a purely private rail system with no government support, these externalities would not be taken into account and there would be a socially sub-optimal use of the railways. If all government support for the railways were withdrawn, this would almost certainly result in rail closures, as was the case in the 1960s, following the publication of the Beeching Report in 1963.

Also the returns on rail investment are generally long term. Such investment may not, therefore, be attractive to private rail operators seeking shorter-term returns.

These are strong arguments for government intervention to support the railways. But there is considerable disagreement over the best means of doing so.

One option is full nationalisation. This would include both the infrastructure (track, signalling, stations, bridges, tunnels and marshalling yards) and the trains (the trains themselves – both passenger and freight – and their operation).

At present, the infrastructure (except for most stations) is owned, operated, developed and maintained by Network Rail, which is a non-departmental public company (NDPB) or ‘Quango’ (Quasi-autonomous non-governmental organisation, such as NHS trusts, the Forestry Commission or the Office for Students. It has no shareholders and reinvests its profits in the rail infrastructure. Like other NDPBs, it has an arm’s-length relationship with the government. Network Rail is answerable to the government via the Department for Transport. This part of the system, therefore, is nationalised – if the term ‘nationalised organisations’ includes NDPBs and not just full public corporations such as the BBC, the Bank of England and Post Office Ltd.

Train operating companies, however, except in Northern Ireland, are privately owned under a franchise system, with each franchise covering specific routes. Each of the 17 passenger franchises is awarded under a competitive tendering system for a specific period of time, typically seven years, but with some for longer. Some companies operate more than one franchise.

Companies awarded a profitable franchise are required to pay the government for operating it. Companies awarded a loss-making franchise are given subsidies by the government to operate it. In awarding franchises, the government looks at the level of payments the bidders are offering or the subsidies they are requiring.

But this system has come in for increasing criticism, with rising real fares, overcrowding on many trains and poor service quality. The Labour Party is committed to taking franchises into public ownership as they come up for renewal. Indeed, there is considerable public support for nationalising the train operating companies.

But this system has come in for increasing criticism, with rising real fares, overcrowding on many trains and poor service quality. The Labour Party is committed to taking franchises into public ownership as they come up for renewal. Indeed, there is considerable public support for nationalising the train operating companies.

The main issue is which system would best address the issues of externalities, efficiency, quality of service, fares and investment. Ultimately it depends on the will of the government. Under either system the government plays a major part in determining the level of financial support, operating criteria and the level of investment. For this reason, many argue that the system of ownership is less important than the level and type of support given by the government and how it requires the railways to be run.

Articles

The case for re-nationalising Britain’s railways The Conversation, Nicole Badstuber (27/8/15)

Lessons from the Beeching cuts in reviving Britain’s railwa The Conversataion, Andrew Edwards (7/12/17)

Britain’s railways were nationalised 70 years ago – let’s not do it again The Conversation, Jonathan Cowie (1/1/18)

FactCheck Q&A: Should we nationalise the railways? Channel 4 News, Martin Williiams (18/5/17)

Britain’s railways need careful expansion, not nationalisation Financial Times, Julian Glover (5/1/18)

Right or wrong, Labour is offering a solution to the legitimacy crisis of our privatised railways Independent. Ben Chu (2/1/18)

Whether or not nationalisation is the answer, there are serious questions about the health of Britain’s railways Independent. Editorial (2/1/18)

Why Nationalising The Railways Is The Biggest Misdirect In Politics Huffington Post, Chris Whiting (5/1/18)

Questions

- What categories of market failure would exist in a purely private rail system with no government intervention?

- What types of savings could be made by nationalising train operating companies?

- The franchise system is one of contestable monopolies. In what ways are they contestable and what benefits does the system bring? Are there any costs from the contestable nature of the system?

- Is it feasible to have franchises that allow more than one train operator to run on most routes, thereby providing some degree of continuing competition?

- How are rail fares determined in Britain?

- Would nationalising the train operating companies be costly to the taxpayer? Explain.

- What determines the optimal length of a franchise under the current system?

- What role does leasing play in investment in rolling stock?

- What are the arguments for and against the government’s decision in November 2017 to allow the Virgin/Stagecoach partnership to pull out of the East Coast franchise three years early because it found the agreed payments to the government too onerous?

- Could the current system be amended in any way to meet the criticisms that it does not adequately take into account the positive externalities of rail transport and the need for substantial investment, while also encouraging excessive risk taking by bidding companies at the tendering stage?

UK productivity growth remains well below levels recorded before the financial crisis, as Chart 1 illustrates. In fact, output per hour worked in 2016 Q3 was virtually the same as in 2007 Q4. What is more, as can be seen from Chart 2, UK productivity lags well behind its major competitors (except for Japan).

UK productivity growth remains well below levels recorded before the financial crisis, as Chart 1 illustrates. In fact, output per hour worked in 2016 Q3 was virtually the same as in 2007 Q4. What is more, as can be seen from Chart 2, UK productivity lags well behind its major competitors (except for Japan).

But why does UK productivity lag behind other countries  and why has it grown so slowly since the financial crisis? In its July 2015 analysis, the ONS addressed this ‘productivity puzzle’.

and why has it grown so slowly since the financial crisis? In its July 2015 analysis, the ONS addressed this ‘productivity puzzle’.

Among the many reasons suggested are low levels of investment, the impact of the financial crisis on bank’s willingness to lend to new businesses, higher numbers of people working beyond normal retirement age as a result of population and pensions changes, and firms’ ability to retain staff because of low pay growth. While these and other factors may be relevant, they do not provide a complete explanation for the weakness in productivity.

The lack of investment in technology and lack of infrastructure investment have been key reasons for the sluggish growth in productivity. Many companies are prepared to continue using relatively labour-intensive techniques because wage growth has been so low and this reduces the incentive to invest in labour-saving technology.

Another factor has been long hours and, for many office workers, being constantly connected to their work, checking and responding to emails and messages away from the office. The Telegraph article below reports Ann Francke, chief executive of the Chartered Management Institute, as saying:

“This is having a deleterious effect on the health of managers, which has a direct impact on productivity. UK workers already have the longest hours in Europe and yet we’re less productive.”

Another problem has been ultra low interest rates, which have reduced the burden of debt for poor performing companies and has allowed them to survive. It may also have prevented finance from being reallocated to more dynamic companies which would like to develop new products and processes.

Another feature of UK productivity is the large differences between regions. This is illustrated in Chart 3. Productivity in London in 2015 (the latest full year for data) was 31.5% above the UK average, while that in Wales was 19.4% below.

This again reflects investment patterns and also the concentration of industries in particular locations. Thus London’s financial sector, a major part of London’s economy, has experienced relatively large increases in productivity and this has helped to push productivity growth in the capital well above other parts of the country.

Another factor, which again has a regional dimension, is the poor productivity performance of family-owned businesses, where ownership and management is passed down the generations within the family without bringing in external managerial expertise.

The government is very aware of the UK’s weak productivity performance. Its recently launched industrial policy is designed to address the problem. We look at that in a separate post.

Articles

UK productivity edges up but growth still flounders below pre-crisis levels The Telegraph, Julia Bradshaw (6/1/17)

Weak UK productivity spurs warnings of living standards squeeze The Guardian, Katie Allen (6/1/17)

Productivity gap yawns across the UK BBC News, Jonty Bloom (6/1/17)

The UK productivity puzzle Fund Strategy. John Redwood (26/1/17)

Productivity puzzle remains for economists despite UK growth in third quarter of 2016 City A.M., Jasper Jolly (6/1/17)

Portal site

Solve the Productivity Puzzle Unipart

Report

Productivity: no puzzle about it TUC (Feb 2015)

Data

Labour Productivity: Tables 1 to 10 and R1 ONS (6/1/17)

International comparisons of UK productivity (ICP) ONS (6/10/16)

Gross capital formation (% of GDP) The World Bank

Questions

- In measuring productivity, the ONS uses three indicators: output per worker, output per hour and output per job. Compare the relative usefulness of these three measures of productivity.

- How would you explain the marked difference in productivity between regions and cities within the UK?

- How do flexible labour markets impact on productivity?

- Why is investment as a percentage of GDP so low in the UK compared to that in most other developed countries (see)?

- Give some examples of industrial policy measures that could be adopted to increase productivity growth.

- Examine the extent to which very low interest rates and quantitative easing encourage productivity-enhancing investment.